69 Trillion: The Tokenisation Opportunity

$69 trillion: This is the estimated market cap of the US stock market, bringing the grand, global total to $130 trillion.

The opportunity to participate in equities is increasingly being considered by onchain natives, after they initially ignored it. The reasons are multiple, but the consensus was that crypto offered faster returns. However, more and more investors chose to diversify; the Wall Street Journal highlighted this trend as a rotation from Bitcoin to gold or the Magnificent Seven (MAG7).

Until recently, the crypto thesis was defined by a monogamous devotion to digital assets, accepting the cyclical contingencies where every four years, everything must mysteriously collapse; almost astrological in nature, most cryptocurrency assets had their all-time-high after Q2 2025 and have yet to come back to life. Meanwhile, equities hit new all-time highs, prompting investors to question whether loyalty to the blockchain amounts to neurosis veiled as conviction.

The entire use case of tokenisation is not “financial inclusion” or “democratising access“, but a way to allow traders to short TSLA to death, borrow against NVDA without KYC, trade pre-IPO equities or earn yield in Kamino vaults.

This article analyses three different approaches for onchain tokenisation:

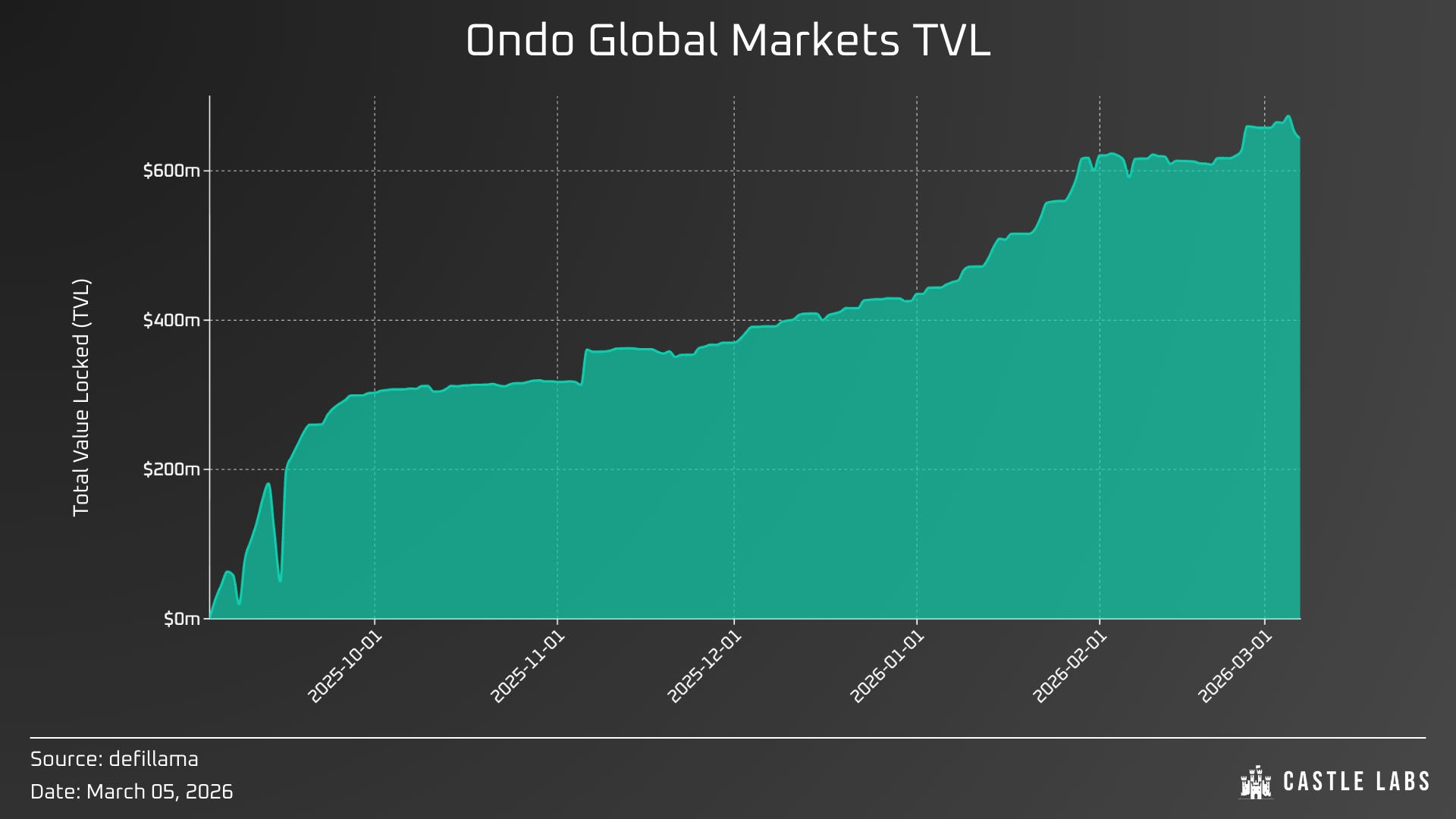

Ondo Finance launched Global Markets in September, bringing institutional-grade tokenisation to the Ethereum network.

Backed Finance’s xStocks (now owned by Kraken) debuted in June, targeting retail with multi-chain composability.

Hyperliquid activated HIP-3 in October, enabling permissionless perpetual futures on any asset, including commodities, stocks and more.

This article explores the inner workings of each protocol, focusing on how they “tokenise” assets onchain.

General considerations will be made regarding the legal contingencies underlying each protocol and their implications for investors.

Finally, we are going to explore where the broader tokenisation trend is going and what it means for the crypto ecosystem we are accustomed to.

Ondo: BlackRock Onchain

Founded in 2021 by Goldman alumni Nathan Allman and Justin Schmidt, Ondo spent years building tokenised treasury products (USDY for retail and OUSG for institutions), holding over $2 billion before launching Global Markets in September 2025. Ondo holds $2.47 billion in TVL across all products, including T-bills.

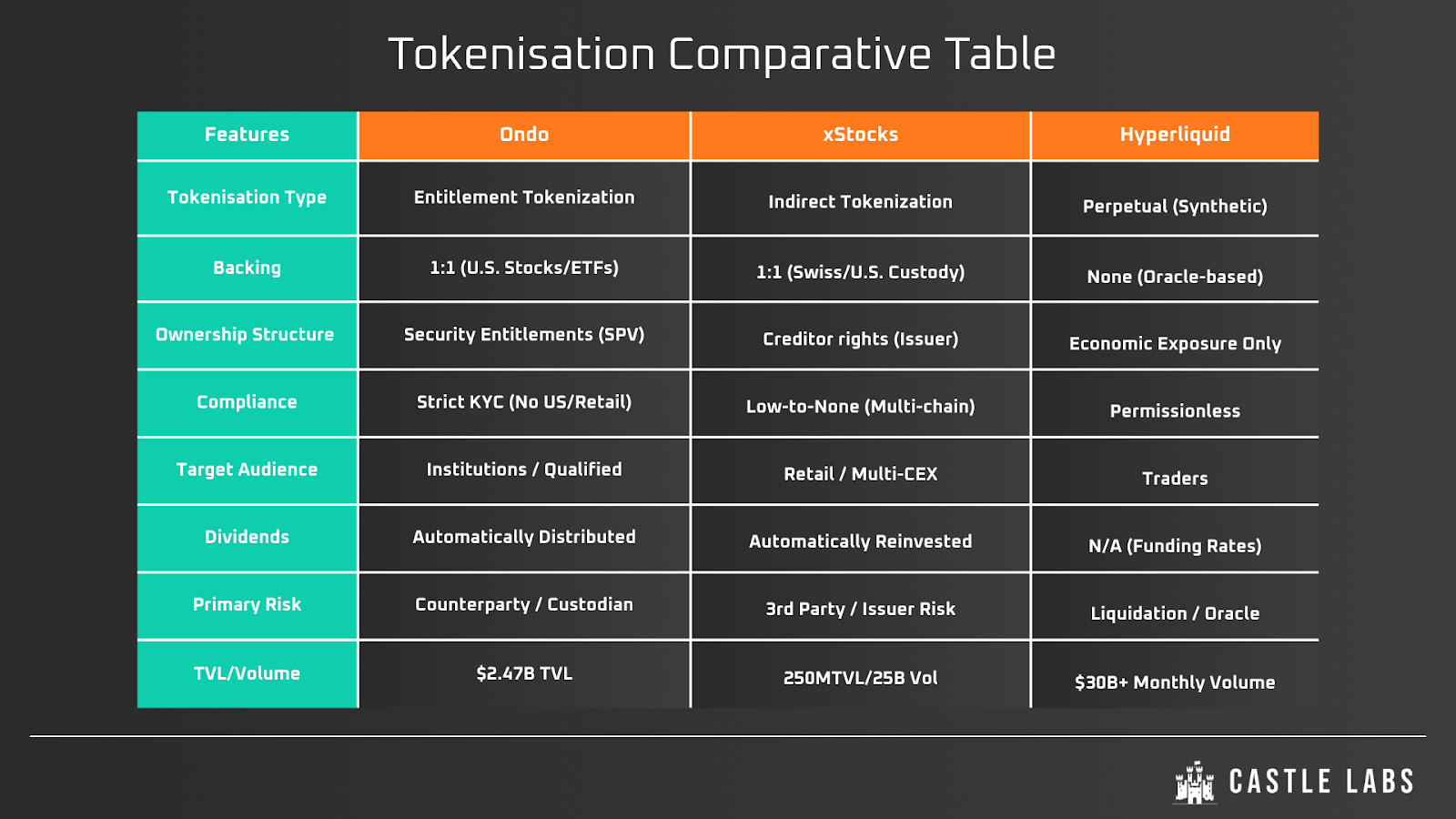

Ondo’s tokenisation model is what the industry calls indirect tokenisation. An offshore SPV purchases and holds the underlying equity on behalf of token holders, then issues onchain structured notes that pass through the economic exposure without granting legal ownership. The buyer holds a claim against Ondo’s issuing entity, secured by the underlying stock sitting in a segregated account at a US-registered broker-dealer.

Ondo tokens are debt instruments collateralised by equities, not equities themselves. There are no voting rights, for example, reserved for holders of the underlying.

The most notable features are:

Institutional-grade tokenisation with bankruptcy-remote SPVs, daily proof of reserves, US-registered custodians, and instant minting during market hours.

If Apple trades at $180 on NASDAQ, users mint AAPLon for $180 in stablecoins and redeem it instantly. Arbitrageurs keep onchain prices tight by averaging tokenised share prices across DEXs and Global Markets: The arbitrage loop is what keeps the peg in place. Ondo settles atomically: stablecoins in, token out, one transaction. If AAPLon trades above $180 on a DEX, a market maker mints new tokens on Global Markets and sells them into the market to balance the premium. If it trades below, they buy the token onchain, redeem at par, and keep the difference.

Ondo tokens are fully backed and secured by U.S. stocks and ETFs held at one or more U.S.-registered broker-dealers. Holders do not hold shares directly; they have economic exposure through tokens, whereas dividends are automatically distributed.

There are no minting or redemption fees, as Ondo profits from the spread.

The platform launched with 100+ assets on Ethereum, expanded to BNB Chain and Solana, and recently announced Ondo Chain, which adds a specific POS mechanism for staking RWAs.

The current catalogue is vast: mega-caps (AAPL, TSLA, NVDA, GOOGL), ETFs (SPY, QQQ), and commodities.

Geographic restrictions, however, are stringent: no US persons or residents are permitted. Ondo tokenised stocks are available only to qualified investors, and KYC is mandatory.

The tokenisation process deserves attention because each protocol has its own alchemy.

Alpaca, the US-headquartered self-clearing broker-dealer, now custodies over 94% of all tokenised US equities and ETFs by value, including Ondo’s. Its Instant Tokenisation Network provides the in-kind minting and redemption rails, meaning the underlying stock is journaled between brokerage accounts rather than liquidated into cash and re-bought, eliminating slippage and keeping token prices stable. Ondo also recently filed a registration statement with the SEC; once effective, it would make Global Markets the first issuer of transferable tokenised stocks subject to SEC reporting requirements. The SEC closed its two-year investigation into Ondo in November 2025 without recommending charges, and the protocol subsequently acquired Oasis Pro Markets, an SEC-registered broker-dealer, to accelerate its domestic ambitions.

Ondo believes that institutions care more about regulatory clarity and operational efficiency than ideological purity.

xStocks: Retail’s Best Friend

xStocks occupies a sweet spot between crypto and TradFi: More accessible than Ondo, more compliant than HIP-3, open to all.

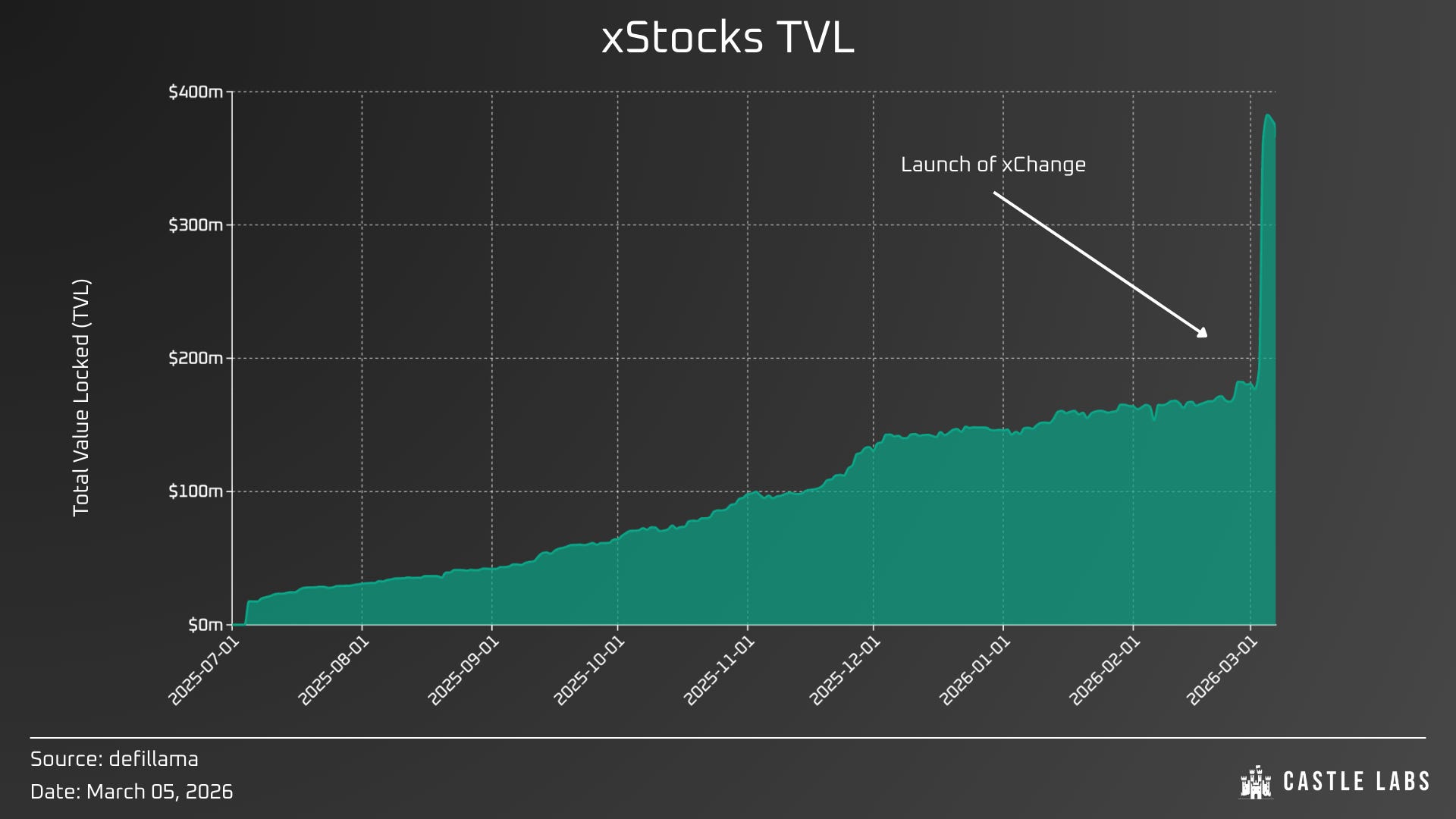

Launched in June 2025, xStocks offers 60+ tokenised equities and ETFs, each backed 1:1 by securities held in Swiss/US custodians under Swiss regulatory oversight. Tokens are SPL/ERC-20, freely transferable across chains.

Its timely success prompted Kraken to buy Backed in 2025. xStocks now holds $250 million in public equities, with Tesla accounting for more than a quarter of that figure.

In this specific model, token holders don’t own shares; they hold creditor rights against the issuer. Each xStock is backed 1:1 by underlying equity; dividends are automatically reinvested, following Ondo’s model: When the underlying equity distributes a dividend, holders receive additional xStock tokens airdropped to their wallet, equal in value to the dividend amount.

The tokenisation mechanism mirrors traditional structured finance compressed onto blockchain. Legally speaking, each xStock is a tracker certificate, classified as a bearer debt instrument, issued by Backed Assets Limited, a Jersey-domiciled SPV and wholly owned subsidiary of Backed Finance AG in Switzerland. The token’s financial value tracks a specific underlying equity or ETF, but grants no ownership or voting rights. Token holders are creditors of the issuer, not shareholders of the underlying company. This is the same indirect tokenisation model as Ondo, but the legal architecture and post-issuance mechanics are different.

The issuance works as follows:

An authorised participant (AP) submits a mint request through Alpaca’s API, specifying the ticker, quantity, target blockchain, and wallet address.

Alpaca, acting as the US-headquartered self-clearing broker-dealer, validates the request and records the corresponding shares from the AP’s brokerage account into the issuer’s account.

Once Backed confirms receipt of the underlying security, the equivalent xStock tokens are minted onchain and delivered to the AP’s wallet.

Redemption works in reverse: the AP burns the tokens, Alpaca confirms the burn, and the underlying shares are recorded back. This is an in-kind process which keeps the token price tethered to the underlying equity.

On March 5th, xStocks unveiled xChange, a swap engine designed to siphon capital-market liquidity directly into DeFi during trading hours while maintaining onchain liquidity pools for weekend price discovery.

The system has three components:

Onchain liquidity for off-hours price discovery.

xChange itself connects DeFi and TradFi during market hours.

xPort for porting assets onchain.

Powered by Chainlink oracles, xChange is already live on Solana aggregators and launching on CoW Swap and 1inch on Ethereum, with integrations with PancakeSwap, LiFi, DFlow, and Kamino Swap in the works.

The vertical effect is that offchain liquidity gets siphoned into the blockchain through arbitrage, tightening spreads in onchain pools; horizontally, it opens access to the long tail of xStocks without requiring pre-seeded liquidity for every ticker.

The regulatory wrapper spans three jurisdictions:

The issuer sits in Jersey, regulated by the Jersey Financial Services Commission under the Control of Borrowing Order

The prospectus is approved by the FMA in Liechtenstein, making the tokens passportable across the EU

The tokenisation itself is carried out by Backed Finance AG in Switzerland.

Collateral is held in segregated accounts at regulated custodian banks in both Switzerland and the US (InCore Bank and Maerki Baumann among them), governed by a three-party Account Control Agreement: if token holders’ rights are breached, a security agent can seize the collateral accounts.

The distribution is aggressive, with shares available on Kraken, Bybit, Gate and other CEXs. Kraken offers instant settlement, fractional investing ($1 minimum), and competitive fees (0.1% taker, -0.02% maker rebate).

Unlike Ondo, the concept is to onboard retail where they are found. There are no specific KYC or whitelisting requirements, as anyone can buy shares and freely transfer them between self-custody wallets.

On the 25th of February, xStocks achieved $25 billion in volume.

Kraken named Alpaca its preferred partner for sourcing/custodying underlying equities 1:1. Alpaca’s Instant Tokenisation Network provides real-time minting and redeeming for institutions. At the beginning of February 2026, the Deutsche Börse-owned 360X platform started offering xStocks to its clients! The BaFin and ESMA regulate this exchange, the gold standard for Europe.

The idea behind xStocks is that retail cares more about self-custody and multi-chain access than institutional-grade custody. Naturally, retail desires the same weapons available to institutions; tokenising stocks is a first step to fill the chasm of informational asymmetry: now, anyone can listen to the earnings call and immediately dump or buy before the market opens.

Hyperliquid: Anything Goes

An altogether entirely different model has been promoted by Hyperliquid, where tokenisation is reduced to its bare minimum: instead of an economic exposure, traders long or short derivatives, and nothing more.

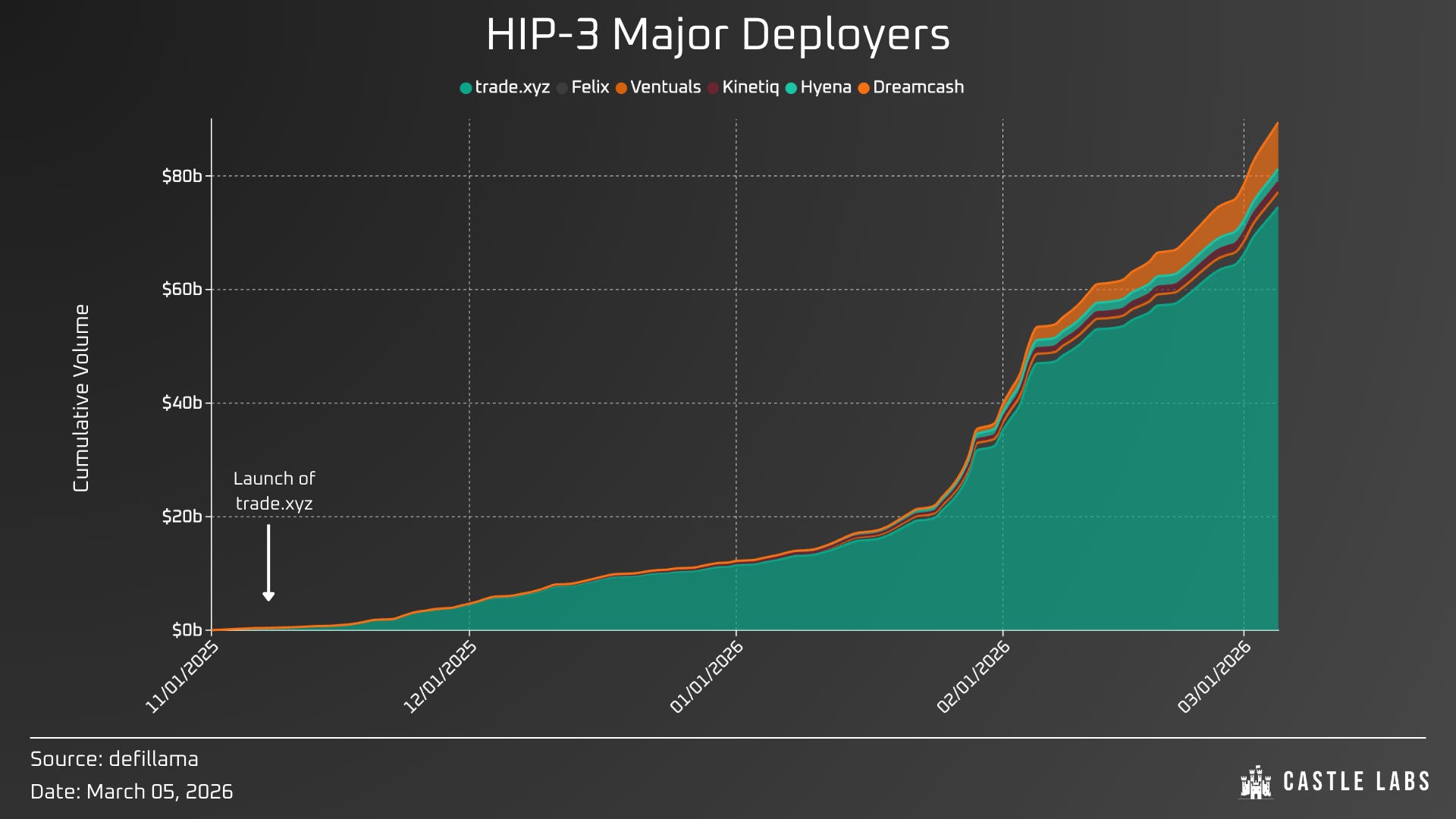

HIP-3, activated in October 2025, lets anyone staking 500,000 HYPE launch their own perp exchange on HyperCore. The deployer sets the oracle, defines leverage, manages risk, and earns 50% of fees.

The mechanics here are fundamentally different. In the Ondo and xStocks model, there is an actual stock sitting in a custodial account; the token is a structured claim on that stock, and when a holder burns it, the share is sold. The chain of custody looks like this:

NASDAQ → broker → SPV → blockchain.

In Hyperliquid’s model, none of that exists. HIP-3 markets are isolated-margin, not listed on Hyperliquid’s main frontend, and distributed entirely through third-party builders who choose which markets to offer. The oracle is the critical variable: each deployer selects its own pricing source and defines what happens off-hours, when US markets are closed, but the perp trades 24/7. During off-market hours, the exchange relies on EMA-smoothed internal pricing, protocol clamps, and specific trust tiers based on the assets’ liquidity depth.

This is not tokenised equity, like Ondo’s Global Market. There are no shares, no dividends, no redemption, no SPVs, only contracts that track price via an oracle, settled in stablecoins or HYPE.

XYZ100, deployed by trade.xyz tracks the “value of a modified capitalisation-weighted index of 100 large non-financial companies listed on a U.S. exchange.” It hit $72 million daily volume and $55 million open interest within two weeks, breaking into Hyperliquid’s top 10; it now averages billions in monthly volume.

Hyperliquid’s edge is decentralised market creation. Any builder meeting the 500K HYPE requirement deploys three markets free; additional markets require a Dutch auction.

This creates niche explosions:

trade.xyz (XYZ100, NVDA, TSLA, AAPL, GOOGL)

Ventuals (pre-IPO SPACEX perps)

Felix (USDH collateral, 20% lower taker fees)

Kinetiq, a liquid staking protocol with more than a billion dollars of monthly volume

Through HIP-3, Hyperliquid becomes AWS for perpetuals: instead of competing with every market, they provide infrastructure and let builders compete.

AWS rents users compute, storage, and networking, and users build whatever they want on top. Hyperliquid does the same with financial infrastructure:

HyperCore provides the order book, the margining engine, and the settlement layer.

The deployer decides what asset to list, which oracle to use, what leverage to permit, and how to manage risk.

The protocol is indifferent to whether the market tracks Tesla, pre-IPO SpaceX, gold, or a basket of GPU manufacturers. It collects its 50% fee share regardless. This is a fundamentally different business model from Ondo or xStocks, which must individually structure, custody, and legally wrap every single asset they tokenise. Hyperliquid delegates those functions to builders and adopts a laissez-faire approach to tokenisation.

The current meta is highly favourable to perp DEXs, and the volume is not decreasing at all in 2026. Crypto speculators care more about leverage and accessibility than ownership rights, but, as explained above, this is partly because the culture has yet to change, and accessibility was poor until tokenisation emerged in recent years.

The risk, however, is far more important than in tokenised equities. Oracle failures during periods of high volatility or off-market hours, liquidations, or MMs pulling off to avoid drawdowns can lead to an absolute loss. Unlike tokenised stocks, once a position is liquidated, the capital is lost and cannot be recovered.

Institutional desks require auditable counterparties and regulatory clarity on the classification of derivatives, while HIP-3 offers neither. For a fund with compliance obligations, trading an equity perp on Hyperliquid would raise immediate questions from auditors and risk committees, especially concerning ISDA compliance. Hyperliquid’s current user base is mostly retail, as it focuses on public access; however, there are signs that this is changing. Ripple has integrated Hyperliquid into its institutional prime brokerage platform Prime, providing clients with access to perps; another sign of the times. The availability of Hyperliquid gold, silver and oil markets during the Iran strikes on the weekends is increasingly an argument to become a key benchmark for tokenised asset prices during off-market hours.

Tokenise It All

Hyperliquid proved that decentralised protocols can and will compete with legacy exchanges.

Others are following suit. Binance relaunched tokenised stocks on February 24, 2026, partnering with Ondo to list 10 tokenised US equities and ETFs on Binance Alpha. This is their first tokenised stock offering since shutting down the service in July 2021, following FCA and BaFin questions about their compliance, which led to a series of unfortunate events for CZ.

The current US market exclusion is another point of contention. The moment the SEC approves domestic tokenised securities (and they will, as post-GENIUS Act momentum is not slowing), the onchain RWA sector will explode. If cryptocurrencies are bleeding to death, equities only go up, whether public or not.

The real competition is between whoever controls the infrastructure when US approval is official.

Hyperliquid is not competing with xStocks and Ondo in any direct sense; it serves a fundamentally different function. Ondo and xStocks provide economic exposure to equities, with tokens backed by real shares, dividends reinvested, and a redemption mechanism tied to the underlying. The backbone is access: holding, lending against, and composing with assets that were previously accessible only on Schwab or Interactive Brokers. Hyperliquid’s HIP-3 provides leverage and speculation: a synthetic contract that tracks the price, with no claim on any asset, no custody chain, and no creditor rights. In a way, this is the apex of financial freedom, where anyone with a wallet and some dollars can access almost anything, immediately.

For retail, the choice should not be a dilemma, as each alternative yields a different outcome. A trader might hold xTSLA in a self-custody wallet as a medium-term position while simultaneously shorting TSLA-USDC on Hyperliquid to hedge a potential grim earnings call, like many traders arbitrage between Polymarket, pre-markets, OTC points platforms, etc.

One is a long-run portfolio allocation, the other is a trade. The confusion arises because both are accessed through crypto wallets, denominated in stablecoins, and marketed under the umbrella of “tokenised equities.” But the comparison is skewed: xStocks and Ondo carry issuer and custodial risk (the SPV must remain solvent and the collateral must stay segregated), while Hyperliquid carries oracle and liquidation risk (the price feed must remain accurate, the margin must stay healthy, or the position is gone permanently). So, despite a common idea, each protocol cannot reasonably be compared to the others.

What Hyperliquid does better than either is speed and flexibility. The permissionless nature of HIP-3 means the market itself is the product, seeing as any asset with an oracle feed can have a perp within hours, not the months of legal structuring required for tokenised equity issuance.

Three hardly comparable protocols, each pursuing a very specific niche, for everyone to be satisfied: competition between them is illusory.

This is ultimately a discussion about choice, self-agency and inventiveness.

written by @TradFiHater ✍️

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram guy, you can read all of our research without the noise on our TG channel: