A New Crypto Era: From Gambling to Investing

Its 2026 and crypto is not just about gambling anymore.

2026 has not been a great start for crypto. The majority of assets are down in price; BTC reached its all-time high six months ago and has since been in a constant drawdown. There has been no bullish news recently, constant ETF outflows, a loss of interest in crypto, businesses shutting down, VCs not actively investing, and it seems like the well of opportunities crypto once had is drying up.

While all of this is true and there is no positivity in it, we are moving towards a major shift in which tokens that have no connection to protocol revenue will plummet in value, and those with no revenue will fail to survive. The land of rugs is turning from “Gambling” to “Investing”.

The event that accelerated this shift was the October Liquidation Event, followed by a series of macro events, such as gold outperforming Bitcoin, which left us asking whether crypto is investable anymore and whether it has the upside that attracted many people in the first place.

This piece highlights the same shift and its effects on cryptocurrency assets and the investment models that underlie them

From Gambling to Investing

Crypto has gone through its phases, including the initial discovery phase, when it was tech for nerds, and no one saw its use cases; the extreme speculation during the ICO boom; regulatory disregard; huge blowups like the Luna Crash and FTX; and the current era, where institutions are stepping in.

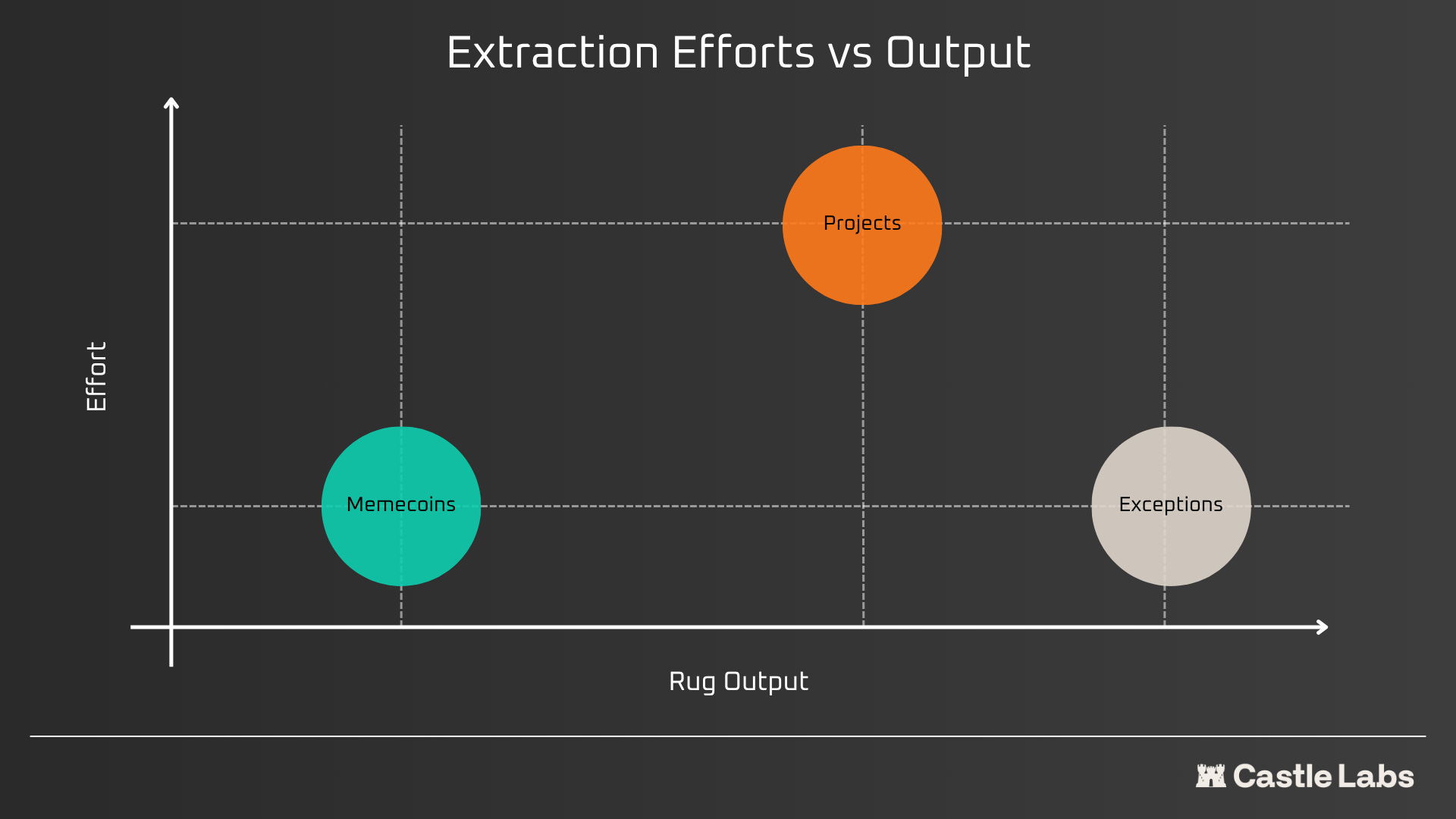

For a long time, crypto has run on an extraction-first approach and has set a norm of gambling rather than investing. Launches and successes of products like pumpdotfun that let users create memecoins with just a click validate that crypto has always been a gambling bubble where new users come in hoping to make big. The crypto extraction approach can be classified into three classes:

Low Effort Low Output (Memcoins)

High Effort High Output (Scam Projects and Slow Rugs)

Low Effort High Output (Celebrity Coins)

At one end of the spectrum lie the simple extraction methods that have worked quite well so far and will also work in the future, but might slow in rate: memecoins. Memecoins are easy to launch; they don’t need to be explained to anyone why this coin was launched or what its utility is, because making money with them rests on a single principle: exiting the trade before others. Whoever trades memecoins is aware of this, and in some cases they deserve to lose their money, cause that’s how the market works. On the other hand, come the projects that overpromise, hype themselves up, and do a slow rug. There are a few exceptions as well that are just our low-effort and extract the most, for example, the celebrity coins.

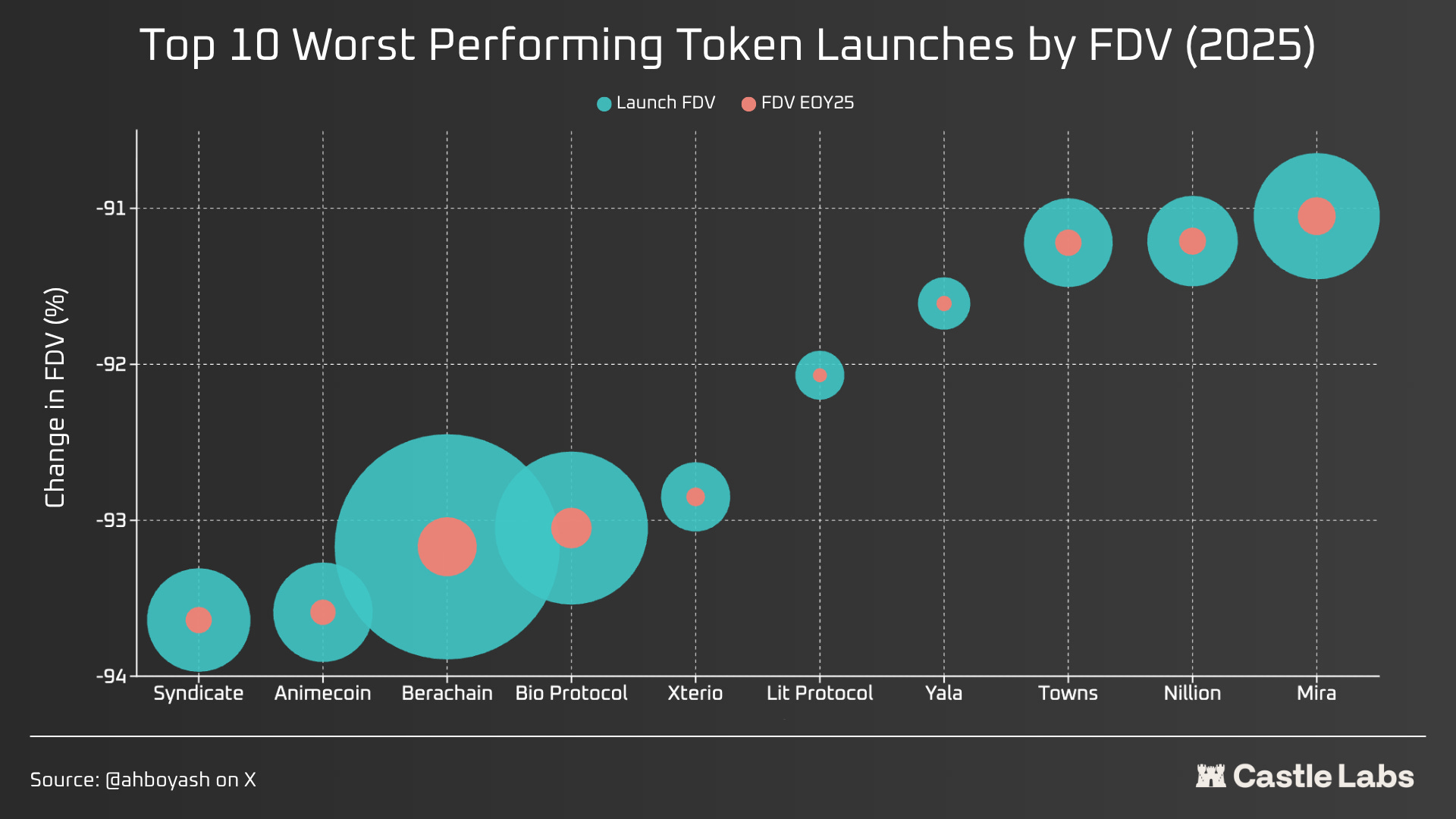

Taking last year’s TGEs as an example, most can be categorised as bad investments, as they closed the year with significant losses for their tokenholders. Reasons for them being down could be bad tokenomics, launching at a ballooned valuation (mostly), market and project sentiment, and much more.

For a long time, crypto projects focused on building the best tech possible, but never on achieving product-market fit (PMF), which is why we have tech no one uses. But as of 2026, things seem to be changing, and the extraction-first approach of crypto seems to be taking a back seat as institutions move onchain. They want to use the infrastructure crypto built over several years, but their arrival comes with a huge caveat that they don’t want to do anything with the tokens we produced in our way to build the tech; they like the code and infrastructure, they will use it, but that wouldn’t have a positive impact on the majority of the assets.

Some time back, the NYSE shared that it would use blockchain infrastructure to support 24/7 trading. Robinhood has begun testing its L2, built on the Arbitrum Stack, to tokenise equities and ETFs, allowing users to hold “Stocks” in self-custody wallets. BlackRock’s BUIDL and Franklin Templeton’s Benji are great RWA products onchain. All of this enables instant settlement, a problem that TradFi has faced for years due to the limited trading period.

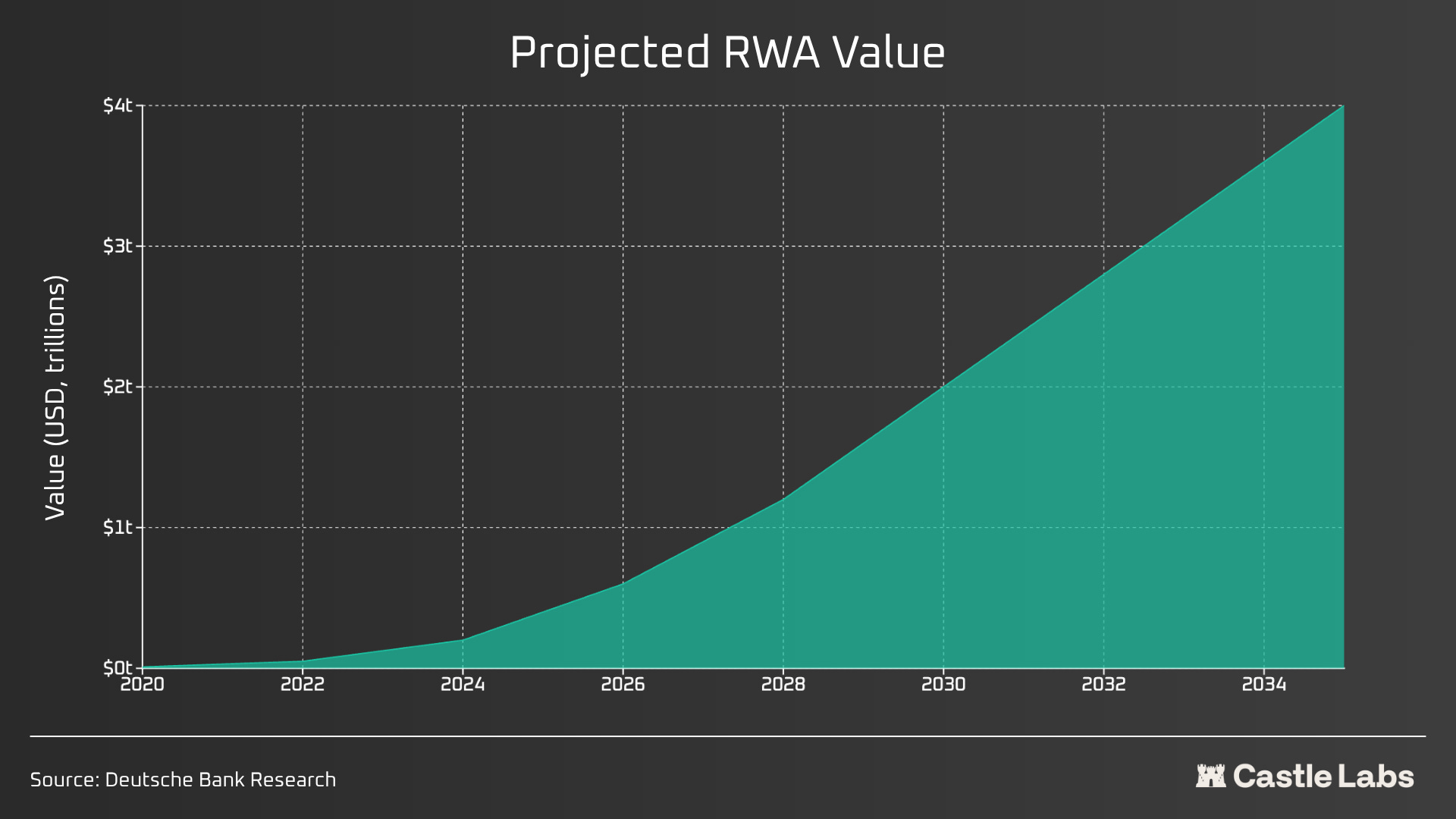

Coming to RWAs, they are projected to go into the trillion-dollar league in the next few years. Private Credit, public equities, and short-term U.S. tokenised debt are growing onchain; one can leverage trade commodities and equities on platforms like Hyperliquid and Ostium, and these stats keep on going up.

Everyone is coming onchain because these are the rails which can take finance to the next level. The dream of the complete adoption of decentralised finance becomes a reality as institutions and every retail user use the same rails we use today, enabling transparency, faster settlement, no delays, and greater control over funds.

The apps that have built a strong foundation will still thrive in this new age. The incumbents in Lending, like Morpho, Aave, and a few others, will continue to dominate as they have been battle-tested during the worst drawdowns, have performed well across them and have continuously innovated. Furthermore, protocols like Hyperliquid are becoming one of the deepest sources of onchain liquidity while enabling leveraged trading in public equities and commodities. As institutions grow, they need venues that can accommodate their size.

Oracle networks, crosschain interoperability stack, L2/L1 scaling, and token standards are what will matter. Obviously, there are no surefire assets that will deliver the best returns when institutions go all-in on the onchain rails, but those with a solid track record are not going anywhere and will find their way into use by both institutions and retail investors.

Revenue is the King

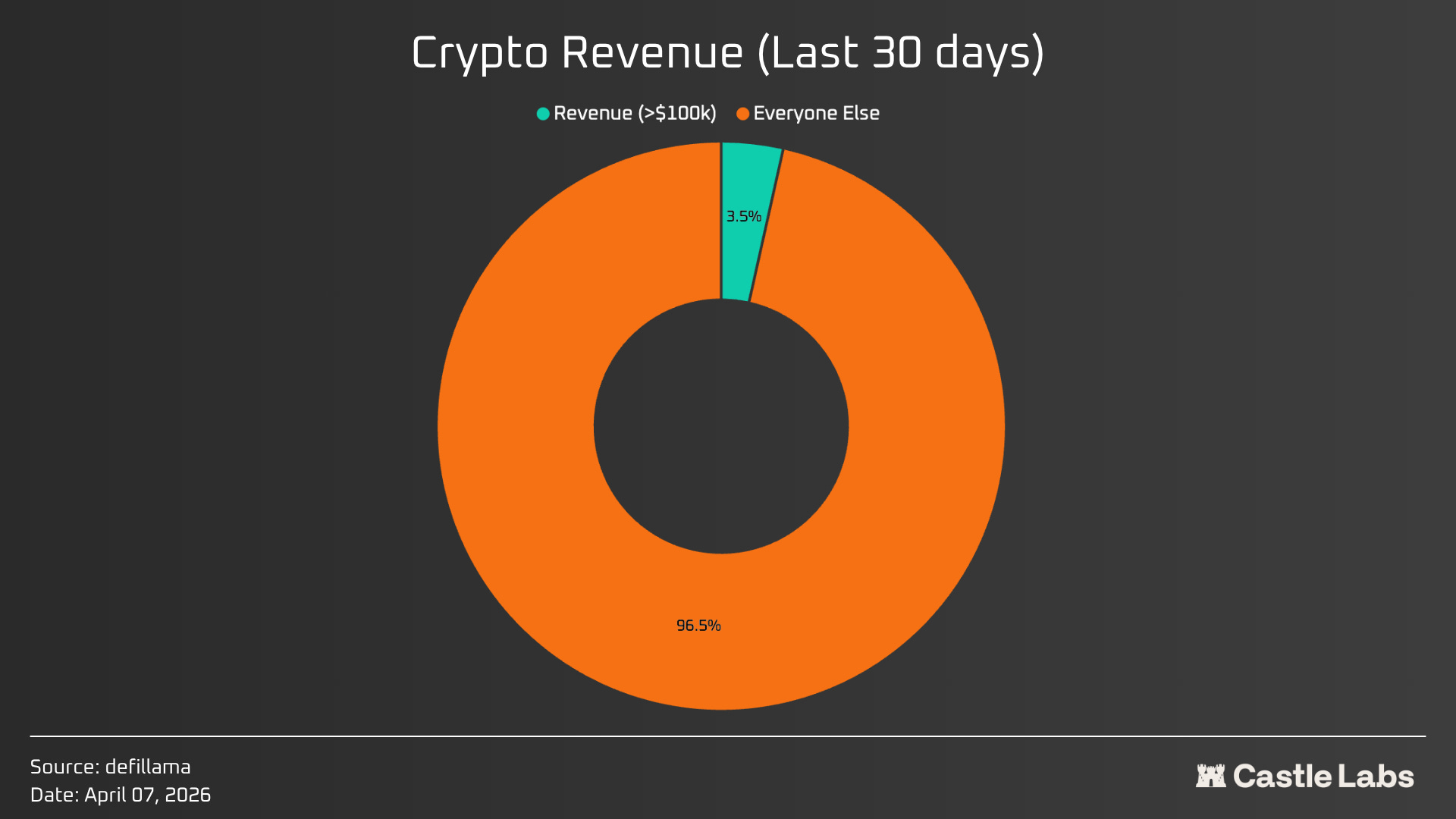

There are over 17000 tokens listed on Coingecko.

Around 5,700 protocols on DeFillama; if we include protocols that generated >$100k in revenue in the last 30 days, we get ~200 protocols or products, which is 3.5%. The investable pool of crypto is smaller than anyone would expect. Most of the tokens are uninvestable.

If I were to crunch these numbers more realistically, I would consider holder revenue. The revenue that goes back to holders in any form. It’s surprising that only ~50 protocols did over $100k in holders revenue in the last 30 days, that’s <1% of the total protocols listed on Defillama.

Increasing these benchmark numbers is fair, maybe to a million dollars a month, because most tokens trade at hundreds of millions and even billions of dollars.

If we were to dive into the issue of lower token holder revenue, it stems from the alignment issue crypto has always had and from the token structure. There are always two entities related to a project: Labs and the DAO/tokenholders. Labs are the “team” in tokenomics; they are the project’s initial developers, and they raise funds by selling a portion of their company and issuing tokens to investors at an early stage, in exchange for funds they use to grow the business. Tokens are not a legal representation of the business and don’t offer any actual rights over the company’s profits, unlike equity. Investors who receive tokens have these rights through the equity they hold. But token holders are usually at the project’s mercy when it comes to aligning their product with their token.

But over the last year, things have started to change, and people are betting less on speculative plays and focusing more on how much the protocol actually makes. This single shift will take crypto where years of an extraction-first approach couldn’t.

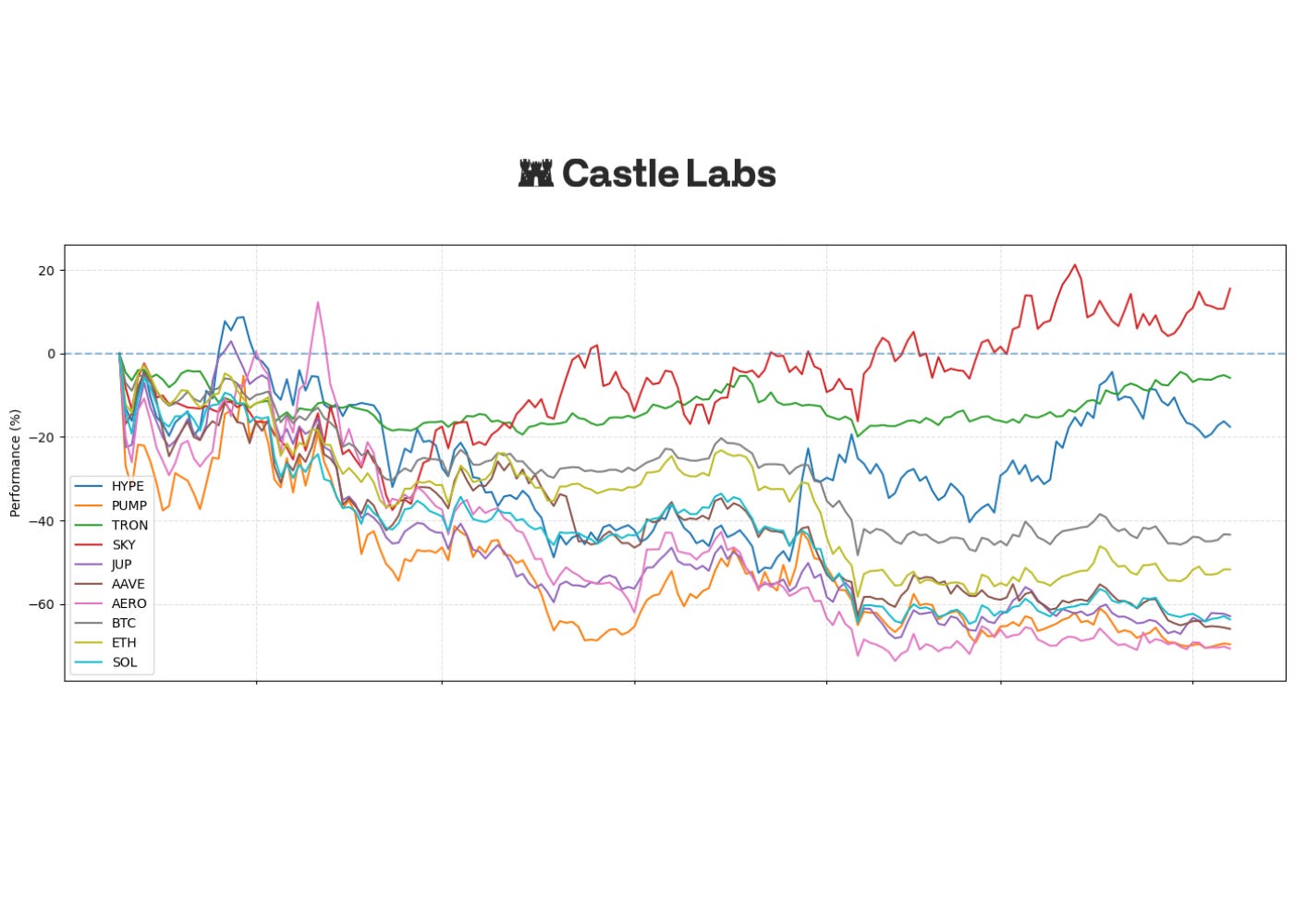

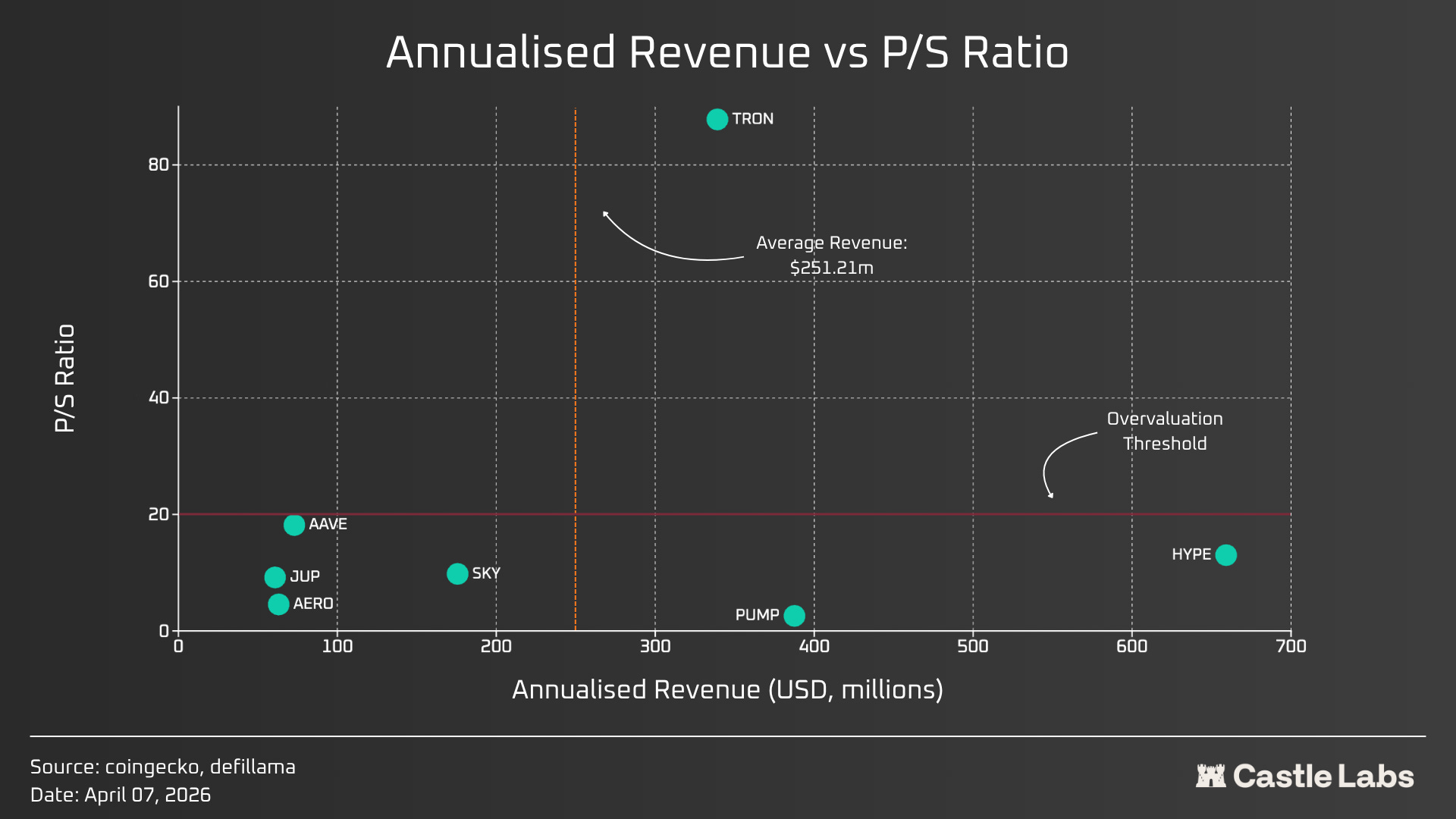

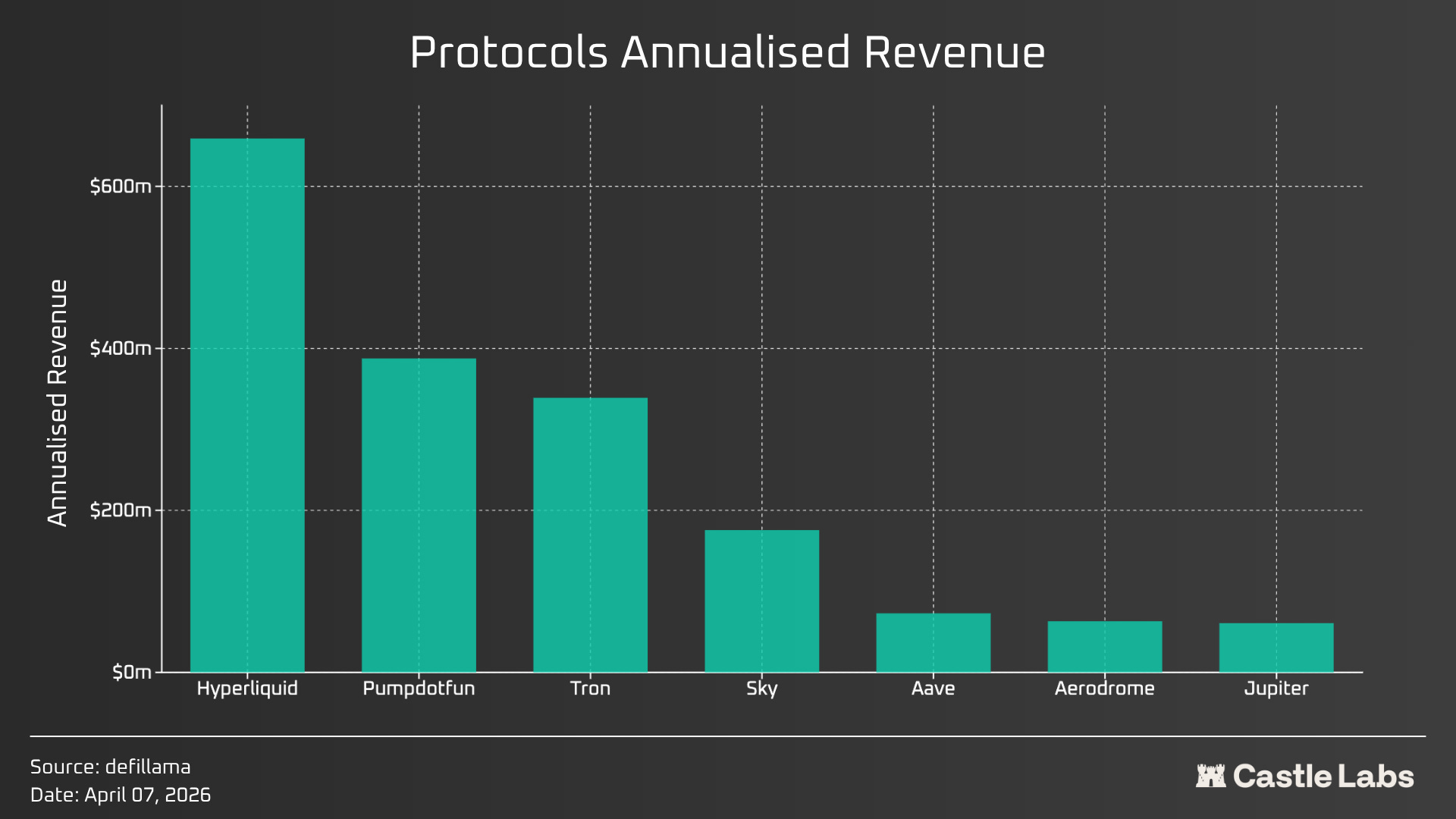

Below, we discuss some key metrics every crypto investor should consider when analysing the token. We analyse the top revenue-generating token protocols over the last 30 days, including Hyperliquid (HYPE), Pumpdotfun (PUMP), Tron (TRON), Sky (SKY), Jupiter (JUP), Aave (AAVE), and Aerodrome (AERO).

Price-to-Sales Ratio

The Price-to-Sales (P/S) ratio is calculated by dividing the protocol’s market capitalisation by its annualised revenue. P/S serves as a gauge of how much the market is willing to pay for every dollar of revenue generated. The premium reflected in this ratio indicates how much users value the protocol’s future capabilities and growth factors.

We compared some of the top revenue-making protocols and their tokens based on their annualised revenue and P/S ratio. We took the revenue for the last 30 days and multiplied it by 12 to get the annualised revenue figures. The result we get is visualised below.

The overvaluation threshold is set at 20, based on the top U.S. public equities’ P/S ratios. Most protocols are around or below this threshold, except Tron, which trades at a much higher ratio than the others. Another threshold we considered is revenue, for which we used the average annualised revenue of the protocols discussed, amounting to ~$250 million. Only three protocols, Pumpdotfun, Hyperliquid, and Tron, exceed this threshold and together account for ~80% of the revenue among the mentioned protocols

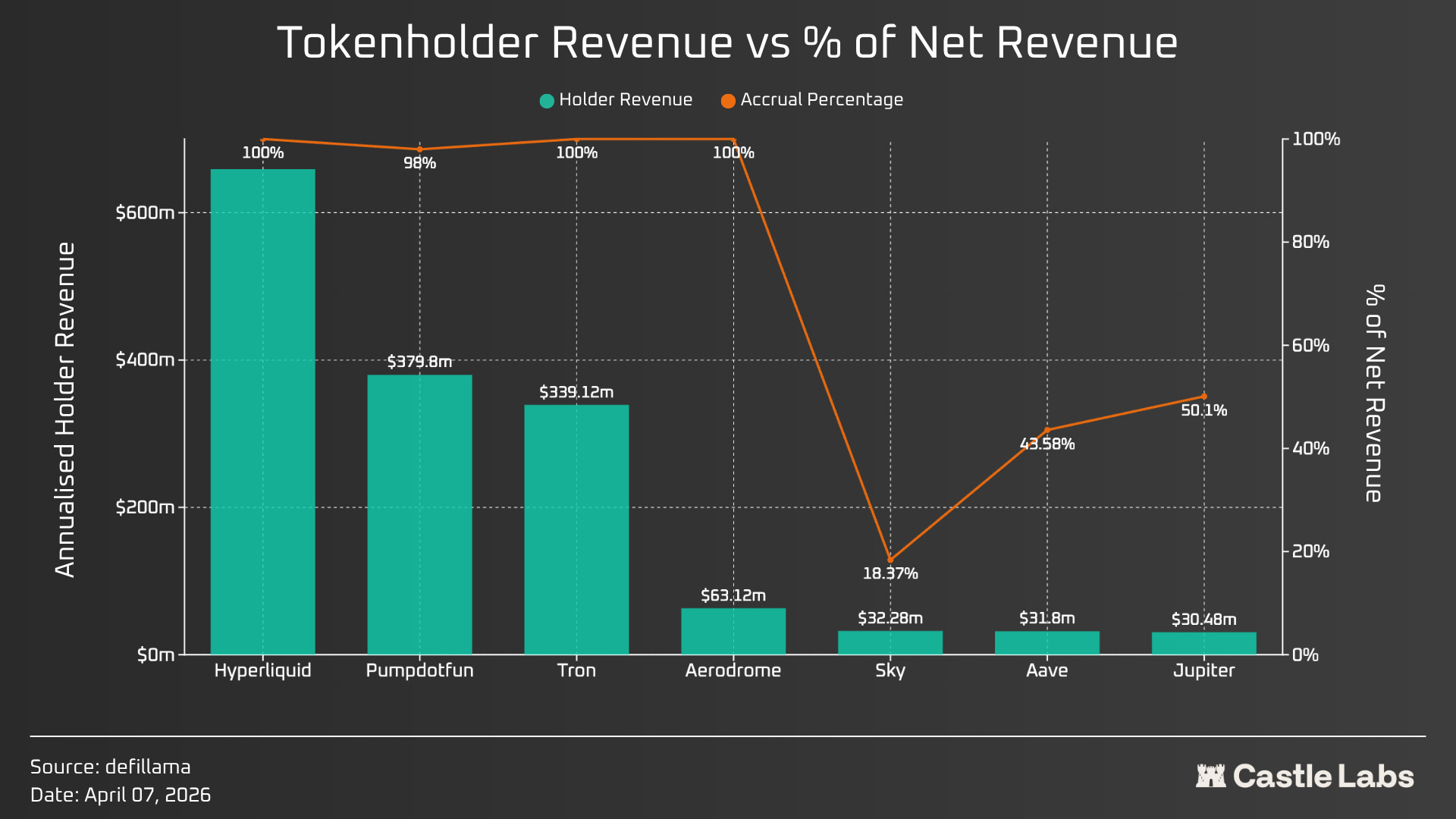

Token Holder Revenue

The next important factor we discuss is the token holder revenue. This largely depends on the protocol’s revenue and how much of it is actually returned to tokenholders through buybacks, token burns, and staking rewards. It is a famous metric now, and everybody has been talking about it, and it holds more importance than the actual revenue because this is how the token accrues value.

We have once again classified protocols by holders’ revenue over the last 30 days and multiplied it by 12 to obtain the yearly estimates. At a glance, we can see most protocols are playing pretty fairly with their holders and using most, if not all, of the revenue to accrue value for their tokens.

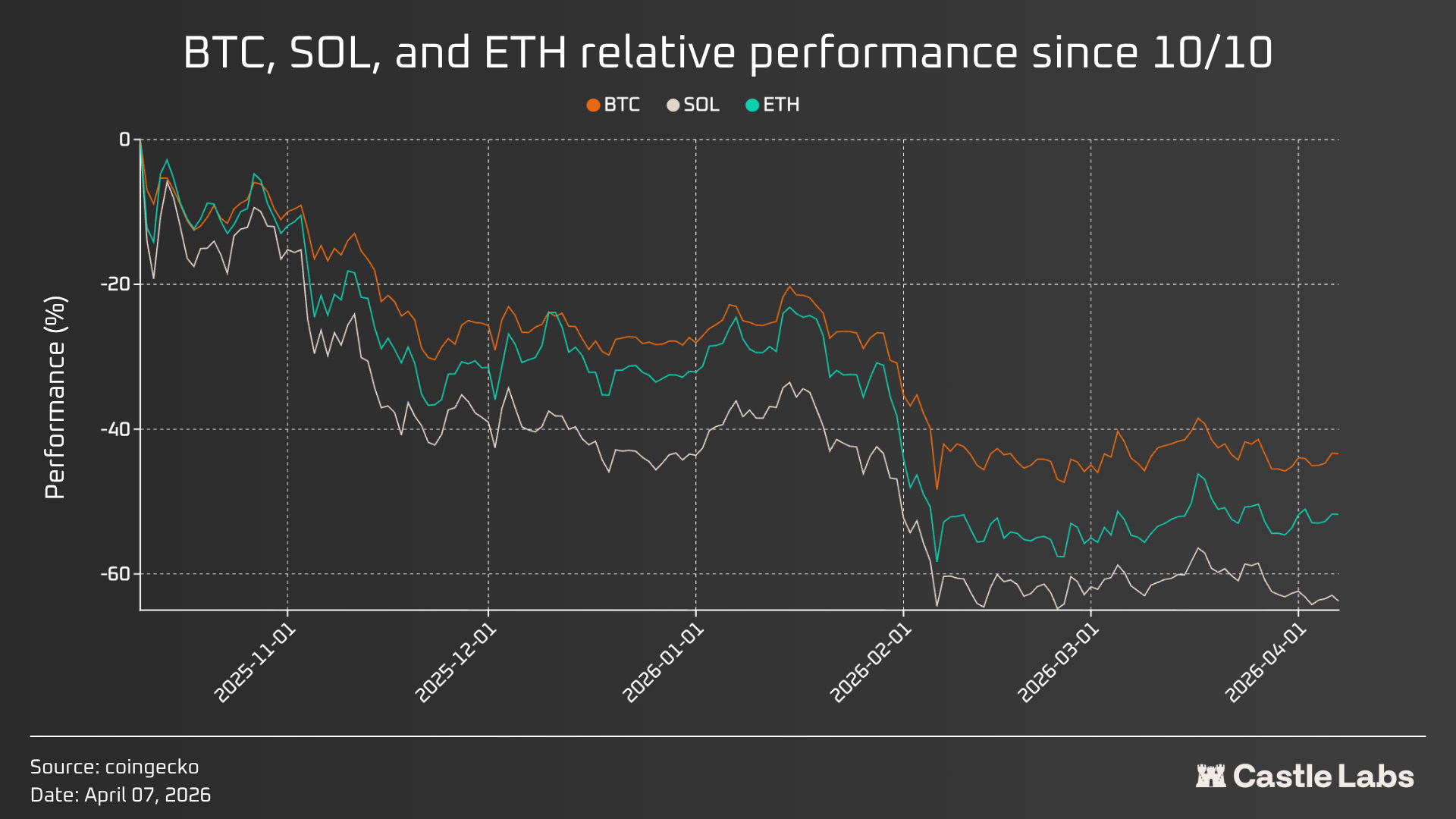

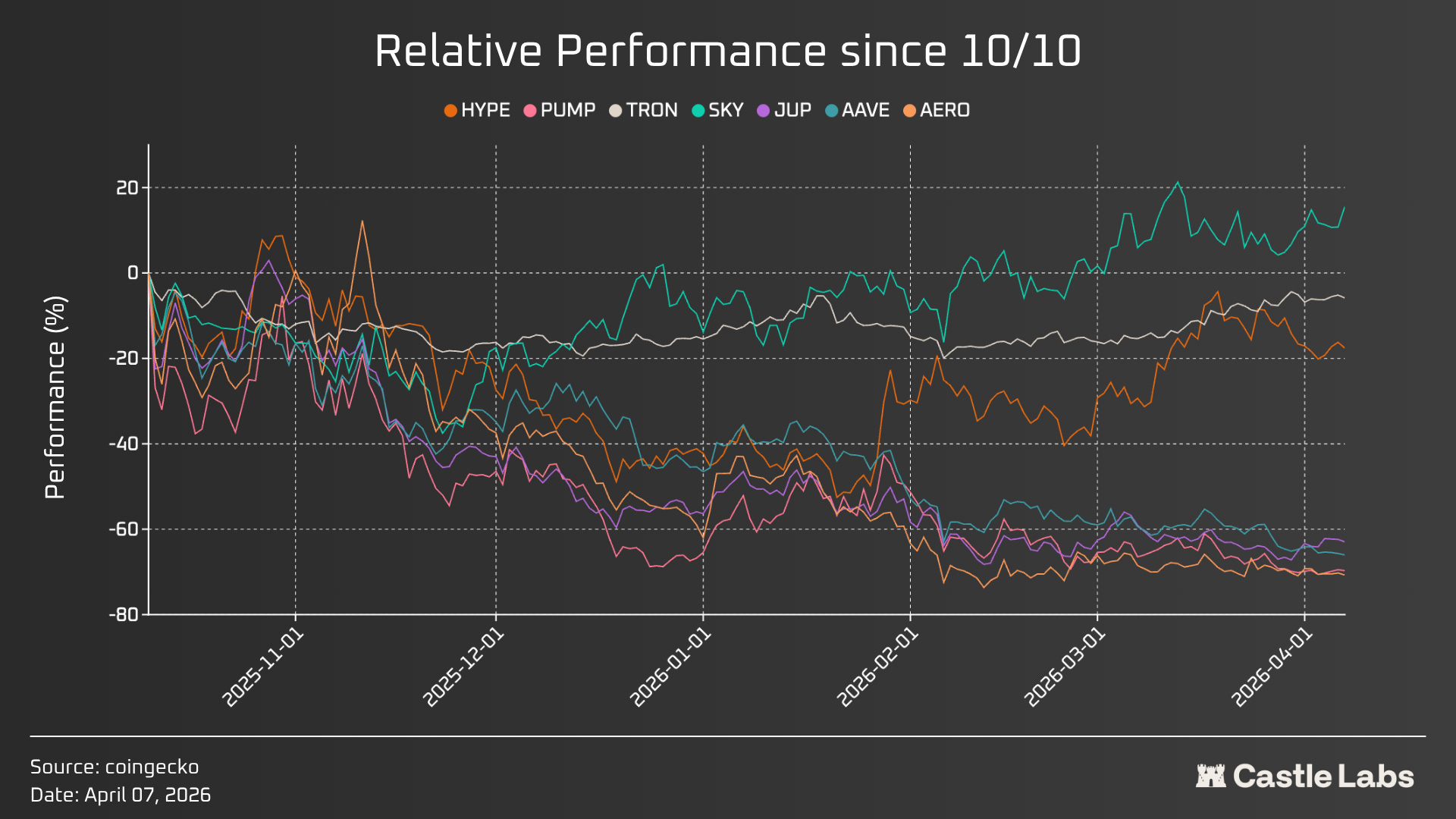

This is one side of the picture and reflects that buybacks are being executed and, if done at a similar pace, would add millions of dollars in token value. To better understand this value accrual, we also compare the relative performance of these same tokens from the October Liquidation Event to better picture the impact of token accrual activities.

In the chart above, we have a few outliers, such as TRON, HYPE, and, in particular, SKY, which is relatively positive. Of these three, TRON didn’t move much and has followed a more sideways pattern, while HYPE diverged from the other token patterns in late January.

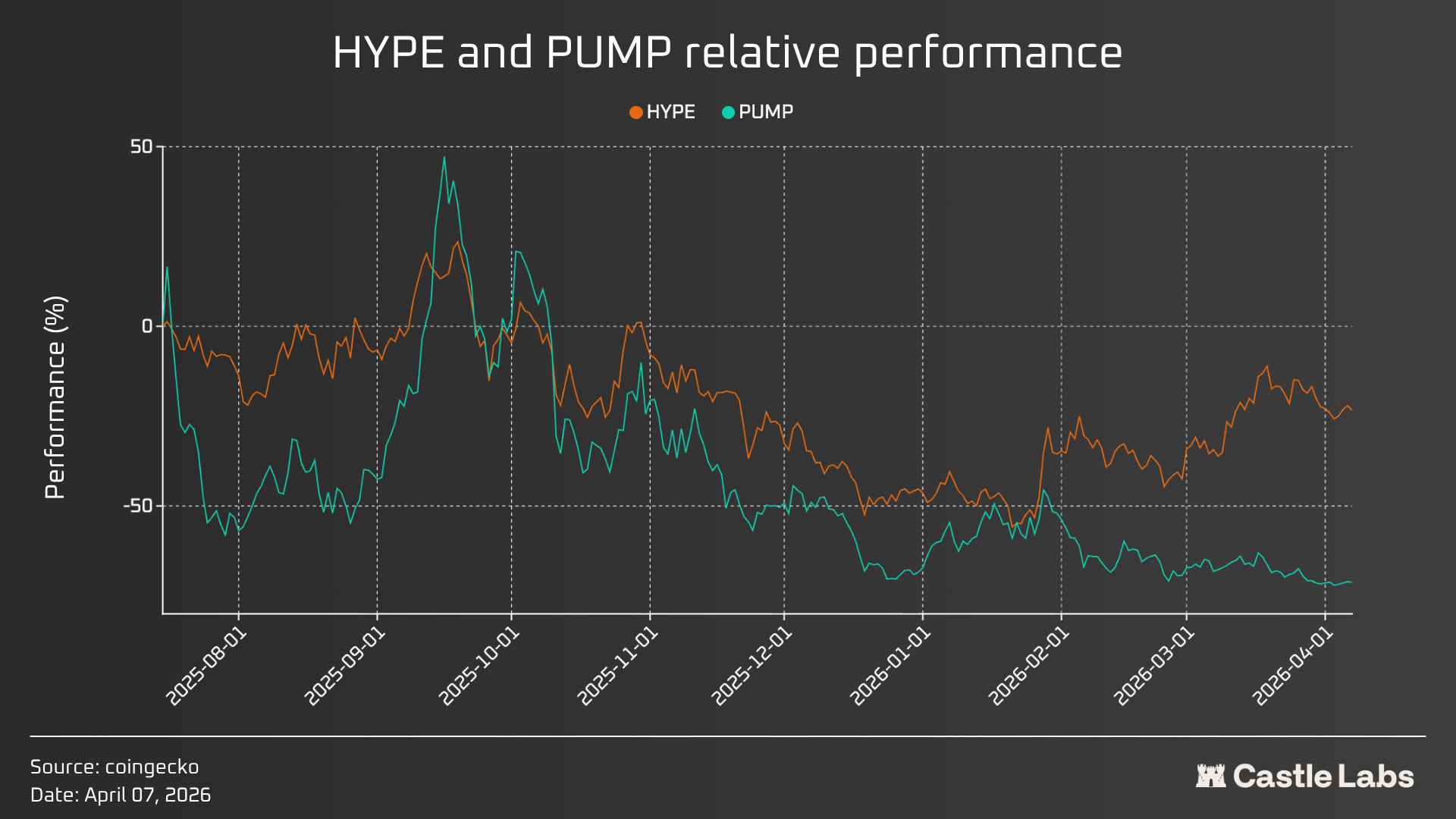

This points out that buybacks alone are not sufficient for token value increases; other factors, such as broader market drawdowns, vesting schedule and cliff unlocks, category narrative, and the protocol’s overall sentiment, also play a role. All these different points are discussed in the sections to follow. Before moving on to that, let’s also compare two of the most revenue-generating protocols and their token performance: Pumpdotfun and Hyperliquid. From the figure below, it’s clear that HYPE performed better when both tokens had active buybacks (annualised holder revenue for HYPE is ~$660 million, and for PUMP is ~$ 380 million), due to the protocol’s overall sentiment and people pricing the tokens based on future supply shocks and unlocks.

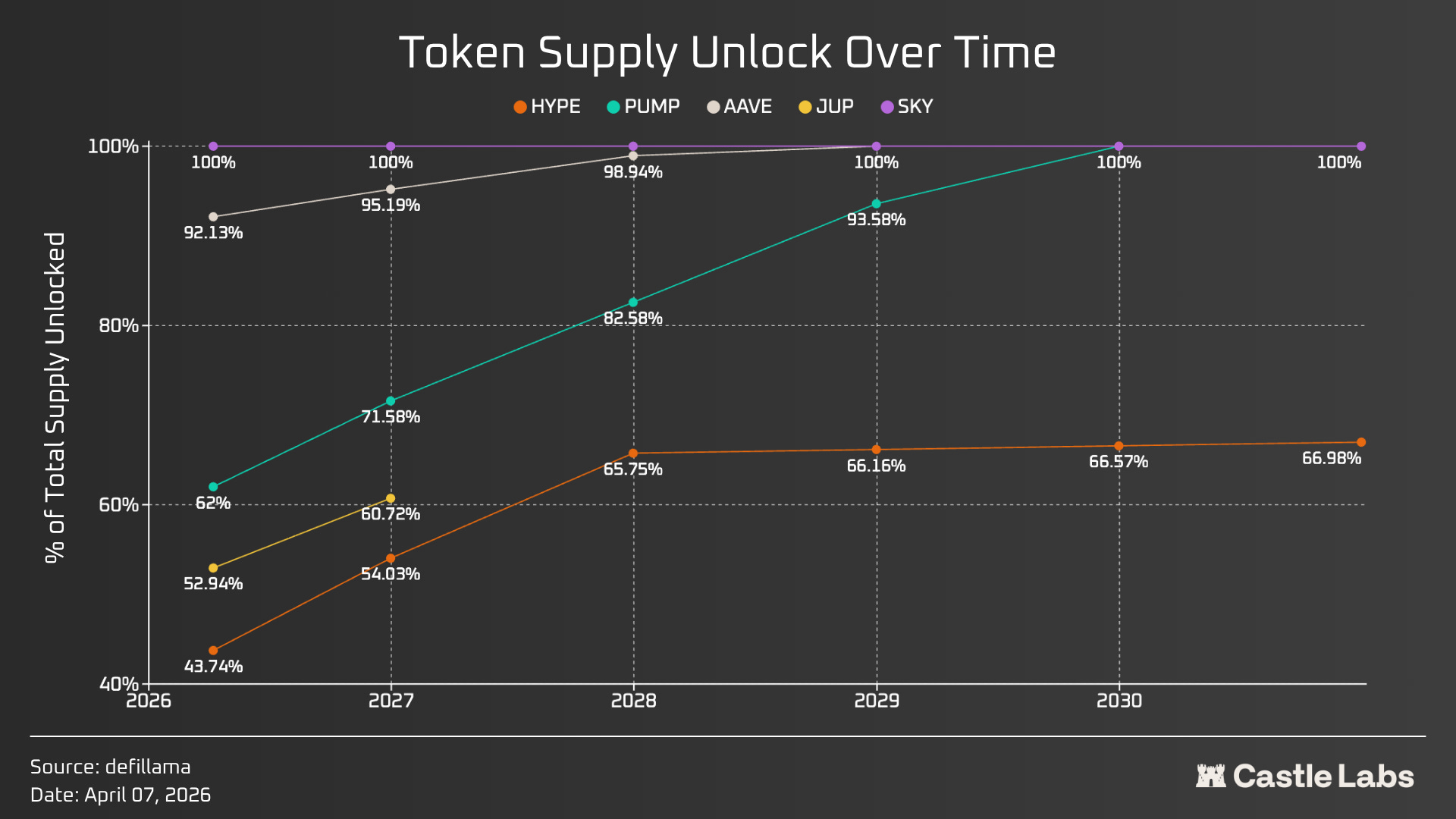

Tokenomics Design and Supply Overhang

In crypto, tokenomics is designed to help raise funds from investors, incentivise users, sometimes run a community raise, and allocate token supply to the team. There is not much of a hard-and-fast rule around tokenomics design, and different projects handle this process at their own discretion. This part of the project is important because it determines not only the token’s near-term supply pressure, but also how value accrues to the token, which value sinks exist to offset sell pressure, and how well the tokens align with their holders.

Below, we capture the supply-unlock velocity for a set of fixed-supply tokens. While most tokens eventually become fully unlocked, the pace varies significantly: PUMP exhibits the fastest unlock velocity, while HYPE unlocks the slowest. A slower unlock schedule is generally preferable, as it reduces the likelihood of abrupt supply shocks and the associated sell pressure that markets may struggle to absorb. For tokens like AAVE and SKY, most of the supply is already unlocked, whereas for JUP, the long-term unlock schedule is discretionary rather than deterministic and is governed by the DAO.

It is also important to highlight that the unlocked tokens can be further categorised into investor unlocks, team unlocks, and community unlocks. Community unlocks can be routed towards staking rewards, incentives, and airdrops. It needs to be analysed on a per-token basis and plays an important role in understanding the token’s sell-side dynamics.

The Lindy Effect

“The longer something has survived, the longer it is likely to continue surviving.”

This is what the Lindy Effect actually is, and it is true for almost all businesses, including onchain ones, with innovation as the key factor, as those who fail to innovate can’t survive for long.

Last year, crypto protocols generated cumulative revenue of ~$16 billion, and revenue concentration among the top few protocols is quite high. The top 10 protocols accounted for 80% of net revenue, with the top 3 representing 64% and Tether alone accounting for 44%.

Additionally, not all of them have tokens; for example, Circle, the second-highest-revenue protocol after Tether, has a stock listed on the NYSE under the ticker symbol CRCL. At the same time, Tether doesn’t have a token. Even among the top 10 protocols, only three included a token, indicating that launching a token might not always be the best approach, depending on the protocol design.

Returning to the Lindy Effect, in most crypto categories, the top 2 protocols account for the largest share of the market and dominate. It’s more commonly seen in categories like Stablecoin, where Tether (USDT) and Circle (USDC) represents 84% of the whole market, followed by other players like Sky (USDS) and Ethena (USDe). There are other examples where this pattern might not look as strong, but it can still be pointed out, such as Lending, where the top 2 protocols by TVL (Aave and Morpho) represent 64% of the market. The same pattern can be observed across multiple categories, such as prediction markets, yield, liquid staking, restaking, and more.

The Lindy Effect also becomes important because of the hacks the crypto industry regularly experiences at the protocol level. This year alone, we have witnessed more than $130 million vanishing from the smart contracts and, over time, tens of billions of dollars. Over time, it has become even harder to trust any new protocol with your money because you won’t know when it might get hacked. So here, the contract age and the protocol existence matter a lot because the system has stood the test of time without failing. Even if in some cases when the system doesn’t work as intended, like recent Aave’s CAPO oracle misreporting, the users get the refund because the protocol’s treasury can afford it. Additionally, the longer the system had existed, the more it had proven its significance during market drawdowns. The top protocols perform as intended during market drawdowns, a strong signal for anyone to adopt the already battle-tested system.

On the other hand, innovation is equally important, as market leaders have continually innovated and improved their products over time. For example, Morpho is onboarding various institutions to onchain finance through its vault architecture, giving them a way to curate a vault that allows maximum customisation to fit their needs. Aave will also enable this by introducing Spokes in its upcoming v4 upgrade. Additionally, Aave, through its Horizon instance, allows institutions to borrow against tokenised RWAs.

The next wave of crypto consists of Institutions and Agentic Finance; the protocols best positioned for both will grow the most.

Crypto Doomerism

In the Citrini article on “The 2028 Global Intelligence Crisis”, they write:

The biggest way to repeatedly save the user money (especially when agents started transacting among themselves) was to eliminate fees. In machine-to-machine commerce, the 2-3% card interchange rate became an obvious target.

Agents went looking for faster and cheaper options than cards. Most settled on using stablecoins via Solana or Ethereum L2s, where settlement was near-instant and the transaction cost was measured in fractions of a penny.

This begins our next chapter, which goes beyond crypto institutional adoption and focuses on Agentic Finance and the broader adoption of blockchain technology by agents. This has already started, and many protocols are integrating AI agents to streamline the user flow and eliminate user-experience bottlenecks that crypto products have long had. All these efforts can be categorised under the category that surfaced in late 2024: a combination of decentralised finance and Artificial Intelligence (DeFAI). It did its part and turned itself into an extraction-first narrative like everything else in crypto, but it also highlighted how much crypto experience can be improved by incorporating more AI.

It’s June 2028, and most crypto transactions are done by agents with no humans in the loop. Agents find the best possible yield for users based on their risk appetite. For non-crypto agents, blockchains are considered best for conducting most transactions because of their low cost, efficiency, and verifiability. Blockspace has become cheaper with time, and transactions cost way less. Crypto is no longer complex. You can give an AI agent a prompt and some money to help you earn the best yield. Crypto and blockchain are finally mainstream and widely used. To increase overall capital efficiency, agents moved funds from low-yield-generating protocols or from liquidity that was not being used optimally to a few concentrated venues where they could find the best yield. Most public blockchains and protocols are effectively wiped out for lack of use. The tokens you invested in are worth the least since you invested; you think you should’ve pulled out in 2026. Few tokens went up, including those that were actually generating revenue and continuously accruing value through revenue. From all the other tokens, the value got rotated into the few that actually perform and have some utility attached to them. Crypto market capitalisation is up when compared to March 2026, but most tokens haven’t benefited from institutional adoption and the growth of agentic finance. The crypto dream finally came true; it is being used by the masses, but the token part of the dream didn’t quite play out the way many expected.

It’s March 2026; whether or not you believe the above will become true, protocols with positive cash flow will sustain long-term, and their tokens will thrive.

Conclusion

For so many years, crypto protocols focused on the tech problem and never really on PMF, which was the biggest risk investors never priced in, but the market did over time. With most tokens seeing a downward trend for years now and their all-time highs well in the past, the story is clearer than ever that a change is imminent. The rise of certain tokens in 2026 reflected the importance of revenue numbers and a token-forward approach, as investors began to shift from Gambling to Investing.

Bad actors in crypto have always benefited from the extraction-first narrative, while most participants in the space have left with negative portfolios and become exit liquidity, which isn’t healthy at all. As institutions are flowing in, this realisation hits even harder because they don’t want to do much with our assets but are more focused on the infrastructure we helped build over the years and is battle-tested.

As we move further with institutions and AI-enabled crypto infrastructure, we are likely to see this trend grow even stronger, as more and more investors look for hard metrics that can convince them to buy a token/equity.

written by @noveleader ✍️

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram person, you can read all of our research without the noise on our TG channel: