This Year’s Largest Exploit and the Design Choices Behind It: The Castle Chronicle

Plus: TradFi's week in crypto, Hong Kong's first stablecoin licenses, CLARITY's make-or-break month, and the protocols that shipped this weekend

Welcome back. This week, DeFi’s composability thesis is being tested in public.

Friday started with optimism:

A sharp short squeeze occurred after Iran declared the Strait of Hormuz fully open

As the bitcoin price moved up to $78k, we saw one of the biggest short liquidations in 2026 ($762M)

The S&P 500 reached all-time highs, and the crypto Fear and Greed Index climbed out of extreme fear for the first time in weeks

Then on Saturday, Kelp DAO was drained for $292 million in the largest DeFi exploit of 2026, and DeFi TVL dropped nearly $15 billion in 48 hours, with Aave losing $9.4 billion in deposits.

By Sunday, Iran had closed the Strait again, and Bitcoin had returned to $75k.

We’ll start with this Kelp hack, what it exposed, where the contagion has spread and where the responsibility lies. Then we cover one of TradFi’s biggest acquisition weeks in crypto, Hong Kong licensing banks to issue stablecoins, and Noveleader’s take on low-risk DeFi when security is under more scrutiny than it has been in years. We also got on the record with Fluid, who shipped a product while the rest of DeFi was scrolling for updates on X.

Inside the $292M Kelp hack

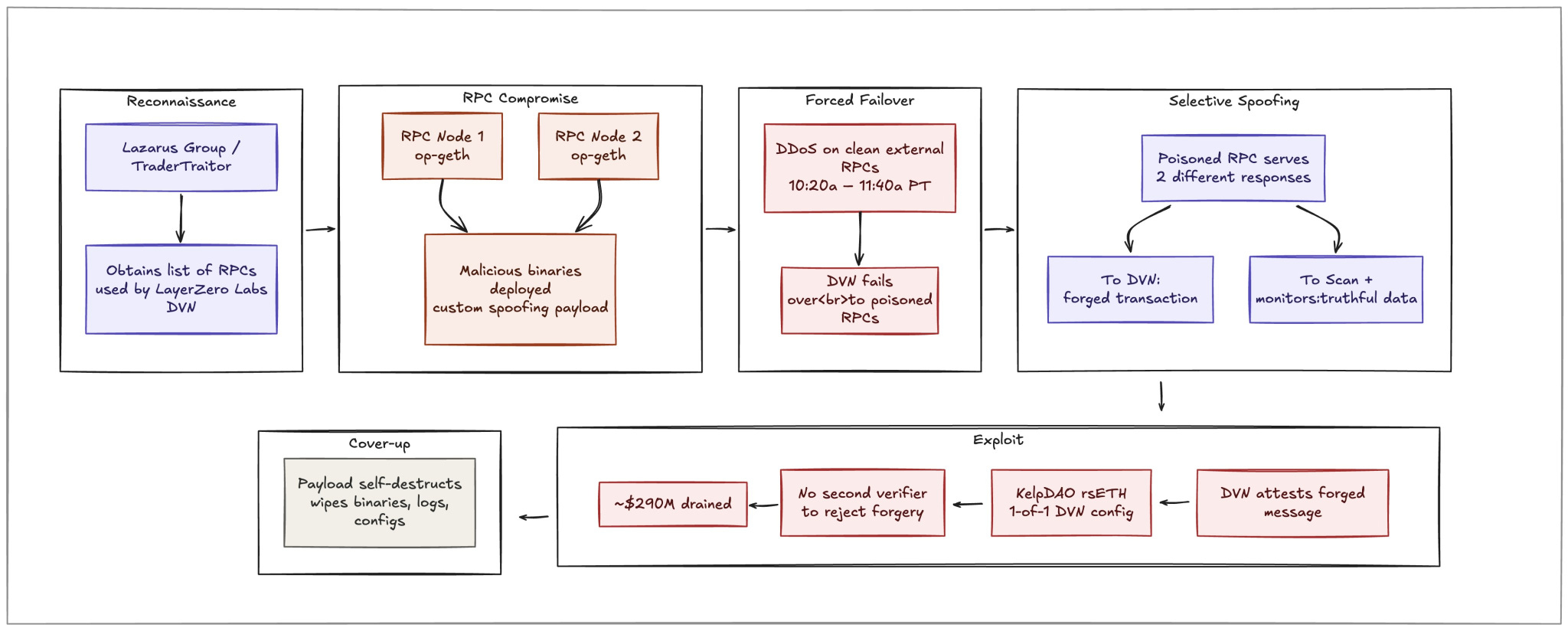

On Saturday (18 April), North Korea’s Lazarus Group is believed to have compromised two RPC nodes within LayerZero’s Distributed Verifier Network (DVN), whilst DDoS-ing the remaining nodes, forcing a failover to the compromised nodes. These compromised RPCs had been installed with malicious versions of the node software, essentially replacing the programmes these nodes run with versions that forge cross-chain messages, leading to Kelp’s bridge minting 116,500 rsETH, or 18% of the circulating supply. The software then self-destructed inside these nodes, wiping all binaries and logs.

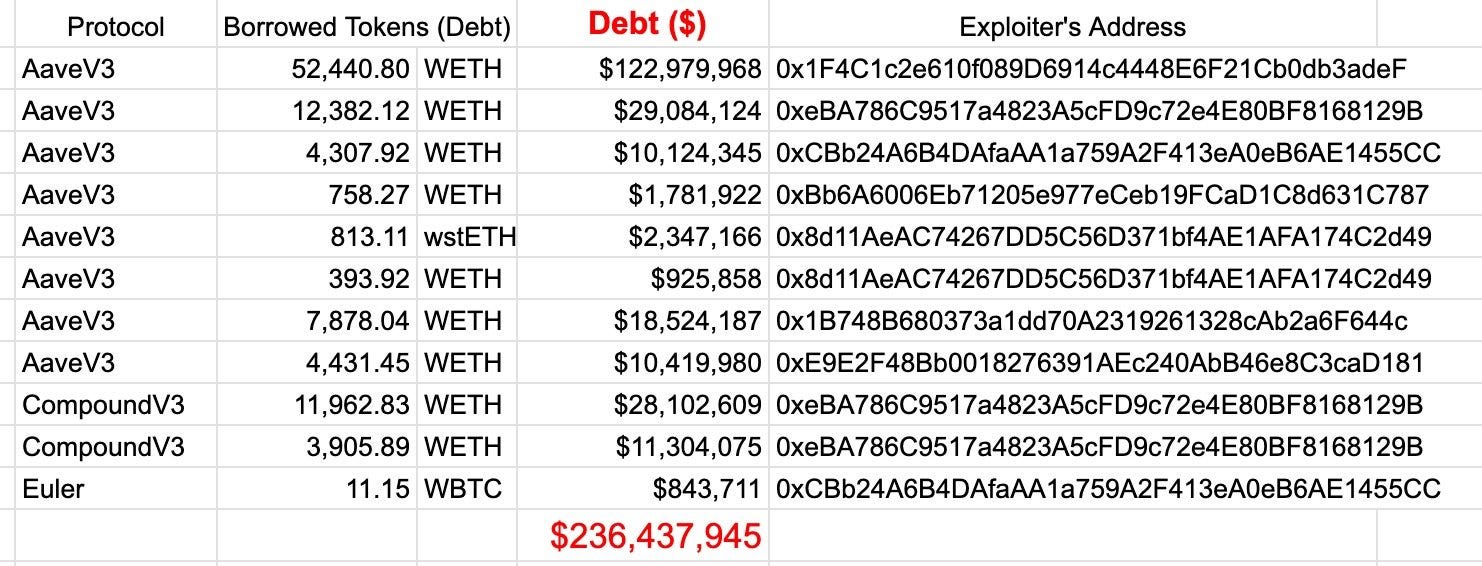

RPCs are data feeds that provide LayerZero’s verifier with updates on each blockchain. The verifier trusts those feeds to determine whether a cross-chain message is legitimate and takes action accordingly. The LZ verifier signed a message claiming that rsETH was burnt on Unichain, even though it never actually happened, causing the OFT bridge to mint. After this unbacked mint, the attacker deposited these funds into protocols such as Aave, Compound, and Euler, borrowing WETH and other assets against them, while also selling some of it on Uniswap and Fluid DEX pools, bringing the net extracted value to ~$245 million.

After the attack, Aave is left with a large amount of bad debt, and Kelp DAO has a ton of new, unbacked tokens in circulation, pushing the net collateralisation of rsETH to ~83%.

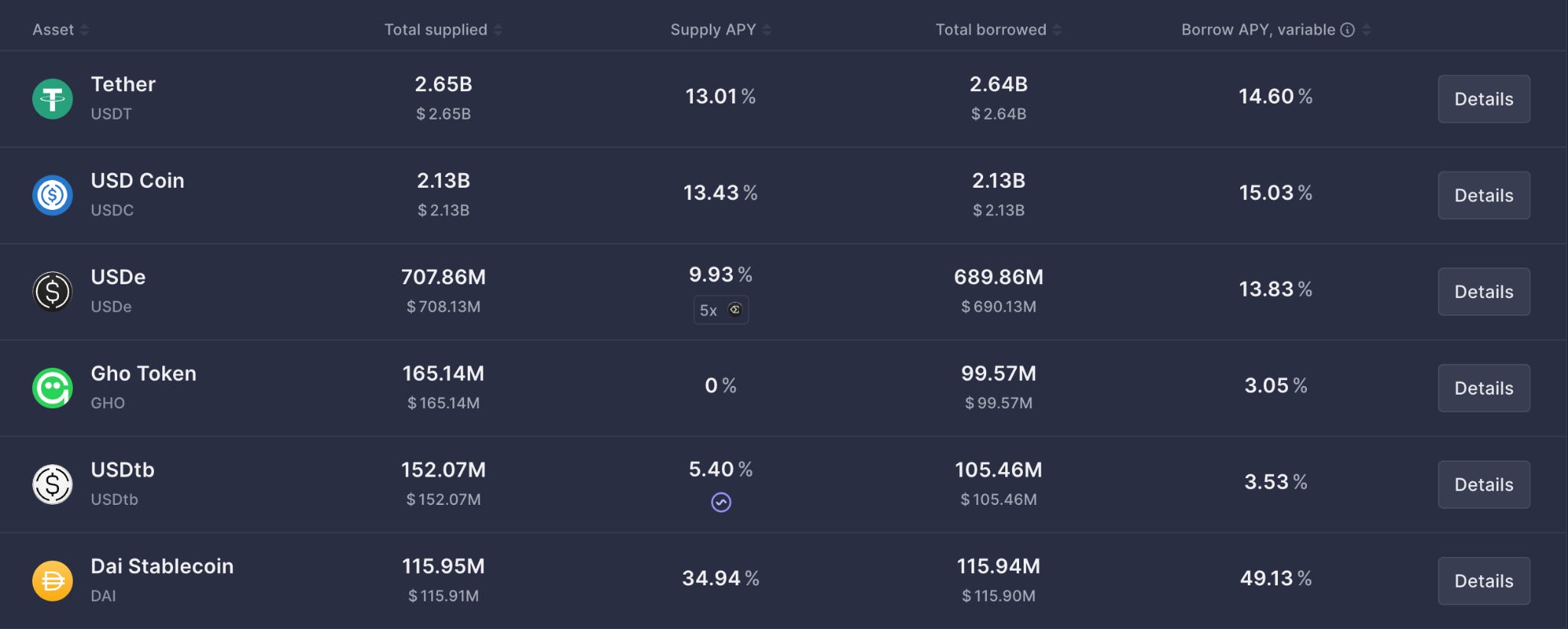

The damage compounded fast. With liquidity depleted and withdrawals impossible, lenders started borrowing against their own locked deposits to reduce exposure. This increased borrowing demand drove stablecoin pool utilisation to 100% and pushed stable borrowing rates even higher.

Aave’s role in this story is not just as a victim. Last year, a governance proposal raised rsETH LTV to 93%, leaving only a 7% buffer on a receipt token backed by a single-verifier bridge. Not one comment in the forums was raised about the risks of this one-of-one DVN.

The two groups that will take the biggest hit are Aave users and rsETH holders. To close this saga, Kelp likely needs to choose between:

Socialising the loss among Aave users (an 18.5% haircut)

Concentrating the impact on L2 holders (a 73.54% haircut, but just for L2 holders).

In the first case, combining the Umbrella pool and the protocol treasury, selling AAVE tokens, and taking out a loan would cover the bad debt (~$216 million), whereas in the second case, the situation becomes more difficult. For now, the path to resolution is still unclear.

The L2 equation changed after the Arbitrum Security Council recovered 30k ETH (~$70 million) from the attacker by upgrading the inbox contract on Ethereum with a function that could impersonate the sender. Now on L2, if Arbitrum prioritises its Aave market users, two scenarios play out:

If the case of loss socialisation, there will be no bad debt on Arbitrum.

If the impact is concentrated on L2 holders, the bad debt is reduced by 80% ($88 million to $17 million)

LayerZero claimed this attack succeeded directly because Kelp chose to run a one-of-one DVN configuration, despite LayerZero’s recommendations to use a multi-verifier configuration, whilst Kelp is preparing a memo blaming LZ, suggesting that a 1-of-1 DVN is the default configuration.

To make matters more interesting, LayerZero were running the DVN themselves and allowed several other clients to run a similar setup. Dune conducted an open analysis of DVN security configurations across all active OApps on LayerZero over the last 90 days. They found that 47% of OFT contracts (~2,665) run on 1-of-1 DVN, 45% on 2-of-2, and ~5% on 3-of-3.

This is now the second nine-figure DeFi exploit in 18 days attributed to North Korea. Drift Protocol lost $285 million on April 1 via social engineering. These are amongst various other attacks this month:

CoW Swap: DNS hijacking ($1.2M)

Zerion: team member’s device compromised via AI-driven social engineering ($100K)

Fake Ledger app: malicious app on Apple App Store, $9.5M from 50+ victims

Hyperbridge: $1.2B in counterfeit DOT created, sold for $237K

Whilst these attacks were structurally different, both nine-figure exploits bypassed smart contracts and targeted the team’s opsec or the infrastructure surrounding the protocols. The trend emerging this month is clear: security audits need to extend well beyond the core contracts. In line with this, we have also been seeing multiple calls for further defensive mechanisms within DeFi, learning from our TradFi counterparts by using and standardising rate limits, throttles, and circuit breakers.

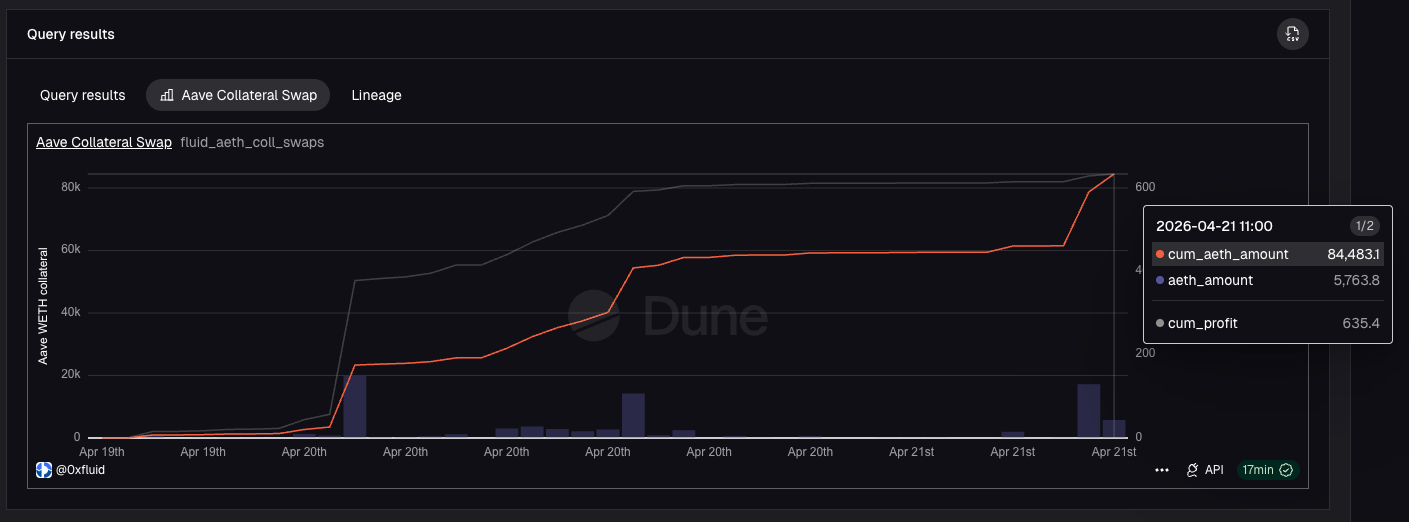

Now, as with any crisis, there were those who moved fast and benefited. Fluid launched an aWETH Redemption Protocol that matched users stuck with ETH collateral in frozen Aave markets against Fluid’s own wstETH and weETH collateral positions. The inverse positions cancel each other out, giving trapped users an exit. Agra, whose order book exchange for tokenised fixed income launched in open beta weeks earlier, offered the same exit through a different mechanism, a rate-based order book where trapped depositors could sell their yield-bearing positions at a discount to buyers willing to take on the duration.

Fluid, working with Lido, EtherFi, 1inch, and other protocols, helped users swap ~84k aETH in collateral.

More TradFi entrants to crypto

While DeFi spent the weekend firefighting, TradFi spent the week buying in:

Charles Schwab launched Schwab Crypto, offering spot BTC and ETH trading to retail clients. They have $12.2 trillion in client assets and will charge 0.75% per trade, with Paxos handling sub-custody and execution.

Deutsche Börse took a $200 million stake in Kraken at a $13.3 billion valuation, deepening a partnership announced in December 2025 that covers regulated crypto trading, derivatives, tokenised assets, and institutional custody.

Goldman Sachs filed for a Bitcoin Premium Income ETF, a covered call structure that sells options with 40-100% BTC exposure and distributes the premium as monthly income.

Kraken’s parent, Payward, is acquiring Bitnomial, the only crypto-native US firm holding all three CFTC licences required for a full-stack derivatives business, for up to $550 million in cash and stock. The deal gives Kraken the regulated infrastructure to offer spot margin, perpetuals, and options to US clients.

CLARITY Act markup expected this month

The other story in the regulated world this week is the CLARITY Act, and its window is closing fast. The Act serves as a broader piece of legislation to the GENIUS Act, which, whilst establishing the full reserve and regulatory framework for payment stablecoins, banned passive yields on them. JPMorgan says negotiations are nearing a breakthrough, as disputes have dropped from 12+ to only 2-3 core issues, and White House crypto advisor Patrick Witt confirmed the yield compromise is holding: passive yield would remain banned, while activity-based rewards tied to payments, transfers, and platform usage could be permitted.

A markup is expected as early as this month, with the Senate floor vote projected for May, but the time pressure is on. Galaxy Digital’s head of research, Alex Thorne, warns that if the bill doesn’t clear the banking committee by the end of April, the odds of it passing this year would become extremely low. This is a topic several stablecoin issuers will be waiting on to plan the next steps in their roadmaps, with fears that missing this window could delay any legislation until the 2030 elections.

Hong Kong grants first stablecoin licences

The Hong Kong Monetary Authority (HKMA) has granted stablecoin issuer licences to HSBC and Anchorpoint Financial (a joint venture among Standard Chartered, HKT, and Animoca Brands). Both will issue HKD-denominated stablecoins fully backed by cash and short-term government bonds, with HSBC planning to embed its stablecoin into PayMe, a Hong Kong-based P2P and business payments app, by late 2026.

There are, however, restrictions that come with this jurisdiction, as expected. No interest is permitted in relation to the issuance of stablecoins under the Ordinance, and licensed stablecoins can only be transferred to identity-verified wallets with travel rule compliance exceeding HK$8,000 (~$1,000). On the flip side, the HKMA effectively deprioritised its retail CBDC efforts after an 11-group pilot found the retail case to be weak.

Hong Kong, and by extension China, is making its first formal steps into stablecoins. They’ve seen the success of US-denominated stablecoins and want a piece of it, but on their own terms. The yield ban and identity-verified wallets tell you everything about how tightly this will be regulated, controlled, and monitored.

DeFi Risk Equation

Noveleader from the Castle team on where DeFi yield sits right now.

Interacting with any yield source comes down to the risk the depositor is assuming.

Given the current state of DeFi, an obvious question comes to mind: “Is any yield enough if it comes at the risk of losing your principal?”

DeFi risk has increased exponentially this year and last year as many blue-chip DeFi protocols handling large sums of value have been hacked, starting with GMX v1, Balancer v2, Resolv, Drift, and now KelpDAO + LayerZero. This year alone, crypto hacks have led to losses of over $750 million.

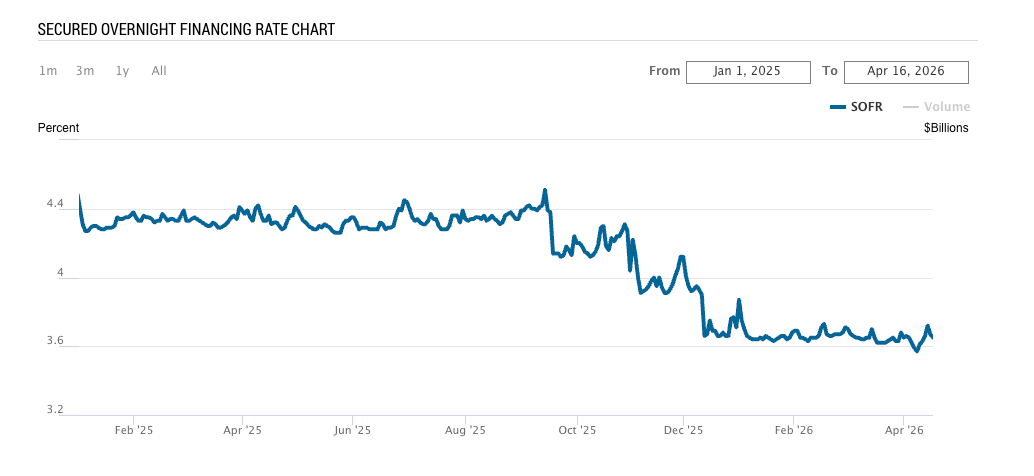

Meanwhile, DeFi “risk-free” yields have been underwhelming, remaining between 2% and 4%, and compete with the Secured Overnight Financing Rate (SOFR), which currently sits at 3.65%, a benchmark that closely tracks risk-free returns on U.S. Treasuries. For most users, keeping capital in DeFi doesn’t make much sense when they can earn similar yields elsewhere with almost no tail risk. DeFi yields are also highly market-dependent: in good markets, they beat SOFR, but during drawdowns, they fail to do so, making them inconsistent.

With yields at an all-time low and the risk of keeping money in DeFi at an all-time high, users are rushing to exit DeFi altogether, and low-risk DeFi is taking a back seat. In the last 2 days, DeFi TVL plummeted by 15% from ~$100 billion to currently ~$85 billion, with Aave being the biggest contributor, losing $9 billion in TVL, a 34% drop, a direct effect of the recent bad debt accumulation on the protocol.

On a positive note, these cases give DeFi an opportunity to evolve by incorporating stronger security practices and considering additional safety mechanisms, such as circuit breakers. In this rsETH exploit, the attacker was not only able to deposit a large amount of rsETH and borrow against it almost instantly, but also to mint a large amount from a chain that actually had very little rsETH.

Protocols can, for example, introduce a phased increase in LTVs for users based on collateral age, so that malicious intent can be detected early before a large loss occurs. They can set withdrawal limits for newer entities and tie borrowing privileges to user history, so higher privileges come with longer use of the protocol.

We reached out to both the Fluid and Agra teams after watching them ship over the weekend.

Fluid didn’t have the aWETH Redemption Protocol planned. “We saw the urgent need from the DeFi ecosystem and the opportunity, and we decided to take it,” the team told us. When we asked whether this was the start of an ongoing demand for secondary credit markets in DeFi, they pointed to TradFi. Products like credit default swaps exist for exactly these situations in traditional markets, and he expects DeFi to develop its own equivalents. Due to recent exploits, the team told us they were “used to these crisis situations.”

Agra, on the other hand, was already live and waiting. They spun up a new market on their existing infrastructure, as the crisis became their biggest onboarding event to date. “We saw bids from both whales and onchain asset managers,” the team told us. “Asset managers were bidding aEthWETH at a ~5% discount to par, which reflected their underwriting of how Aave would socialise bad debt and where aEthWETH sat in the credit stack.” All were net new users.

Before this incident, secondary market liquidity for credit was something they had to argue for. Now they are seeing their conversations change from “why does this matter?” to “how do we establish this for our protocol?”

This weekend was one of the first examples of secondary markets for credit appearing onchain and seeing meaningful volume, even if it came from distressed conditions. For both Fluid and Agra, the crisis served as a live stress test of their products, giving both teams real data to iterate on. We see this as a natural evolution in DeFi’s product offering. We’ll be watching how these markets develop from distressed conditions into normal trading, and what that unlocks for both the assets being issued and the users looking to manage duration and risk.

Aave bad debt resolution. The path forward is still unclear. Socialising the loss across all users (an 18.5% haircut) or concentrating it on L2 holders (70%+) are the two options being discussed. The applicability of the Umbrella mechanism is also up for debate, as stkAAVE holders are watching for potential slashing.

Kelp DAO’s response. Kelp is reportedly preparing a memo contesting LayerZero’s framing. rsETH holders on 20+ L2s are still waiting to find out whether their tokens are backed. Net collateralisation is sitting at ~83%.

What will happen to protocols running single-verifier configurations? Dune’s analysis found that 47% of OFT contracts (~2,665) run on 1-of-1 DVN. LayerZero has announced it will no longer sign for any project using this setup. Expect verification-as-a-service to become a more discussed category.

CLARITY Act markup. If the Banking Committee clears it this month, the bill is alive. If it slips, it may be dead for 2026.

Iran ceasefire expires April 22. One to watch, but realistically, the situation is so opaque that nobody knows what’s going on.

Another tough week, but with it comes opportunity. See you next Tuesday.

Don’t forget to join our Telegram channel for the latest updates from Castle and all our research: Link here

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn’t guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.