The State of Onchain Neobanks, with EtherFi, Kast, MoonPay and Osero: The Castle Chronicle

PLUS: the CFTC clears the first US-regulated perp, Paxos wins settlement relief from the SEC, and a new wave of fixed-rate lending

The second quarter of the year has come to an end, with a clear winner.

Hyperliquid ($HYPE) continued to diverge from the rest of the major tokens, recording an ~85% move higher in the month, with HYPE touching an all-time high of $74.

This is reflected in HYPE.D, Hyperliquid’s share of the total crypto market cap, rising at the sharpest rate seen to date, as well as the launch of HYPE ETFs, which have absorbed more than 1% of HYPE’s total market cap in under two weeks.

All this whilst continuing to post records in open interest on its RWA perpetual markets.

This is a very different picture from the rest of the ecosystem, characterised by three consecutive weeks of outflows across all digital asset investment products, totalling $2.617B in May.

In other news, the CFTC approved regulated US perps, but not everyone is cheering on it, with Jamie Dimon criticising Coinbase and stablecoin rewards, and vowing to fight the Clarity Act.

In this week’s Castle Chronicle, we dive into:

The CFTC clearing the first US-regulated perp

Paxos is receiving securities settlement relief from the SEC

A new wave of fixed-rate lending products is coming

The State of Onchain Neobanks from Atomist’s ETH Milan speech, with interviews from EtherFi, KAST, MoonPay, and Osero.

CFTC opens the door to onshore perps

Regulated US perpetuals were given the green light last week when the CFTC approved KalshiEX’s BTCPERP, the first true bitcoin perpetual cleared on a US-regulated exchange.

This news arrived alongside:

A policy statement on how it will treat future perp listings

A no-action relief allowing Coinbase to offer its US clients access to perps on Deribit, the offshore venue it now owns

After the years the industry has spent circumventing US regulation, it cannot be overstated how much of a positive signal these statements are for builders and, more importantly, risk-averse institutions, who continue to operate with greater confidence.

Ambiguity in the past has driven these markets offshore and, in the words of Hyperliquid Policy Center, left American traders and institutions without “access to regulated venues”. They welcomed the CFTC’s move while asking that the framework work for the onchain protocols where most perpetuals activity actually occurs.

Kalshi’s perp launch is expected within the month, with more than a dozen assets to follow. The questions on everyone’s lips are who will come next, when this grace will be extended to onchain protocols, and what they will have to comply with to be included in the framework.

Paxos gets the SEC’s clearing-agency nod

Perps were not the only piece of crypto infrastructure handed a regulated win last week. Paxos’ settlement arm won temporary registration as a clearing agency from the SEC, making it the only blockchain-native firm cleared to settle securities as a central depository. This comes seven years after a 2019 no-action letter, showing just how long the industry has been waiting for authorisation to innovate within regulated boundaries.

Clearing and settlement isn’t the most glamorous corner of finance, but it is a hugely important one. This is the layer that determines whether a trade actually completes, and it has been dominated by a handful of incumbents, such as the DTCC, for decades.

A crypto-native firm holding this licence means tokenised securities can settle on infrastructure built for the following generation of programmable finance. Meaning less friction, greater access, and more possibilities.

Slowly but surely, crypto-native firms are being granted access to traditional parts of the financial stack, just as traditional firms are beginning to dip their toes onchain. Not everything is simply happening in one direction.

Jupiter and Morpho ship fixed-rate lending

Two of DeFi’s biggest names launched fixed-rate credit products this past week.

Jupiter, Solana’s DeFi heavyweight, opened Offerbook to public beta, a peer-to-peer marketplace where borrowers post almost any Solana asset (tokens, NFTs, even trading-card collectables), and lenders make USDC offers at a fixed rate and term. There are no oracles and no price-based liquidations, so as long as the borrower repays on time, the collateral is theirs, whatever happens in the market. It is built primarily for the long-tail assets that the majority of pooled lenders will not touch, running on RainFi, the P2P lender Jupiter acquired in December, with 230,000 loans already in its locker.

Morpho, meanwhile, released the whitepaper and open-sourced the code for Midnight, its fixed-rate, fixed-term credit protocol. The design is similar to an onchain bond market, where lenders and borrowers post offers but do not lock capital until settlement, so a lender can keep earning elsewhere until a borrower fills the order.

Fixed-rate lending onchain has had a tough time in the past. Yield Protocol wound down in 2023, citing a lack of demand, and other survivors struggled to grow without incentives and remained a minute fraction of variable-rate giants like Aave.

These previous models meant lenders had to park capital waiting for borrower demand that often failed to arrive, leaving these assets completely unproductive. Morpho’s design aims to overcome this, paired with the distribution they already have to the institutional users that fixed-rate products are catered towards.

The demand for each product is still unproven, and they are targeting vastly different customer segments, but the industry is maturing to the point where these kinds of products are more likely to be welcomed than the triple-digit APR farms of old. We will be tracking the adoption of Morpho Midnight in particular, and how successful they are in onboarding and matching lenders and borrowers with this new product.

The State of Onchain Neobanks

A couple of weeks ago, our co-founder, Atomist, took to the stage at ETH Milan to present some of our research around onchain neobanks: their origins, evolution, and future trajectory.

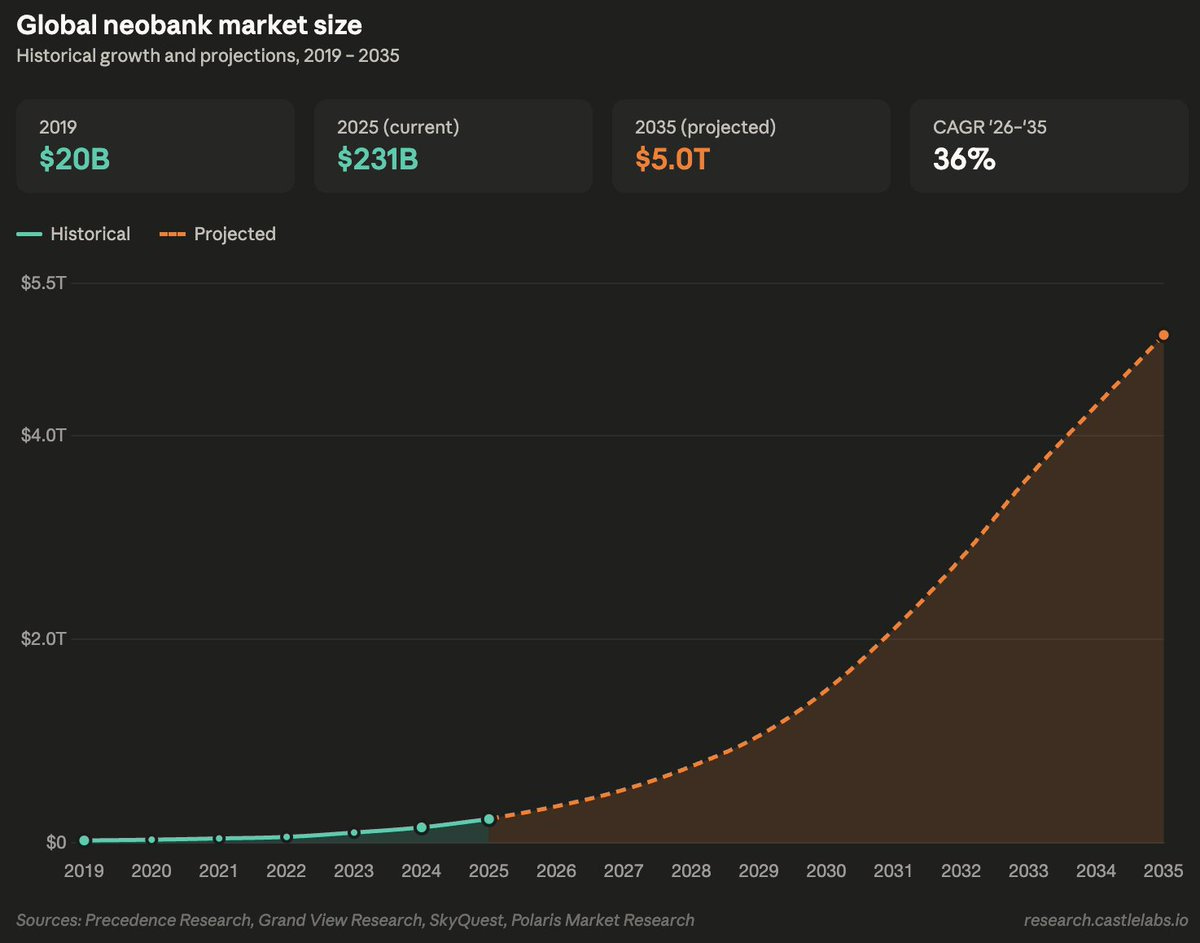

We have all heard of Revolut, which started as a travel card for people tired of bank FX rates. Today, it has 70 million users, six billion in annual revenue, and moved 1.7 trillion in 2025. The global neobank market is already worth $357 billion and projected to pass $5 trillion by 2035.

Traditional neobanks promised to replace legacy banking but ended up running on the same rails: the same correspondent banks, the same settlement delays, the same custodial model, just with a better experience, using an app.

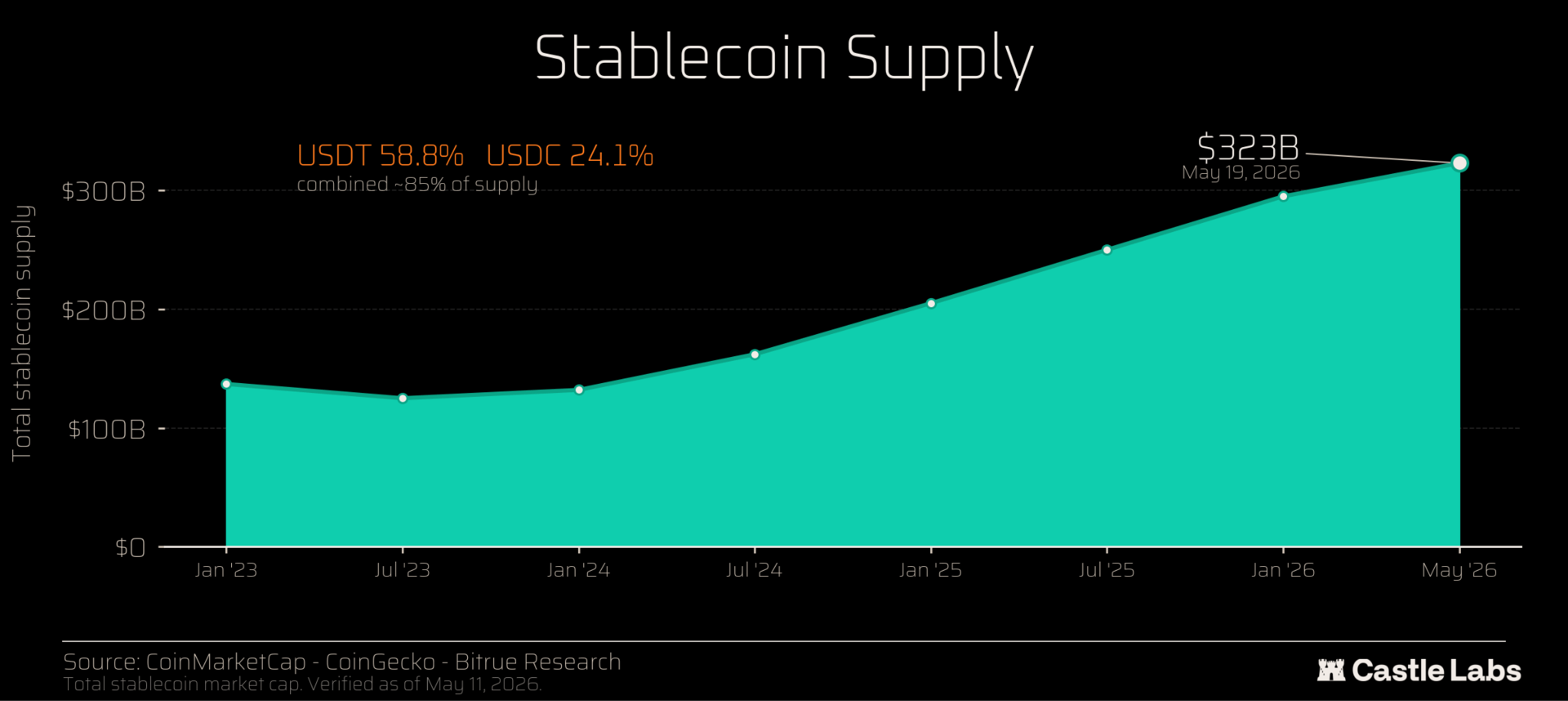

During the rise of regular neobanks, a separate growth story has been happening. Stablecoins. Total supply just crossed $320 billion, and with it the arrival of new utility and applications for blockchains. One of these is onchain banking, and with it, storing, spending, growing, and borrowing capital.

Crypto card spend climbed to $656 million a month in May, up from $271 million a year earlier, a 230% jump. Visa processes around 90% of it, and its own stablecoin settlement pilot is now running at a $7 billion annualised rate, up 50% in a quarter.

Crypto cards give users the feeling that they finally own their money, and increasingly, the infrastructure backs it up.

What makes these onchain banks different is that you do not store money with them, you use money through them.

We spent the last few weeks talking to the people building in this growing sector, and the demand they describe often comes from outside of crypto and outside the West. Emanuel from Kast told us its traction is with “modern, globally mobile people, USD earners and businesses,” and that it is expanding across Latin America and the Middle East. EtherFi’s growth lead (masterzorgon on X) sees the same pull in emerging economies, where “users want access to USD via stablecoins.” This isn’t just degens spending gains anymore, it’s people in the real world who want dollars and can’t easily get them through their local bank.

Crypto cards have come and gone for years, so the obvious question is, why is this time any different? MoonPay’s Andrea Mars thinks the arrival of stablecoins has changed everything: earlier cards asked you to spend a volatile, appreciating asset and “triggered a taxable event on every swipe.” Stablecoins remove both problems, and the yield on the backing, sourced onchain, can fund the rewards. EtherFi’s read is simpler: the use case was always obvious, and “now it’s a matter of delivering a consumer-grade mass market product.” Anyone who used the CeDeFi cards of previous cycles knows they weren’t exactly a focus of the businesses running them, and that showed in the user experience.

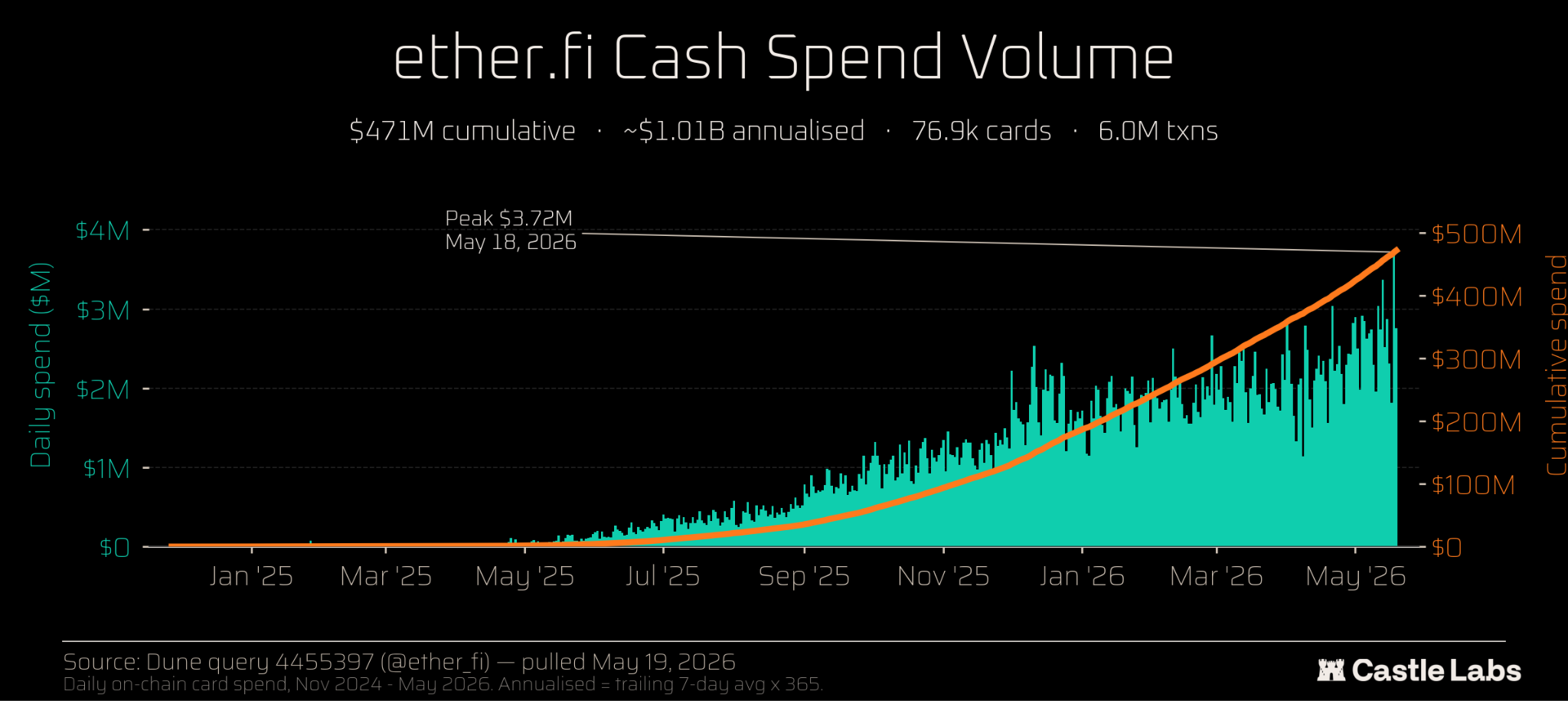

The numbers behind EtherFi’s Cash offering show how in this new environment, good products can generate real volume. They now stand at more than 300,000 accounts, with over 70,000 active cards, and daily spend hitting a record $3.7 million in mid-May. Their Cash product now accounts for around half of EtherFi’s protocol revenue.

Another product seeing strong growth and recently closing out its highest-volume week is Avici. Avici feels more like a neobank than many others, with access provided through its mobile app and self-custody hidden behind passkeys and account abstraction, making login feel seamless as retail would expect. Its Visa credit cards are issued by Rain, with users spending against their own crypto collateral rather than topping up a debit card balance.

The last one worth a mention is Plasma One. They are currently in private beta but have been ramping up access of late, with $765K volume in April and $3.1M in May (+305% in one month). Full launch is due this month, so expect this to increase even more sharply, especially when the Android version comes out.

All of these providers have obviously got their spending features locked down. But what about savings?

Osero, which grew out of the stablecoin-yield platform Stablewatch, claims that offering stablecoin yield means a neobank effectively has to start “becoming a DeFi asset manager,” taking on custody, risk assessment and ongoing management of where deposits sit. Not all neobanks offer yield on deposits, and if they do, it’s often through token emissions. Osero have recently entered the fray with a savings product built on top of the Sky Savings Rate. They point out that most large neobanks already use stablecoin rails internally for treasury, but “haven’t turned this into a user-facing yield feature.”

What we are beginning to watch closely is the battle for control of the infrastructure underneath these banks. White-label stablecoins are one route, with neobanks and applications starting to explore issuing their own branded dollar. Mars gave some insight into why: neobanks already own users and distribution; “what they’re missing is the rail.” MoonPay aims to provide them with issuance, ramps, and settlement as a single piece, looking to become the infrastructure layer that consumer apps run on in the background. He goes so far as to claim the market cap of white-label stablecoins will increase 10x in the next year.

The downside is that onchain banks trade one risk for another. You remove exposure to the bank’s balance sheet, so your money can’t be frozen, rehypothecated, or lost in a bank run, but you take on smart contract risk, oracle failure, exploits, and your own mistakes.

For someone who understands DeFi, that’s arguably the better deal. But for the average consumer who expects someone to pick up the phone when it goes wrong, it isn’t - yet at least. Gnosis Pay’s exploit yesterday, in which a shared module drained user funds without a single key vulnerability, showed how real this risk is.

This week, we began to see where this industry goes next, with Base releasing its MCP and Liquid shipping a chat interface to move and control a user’s capital through agent workflows.

Every one of these products is converging on the same four functions: save, spend, earn, borrow, but this time, owned by the user rather than the bank, with onchain rails and DeFi supercharging the possibilities.

Who clears the CFTC next: With Kalshi securing itself as the first out of the gate, which exchanges will be next, and when will the first DEX get authorisation? Other CFTC-regulated crypto exchanges include Bitnomial (recently acquired by Kraken) and Gemini, plus Kalshi’s prediction-market rival Polymarket.

Whether fixed-rate lending finds its demand: Fixed-rate lending is commonplace in traditional finance, where rate assurance enables players of massive size to lock in long-term yield strategies, something that has always been lacking onchain.

Whether the agentic layer gets adoption: Despite Base releasing their MCP and new teams like Liquid bringing agentic products to market, we are still waiting for a breakout app to drive volumes in agentic finance. Read more here: https://research.castlelabs.io/p/the-beginning-of-agentic-finance

When will Saylor sell again: This week, Saylor’s Strategy sold 32 BTC, framing it as a one-off for STRC dividends, but now the door is open, it is surely just a matter of time before the next batch.

Don’t forget to join our Telegram channel for the latest updates from Castle and all our research: Link here

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn’t guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.