Composable TradFi: RWAs in DeFi

Mapping the growth of RWAs in DeFi

This article is an excerpt from our research on the Real-World Assets: Bringing TradFi Onchain

Download the complete report here: https://docsend.com/v/sjv2g/rwareport

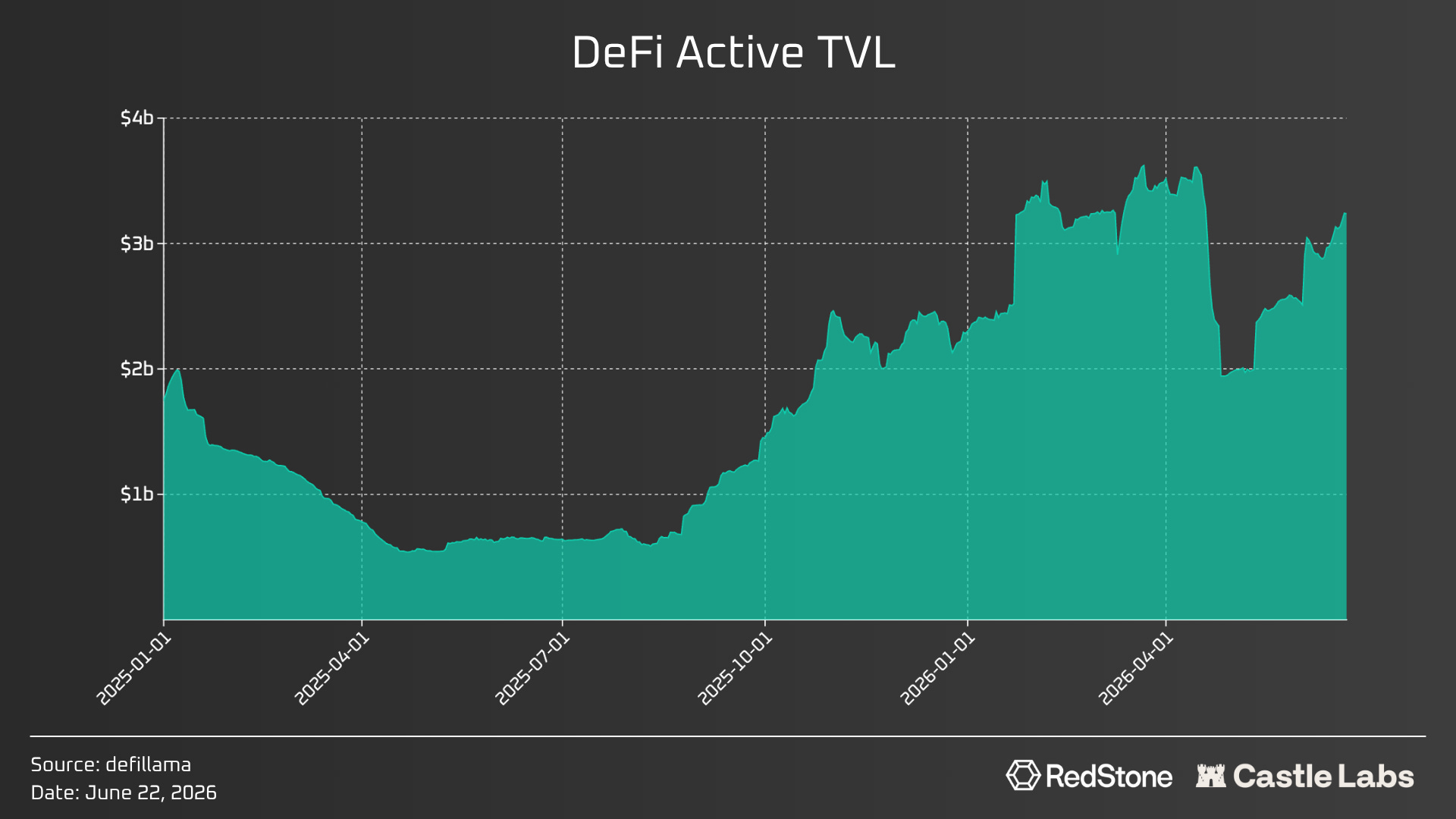

While the RWA market size is huge, at ~$28 billion, the actual value deployed in DeFi is only 10% of that, at ~$3 billion.

The 90% of unutilised RWAs are tokenised assets for exposure; they still have a use case, but not an enhanced one, such as serving as collateral in lending protocols. The main reason for using these assets in lending protocols is that they can be used in looping apart from just earning additional yield as a deposit.

In Looping, an asset that has an underlying yield is used as collateral to borrow against. These borrowed assets, usually stablecoins (USDC/USDT), are used to buy the same asset again, which are then put up as collateral and borrowed against. This process can be repeated multiple times, depending on the collateral allowed loan-to-value (LTV) ratio. The leverage a user can achieve can be calculated using the same ratio: leverage = 1 / (1 - LTV). So for an LTV of 70%, a user could take ~3x leverage. This strategy becomes profitable only if the borrowing rate is lower than the RWA yield.

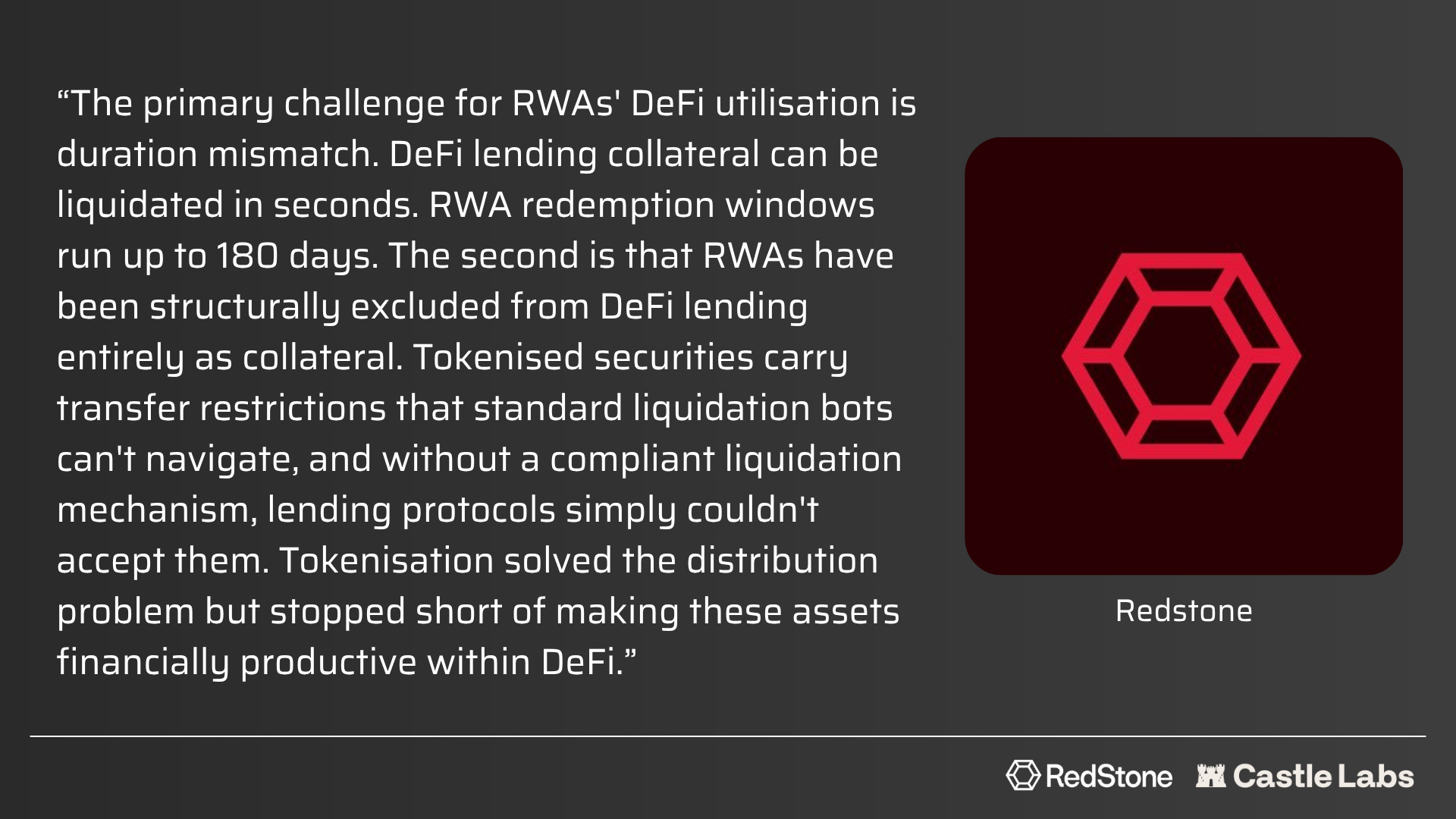

While dynamic borrowing rates in lending protocols play an important role in the profitability of looping, scaling the strategy actually needs a better liquidity profile and instant redemption. If these positions need to be liquidated because higher borrowing rates erode collateral or because their value changes, the liquidators must sell the collateral to pay off any debt. But due to settlement delays and redemption availability ranging from T+1 to T+3, it becomes a major problem. To address this, multiple protocols are building products, which we will explore in this section. Before that, we will take a brief look at which assets are currently being utilised and why.

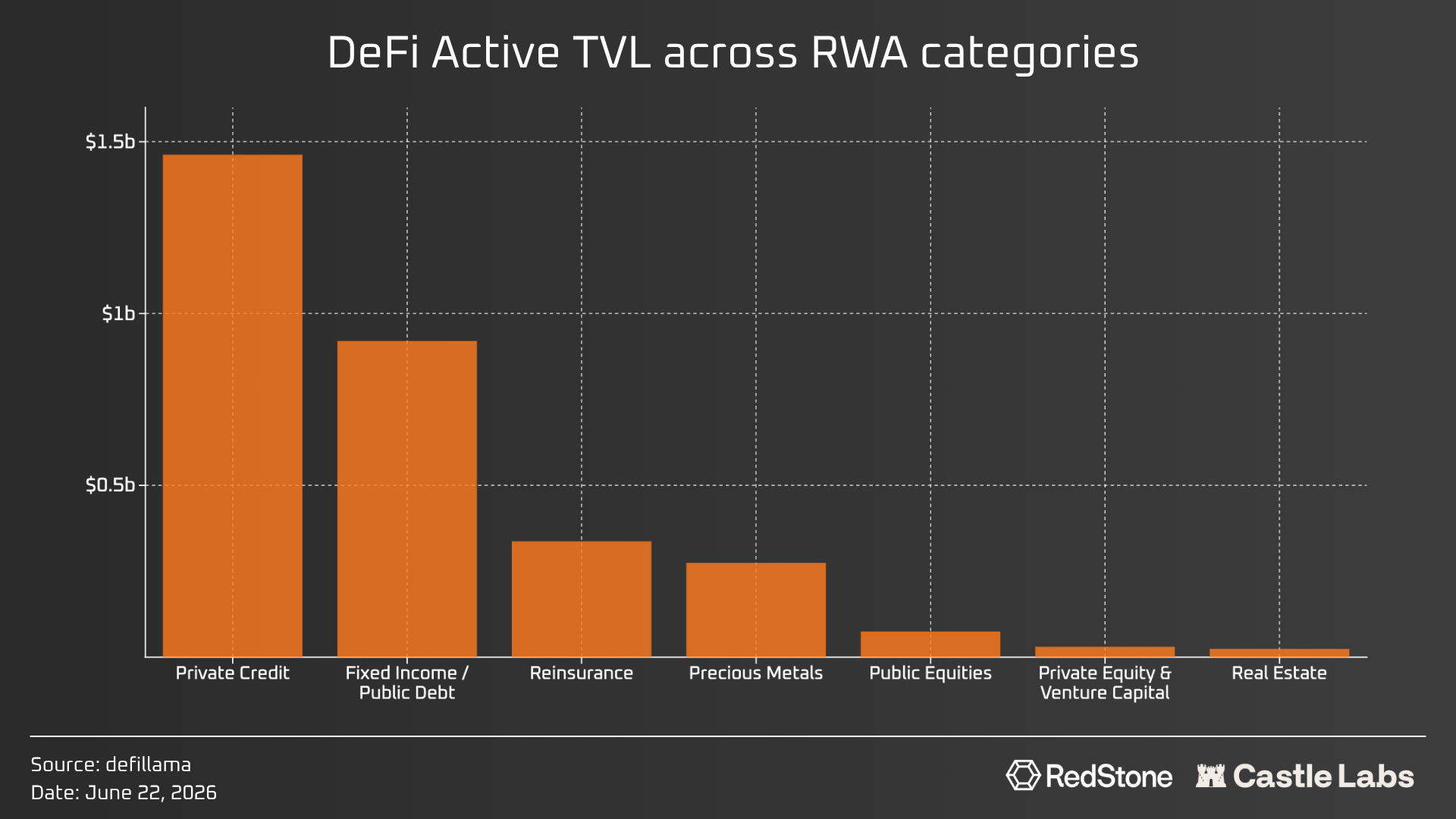

The current RWA DeFi TVL is lower than expected. The majority of this number comes from private credit, followed by public debt and reinsurance. However, if we compare utilisation relative to an asset class’s market size, reinsurance ranks at the top, with over 83.2% of its market capitalisation actively deployed in DeFi. The same numbers for private credit and public debt are 46.7% and 5.5%, respectively. These three categories alone represent 84% of all RWA deployed in DeFi.

But behind this usage in DeFi lie multiple protocols, including Morpho, Maple, Aave, Kamino, Fluid, and more.

Current Stage of RWAs in DeFi

The current active DeFi TVL is about $3 billion, with categories such as private credit and reinsurance leading the way. In this section, we explore the reasons behind this concentration and recent developments that have helped increase DeFi utilisation of RWAs, with a focus on protocols, liquidity, and redemption.

Pendle and Fixed Rate Products

Pendle is a yield tokenisation layer with $956 million in TVL across 11 chains, making it the leading fixed-rate primitive in DeFi by a wide margin.

Pendle takes yield-bearing tokens, whether RWA or not, and splits them into two separate claims: a Principal Token (PT) and a Yield Token (YT). The PT represents the principal portion and can be redeemed at maturity for the accounting asset. The YT receives the variable yield and rewards until maturity.

This aligns well with institutional actors, who are accustomed to creating long-term, stable strategies using fixed-income products, in which rates and maturity dates are known. Variable onchain yield, on the other hand, is harder to underwrite.

As TN, Co-Founder and CEO of Pendle, put it: “Fixed income and interest rate swaps are the backbone of TradFi, and bringing the same structure to RWAs opens these assets to a wider set of strategies and, in turn, a different class of user.”

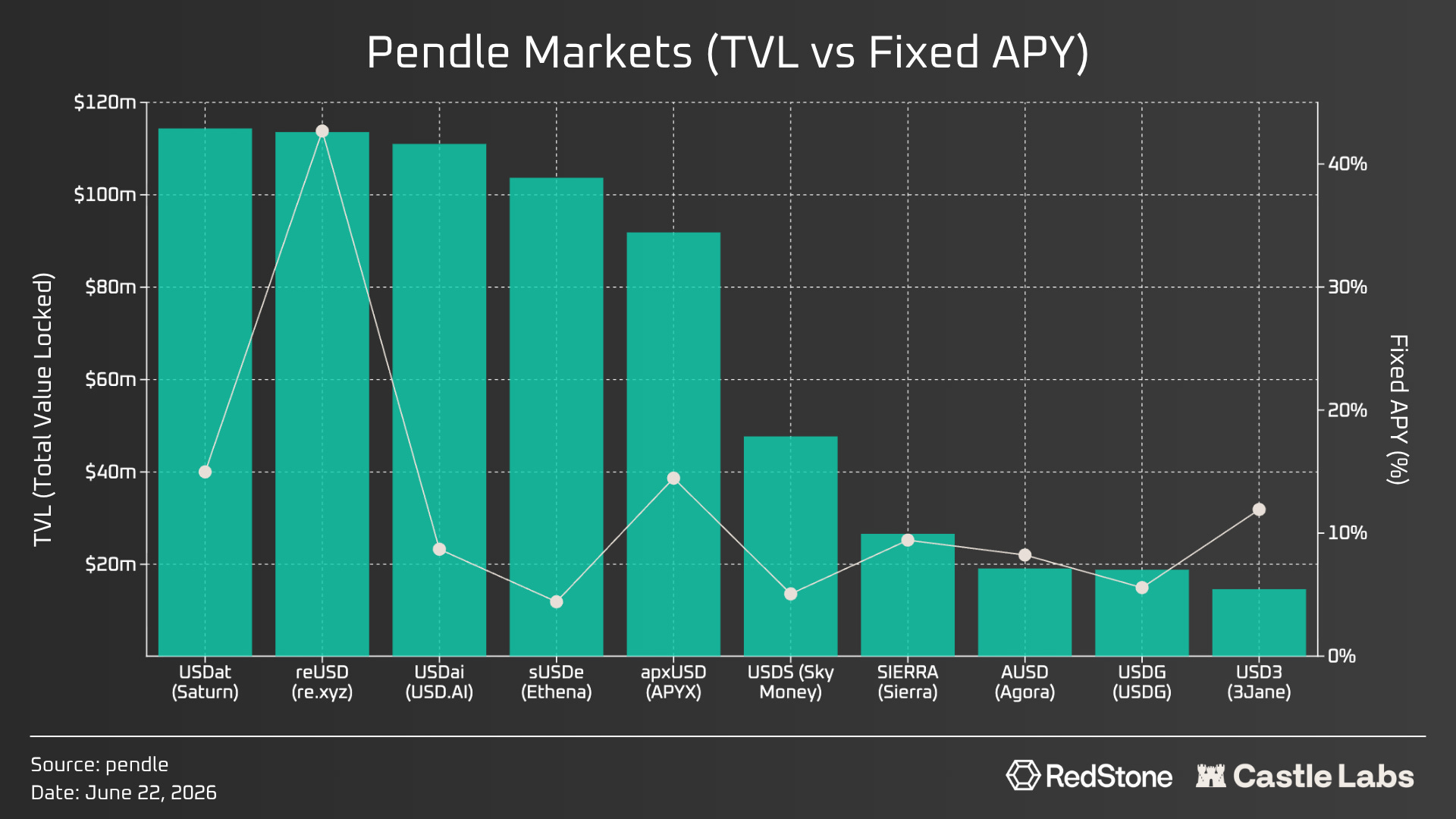

This institutional story is still developing, however. Pendle’s largest markets still include crypto-native assets such as sUSDe, liquid staking assets and points-driven yield products. Current Pendle RWA markets remain short-dated, with TVL and 7D volume concentrated in maturities under 6 months.

Public dashboards show many of the largest Pendle markets are actually PT-heavy, including major stablecoin, Ethena and RWA-labelled markets. That suggests there is real demand for locking in a consistent yield rather than only speculating on YT. The caveat is that the largest markets still skew toward crypto-native yield, stablecoin yield, points and structured products rather than mature institutional RWAs.

The current RWA-labelled metrics from Pendle V2 show exactly this. The TVL leaderboard is led not by institutional tokenised assets but by structured yield assets like USDat (saturn.credit), reUSD (re.xyz), USDai (USD.AI), and apxUSD (apyx.fi).

Stablecoins remain the clearest near-term category, while “tokenised preferred shares have also demonstrated real appetite.” Assets such as USDat and apxUSD sit near the top of the leaderboard and are linked to DAT / STRC-style yield. Others are different again: reUSD introduces reinsurance-linked exposure, while USDai brings AI-compute credit onchain.

Pendle has built one of the best onchain venues for turning variable yield into fixed-rate instruments, but demand for institutional RWA assets and markets is still forming.

Lending Protocols

Lending protocols are the most important part of RWA utilisation, as they enable RWA to participate in the active onchain credit economy.

Having an RWA being utilised as collateral and borrowed against is a huge utility add-on for any asset because it can help boost the yield of the asset or leverage the exposure by borrowing against and buying the same asset again, a process which is done multiple times, also called “looping”, as highlighted above.

While looping helps drive growth, it is a leveraged strategy and should be viewed as such.

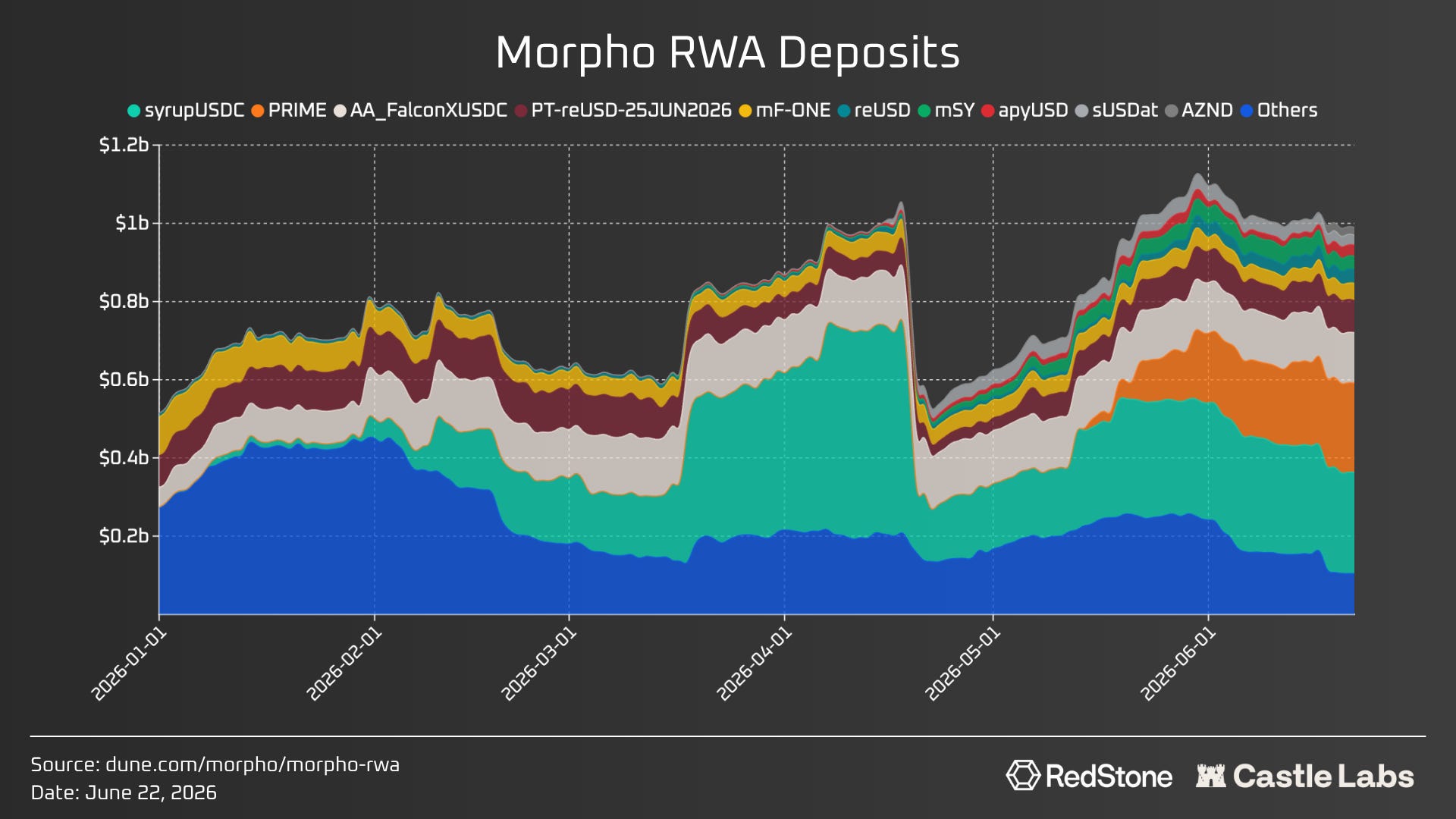

Morpho

Morpho is the leader in RWA utilisation, with over $1 billion in RWA deposits and $400 million in active loans against them, and ~40% RWA-specific borrowing utilisation. For reference, this is already 10% of the cumulative deposits on Morpho, which is ~$10.5 billion.

The majority of this growth came in the last two months from assets such as syrupUSDC, PRIME, and AA_FalconXUSDC, driven by overall growth, leading to increased allocation and looping demand from specific vaults (supporting automated looping) and users.

Why is Morpho a leader in RWA deposits?

Isolated Markets: Morpho’s design isolates markets and the risks associated with them, making them a suitable venue for RWAs, as they carry their own risks and, in the case of any bad debt, won’t lead to larger contagion effects, unlike in pooled models.

Permissionless Curation: Another aspect of morpho’s is that it is built on the curator model, allowing curators to customise vaults to accommodate custom collateral ratios, interest rates, and compliance checks, which is a much-needed addition, as different RWAs have different legal structures and liquidity profiles.

To really understand what permissionless curation enables, Steakhouse Vaults are a great example. They provide exposure to multiple RWAs, and their allocation process includes assessing risks related to “Credit, Counterparty, Liquidity, Oracle, Smart Contract, and Liquidity Traps”.

Morpho’s architecture is self-sustaining and scalable, requiring minimal governance inputs to add new assets, markets, and vaults.

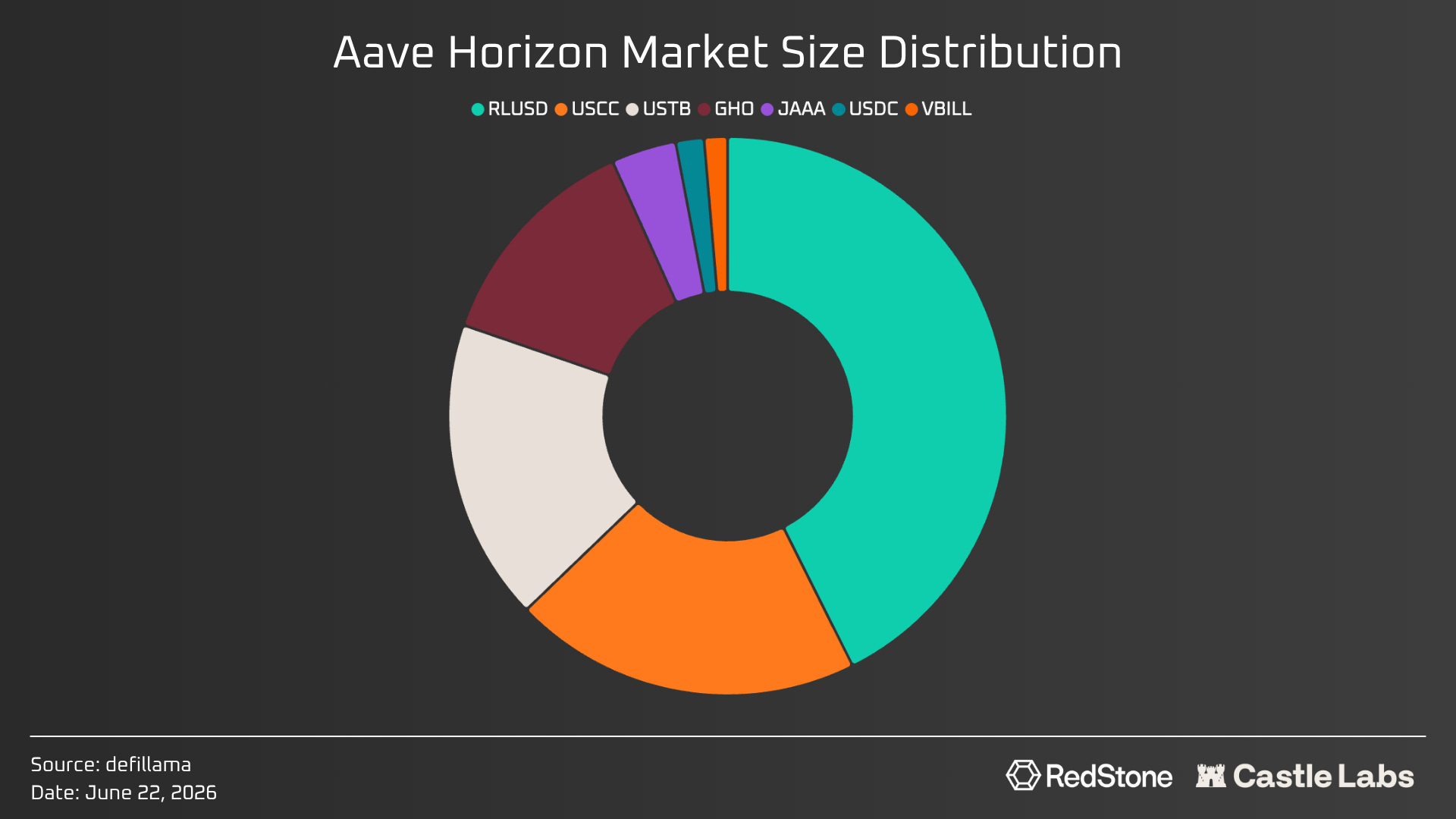

Aave

Aave, the largest lending protocol, also launched its RWA instance, Aave Horizon, in August 2025. Today, it has a market size of ~$500 million and accepts multiple RWA collateral, such as USCC, USTB, VBILL, and JAAA, as well as deposits from lenders in RLUSD, GHO, and USDC, which are then lent to institutional borrowers who deposit the whitelisted assets.

Most of its supplied assets and borrowing demand are associated with RLUSD, which has active rewards pushing the supply yield. Aave also allows RWA assets to be utilised in v3, with Maple assets (syrupUSDC and syrupUSDT) having cumulative deposits of over $330 million.

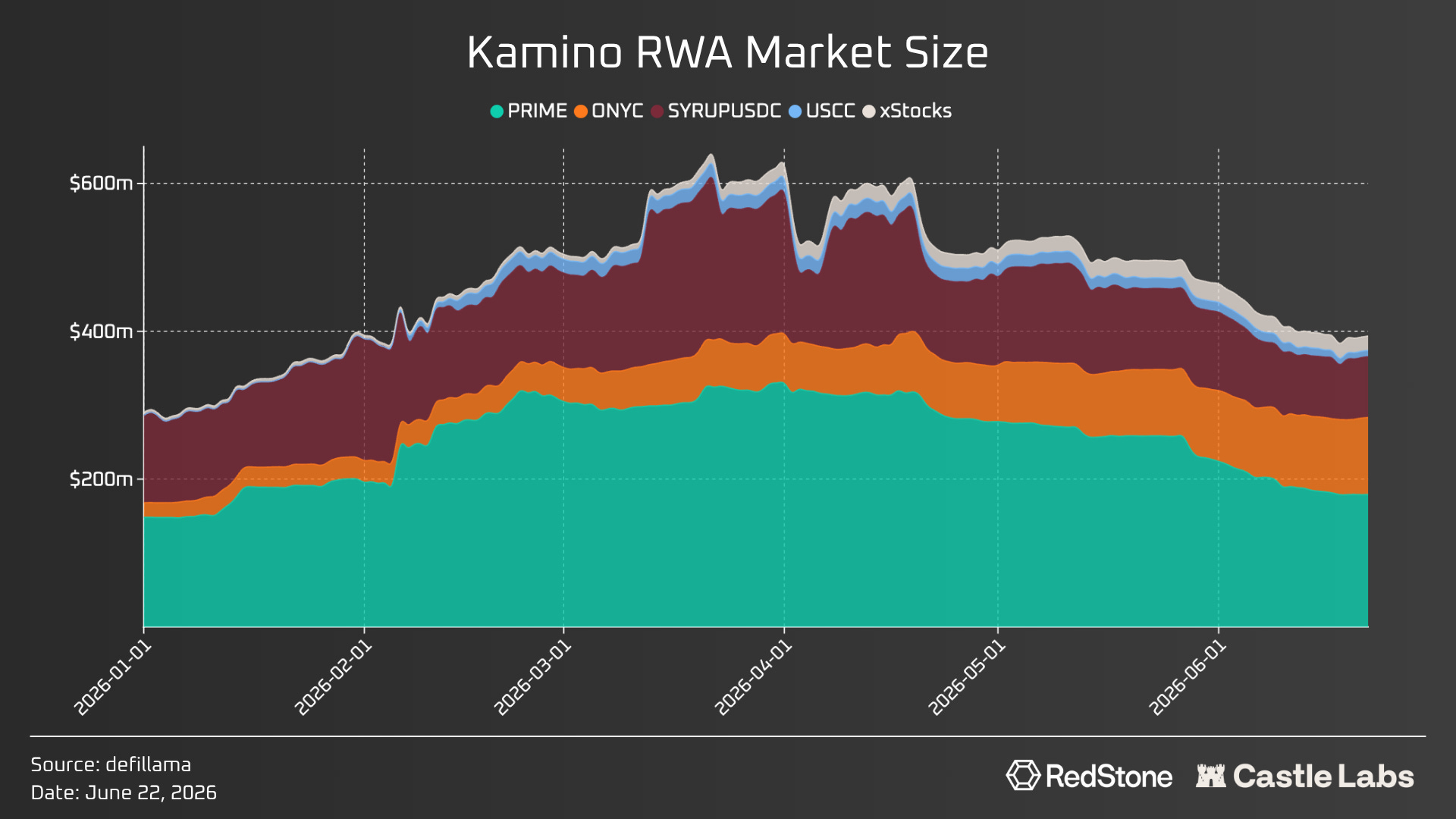

Kamino

Kamino on Solana has strong RWA demand with PRIME (Hastra), syrupUSDC, ONyc (OnRe), and USCC being deposited on the platform, totalling $400 million in market size.

An interesting bit about Kamino is its integration of assets from xStocks, which currently sits at net deposits of over $20 million, beating every platform in tokenised public equities deposits. Since the majority of xStocks products’ liquidity is on Solana, Kamino becomes an obvious choice for deploying these assets.

But tokenised stocks still have particularly low utilisation given their size, though the category is developing to address this.

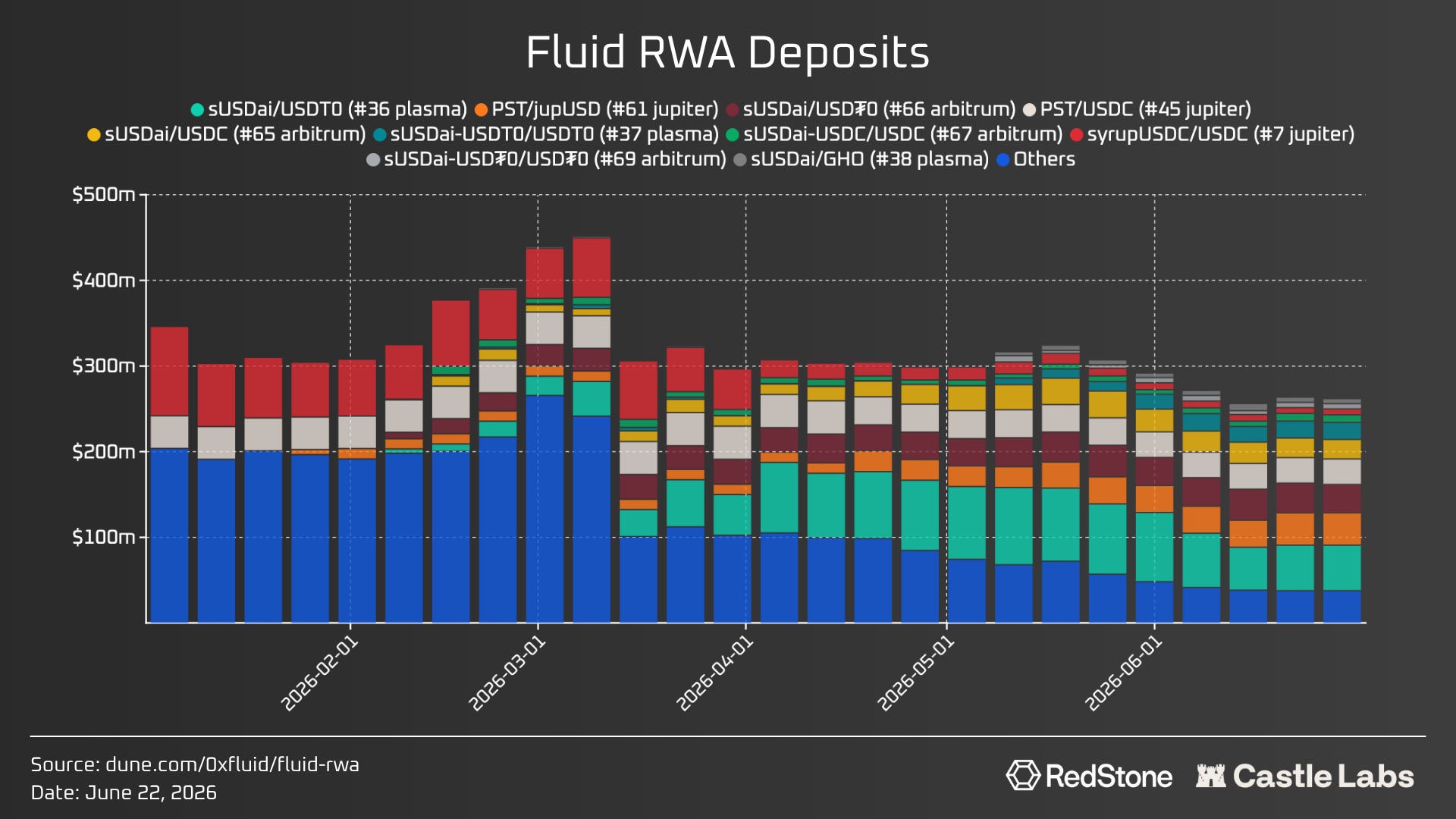

Fluid

Fluid’s architecture is unique due to its liquidity hub design and primitives like Smart Debt and Smart Collateral, which can help deploy collateral into AMM pools, reducing borrowing costs and making it a more profitable venue for running loops. Due to this design, Fluid is able to provide a venue which is “cheaper to bootstrap deep secondary market liquidity, enable deep borrow/lend markets, and provide the best borrowing conditions with high LTVs and low LTs”.

Currently, the market size of RWAs on Fluid is $270 million, primarily led by sUSDai from USD.AI. This number also includes the RWA deployed in JupLend (Fluid’s whitelisted deployment in collaboration with Jupiter Exchange on Solana). Juplend mainly has deposits of PST (tokenised by Huma Finance, earning yield from real-world payment flows), syrupUSDC, and tokenised public equities like SPYx from xStocks.

Additionally, with its design and collaborations, Fluid provide “large cross-ecosystem distribution (across EVM and Solana via Jupiter - the largest retail user base in all of DeFi) and services like Liquidity-as-a-Service (LAAS), which can save asset issuers millions by totally cutting out market-making and liquidity management costs.”

Onboarding these assets into any system requires multiple processes to ensure they are fit for the platform.

While the adoption of RWAs in DeFi looks promising, it still only accounts for 10% of net tokenised RWAs. While transfer restrictions and KYC requirements for these assets contribute to this number, another problem is the slow redemption infrastructure for RWAs.

For example, for an asset with T+1 settlement that is bearing high borrowing rates and decides to close its 3x-leveraged position, the exit would take 2-4 days. If they had sufficient liquidity to exit, the exit could have been executed instantly. While they are trying to exit, their position still accrues the spiked borrowing interest.

A solution to avoid an invariant borrowing rate is fixed-rate lending, which has also begun to emerge within the lending category through products such as Jupiter Offerbook (already launched) and Morpho Midnight (in the audit phase).

Even with fixed-rate lending and borrowing costs known, exiting the loop takes time, and for someone looking for an instant exit, it remains an issue.

The next section explores the products working in this direction.

The Developing Redemption Infrastructure

While RWAs have achieved good scale, they still face the problem of active onchain redemption required to access liquidity immediately, which is also essential for making them composable within DeFi. For example, in a lending protocol, when a position needs to be liquidated, the liquidator would need to sell the RWAs to pay back the loan.

Solving this issue requires a third party willing to assume that duration risk in exchange for the instant liquidity they provide to the liquidator.

Products like Redstone Settle, Upshift Clear, and others provide this exact form of redemption.

RedStone Settle

Redstone Settle launched in April 2026 and operates as a KYC-verified solver auction for atomic cross-chain RWA redemption.

A user initiates a redemption request.

Redstone runs a competitive auction among KYC-verified solvers capable of providing immediate liquidity.

Winning solver fronts USDC at T+0 (instantly).

The solver is reimbursed at T+1 or T+2 when the issuer processes the underlying redemption.

The solver (currently on a whitelist basis) bears the duration risk during the asset’s settlement window and maintains the spread post-settlement, while DeFi protocols receive immediate settlement. This essentially creates a market amongst solvers to provide competitive bids while accounting for duration risk.

Upshift Clear

Upshift Clear, launched in May 2026, provides T+0 USDC liquidity for RWA assets at a 50 bps fee via their dedicated USDC Vault. They have initially provided support for Superstate Crypto Carry Fund (USCC) redemption.

The 50 bps fees create a structured repo market for RWA assets: Clear vault lenders earn from the spread plus USCC yield accrual during the redemption window.

Grove Basin

In May 2026, Grove launched its institutional instant RWA redemption product, Basin, providing up to $1 billion in daily liquidity. This product is launched in partnership with BlackRock (BUIDL) and Janus Henderson (JTRSY). For this redemption product, Securitize and Centrifuge provide the underlying tokenisation workflows, while platforms such as Anchorage Digital, Galaxy and FalconX facilitate access to the product.

Basin targets the settlement gap for funds that cannot use permissionless solver auctions like Redstone Settle due to regulatory constraints or counterparty KYC, making it an institutional-grade complement to products like Settle and Clear.

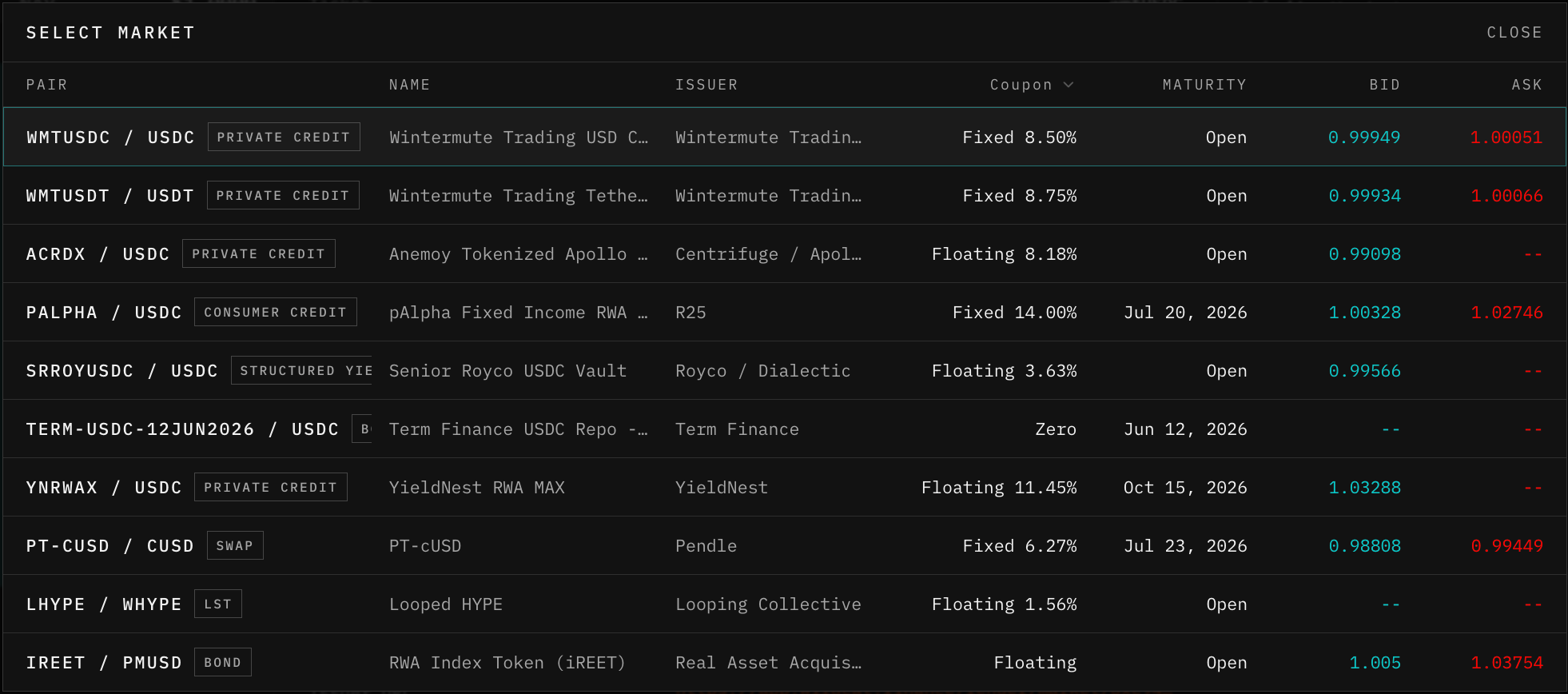

Agra

Agra is a central limit order book for tokenised credit instruments. It currently supports markets such as wmtUSDC/USDC (the receipt token for deposits in the market that provides loans to Wintermute on Wildcat), ACRDX/USDC (Anemoy Tokenised Apollo Diversified Credit Fund), and a few others.

Makers post bids at a discount to the NAV of these assets, and get access to the yield visible on the platform itself. It essentially boosts the total yield for makers since they got the asset at a discount. After that, they can either sell using the same mechanism or hold it until maturity. While on the taker’s side, they are simply swapping one asset for another through a CLOB.

Again, even in the Agra model, markers are essentially getting paid for the duration risk.

3F

Another protocol serving in the redemption and efficient RWA looping category is 3F (a platform for leveraging RWAs onchain). It currently has $7.7 million in net leveraged exposure and approaches the problem of RWA assets in DeFi differently than other solutions.

3F externalises different parts of the RWA instant redemption problem through Bridge Facilitators and Liquidity Integrators.

Bridge facilitators provide upfront liquidity to complete the exposure the user intends to take on their base capital. For example, a user targeting $3 million in exposure and with $1 million to deposit can obtain the remaining $2 million in liquidity from a bridge facilitator, enabling the entire position at 3x leverage. Similarly, when the user intends to unwind, the facilitator provides the required liquidity, solving the redemption delay problem.

Liquidity integrators provide instant liquidity when a user wants to exit immediately. Because even with a Bridge facilitator, the user has a $1 million deposit that must go through the entire redemption process, these integrators provide the much-needed liquidity.

Both of these approaches borrow efficiency from the market, just as liquidation works in lending, with motivated onchain actors filling the required gap in RWA looping for profit. Over time, systems like this become easier to scale because every participant has something to gain from the process: loopers get a smooth exit, and facilitators earn a profit by providing liquidity and faster redemption for users.

Fission

Fission is another instant RWA redemption protocol and currently supports instant redemption of assets such as ACRED, ACRDX, and JAA. While the product aims to address an active issue with RWAs, it charges a 564 bps fee, which is significantly higher than that of any other platform. Additionally, it lacks sufficient liquidity, making it an inefficient venue for asset swaps, as users would incur high slippage and fees.

The redemption of RWAs is a relatively new area, with most products launched in the last few months. While the efforts are in the right direction, these platforms face a “chicken-and-egg” problem.

As they try to provide instant redemption for RWAs, they themselves lack liquidity, which sometimes makes them inefficient venues for trades. As this niche grows, liquidity is expected to deepen because duration risk offers a good risk/reward profile for liquidity providers.

To enable DeFi composability, the backend consists of vault standards. In the next section, we discuss multiple available standards and what they offer.

Vault Standards

The vault standards determine the composability ceiling for any RWA product. There are currently four active standards:

ERC-4626: ERC-4626 is the de facto DeFi yield-vault standard. The standardised deposit(), withdraw(), and convertToAssets() functions create a universal interface. Multiple protocols, such as Morpho, Euler, Fluid, Aave, and other major lending protocols. But the vault must honour redeem() call synchronously, which demands T+0 settlement, making the standard feasible only for onchain native assets like syrupUSDC, wmtUSDC, and others.

ERC-7575: This ERC is a multi-asset extension of ERC-4626 and supports vaults in which a single share token can be deposited/withdrawn in multiple assets (e.g., deposit USDC or USDT and receive the same share token). It is particularly relevant for the RWA product that accepts multiple settlement assets. Additionally, it is fully backwards-compatible with ERC-4626 integrators, adding flexibility without any additional engineering costs. This improves on the ERC-4626 rigid standard, which would require depositors to convert to a specific asset before depositing or to introduce multiple assets per deposit, creating fragmentation.

ERC-7540: Introduced in October 2023, ERC-7540 extends ERC-4626 and introduces asynchronous redemption, a product specific to RWA offerings. It has functions such as requestRedeem() and claimRedeem() for cases that require a waiting period (T+1, T+2, or an arbitrary delay). This ERC is perfect for Treasury products, tokenised private credit, or any RWA with a defined settlement window. Additionally, users still bear duration risk because the NAV could change between the request and the claim, affecting their position’s value. This ERC is widely adopted and promoted by infrastructure providers such as Centrifuge, which is also its developer, with many assets utilising it on platforms like Aave, Euler, and Morpho.

There is a great development regarding vault standards as well, aimed at addressing various issues with the most widely adopted standard, ERC-4626.

Another interesting standard is ERC-3643, developed by T-REX and is the compliance-first standard, which introduces onchainID. Every transfer of assets that adopts this standard requires whitelist verification against KYC’d addresses. It is adopted by asset issuers like KKR, Hamilton Lane, and Apollo, which use Securitize infrastructure. Additionally, it is functionally incompatible with standard DeFi: Morpho vault addresses, Aave pool addresses, and Uniswap pool addresses are all non-KYC’d and cannot receive ERC-3643 tokens. Only specialised compliance-aware wrappers (Ember’s sACRED, Securitize’s own bridge) can interface ERC-3643 with DeFi, adding a wrapper counterparty risk layer.

Find the complete report here:

https://docsend.com/v/sjv2g/rwareport

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram guy, you can read all of our research without the noise on our TG channel: