DeFi Will Win

This report is an excerpt from the EOY Report we published in collaboration with OAK Research and Hazeflow.

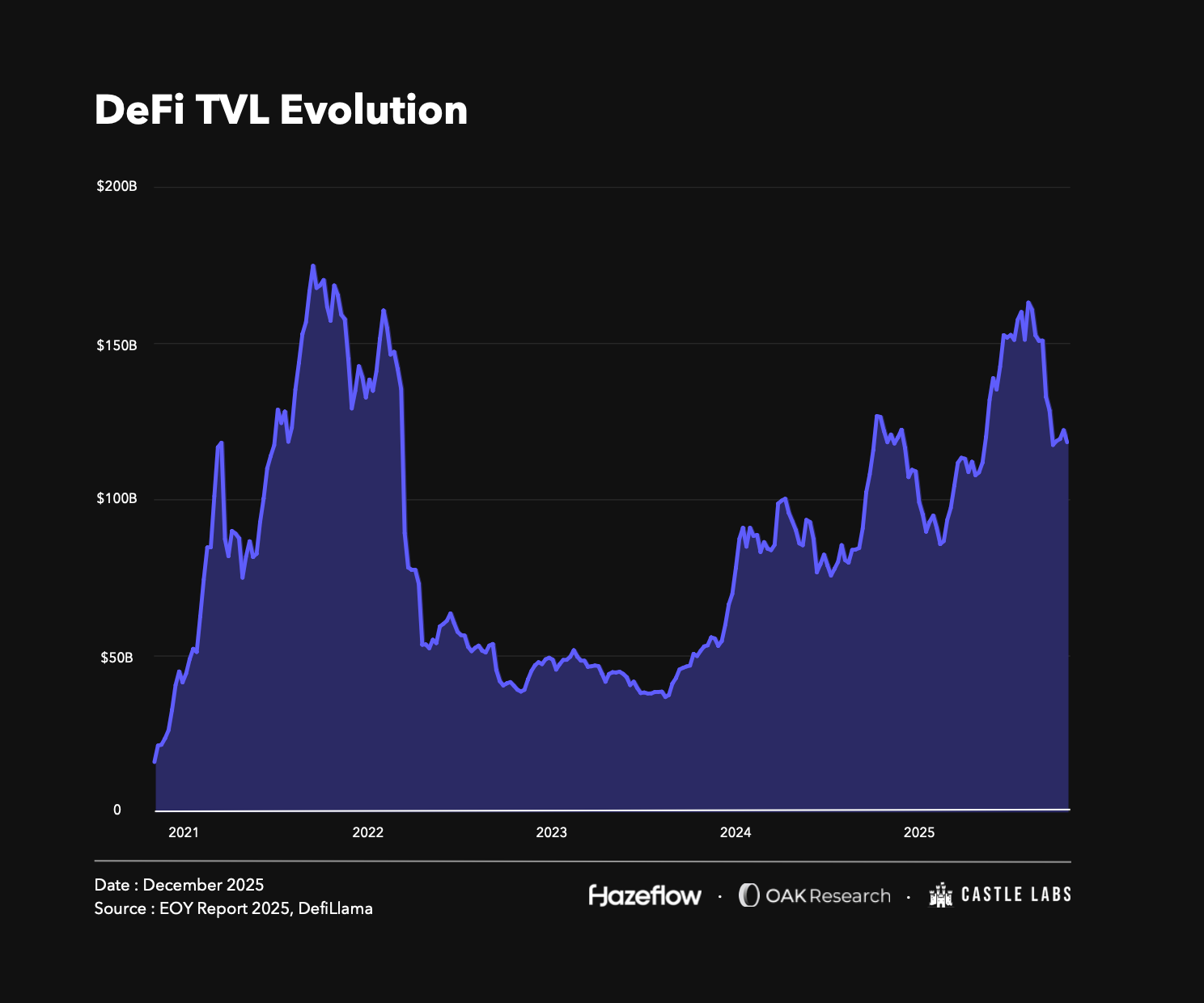

DeFi has seen, over time, the good, the bad, and the ugly phases. Currently, it has sustained a particular level and is in a higher-highs, higher-lows pattern across key metrics, indicating sustained growth. Many of these TVL patterns depend on asset prices, since most DeFi TVL is composed of volatile assets, and any movement in those assets can affect key metrics.

At the time of writing, we are at a higher TVL than we were at the start of the year. The difference between these two numbers is minimal, and we saw a peak around October, when we witnessed all-time-high prices for the key assets. This was before the October Liquidation Event, which led to $19 billion in liquidations. Since then, a few protocols have blown up, leading to a ~28% decline in total TVL and lower token prices.

Nonetheless, this part of the report is not just about the blow-ups and harsh liquidation cascades but all the different things we experienced in DeFi this year, the growth, the changes, and so much more.

2025 DeFi Landscape

There were quite a few winners across the year who were trending on the timeline and had a fair share of mindshare. This includes both protocols and categories. While it is hard to include all winning protocols, we have selected a few to shed some light on them.

Winning Protocols

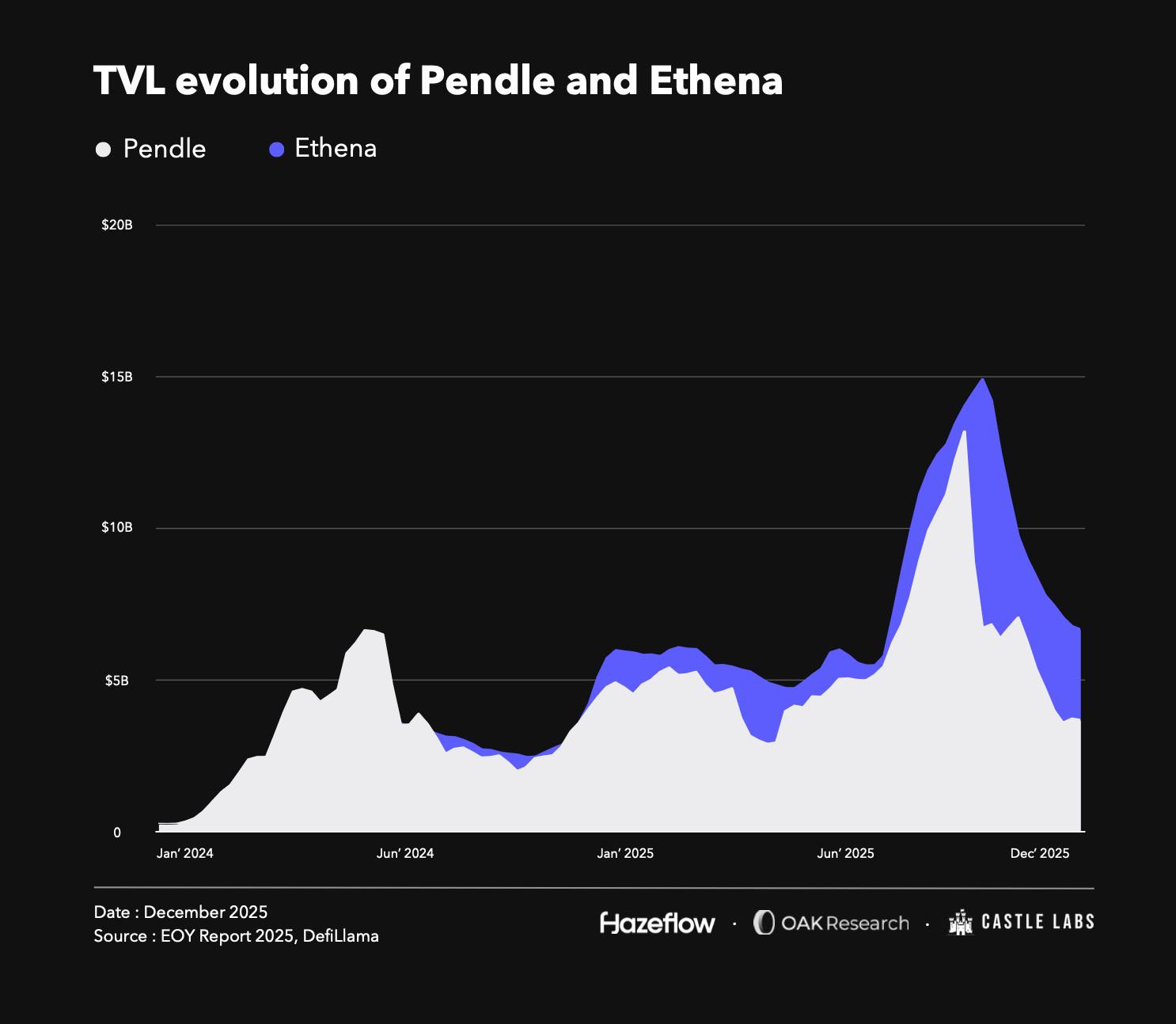

First and foremost, 2025 was the year of yield, and within the category, the dominant player is Pendle. The protocol separates yield-bearing assets into two components: the principal (PT tokens) and the yield (YT tokens). The yield component can be traded independently, while the principal is preserved and redeemable at maturity. This unique proposition, along with its multiple partnerships with other protocols such as Ethena and Aave, helped it grow its TVL.

It is important to note that the Pendle TVL is currently not at an all-time high and is lower than it was at the start of the year, with a peak around mid-September. The primary reason for this was the launch of Plasma, which incentivised users to unwind their positions on other platforms and bring their assets onto its chain, leading to a decline in value locked. But the fundamentals remain strong, and Pendle has carved out a prime position as a yield distributor.

The other protocol Pendle has been focusing on to expand its yield services is Boros. Boros is designed to hedge the funding rate exposure or trade it with leverage by shorting or longing Yield Units (YU). YU represents the yield on 1 unit of collateral asset from issuance to maturity. For example, 1 YU-ETH is equal to the Yield from 1 ETH notional value until maturity, similar to how YT (Yield Tokens) work on Pendle.

Adding to the list, Ethena has made its mark this year. Ethena provides a synthetic dollar (USDe), a yield-bearing asset that accrues its yield from basis trading. Volatile assets, including BTC, ETH, and LSTs, back Ethena’s stablecoin USDe. To operate in a delta-neutral environment, Ethena hedges these volatile assets held as a spot position and uses them as margin by subsequently opening a short perpetual position. While the delta of Ethena’s positions is neutral, it earns its yield from the favourable funding rates that the long positions pay to the short positions.

Similar to Pendle, Ethena also lost TVL in the second half of the year. The significant drop in its TVL occurred after the October Liquidation Event, when it was at its peak. The primary reason for the decline was that USDe was depegged on Binance, leading to USDe-backed positions being liquidated and cascading effects on the value locked in the yield-bearing asset. The token didn’t actually depeg, and its backing remained secure. The Binance case was a standalone case due to the oracle configuration and thin liquidity on the pair. Though on other platforms like Aave, the positions didn’t budge due to the hardcoded price feed for USDe to USDT.

Ethena’s moat is strong and scalable. They have recently been focusing on a Stablecoin-as-a-Service model, including launching a stablecoin for a specific use case. They have partnered with MegaETH, Jupiter, and Sui to launch native stablecoins through this model. This helps protocols accrue value routed outside the ecosystem to players like Tether and Circle, which generate billions in revenue, none of which goes back to the chains or protocols these stablecoins sit on.

Additionally, Ethena has been focusing on expanding its token’s use case, with the recent launch of HyENA, a USDe-margined perpetual DEX built on Hyperliquid’s HIP-3 standard. This is unique because traders can now earn a good APY on their margin, whereas other stablecoins wouldn’t yield anything. For the moment, Hyena works on an invite-only basis, and if you want to access it, you can use the code OAK to try out the platform.

With a focus on expanding its core services and creating more use cases for its existing offerings, Ethena is well-positioned to gain market share in the stablecoins category in the coming years.

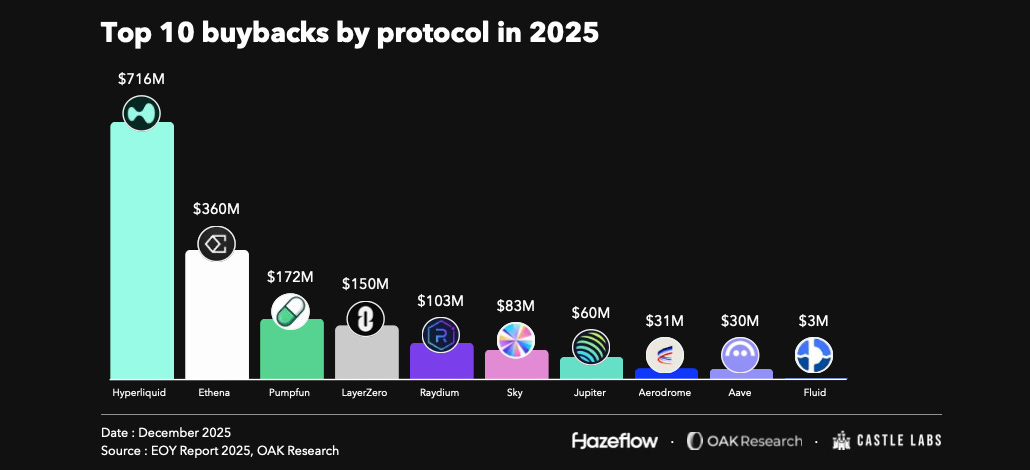

While mentioning the winning protocols, Hyperliquid has been at the top of every metric this year. After a successful token launch, it became one of the best onchain venues for trading perpetuals. They also made a ton of revenue and fees in between and routed it all to their token buybacks, which gained billions in valuation as a result. Hyperliquid aims to house all the finance and is walking its path with updates like HIP-3 and the launch of HyperEVM. We also have a dedicated section in the report on the protocol, focusing on its growth in more detail.

Winning Categories

It would be fair to highlight that the protocols that succeeded belonged to the categories that were outperforming. Two such winning categories include Perpetuals and Stablecoins, both of which have found a strong product-market fit (PMF) with sustainable demand.

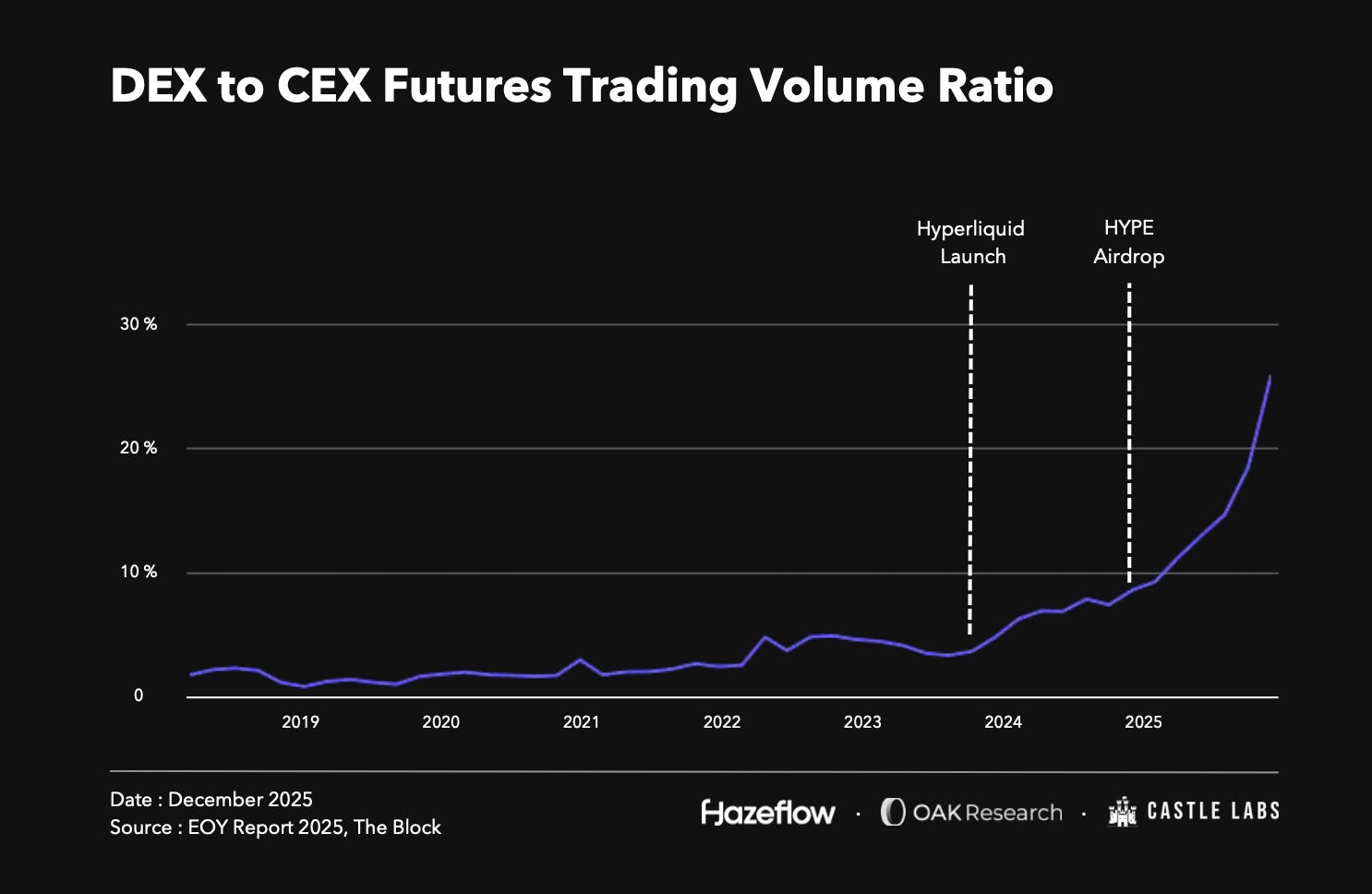

Perpetual Trading has been a crucial part of the crypto market for a long while now. They handle billions of dollars in daily volume, but before this year, most of that volume occurred on CEXs. This equation really started to change with the emergence of Hyperliquid and its massive airdrop in late 2024, and interest in perpetuals was once again up. With that, competition rose. This surge in competition led to DEX-to-CEX trade volume reaching an all-time high of around 18% at the time of writing. Now, multiple protocols are being built in this category, aiming to capture market share from the rise of onchain perpetual trading, such as Lighter, Aster, Extended, Pacifica, and more.

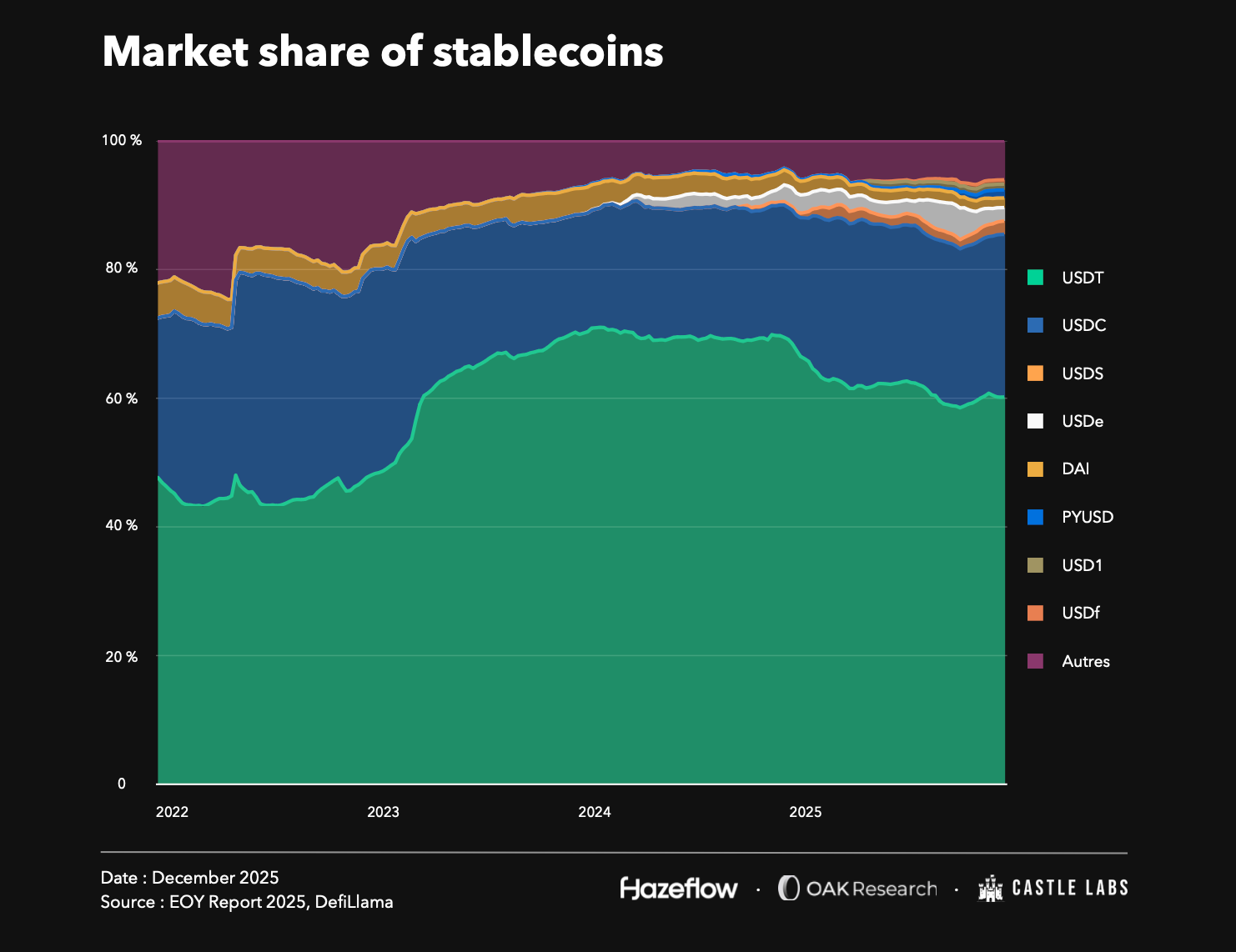

Another winning category is stablecoins with an upward-only market cap chart. The total stablecoin market cap currently sits at ~$309 billion. Upon comparing with the start-of-year value, we have gained over 50%, up from $200 billion. Over the years, the demand for stablecoins has only increased, with over 300 stablecoin issuers signalling rising competition.

Even with so many issuers, most of the stablecoin market cap is held by two issuers, Tether (USDT) and Circle (USDC), which together represent 85% of the market, followed by protocols like Ethena (USDe) and Sky (USDS). Tether and Circle have sustained their dominance even amid an influx of new issuers, thanks to their market timing and deep integration across every blockchain and protocol.

This dominance has created the problem of routing value outside the ecosystem in which it originated, to external entities. Tether and Circle, combined, have generated ~$700 million and ~$240 million in revenue over the last 30 days, driven by their usage across multiple chains and protocols. To address this problem, Ethena launched a Stablecoin-as-a-Service model to help blockchains retain the value created rather than route it out. At the same time, it is very hard to kill their dominance because they are deeply integrated within the ecosystem.

October Liquidation Event

The October Liquidation Event, also known as the Crypto Stress Test, occurred on the 10th and resulted in over $19 billion in liquidations. The reason for this event was Trump’s announcement of 100% tariffs on China in response to China’s restrictions on rare earth exports and its announcement of broad export controls on its products. A few weeks after this announcement, JPMorgan made another announcement that Strategy could be excluded from the MSCI index, which was initially shared only through an internal memo with US banks.

This led to a drop in all asset prices. Significant assets such as BTC and ETH have since then declined by 23% and 33%, respectively. The crypto market cap fell from $4.24 trillion around October 10 to $3.16 trillion at the time of writing, a 25% decline.

On platforms like Binance, USDe (a yield-bearing stablecoin issued by Ethena) depegged because it was using the exchange’s spot prices, which had lower liquidity, leading to unfair liquidations of users’ positions. The exchange eventually paid out over $280 million in reimbursements to users affected by this and other similar incidents, including assets such as BNSOL and WBETH.

DeFi lending protocols performed as expected, liquidated, and accrued no bad debt during the cascade. In total, protocols such as Aave, Morpho, Fluid, and Euler liquidated over $260 million with almost no bad debt.

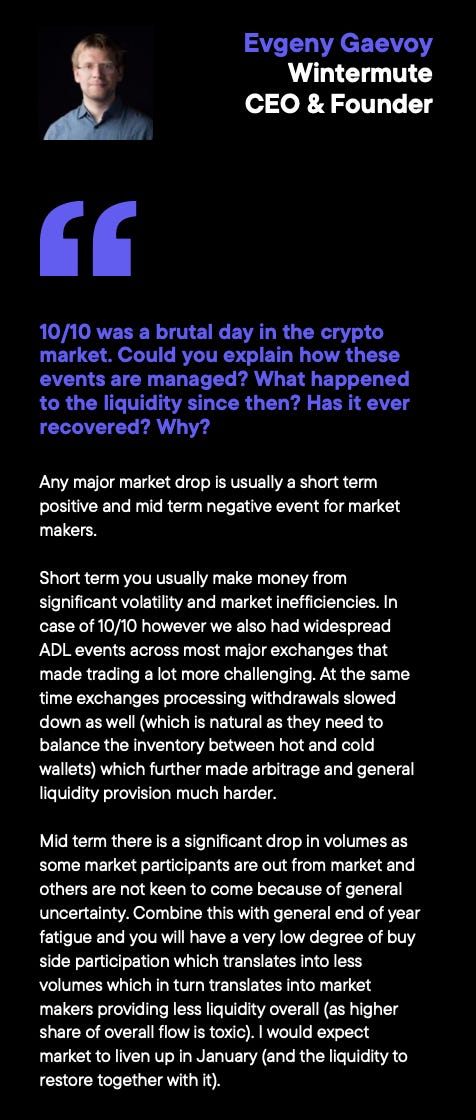

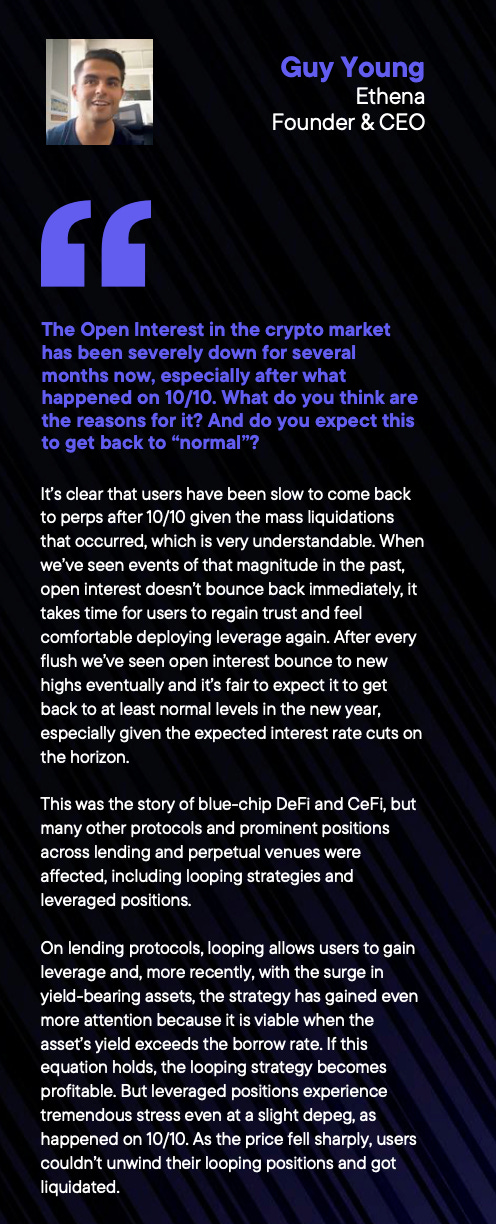

This was the story of blue-chip DeFi and CeFi, but many other protocols and prominent positions across lending and perpetual venues were affected, including looping strategies and leveraged positions.

On lending protocols, looping allows users to gain leverage and, more recently, with the surge in yield-bearing assets, the strategy has gained even more attention because it is viable when the asset’s yield exceeds the borrow rate. If this equation holds, the looping strategy becomes profitable. But leveraged positions experience tremendous stress even at a slight depeg, as happened on 10/10. As the price fell sharply, users couldn’t unwind their looping positions and got liquidated.

Though there were many incidents of users being eaten by leverage, some stood out, such as Stream Finance, which showed that chasing too much yield is not good in the first place.

We dive deeper into it in the next section.

Are stablecoins truly stable? The Stream Finance Incident

In the last quarter of the year, several stablecoins collapsed due to poor mechanics. They could have kept this going for even longer, but the October Liquidation Event swept up some of the overleveraged stable assets. The ones that came in light and were the largest in size among others were xUSD (Stream Finance) and deUSD (Elixir). Both of these coins were interlinked and collapsed together.

In the case of Stream Finance, they were selling an overleveraged, undercollateralised trade wrapped in a stablecoin, xUSD. Whenever a user deposited collateral into their protocol, they minted xUSD, swapped the user’s deposit into deUSD from Elixir (which also had a high APY), and then deposited the deUSD across lending protocols like Euler and Morpho.

By borrowing capital against their deposit, they didn’t run a simple loop: they minted more xUSD, inflating its supply to over 7x synthetic exposure, with only $1.9 million in verifiable USDC collateral representing $14.5 million in xUSD.

They also had some offchain dependencies which users weren’t aware of. During the 10/10 liquidation event, their prominent offchain positions were liquidated as well, leading to the collapse and a $93 million loss, after which they closed their withdrawals. This withdrawal closure panicked xUSD holders, who sold their assets in secondary markets with thin liquidity, causing the token to lose its peg very quickly. Following a similar timeline, Elixir’s deUSD also depegged, but they were able to process redemptions for most users.

All the vaults and their managers that were exposed on lending protocols like Euler and Morpho to these stablecoins took a hit. Even protocols got hit with bad debt because they were using Fixed-Price Oracles that hardcoded the price of these assets to $1 while they were de-pegging in the real market. There is no optimal solution for pricing such assets; protocols can use a Proof-of-Reserves oracle, but in most cases, the backing of such stablecoins is overleveraged or simply opaque, as with xUSD. At the end of the day, it’s users who are getting in on such trades to earn high APYs; they need to invest with due diligence, as these are risky investments.

The Pivot To Fundamentals: Revenue is King

Revenue is the core of every business. If a protocol makes money and has good value accrual mechanisms for its token holders, everybody goes home happy. However, obviously, there are many caveats, and token holders usually suffer. Before we go into the value accrual, let’s understand where most of the revenue in crypto is situated.

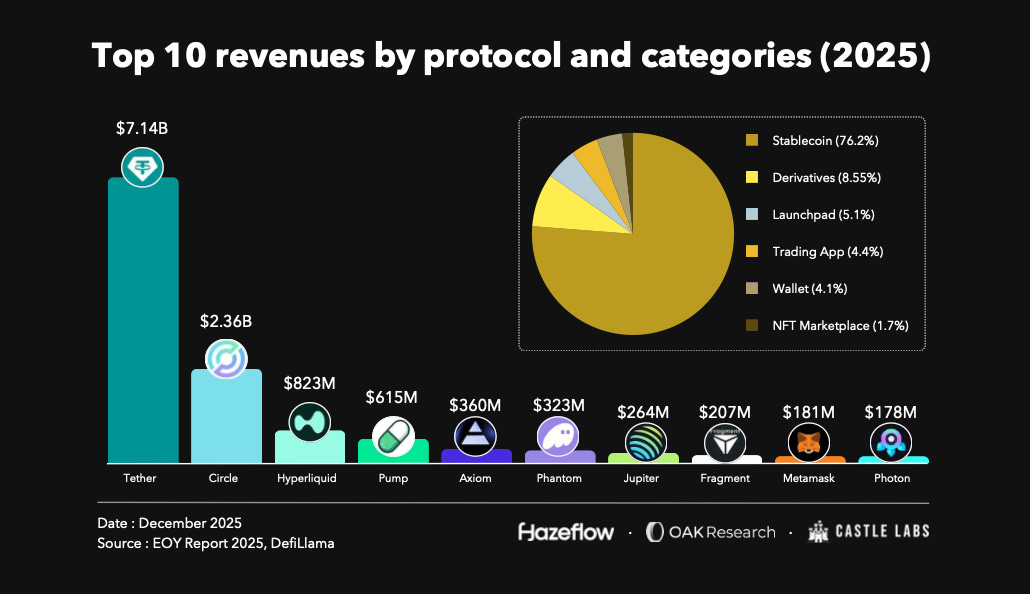

If we focus on the top 10 protocols by revenue over the last one year, stablecoin issuers account for ~76% of the revenue share, followed by derivatives, launchpad, trading apps, and more.

Stablecoins have always been the best revenue-generating business in crypto because they are used everywhere, they serve as the foundation of DeFi, and enable money to flow in and out of the system. Following that, Derivatives and Launchpads drive another significant share of revenue.

Tether and Circle combined generated $9.8 billion in revenue over the last year and have consistently witnessed similar revenue numbers. Following them, the list includes Hyperliquid and Jupiter in the derivatives category, which cumulatively contributed $1.1 billion in revenue.

Apart from these already winning categories, protocols like Pumpdotfun also have a sustainable revenue stream. Additionally, it is worth noting that some of the protocols listed below launched last year and are new comparatively, reflecting readiness to explore alternatives. At the same time, incentives contribute significantly to a protocol’s performance and draw that initial attention that might stick for the features.

The UNIfication Proposal

Before this proposal, one of the largest DeFi protocols, Uniswap, had its token misaligned with its revenue-generating capabilities due to regulatory constraints. The proposal burned 100m UNI tokens from the treasury, representing the protocol fees that would have been burned if fees had been enabled at the token launch. Additionally, it enabled protocol fees and used them to burn UNI tokens and stop collecting fees on its interface, wallet, and API.

This would mean the protocol’s growth will be more aligned with its governance token. More and more projects are focusing on this alignment and trying to route as much value as possible to token holders.

Buybacks as the Meta

Earlier, token performance in crypto depended on how well the marketing was done, and, generally, users wouldn’t pay much attention to the protocol’s economics. While this is good for someone with a short-term investment framework, it doesn’t work in the long term. Whoever held the tokens of such projects was never able to exit. Instead, the economics and revenue of the protocol now carry the most weight, whereas before revenue was not treated as a primary driver; speculation was.

A major driver of this change was also the launch of HYPE and its value accrual mechanism. 99% of the protocol’s revenue goes to the assistance fund, which conducts HYPE buybacks, thereby renewing interest in perpetuals because Hyperliquid has set such high standards. These buybacks have provided strong price support for the HYPE token and contributed to its growth.

Not only Hyperliquid but also multiple blue-chip DeFi protocols, such as Aave, Maple, and Fluid, have started conducting buybacks. Buybacks are a good mechanism to share revenue with token holders. Still, they work only if the project has sustainable revenue sources; hence, they work well with mature protocols but might fail with new ones, as the protocol’s initial growth should be prioritised.

Aave has used ~$33 million in buybacks since the program started in April.

Following a similar trajectory, Fluid has completed ~$3 million in buybacks since October, directing its revenue to tokenholders.