Ethena Just Killed Its Own Business Model: The Castle Chronicle

Plus: WLFI heads to court, 90% of VCs are gone, Morgan Stanley enters the ETF war, and we go on the record with 1inch's co-founder

Welcome to another week of extreme fear for Bitcoin!

We have now been in the extreme fear zone of the Fear and Greed Index for over 47 days, the longest stretch since mid-2022.

In addition to this, the situation in the market is extremely dire:

Markets priced out every rate cut for 2026

There is a war in the Middle East

A new U.S. naval blockade in the Straits of Hormuz

Despite sentiment at lows, Bitcoin is trading at $75k today, up 1.5% over the last 24 hours, whilst crypto ETFs pulled in $1.32 billion in March, breaking a four-month outflow streak.

We’ll start this 167th Edition of The Chronicle with the main events of the week: dive into crypto VC, WLFI vs Justin Sun and Morgan Stanley entering the BTC ETF race.

Then we have a lot of original content: our analyst sharing his take on prediction markets and an interview with 1inch’s co-founder.

Ethena slashes perp exposure from 90% to 11%

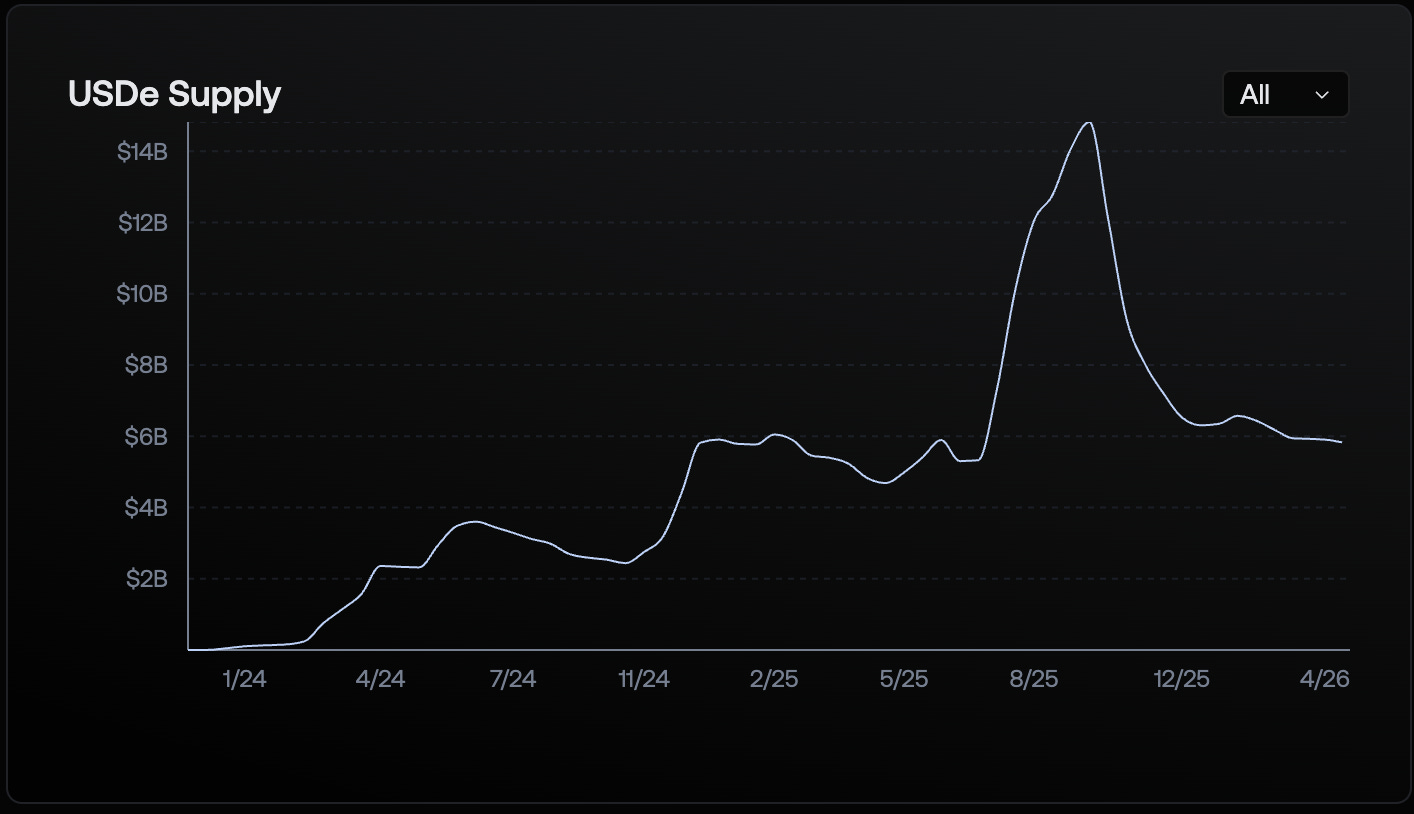

Ethena, the issuer of USDe, just made the most significant change to a stablecoin’s reserve structure in years, cutting its exposure to perpetual futures from 90% to 11%.

This is a huge pivot for Ethena: they are aiming to replace it with institutional lending products through Anchorage, Maple, and Coinbase Asset Management, as well as RWAs and structured credit, paving the way towards becoming a prime brokerage.

USDe grew to $10 billion in TVL faster than any other stablecoin in history on a fairly simple yet elegant model: Hold spot crypto whilst shorting perps and capture the funding rate.

This strategy thrived in 2024 and 2025, when the market was leveraged long, and funding rates were positive. As the cycle turned, funding rates went negative. This resulted in USDe supply dropping from nearly $15 billion at its peak to under $6 billion today.

The new Ethena will look quite different: TradFi allocators aren’t seeking exposure to the funding-basis trade; they want access to the products they’re used to, and that’s what Ethena is building.

The same applied to other DeFi protocols, with similar steps aimed at being more appealing to institutions.

Undeniably, this will cause some friction between the previous core user group and the future one during this migration period, as the USDe example shows us.

The risk profile of this product has fundamentally changed: Perp funding rates carry crypto-native risk, whereas institutional lending and structured credit carry counterparty and credit risk.

USDe holders will have to decide which risk profile they are aligned with.

WLFI vs Justin Sun is heading to court

Now onto the weekly drama!

Turns out, World Liberty Financial deposited 5 billion of its own governance tokens into Dolomite, a lending protocol co-founded by a WLFI adviser, and borrowed $75 million in stablecoins against them. This has drained the Dolomite USD1 lending pool to near-100% utilisation, trapping ordinary depositors who can’t withdraw until WLFI repays.

Justin Sun, once one of WLFI’s biggest backers, went public, accusing the project of extracting value for insiders.

WLFI’s response, “See you in court”, is already a meme.

“Aave Will Win” passes the DAO vote

Now onto DAO governance. The Aave drama has been going on for months. Is it finally over?

The “Aave Will Win” proposal passed this week with a significant majority, formally restructuring Aave Labs as a DAO subsidiary and redirecting product revenue to the treasury.

This follows V4’s mainnet launch on March 30.

Since this proposal’s creation, we have seen three large service providers leave Aave, all of whom were instrumental in the development and growth of Aave V3. To date, BGD Labs, ACI, and Chaos Labs have all departed.

What’s next for Aave?

90% of crypto VCs have disappeared

Tom Dunleavy posted data this week showing that active VCs deploying capital dropped from over 5,300 in 2022 to fewer than 400 today, and predicted that fewer than 20 firms are writing early-stage cheques.

For those interested in the matter, Krate27 compiled a spreadsheet of remaining active funds from the thread responses.

This behaviour is not surprising, just as we are seeing consolidation across protocol teams and products, the capital behind it all is also consolidating

Morgan Stanley launches a Bitcoin ETF and undercuts BlackRock

Morgan Stanley launched MSBT, becoming first US bank-affiliated asset manager to issue a spot Bitcoin ETF.

The ETF launched on NYSE Arca with ~$34 million in first-day volume and a 0.14% expense ratio, roughly half of BlackRock’s IBIT.

Now, Morgan Stanley’s advisors managing $9.3 trillion in client assets can recommend an in-house product rather than sending flows to a competitor.

INFINIT brings prompt-to-DeFi to BNB Chain

INFINIT launched its Prompt-to-DeFi Strategist Challenge on BNB Chain, where users create yield strategies in plain language, and AI agents handle the execution.

They recently expanded their partnership with BNB, integrating Venus Flux, Aster, PancakeSwap, Pendle, and Lista.

If you want to try building a strategy yourself, they currently have a challenge where anyone can create strategies live athttp://app.infinit.tech/en/prompt

Amundi’s tokenised fund hits $400M in three weeks

Amundi, Europe’s largest asset manager at €2.3 trillion AUM, launched a tokenised overnight fund on Ethereum and Stellar via Chainlink. In just three weeks, it became the fastest-growing tokenised fund on record, growing to $400M in AUM.

Tokenised Treasuries now total nearly $13 billion, indicating a clear shift from experimentation to production among these asset managers and funds.

Seeing Things Inverted

Noveleader from the Castle team on a trend worth watching.

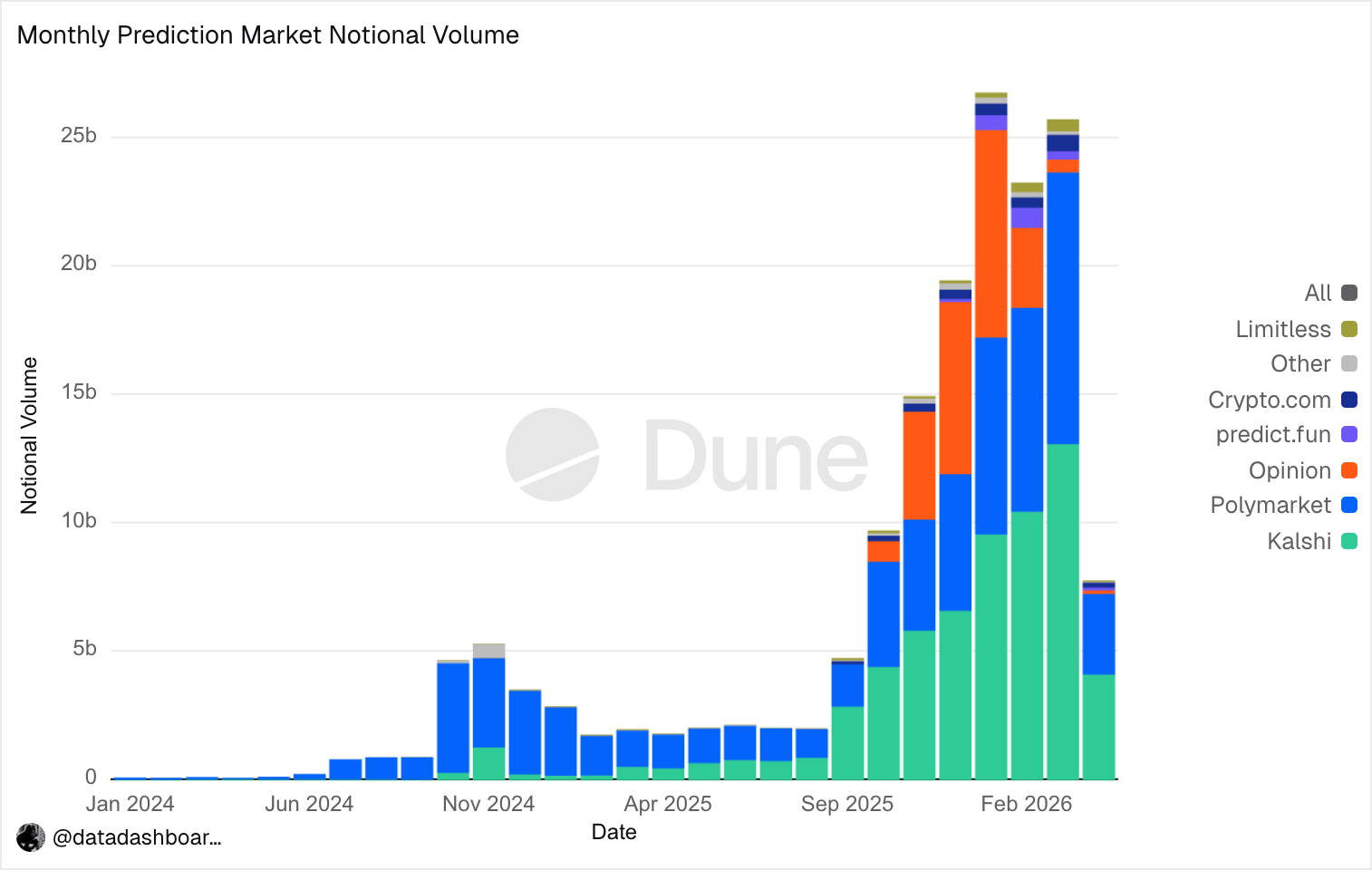

Prediction Markets are growing exponentially; they are breaking their own records and reaching ever-higher volumes every month.

Last month, they did $25 billion in volume, and these instruments don’t even have leverage; they are simply the tools to express one’s opinion about anything. I agree we do have certain bots we deploy on the markets around BTC price that sometimes try to leverage the latency arbitrage of these markets, and sometimes deploy an actual strategy.

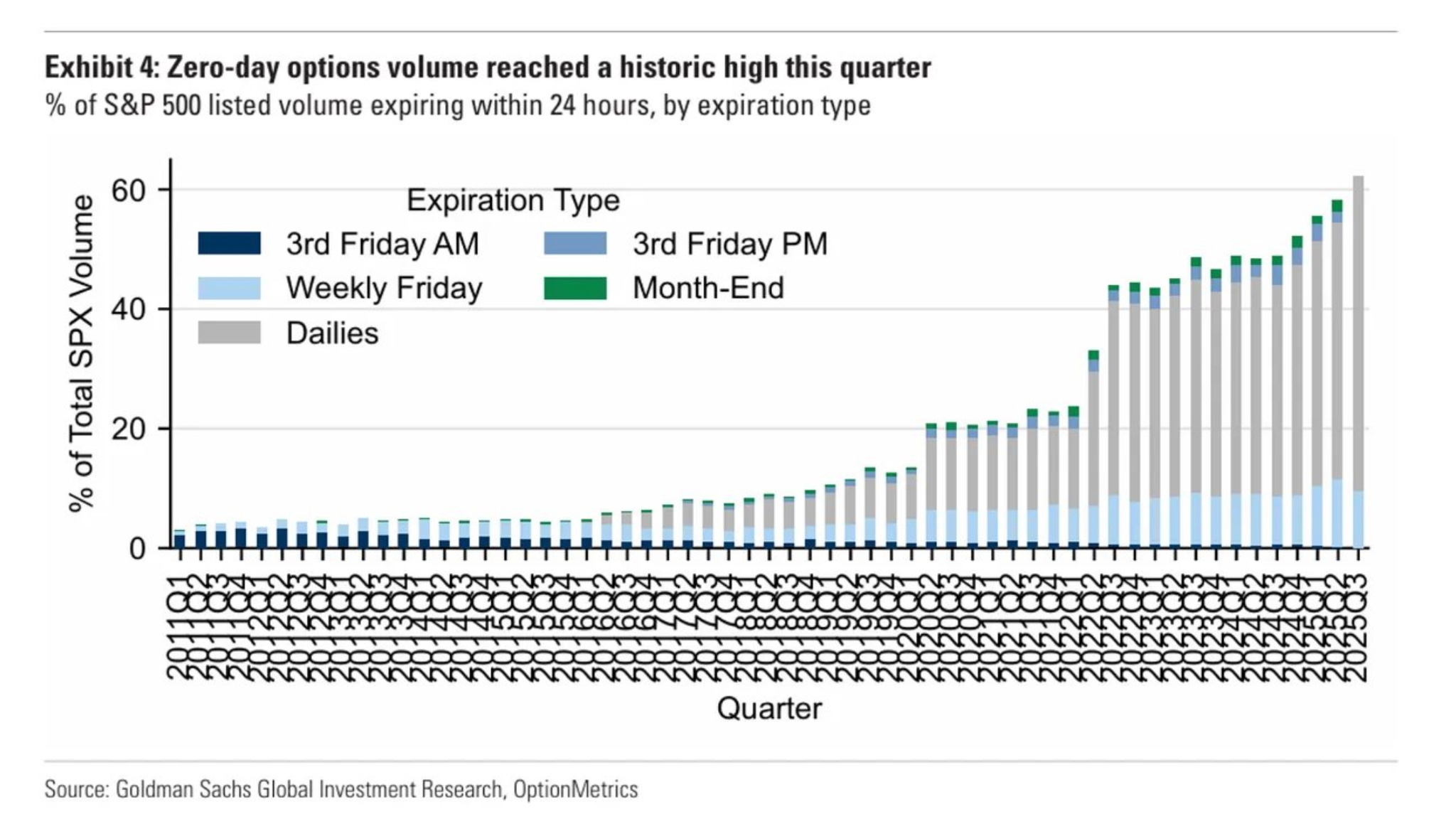

In TradFi, people are not stopping either, and 0DTE is gaining popularity. While I don’t have the latest stats, these options instruments are now a major contributor to volumes, and the numbers are just increasing from here.

Very few people would shed some light on this, but this is the point we call Hyperfinancialisation. I talked about it in one of my pieces last year, and things are becoming way worse.

This is sad, and the trend is not just noticeable among PMs or 0DTEs; it is also evident in the increasing volume of perpetuals, futures, and options. The innate nature is to gamble now to make it in life in a shorter span of time. Honestly, there is no one to blame. Inflation sucks; houses are getting more expensive by the tick of the clock; rent isn’t cheap; and it takes years to get out of college tuition debt, only to wrangle into a mortgage afterwards.

There is no solution unless the system completely evolves, and until then, the numbers associated with any form of gambling or speculation will keep rising, uninformed investors will keep losing money, and things will keep getting expensive.

Welcome to the state of Hyperfinancialisation, where everything will eventually become a market.

Why 90% of DeFi liquidity is doing nothing

At EthCC, we sat down with Sergej Kunz, co-founder of 1inch. One thing he said stuck with us and connects directly to what we’ve been talking about in this edition.

“80-90% of liquidity in traditional AMMs is idle. Protocols competing on TVL are competing on quantity, not quality.”

His point is simple: a million dollars in a Uniswap pool can’t simultaneously earn yield elsewhere. It’s locked, doing one thing. Multiply that across the entire industry, and you have billions of dollars sitting dormant while protocols fight to attract more of it.

1inch’s answer is Aqua, an intent-based liquidity protocol. Instead of locking capital in smart contracts, users sign intents expressing willingness to provide liquidity at specific terms, and market makers settle against them. Your assets stay in your wallet. One pool of capital works across multiple strategies simultaneously.

“Curve and Balancer will need to adapt or disappear,” he told us. He’s already in direct conversations with both teams about becoming strategy providers on Aqua rather than competing with it. Aqua is globally patented, backed by $700K in audits, and he estimates 18-24 months before the flywheel kicks in: enough market maker liquidity settling intents at competitive prices to pull real volume from traditional pools.

But the bigger point was about what accelerates that timeline. “AI agents will drive the next big thing in DeFi adoption. UX is the real bottleneck, not liquidity.”

1inch already has a live MCP server that lets agents execute swaps.

Sergej believes in AI agents so much that he’s built his own, replacing OpenCLaw with his own harness using Claude and Cursor, running it on a Mac Mini at home for self-custody. It executes cross-chain swaps autonomously, and he’s extending it to manage Aqua liquidity positions. It’s great to see him applying self-custody compute in the same way we demand self-custody wallets.

If DeFi’s interface problem gets solved by agents rather than better frontends, the protocols with the best infrastructure APIs are the ones that win.

Aave V4 went live on March 30, but with deliberate training wheels: conservative supply and borrow caps across all three Hubs, with the DAO gradually increasing limits as the system proves itself in production. So don’t expect a sudden TVL migration from V3, but watch out for the changes on Aave Pro.

Ethena’s transparency dashboard currently shows that 89% of backing is in liquid stablecoins, positioning it for the transition to the new reserve structure. All new reserve initiatives are being independently assessed by the Ethena Risk Committee, with analysis published publicly. Worth following if you hold USDe or are evaluating the new risk profile.

The CLARITY Act Senate markup is targeted for late April, which will determine how yield can be distributed to stablecoin holders, something all asset issuers, exchanges, and distribution platforms are keeping a keen eye on.

Rough weeks make for good stories later. That's it from us. See you next Tuesday.

Don’t forget to join our Telegram channel for the latest updates from Castle and all our research: Link here

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn't guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.