From Neobanks to Onchain Banks

The digitalisation of banking has been one of the defining trends of the last decade.

From online banking to mobile banking, to neobanks, a term originally described digital-only banks with no physical branches, built from scratch rather than adapting legacy systems.

Nowadays, they all co-exist with the legacy banking sector.

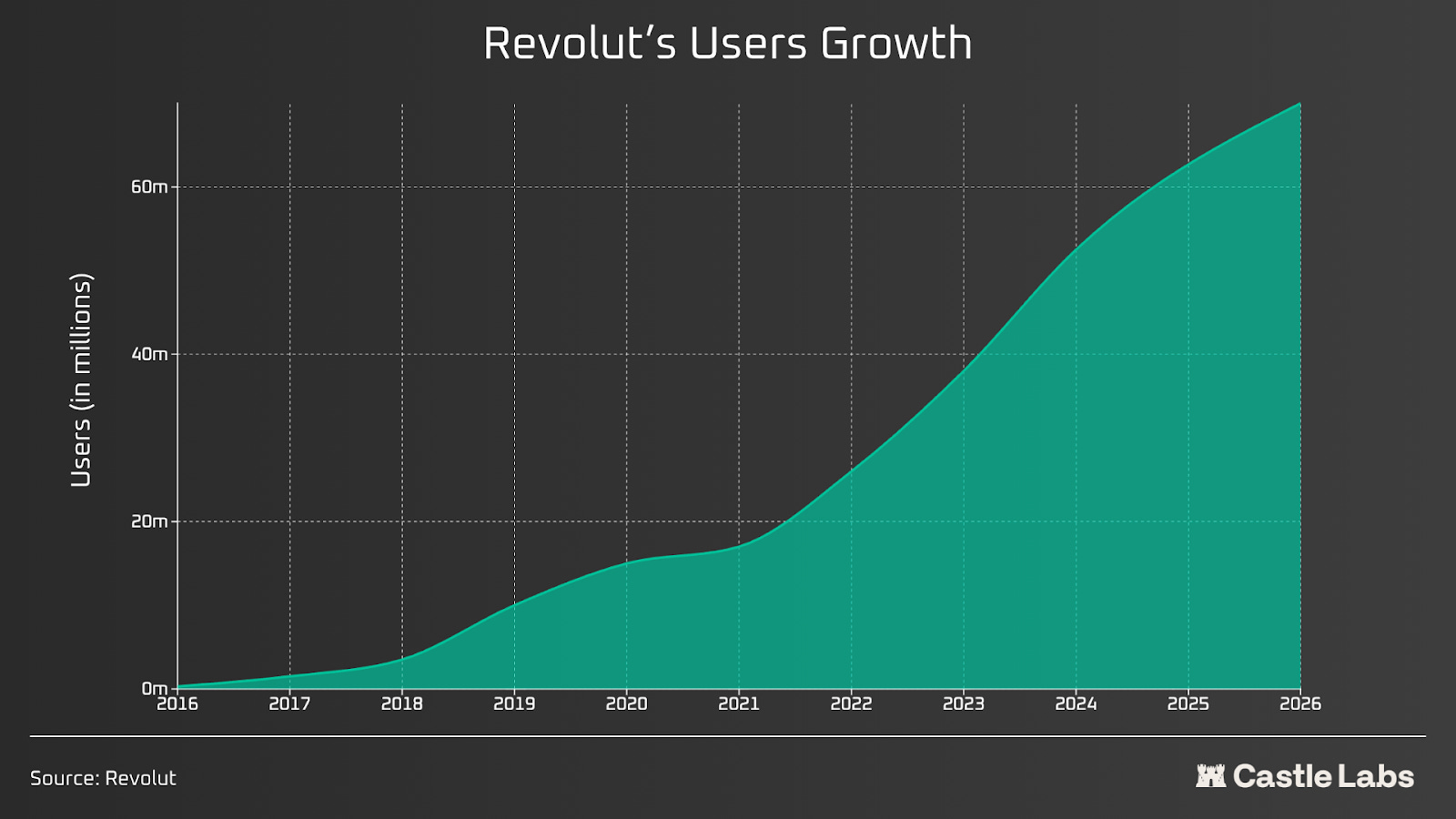

Some neobanks have been extremely successful, including Revolut, which started as a foreign exchange card for travellers and evolved into a multi-product financial platform that now serves over 50 million users globally, with $4 billion in annual revenue.

The global neobank market is valued at $148.9 billion and projected to exceed $4.4 trillion by 2034. Revolut’s transaction volume approached $1.3 trillion in 2024, proving that new entrants can compete with well-established banking monopolies.

Traditional neobanks promised to replace legacy banking but ended up running on the same rails: the same correspondent banks, the same settlement delays, the same custodial model, just with a better experience, using an app.

The underlying infrastructure is the same one that makes banking a hassle, dealing with intermediaries, agents, and compliance officers, regardless of how sleek the mobile interface looks. When Silicon Valley Bank collapsed in March 2023, it reminded its clients how precious a physical banker can be when a crisis looms and things go south. Without a reliable physical fallback, banking remains a remote, impersonal activity, much like DeFi hacks and exploits, which are more often than not left unresolved.

Dozens of crypto banks are live, while stablecoin supply has exceeded $308 billion. The clearest proof that this market is monetisable is RedotPay. Founded in Hong Kong in April 2023, the stablecoin-based payments fintech now processes over $10 billion in annualised payment volume. It raised $194 million in 2025 alone. By February 2026, Bloomberg reported that RedotPay was preparing a US IPO targeting a valuation exceeding $4 billion, with JPMorgan, Goldman Sachs, and Jefferies advising. According to data, RedotPay had $91 million in crypto card volume for November 2025 alone, second only to Rain at $240 million.

The architecture is closer to Revolut’s crypto top-up than to anything described below. RedotPay proves the demand exists. The protocols examined in this piece are building the architecture that could change banking.

The maturation of DeFi infrastructure has created the conditions for a new kind of bank, one where users could store, spend, grow, and borrow assets onchain, without intermediaries.

Crypto cards give users the feeling that they finally own their money without outside control, and increasingly, the infrastructure backs it up.

This article explores how these onchain banks differ from each other, and whether they offer the same guarantees, protect against operational risk, and satisfy compliance requirements, because offchain neobanks are radically different from onchain banks, and the comparison is almost misplaced.

From Neobanks to Onchain Banks

A neobank is a digital-only bank with no brick-and-mortar branches, built from scratch rather than adapting legacy systems. They exist on cellphones, within finger’s reach, but there is no physical presence except in corporate offices.

The evolution of the banking sector follows a clear (though slow) trajectory, with each generation building on the last, mirroring the technological paradigm of scientific discovery. However, crypto banks are far from the neobank model, and we will see how they differ from their elders.

Same Same but Different

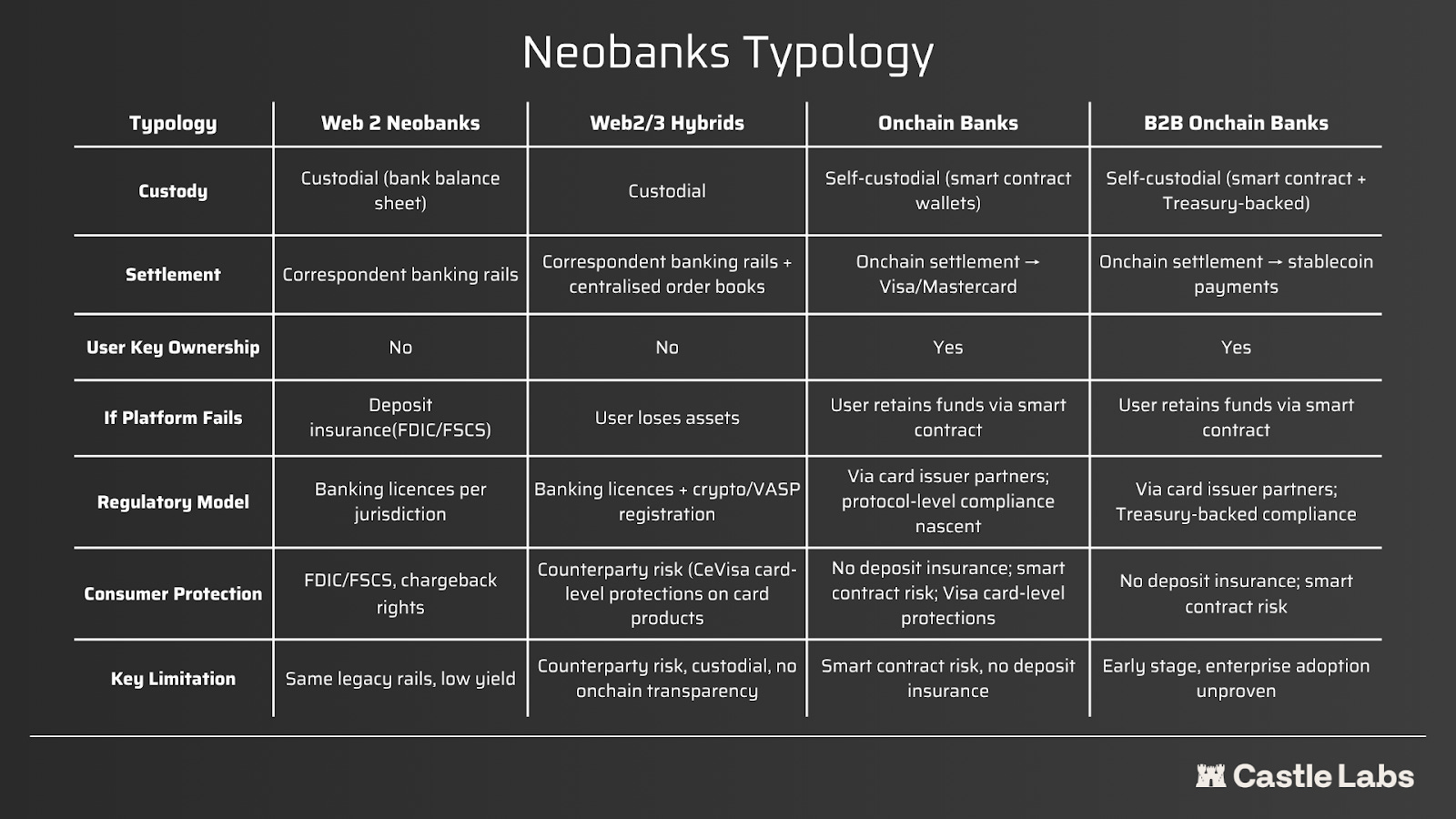

Web2 neobanks like Revolut, SoFi, and Nubank are mobile-first interfaces built on legacy banking infrastructure. Developing countries have benefited from digital banking services in remote locations where traditional banks such as HSBC cannot open branches. These platforms developed access and practicality, but not self-agency.

They are still custodial, with the bank holding the user’s money on its own balance sheet.

They are still dependent on correspondent banks for cross-border settlement.

They are still geographically limited by licensing regimes: Revolut has spent years and hundreds of millions of dollars acquiring banking licences jurisdiction by jurisdiction.

Built for convenience, the model remains centralised, controlled, and far from private in practice.

Web2/3 hybrids like Xapo, Nexo, and Matrixport represent the first attempts to bridge traditional and crypto banking. They offer fiat and crypto in one application, but the underlying model remains largely custodial. Users can hold Bitcoin alongside pounds and euros, but the platform controls the keys and manages the assets. In the backend, these platforms run omnibus custody, in which they pool user funds, use centralised order books for crypto trading, and settle fiat via the same correspondent banking rails as Web2 neobanks. The difference from Web2 is asset class access, not architecture.

These platforms share similarities with centralised exchanges: even if the user can view their assets, those assets are held by a third party. If the platform collapses for structural or financial reasons, as happened with FTX, users lose their assets.

As such, Web2/3 hybrids inherit the counterparty risk of centralised platforms, the same risk model that produced Celsius or BlockFi, while offering only slightly more functionality than a standard neobank by supporting cryptocurrency assets.

Onchain banks like ether.fi Cash, Tria, and Superform represent the architectural turn. Built on smart contract wallets, integrated with DeFi protocols for yield on deposits, and connected to Visa and Mastercard through card infrastructure providers, they are composable and yield-bearing by design, with varying degrees of user custody depending on the product.

Users’ assets are held in smart contracts that guarantee self-custody, not on the platform’s balance sheet. Yield is generated through transparent DeFi strategies, not by banks rehypothecating deposits. Spending happens through onchain settlement routed to Visa or Mastercard. As Blocmates put it: “You do not store money with them; you use money through them.” The distinction is fundamental: it is the difference between trusting an institution and trusting a smart contract.

Both have different risk profiles, but a smart contract offers the benefit of eliminating human input entirely. If anything goes wrong with the platform, the user retains control over their funds at all times.

B2B onchain banks represent the furthest extension of the thesis. Dakota is building crypto-powered neobanking for businesses, offering corporate treasury management, payroll in stablecoins, and cross-border payments without correspondent banking delays, with deposits backed by US Treasuries, zero transaction fees, and yield generated through Treasuries and DeFi strategies.

The distinction is structural: with a traditional neobank, assets sit on the bank’s balance sheet. With a crypto-powered neobank, assets sit on a transparent, verifiable ledger, and the user retains ownership. Each generation has moved closer to direct user control: from digitising the interface, to adding crypto asset access, to eliminating intermediaries entirely. If this model proves to be adopted by businesses, and if it can satisfy the regulatory demands of governments and consumer expectations of safety, the entire financial stack can be deployed onchain.

But the question is not just whether onchain banks can supersede, or at least compete with established outfits. It is how they work in practice, starting with the most basic use case: buying a coffee at the local shop.

How Crypto Cards Get You a Coffee

One of the main value propositions of crypto neobanks is that they let you use your crypto for everyday purchases with a crypto card.

Crypto card spending has grown exponentially to $406 million in monthly volume as of November 2025, the highest on record, with Visa’s stablecoin-linked card spend alone reaching a $3.5 billion annualised run rate.

In this section, we explore the different crypto cards underlying infrastructures, with a simple example of buying a coffee.

When a user taps a crypto card at a coffee shop, what happens between the tap and the merchant receiving payment?

There are two distinct mechanisms in the market today.

Fiat Settlement

The standard model for spending purposes, used by Crypto.com or Binance Card.

The user taps the card, and the merchant terminal sends an authorisation request over Visa or Mastercard, identical to any normal card payment.

The card issuer’s system checks the user’s crypto or stablecoin balance, runs a fraud check, and if approved, automatically sells the user’s chosen asset at the real-time market rate and converts it to fiat. By the time the transaction reaches the card network, it is indistinguishable from any other card payment. Nothing from the merchant’s perspective changes, as he receives local currency as he would have with any other fiat transaction.

Who handles the conversion depends on the card’s infrastructure: programme managers like Baanx and Bridge convert the crypto to fiat themselves, then pass it to an issuing bank (Lead Bank, Cross River Bank), which settles to Visa. Full-stack issuers like Rain handle the entire chain, liquidating stablecoins and settling directly to the Visa network, which then routes the amount to the acquiring bank in the merchant’s desired fiat currency.

Stablecoin Settlement

Stablecoin settlement is growing rapidly but remains nascent and works differently. Rather than converting to fiat before settlement, the issuer settles its obligations to Visa directly in stablecoins over a blockchain. Visa launched USDC settlement for US institutional partners, allowing participating issuers and acquirers to settle VisaNet obligations in Circle’s USDC on the Solana blockchain.

The benefits for issuers are concrete: faster fund movement and 24/7 inter-institutional settlement on blockchain rails, without any change to the consumer card experience. Visa’s stablecoin-linked card spend hit a $3.5 billion annualised run rate in 2025, approximately 460% year-over-year growth, but still represents roughly 19% of total crypto card settlement volume. As of early 2026, native stablecoin settlement supports a limited set of assets, primarily USDC and PYUSD on Visa’s side, with Mastercard expanding to include additional stablecoins. USDT, the world’s largest stablecoin by market capitalisation, remains absent from Visa and Mastercard’s native settlement programmes.

Visa is also a design partner for Arc, a new Layer 1 blockchain developed by Circle, and plans to use it for USDC settlement and to operate a validator node.

The payment network layer is dominated by Visa, capturing over 90% of onchain card transaction volume. The divergence reflects different strategies.

Visa partnered early with emerging infrastructure providers like Rain and Reap, capturing crypto-native issuers through a single integration point that gave Visa exposure to dozens of card products, while Mastercard focused on direct partnerships with major centralised exchanges such as Revolut, Bybit, and Gemini.

To date, Visa has facilitated almost $100 billion in cryptocurrency purchases and over $25 billion in cryptocurrency spending, across a network of more than 150 million merchants and 14,500 financial institutions.

Between the user and the network sit two types of intermediaries, and the distinction determines how much margin each neobank captures per transaction.

Programme managers, companies that manage card programmes on behalf of issuers without holding direct network membership, like Bridge or Gnosis Pay, handle the crypto-to-fiat conversion but depend on issuing banks for settlement to the payment network. Baanx’s Crypto Life is the white-label programme manager behind the MetaMask Card, the Ledger Card, and others.

Full-stack issuance platforms, like Rain and Reap, hold direct Visa principal membership and own the entire stack: BIN sponsorship, lender of record, and network settlement, all in one product. By consolidating the existing card issuance stack into a single offering, Rain captures much of the value that is often lost to banks and other intermediaries. Rain is reportedly approaching a $2 billion valuation.

This is telling because a protocol built on Rain’s full-stack rails (like Plasma One) retains a larger share of the transaction fee, since fewer intermediaries take a cut, compared to one routing through a programme manager, an issuing bank, and a network.

The architecture beneath the card matters as much as the architecture on the blockchain. The next question is what sits above the payment rails, and how these protocols implement the paradigm of banking on a ledger.

The Onchain Bank Models

This section explores different onchain neobank models using four different protocols using very different approaches as our case study.

Each has made fundamentally different architectural choices, and those choices, depending on their success, will set the standard for crypto banks.

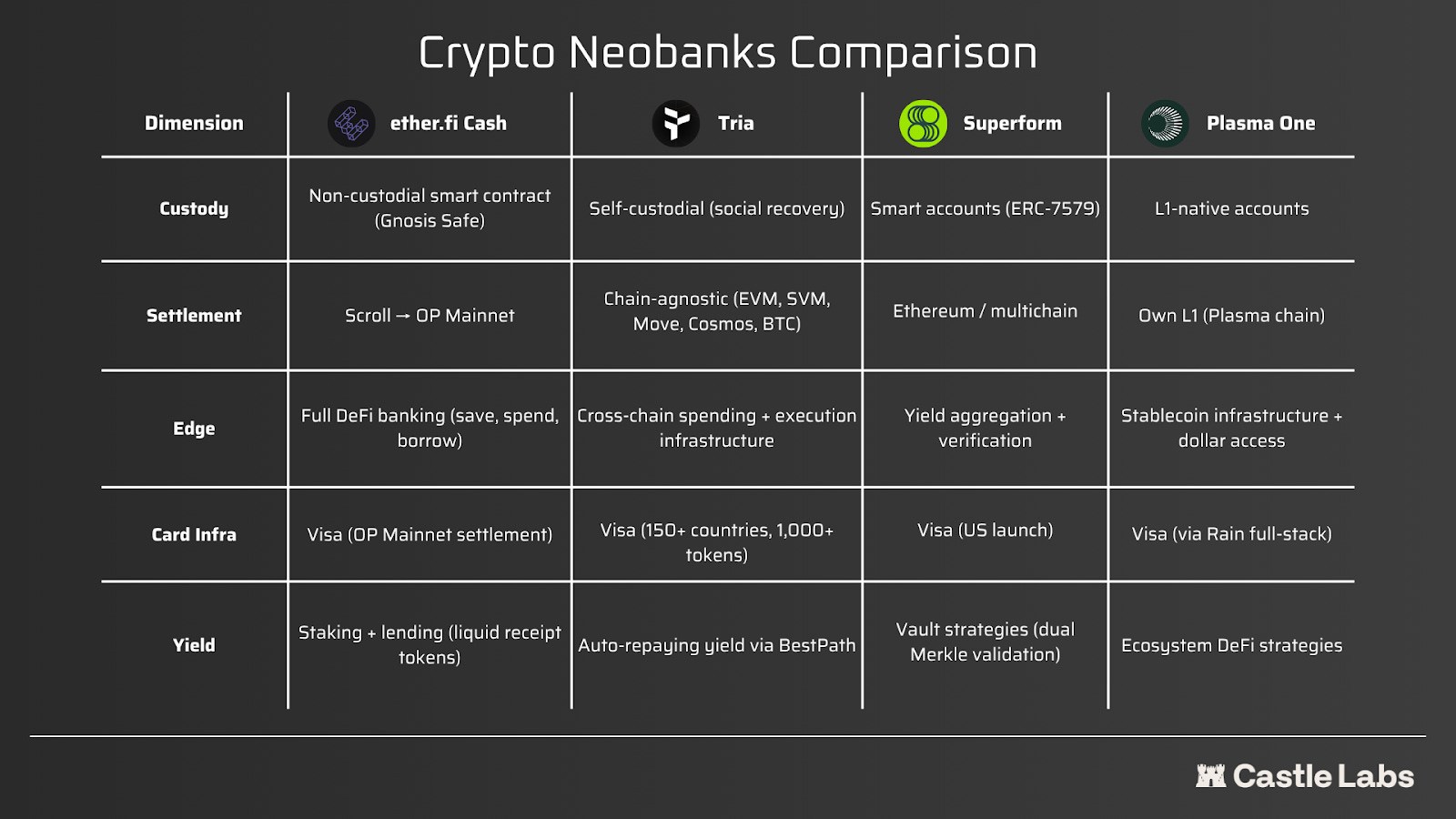

ether.fi Cash, The Onchain TradFi Bank

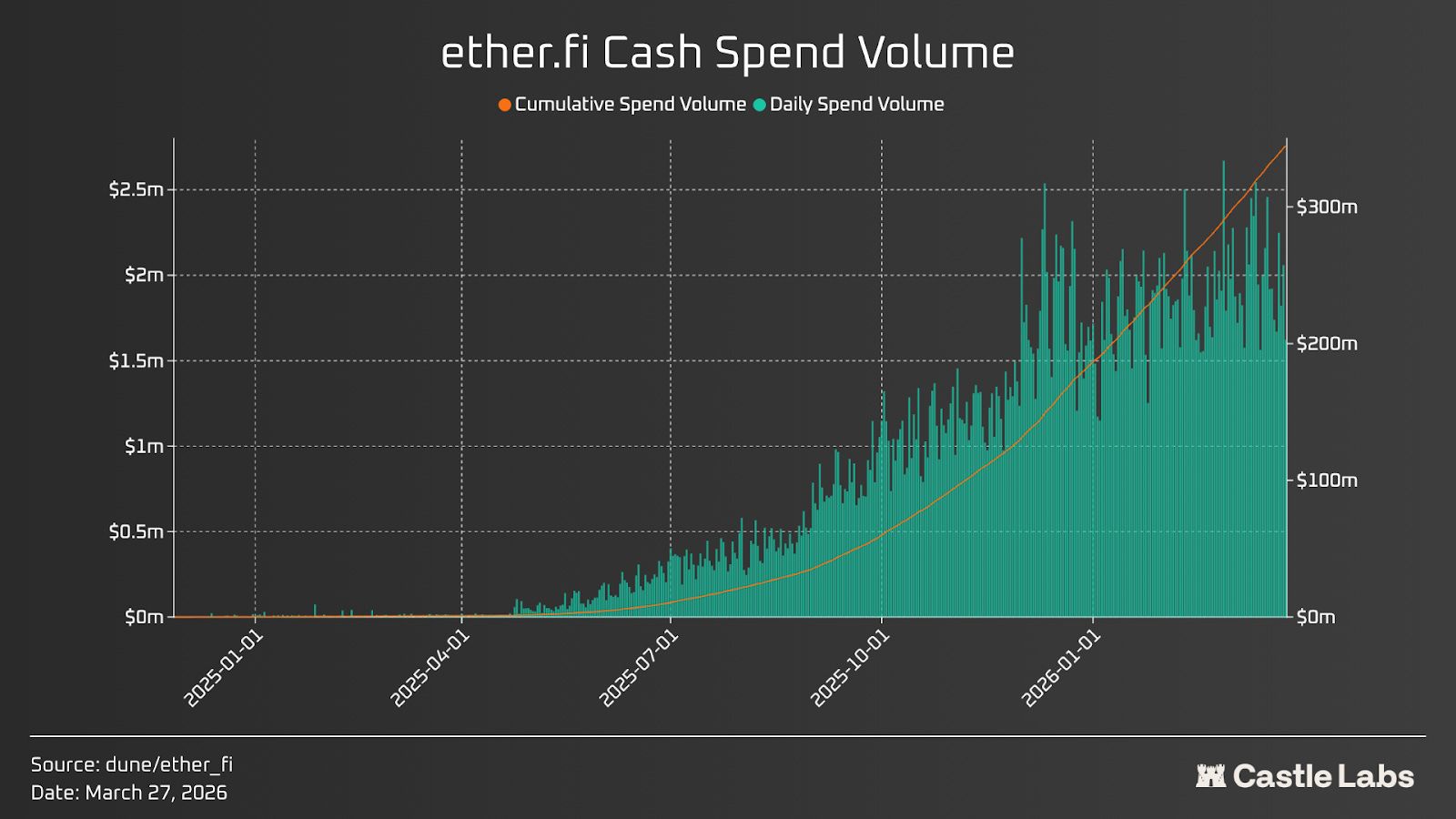

Ether.fi accounts for over a quarter of total spending volume across all crypto cards.

Cash, ether.fi’s non-custodial crypto card is now its largest revenue line, accounting for approximately 50% of protocol revenue.

What makes ether.fi Cash is architecturally distinct in its custody and wallet infrastructure. The architecture is a Gnosis Safe-based modular system called EtherFiSafe. Each user gets a dedicated multi-signature smart contract wallet with whitelisted modules that enable spending, borrowing, and yield generation from a single non-custodial vault.

This is meaningfully different from Web2/3 hybrids. In a hybrid model like Nexo, the platform holds user funds in pooled accounts. In ether.fi Cash: each user’s funds sit in their own smart contract, including ether.fi itself cannot access the user’s private keys. If the ether.fi platform disappeared tomorrow, user funds would remain accessible in the Gnosis Safe, recoverable via any Web3 interface.

The product offers two spending modes:

Direct Pay transfers assets from the user’s vault to fund a card transaction.

Borrow Mode allows users to deposit ETH as collateral into staking or liquid-vault products, then borrow against it via a dedicated Aave deployment. The user spends borrowed stablecoins while their ETH continues earning yield. This is a significant upgrade: no traditional neobank and no Web2/3 hybrid currently offers the ability to borrow against staked crypto collateral and spend the loan directly via a card.

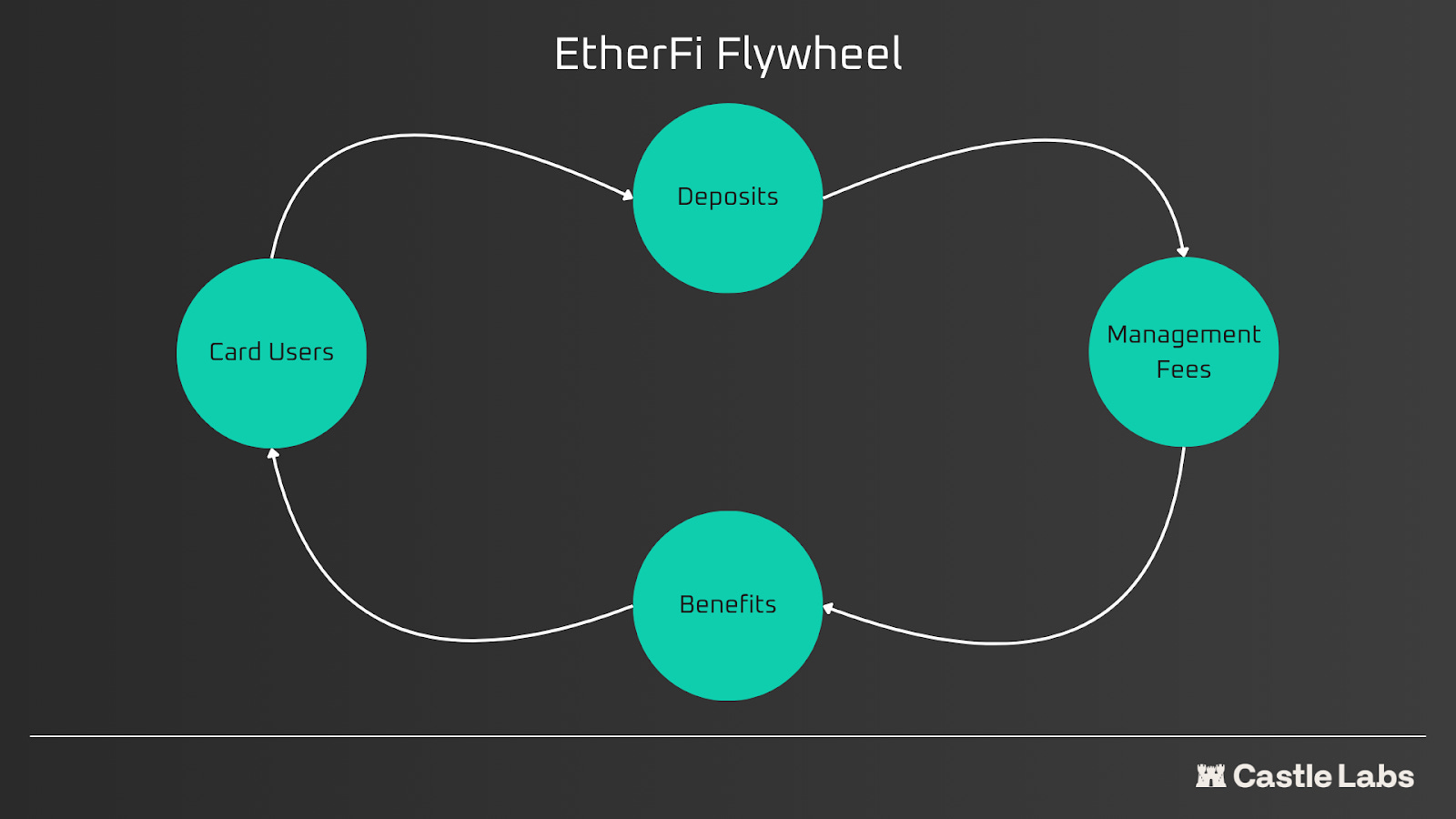

This creates a flywheel: cards drive deposits, deposits drive TVL, TVL drives management fee revenue.

In terms of size, ether.fi reached approximately 300,000 accounts with almost 70,000 active cards,

The migration to OP Mainnet began on February 19, 2026, moving all accounts from Scroll under a long-term Optimism Enterprise partnership. The Visa card launched on February 26 offers up to 3% cashback with Apple Pay and Google Pay integration.

Ether.fi Cash offers cashback ranging from 2% to 3% depending on membership tier, with promotional campaigns pushing total rewards to 5%, a portion paid instantly in SCR or wETH and the rest in ETHFI tokens. The critical difference is in the cost structure of ether.fi. Compared to centralised exchanges that pay rewards in fiat or liquid crypto, thus incurring real-dollar costs, ether.fi funds its rewards through token incentives at near-zero marginal cost of capital. The tradeoff is that rewards are paid in volatile tokens; if the value of ETH or SCR drops 20%, the cashback value drops with it.

Tria, The Self-Custodial Payment Infrastructure

Where ether.fi built a bank, Tria built an operating system.

Rather than competing as a standalone consumer product, it provides the settlement and wallet infrastructure that other crypto banks build on. This is analogous to what SWIFT did for correspondent banking in the 1970s, setting a standard that the industry adopted rather than each bank building proprietary rails.

The core innovation is BestPath AVS, a decentralised settlements marketplace currently being open-sourced, built as an Actively Validated Service on EigenLayer, where solvers, routers, and relayers compete to route transactions across chains. Other neobanks and wallets can plug into BestPath to access cross-chain settlement without building their own bridging infrastructure.

Tria is truly chain-agnostic: a user can hold assets on any supported chain and spend them via a Visa card without manual bridging, swapping, or gas management. The wallet is fully self-custodial with social recovery, no seed phrases, and no gas tokens required.

To date, Tria’s card product has more than $60 million in total volume, settling across Arbitrum, Base, Optimism, Polygon, and Solana, with monthly card spend running at roughly $12 million as of March 2026. The platform serves 500,000+ users.

Beyond payments, Tria’s perpetual product, running on Hyperliquid using builder codes, has crossed $475 million in volume in its first 30 days alone, generating $439K in fees and annualising at $5.3M in revenue from perps alone. Tria now accounts for 0.116% of all global Hyperliquid perpetual volume, a notable share for a product that was just launched in the middle of an explosive market.

BestPath and Tria’s CoreSDKs function as modular developer toolkits for wallet creation, authentication, and payment processing, enabling other neobanks to integrate Tria’s infrastructure without building from scratch.

Additional ecosystems integrating Tria include 0G, Aethir, Sentient, Base, Arbitrum, and Monad.

Superform, The User-Owned Piggy Bank

Superform approaches the neobank thesis from a different angle entirely: yield aggregation with full onchain verifiability.

The architecture uses ERC-7579 smart accounts and SuperVaults that employ dual Merkle validation. What this means in practice is that every yield strategy is cryptographically verifiable onchain. Unlike a traditional savings account, where the bank invests deposits opaquely, or a hybrid platform like Nexo, where yield comes from centralised lending desks, Superform’s vault framework is transparent: users can verify exactly where their capital is deployed across Morpho, Euler, Aave, and Pendle.

SuperVault v2 strategies include SuperWBTC, SuperWETH, and SuperUSDC, offering optimised yield across chains. The validator network adds an additional safety layer: before any yield strategy is deployed, it must be approved by a network of independent validators who stake their own capital as a guarantee of due diligence. If a validator approves a strategy that turns out to be malicious or flawed, they lose their staked capital through economic slashing.

Where ether.fi is a full DeFi bank, and Tria is a payment infrastructure layer, Superform is a savings account, the user-owned piggy bank that earns institutional-grade yield without requiring active management.

Plasma One, The Stablecoin Infrastructure Play

Plasma takes a vertically integrated approach.

Built on its own Layer 1 blockchain with native Tether integration, Plasma controls the full stack:

The consensus layer

The stablecoin infrastructure

The DeFi ecosystem that generates yield

Spending is routed through Rain’s principal Visa membership to the card network.

This vertical integration is the key architectural distinction:

ether.fi builds on Ethereum L2s and uses third-party DeFi protocols for yield.

Tria is chain-agnostic and protocol-agnostic, routing across many chains.

Superform aggregates yield from existing protocols.

Plasma owns the entire stack, from consensus to card settlement, which gives it more control but also introduces centralisation tradeoffs: the ability to theoretically halt or roll back transactions.

Plasma’s focus is on emerging markets and dollar access, targeting the billions of people who need stable dollar exposure more than they need DeFi composability.

Consumer Protection, or the Lack Thereof

The major downside, aside from regulations, which will be discussed further down, is the uncertainty regarding customer protection with regard to onchain banks.

Traditional banks offer a safety net built over decades of regulation and failure.

Card transactions carry chargeback rights: if a merchant defrauds a cardholder, Visa’s Zero Liability policy reverses the charge. If a bank goes bankrupt, depositors are legally prioritised over other creditors. These protections are enforced by law, and every institution, whether JPM or a small regional bank, must abide by them.

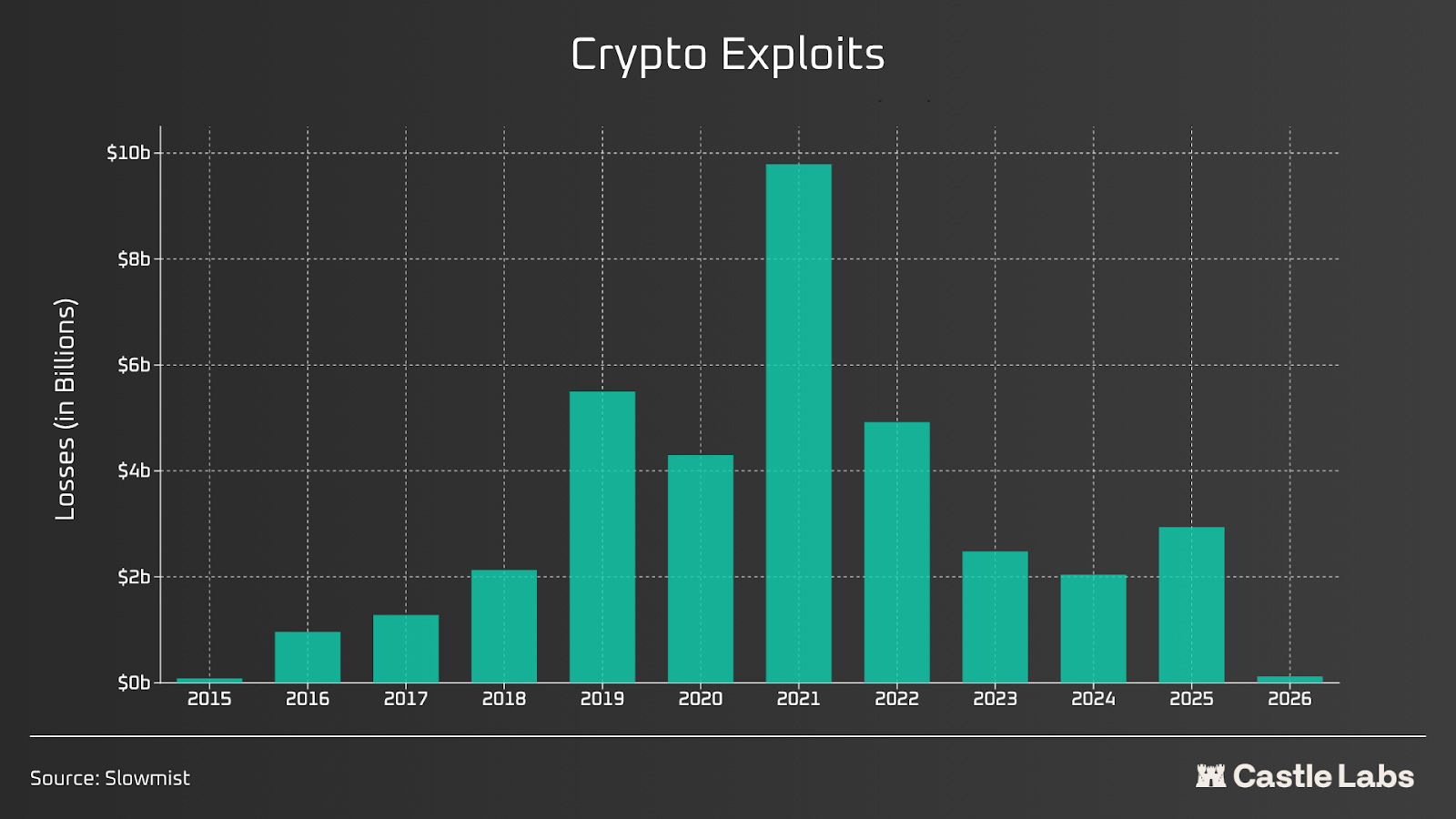

Crypto neobanks offer none of this. There is no FDIC insurance, no deposit guarantee. Blockchain transactions are still irreversible. If funds are sent to the wrong address or stolen in a hack, there is no protocol-level chargeback mechanism. DeFi exploits have drained billions, and there is no meaningful way to recover those funds.

What onchain banks offer instead is a fundamentally different risk model, relying on practical guarantees that the law does not enshrine.

Self-custody is the first line of defence. With ether.fi Cash, a dedicated smart contract vault is deployed for each user, secured by a Trusted Execution Environment (TEE) provided by Turnkey. Even ether.fi itself cannot access the user’s private keys. If the ether.fi platform disappeared tomorrow, user funds would remain accessible in the Gnosis Safe smart contract. However, with power comes responsibility, as this means users bear full responsibility for their funds. There is no helpline for a lost key, no AI agent, no soft-spoken cashier at the counter to receive one’s complaints.

Smart contract audits and bug bounties are the second line. Ether.fi’s contracts are audited by leading security firms, and the protocol runs a bug bounty programme through Immunefi, paying up to $200,000 for critical vulnerabilities. The platform has processed over 80,000 transactions without a security incident as of February 2026, but as ether.fi’s own documentation states, “there always exist risks in interacting with smart contracts“ and the protocol “can make no guarantees that methods are or will remain 100% secure“.

Superform addresses this through its validator network, with economic slashing: validators that approve malicious strategies lose their staked capital.

Plasma’s approach is different again: by controlling its own L1, it builds consumer protection into multiple layers of the architecture.

At the base, Plasma periodically anchors cryptographic state commitments to the Bitcoin blockchain, inheriting Bitcoin’s security model

Its PlasmaBFT consensus, a HotStuff-inspired Byzantine Fault Tolerance (BFT) mechanism, ensures the network continues operating correctly even if up to one-third of validators behave maliciously.

Above the consensus layer, Plasma benefits from native Tether integration with direct issuer oversight, curated DeFi partner onboarding rather than permissionless deployment, and a Bitcoin bridge secured by the same decentralised validator set, with plans to adopt BitVM2 for further trust minimisation.

Only as a last resort could Plasma’s validator theoretically halt or roll back transactions in extremis, though this creates its own centralisation tradeoff.

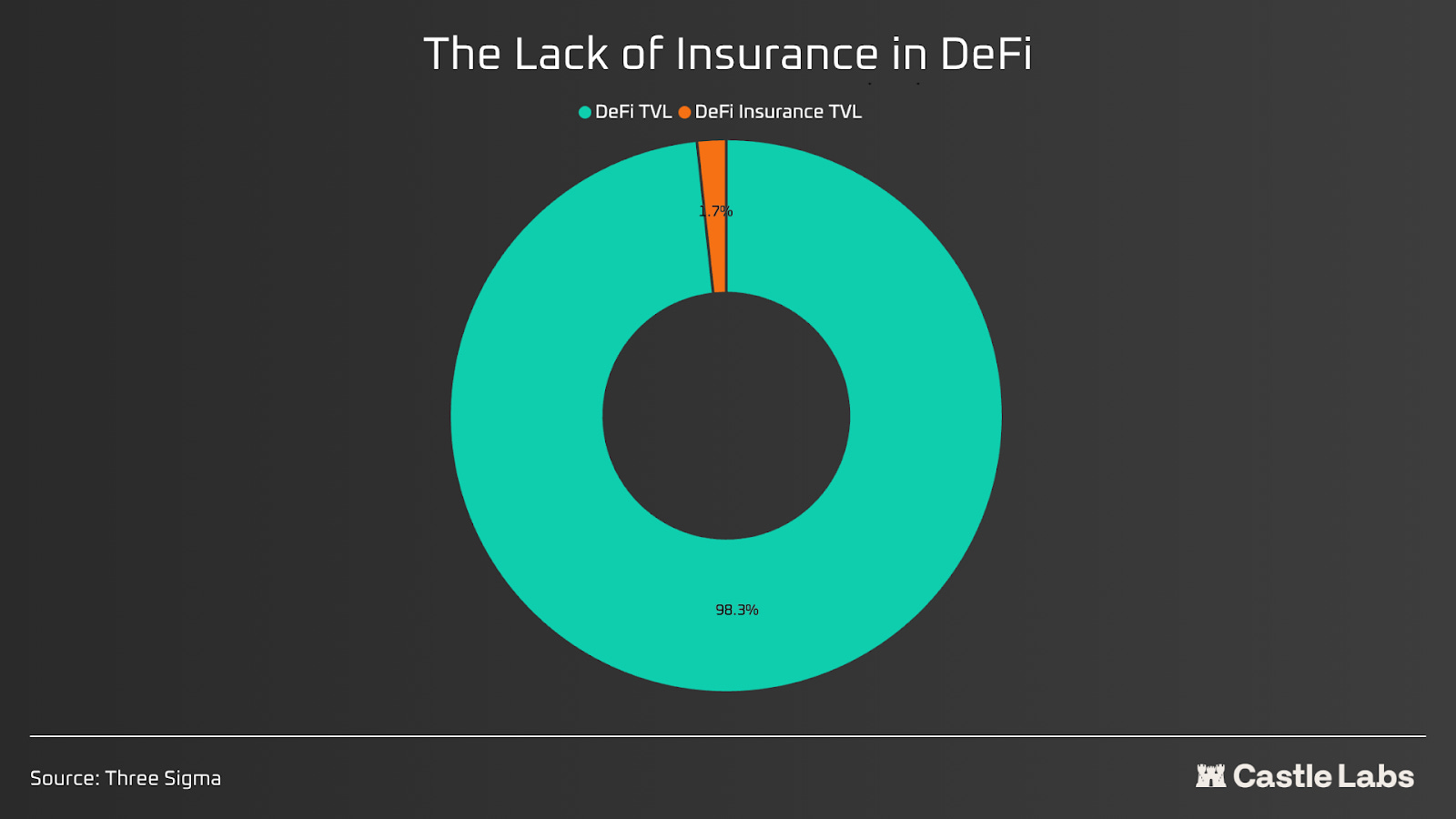

Optional DeFi insurance exists but is not standard. ether.fi users can purchase smart contract cover from Nexus Mutual, a decentralised insurance alternative that bundles protection across EigenLayer, ether.fi, Morpho, Pendle, and Uniswap into a single Cover NFT. This is voluntary and costs the user money; it is not built into the product the way FDIC insurance is built into a bank account. Most users will not purchase it because spending more money to protect their funds is discouraging and not easily accepted: less than 2% of total DeFi TVL is covered by any form of insurance, and the entire decentralised insurance sector holds a fraction of the capital locked in lending or trading protocols. Spending additional money to protect one’s funds is a hard sell when users are accustomed to deposit insurance being built into banking products at no visible cost.

Borrow Mode introduces liquidation risk that has no equivalent in traditional banking. If a user borrows against ETH collateral and the price drops below the liquidation threshold, the smart contract automatically sells the collateral to cover the debt. There is no margin call, no grace period, no human intervention. The user must actively monitor their health factor and adjust collateral ratios.

Card-level protections, however, still apply. Because these cards run on Visa rails, users do get Visa Signature benefits: $2,000 price protection, $10,000 purchase protection, $10,000 extended warranty, and Visa Zero Liability against fraudulent charges. These protections come from Visa, not from the protocol. They cover the card side of the transaction, and nothing else.

Therefore, onchain banks eliminate counterparty risk but introduce smart contract risk. On the one hand, the user is no longer exposed to the platform’s balance sheet. As such, their assets cannot be rehypothecated, frozen by a compliance officer, or lost in a bank run. On the other hand, they are exposed to code vulnerabilities, oracle manipulation, bridge exploits, and the consequences of their own errors, which can be catastrophic.

For sophisticated users who understand DeFi, this is arguably a better risk profile.

For the average consumer who expects a bank to step in when something goes wrong, onchain banking is not yet a comfortable substitute, and the gap between DeFi’s transparency and traditional banking’s safety nets remains wide.

The Regulatory Heavy Burden

In the USA, Trump signed the GENIUS Act into law on July 18, 2025, as the first federal legislation on digital assets ever enacted in the United States.

The framework creates three categories of permitted stablecoin issuers:

Subsidiaries of insured depository institutions.

Federal-qualified nonbank issuers (regulated by the OCC).

State-qualified issuers.

Stablecoin payments must be backed 1:1 with US dollars, short-term Treasuries, overnight reverse repos, or specified money market funds. Monthly attestations and redemption rights are mandatory. Critically, permitted payment stablecoins are explicitly not securities under federal law, removing them from SEC jurisdiction.

The FDIC has already proposed application procedures for supervised institutions seeking to issue stablecoins under the Act. For crypto neobanks, the consequences are optimistic: GENIUS Act-compliant stablecoins become the regulation of reference, and the infrastructure implements the Administration’s word, safe from the regulator’s anger.

In the EU, the Markets in Crypto-Assets Regulation (MiCA) is now fully operational, and the Anti-Money Laundering Authority (AMLA) becomes fully operational this year. Europe has over 50 active neobanks, but compliance costs are rising, and it will become increasingly expensive to satisfy regulatory demands that remain, in many cases, poorly adapted for onchain business models. These models face specific challenges because existing AML frameworks were designed for custodial intermediaries, not self-custodial smart contract wallets, creating friction around transaction monitoring, travel rule compliance, and customer due diligence that does not integrate obviously onto decentralised businesses.

Which leads us to the question of legal enforcement.

The enforcement track record should give crypto neobanks pause.

Even established neobanks have faced significant penalties, both in Europe and the USA:

Monzo was fined $27 million by the FCA for Anti-Money Laundering failures in July 2025.

Revolut was fined $3.8 million in Lithuania.

Cash App paid an $80 million settlement across 48 US states, showing that even the New World can and will sanction those who don’t toe the line.

False-positive rates in transaction monitoring exceed 95% at some neobanks, meaning compliance systems flag 19 legitimate transactions for every genuine suspicious transaction. AML transaction monitoring systems use broad rules: Neobank customers trigger those same red flags, and the systems can’t contextualise whether a flagged transaction is a freelancer paying rent or a criminal structuring deposits due to the nature of crypto transactions (offramping, cross-border payments, small transfers).

Furthermore, traditional banks still refuse to bank crypto businesses: Crypto activities trigger virtually every internal alarm associated with money laundering risk within traditional banking systems, regardless of the actual risk profile. In Europe, correspondent banks exert heavy pressure on smaller institutions to cut ties with crypto clients, forcing them to choose between serving crypto customers and keeping their place in the financial system.

RedotPay illustrates the traditional fintech response to this problem. It holds VASP licences in Lithuania and Argentina, a money lender licence and Trust or Company Service Provider licence in Hong Kong, and maintains full PCI DSS compliance. This is the compliance first strategy: accumulate licences faster than competitors can apply for them.

RedotPay’s multi-jurisdictional licensing is a core reason it operates in over 100 countries while protocol-native actors remain geographically constrained. The planned US IPO would further solidify this advantage by embedding the company within US public market disclosure and governance requirements.

Onchain neobanks are, given their design, more transparent than traditional banks by nature:

Every transaction is verifiable onchain.

Every reserve is auditable in real time.

Every smart contract interaction is recorded immutably.

The onchain transparency advantage should, in theory, make these protocols safer, not more suspicious.

Yet, compliance is becoming an inevitable structural factor, just as it is with traditional banks.

The protocols that build GENIUS Act and MiCA compliance into their architecture will be the ones that become blue-chip retail products.

A Long Way Ahead

The first generation of neobanks changed how banking looks, while the second generation is changing how banking works, by replacing custodial, intermediary-dependent infrastructure with self-custodial, onchain alternatives.

All four models are converging toward the same banking products: save, spend, earn, borrow, but they are arriving from fundamentally different directions.

Ether.fi comes from DeFi staking and has made Cash a major source of revenue.

Tria comes from cross-chain execution infrastructure and is positioning BestPath as the settlement layer that other neobanks plug into.

Superform comes from yield aggregation and is building an automated savings account.

Plasma comes from stablecoin infrastructure and is targeting the billions of people who need dollar access more than they need DeFi.

The massive elephant in the room is, of course, the utter lack of consumer protection.

If crypto cards are a tool for sophisticated users who understand DeFi mechanics, collateral management, and smart contract risk, the absence of deposit insurance, chargeback guarantees, and institutional safety nets means these products are not yet substitutes for traditional banking.

Crypto neobanks remain an experiment that neither neobanks nor banks should see as a threat, given the massive guarantees they offer their customers. Because of a lack of perspectives on long-term regulations in Europe, an uncertain future for current US legislation, and a total lack of consumer protection, it would be wise to rely either on one’s affable banker or, at least, on a useful AI agent ready to answer at any time.

Many neobanks burned cash and never reached profitability. Crypto neobanks face the same unit economics question.

written by @TradFiHater ✍️

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram person, you can read all of our research without the noise on our TG channel: