Mantle's Momentum: Short-Term Catalysts and Onchain TVL

Mantle continues its impressive growth. In our previous report, we highlighted the main growth drivers and strategic approach differentiating Mantle. This time, we dive deeper into how they are taking form and shaping the ecosystem.

A Different Approach

L2 have been struggling in the past market cycle.

Initially established to make Ethereum block space cheaper, now there is an abundance of this blockspace, and their very reason to exist is being challenged.

Mantle has recognised this need early on and has taken a very different approach, fully embracing Real World Assets (RWAs) and focusing on building a financial network that bridges the gap between Traditional (TradFi) and Decentralised Finance (DeFi).

“You just need to have the best distributors of Web3 to get the best assets in Web2 with the right infrastructure, technology and a high caliber team who understand the TradFi interest, and Mantle has it” - Joshua Cheong (Head of Product)

This shift has been proven to resonate with both the community and the broader landscape.

With upcoming catalysts such as the launch of UR, Mantle’s neobank, and deeper utility for MNT, we analyse how this growth is trickling down across the ecosystem, linking offchain catalysts with onchain data.

Short Term Catalysts

Let’s start by contextualising all recent developments by touching on the main recent and future catalysts.

Mantle continues showcasing its interest in doubling down on the RWA niche, through its efforts to expand vertically, nurturing several key primitives:

UR as the gateway to offer banking services

Bybit as the distribution network

Tokenisation as a service (TaaS) as the “Pumpdotfun version of RWAs”

All of these have one common objective: to simplify the path to bring assets onchain, with MNT as a key component of this design.

Mantle has just announced the creation of its TaaS platform, a unified framework for launching RWAs onchain, drastically reducing the time-to-market for these assets.

What is included in the platform?

Licensing

KYC

Legal structuring

Development part: contract deployment, audit and security monitoring

Compliant UX

While often in business, the first-mover advantage tends to fade over time with scale, RWAs might be one of the niches where securing key partnerships and commitments early on can make a significant difference in gaining traction. At Token2049, Eric Trump himself announced that World Liberty Financial will deploy USD1, their US Dollar stablecoin with over $2.6b in market capitalisation, on Mantle. This is a strong signal of confidence from institutional capital.

While most recent efforts have focused on establishing the TradFi aspects of the ecosystem, all assets on Mantle can be leveraged within Mantle’s DeFi ecosystem through its several CeFi and DeFi integrations.

The launch of a TaaS connects demand to a streamlined way to populate the ecosystem with RWA assets, making it easy and appealing for institutional investors to deploy.

Now, the tricky part of most ecosystems that operate between TradFi and DeFi is that they leverage third parties to connect with the “outside world”, leaking value and leading to cumulative third-party risks.

Instead, Mantle is choosing to have full control over its financial stack, with the launch of UR, its neobank.

With one single account, users will be able to operate across both TradFi and DeFi, without leaving the Mantle ecosystem. A practical example is the fact that users will be able to earn 5% yield on sUSDe deposited on UR.

One of the most significant narratives of 2025 has been the rise of stablecoins. Mantle is observing this closely, as Joshua Cheong (product lead at Mantle) shared during his panel at Token: For Mantle, the biggest opportunity and unlock will be “pairing RWAs with stablecoins to unlock real-world financial use cases onchain”.

Another key aspect where Mantle has focused is distribution.

The partnership with Bybit has been an incredible opportunity for Mantle. With MNT fully integrated into Bybit, users can increase their MNT holdings to level up their pass, earning fee discounts and other benefits, including access to launchpad and megadrop opportunities.

But let’s not be fools; if this were just about distribution, it would most likely be a short-term burst. The utility element involved in MNT is what this partnership is really about.

Across different sources, Bybit has a user base conservatively estimated at 50 million users.

Imagine the power of placing the MNT token at the centre of this ecosystem, fully connected to all the existing onchain benefits of Mantle.

The benefits extend beyond retail users. To mention some, institutions can benefit from higher leverage (5-8x) as well as longer fixed loan terms.

Another fascinating element, proof of how far they are willing to go to align interests, is their “discount buy”. Users who choose to set a minimum holding time from 30 to 180 days on their MNT buy receive a discount (up to 6.89% for the maximum hold).

For the nostalgic, this mechanism (loosely) resembles what Olympus DAO used to do with bonds, Bybit edition.

Isolated, these might seem like small perks here and there, however, combined, these are targeted integrations to add additional utility to MNT, increase demand, and reduce short-term selling pressure.

At least for now, the market agrees with the way Mantle is moving.

The MNT token is at an ATH, up over 4x from its lows in July.

Purely in terms of price action, it is outperforming any other CEX and Layer 2 (L2s) token this cycle.

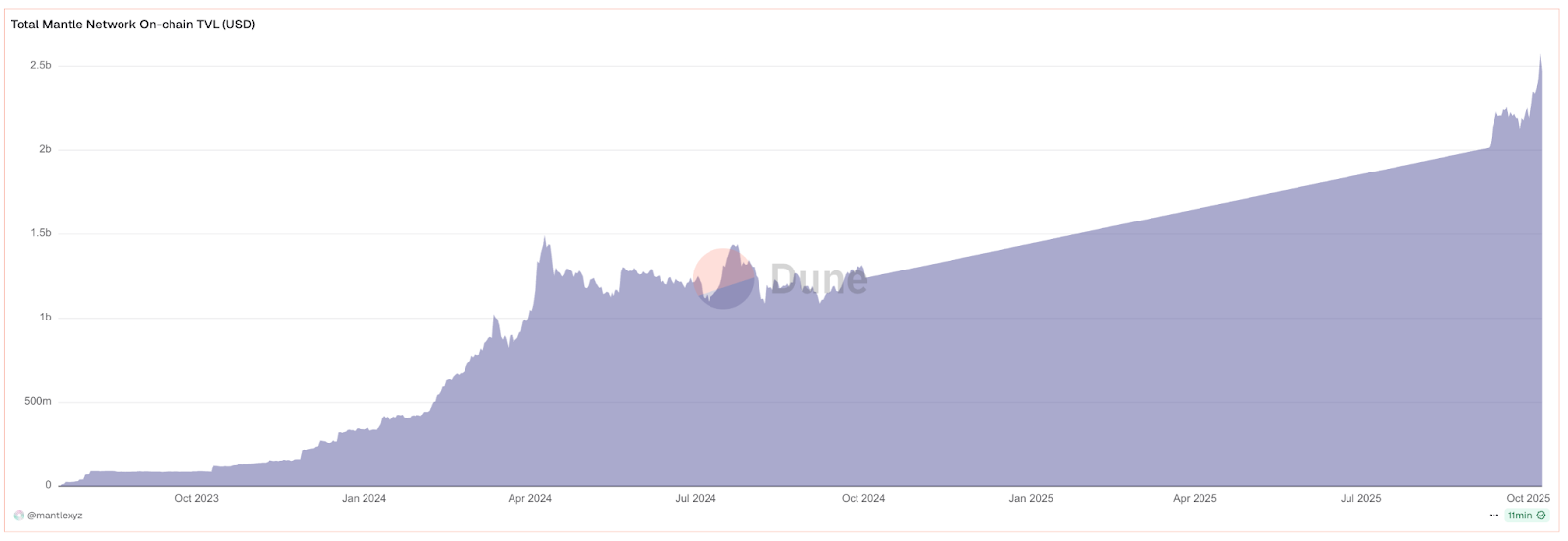

Both the increasing development of RWA assets and offerings, coupled with MNT growth, have led to a steady increase in onchain TVL, now at over $2.5b.

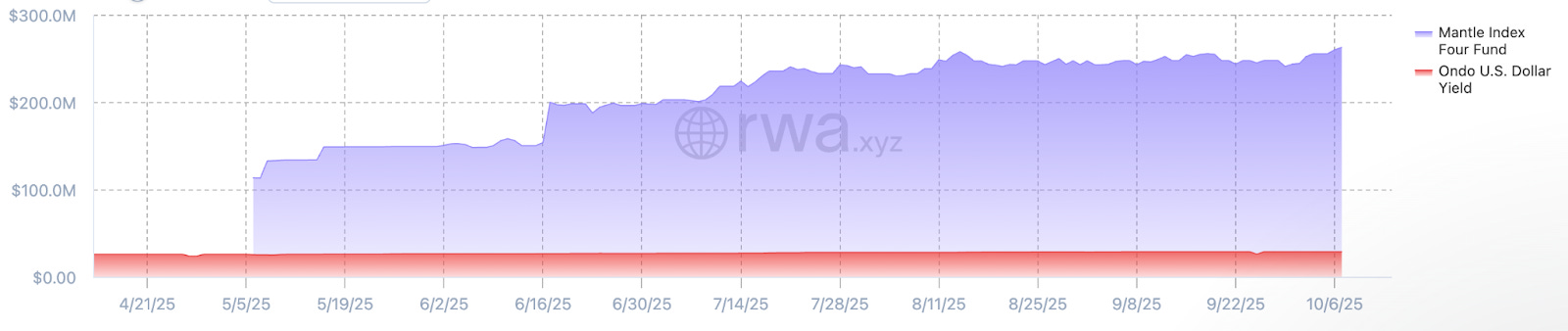

Mantle’s RWA ecosystem began scaling around May, with an initial $100m commitment, which has now grown to over $255m.

The TVL is split across two main funds:

-Mantle Index Four Fund ($233m in TVL): For users looking for risk-adjusted simplified exposure, this fund has market-weighted exposure to bluechip assets such as BTC, ETH, SOL, L1s, and L2s as well as additional yield through yield-bearing assets such as mETH, bbSOL, and sUSDe.

- Ondo’s US Dollar Yield (USDY): Backed by short-term US treasuries and bank demand deposits. Targeted to investors who are looking to get exposure to the US Treasury yield.

Mantle has prioritised building its vertical infrastructure and its RWA side. Nonetheless, it still has over $250m of TVL in its DeFi ecosystem.

Here are Mantle’s top protocols by TVL:

Agni Finance ($91.59m): Mantle’s biggest onchain TVL hoarder, an AMM-based DEX and launchpad. 56% of the TVL comes from CMETH, followed by USDe (16.9%), FBTC (14.56%), WMNT (4.82%) and other assets.

Treehouse Protocol ($91.09m): Treehouse offers several fixed-income products through its Treehouse Assets (tAssets) and Decentralised Offered Rates (DOR). Its TVL on Mantle is derived all from CMETH.

Merchant Moe ($72.2m): A DEX on Mantle and leading native protocol by active users, where LPs can deposit liquidity. Similar to the others, most of the TVL is in USDe, CMETH, FBTC, USDT, and sUSDe.

It would not be unthinkable to envision the ecosystem developing future ways to drive TVL to onchain protocols.

It’s been a long time since we last discussed flywheels, but Mantle’s strategy is worth taking into consideration, even if purely from a research standpoint.

As they have almost finished laying down their infrastructure, we’ll soon see how all these elements will work together.