Most Crypto Assets Need to go to ZERO

Crypto is going through its one of the discovery phases where speculative tokens will stop receiving new inflows.

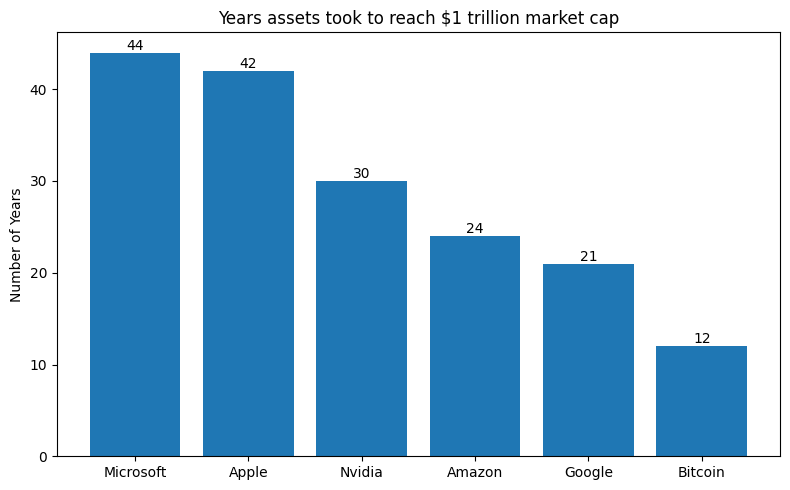

It’s the year 2021, and you have just started investing in crypto and have become a fan of the industry, how it works, and how anyone can make it big if they do it right. You have witnessed many stories, many millionaires, and just straight-out investing in BTC seems to be a good strategy as well. You are shown how BTC is one of the fastest-growing assets, and that it reached $1 trillion in market capitalisation well before any company.

Fast forward to today, you are sitting at your family dinner, and everyone is talking about their portfolios, how the S&P 500 has performed well over time, and how they are happy with their investments. You pull up your phone and see your portfolio down 60% from its all-time high, take a long sigh, and take another bite.

Your cousin brother asks you: “Hey, you’ve been investing in crypto? How’s your portfolio doing?” with a chuckle. He also adds, “I am glad I stayed away from it and never dumped any of my cash there.”

You have nothing to say; you have nothing to add to the discussion. You can say that the NYSE is coming to the blockchain to introduce 24x7 trading, BlackRock is already tokenising short-term treasuries, Robinhood just launched its L2 testnet, and many more institutions are adopting crypto. But you stop, because you know you’re down and none of those factors seems to be helping.

You are confused because BTC has retraced to levels similar to when you first invested. Also, it’s not just BTC you have invested in, it’s a small part of your portfolio, but multiple other cryptos you discovered on your way, that you thought had a great upside, maybe one of the 17000+ tokens listed on Coingecko, maybe, millions of others launched in the last year or two on platforms like Pumpfun.

Over the years, so many coins have been created that 99% of them need to go to zero for the industry’s good.

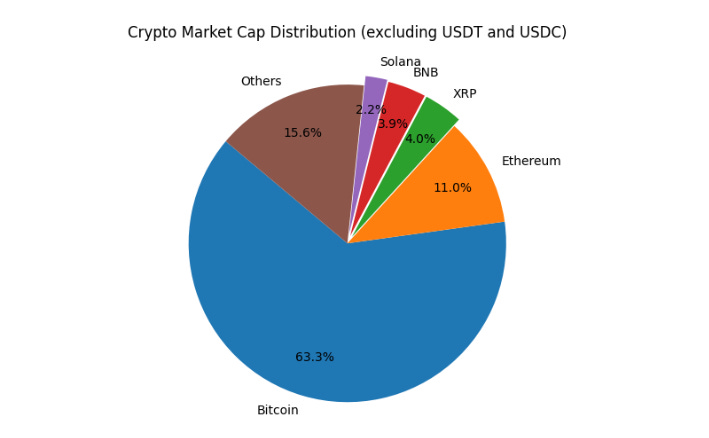

This is also evident in the fact that the top five tokens account for 84.4% of the total crypto market capitalisation, leaving you to wonder what to do with the rest and whether they have any value. The rest of the market (15.6% or $330 billion) is where the thousands of other tokens live.

To put this into perspective, this is a much larger concentration compared to Traditional Finance, where MAG7 companies in the U.S. equity market represent 31%, and the top 500 companies (S&P 500) represent 84.7%. A hundred times more companies, yet the same representation as crypto’s top 5 assets.

If crypto wants to achieve a similar representation, some of the following scenarios need to be true:

Top tokens lose value, while tokens below capture it.

There is a huge external liquidity push or adoption.

Tokens below lose their value, and the majors capture it.

For a healthy system, the first scenario makes more sense for distributing value, but it is unlikely to occur because most assets are correlated with BTC, and would also mean that major assets are losing trust, which isn’t ideal.

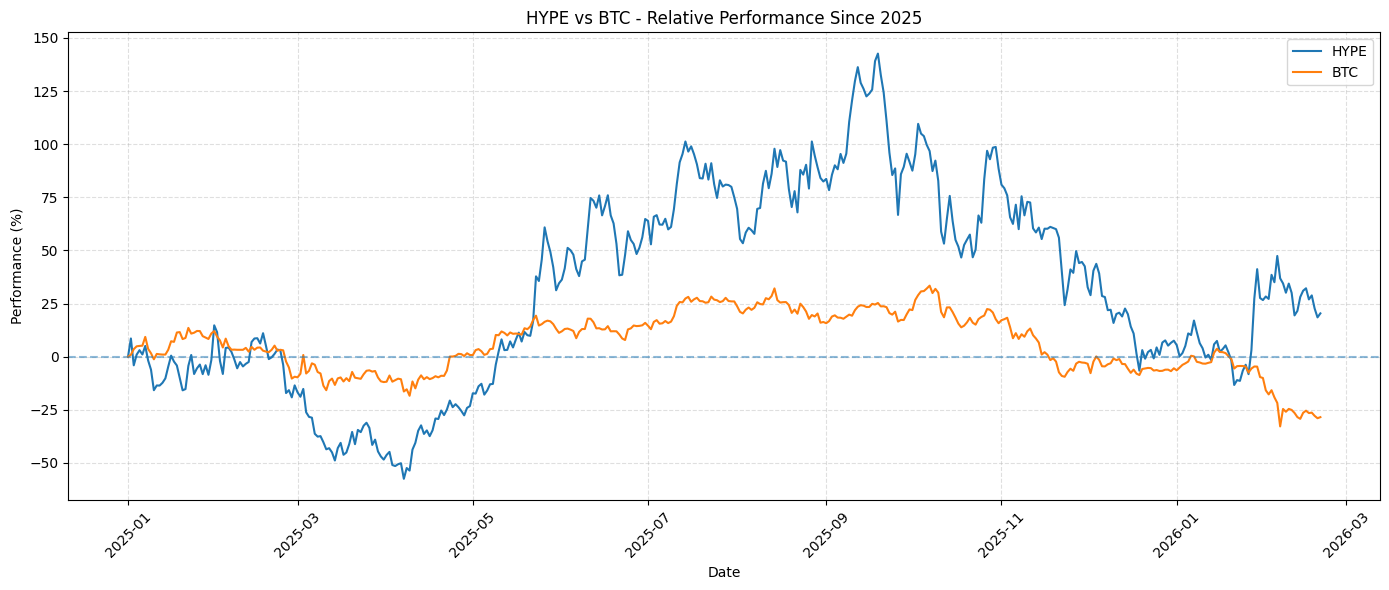

Certain tokens, such as HYPE, achieved significant market representation over time; they fit into the second scenario due to strong adoption and product-market fit. Hyperliquid is obviously one of the few winners in the last year who actually have great token and product alignment, as they redirect the majority of platform-generated fees into token buybacks.

Continuing on the second scenario and attracting value from external entities (or institutions), crypto did fairly well with DATs, at least in terms of accumulation, but they are way down as well. For BTCs, DATs have accumulated 997,257 BTC (5% of the circulating supply), and for Ethereum, it is 6.16 million ETH (5.1% of the circulating supply). Additionally, it’s also fair to argue that they represent a significant share of the circulating supply of majors, so any further involvement would effectively concentrate too much control in a few entities.

The third and last scenario is something that needs to occur rapidly, and here’s why.

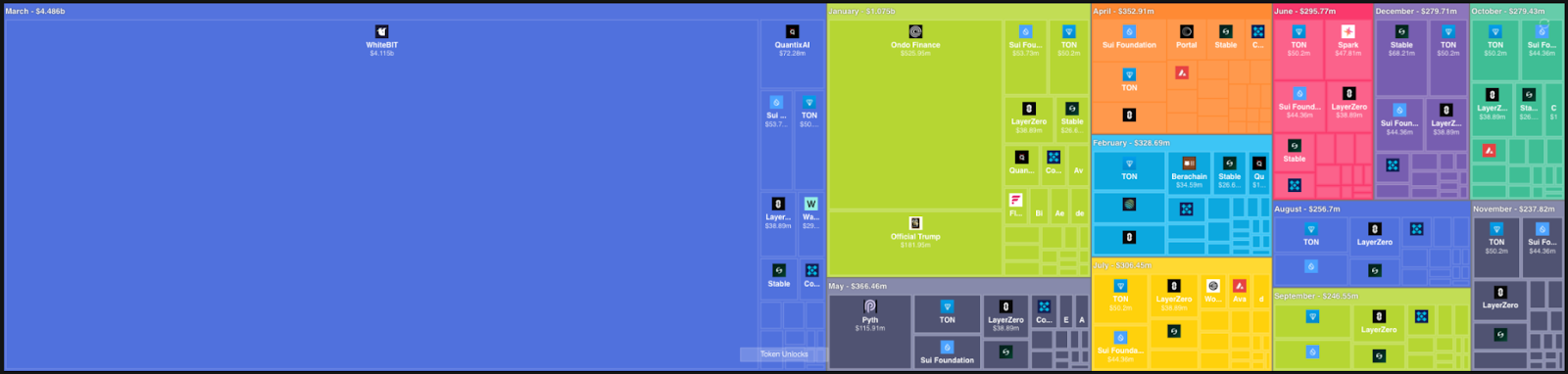

Token vests every month, and in the upcoming years, there will be a lot of supply unlocks. This year alone, token unlocks will add $8.51 billion in value, hitting the market, and over the next five years, $17.12 billion. But it is not clear if there will be enough demand to cater for these supply unlocks and the attributed selling pressure.

For most tokens, this will keep them progressing toward zero added with factors like skewed tokenomics.

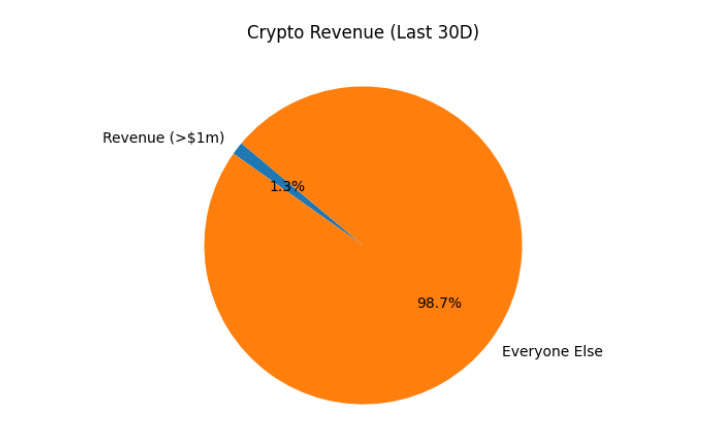

To increase demand, these projects need to succeed as a business. Multiple crypto businesses have been absolute failures. For a trillion-dollar industry, with more than 5600 protocols listed on DeFillama, only 76 generated over $1m in revenue in the last 30 days, that’s 1.3%.

Interestingly, lowering this threshold to >$100k in revenue over the last 30 days would still yield 237 protocols.

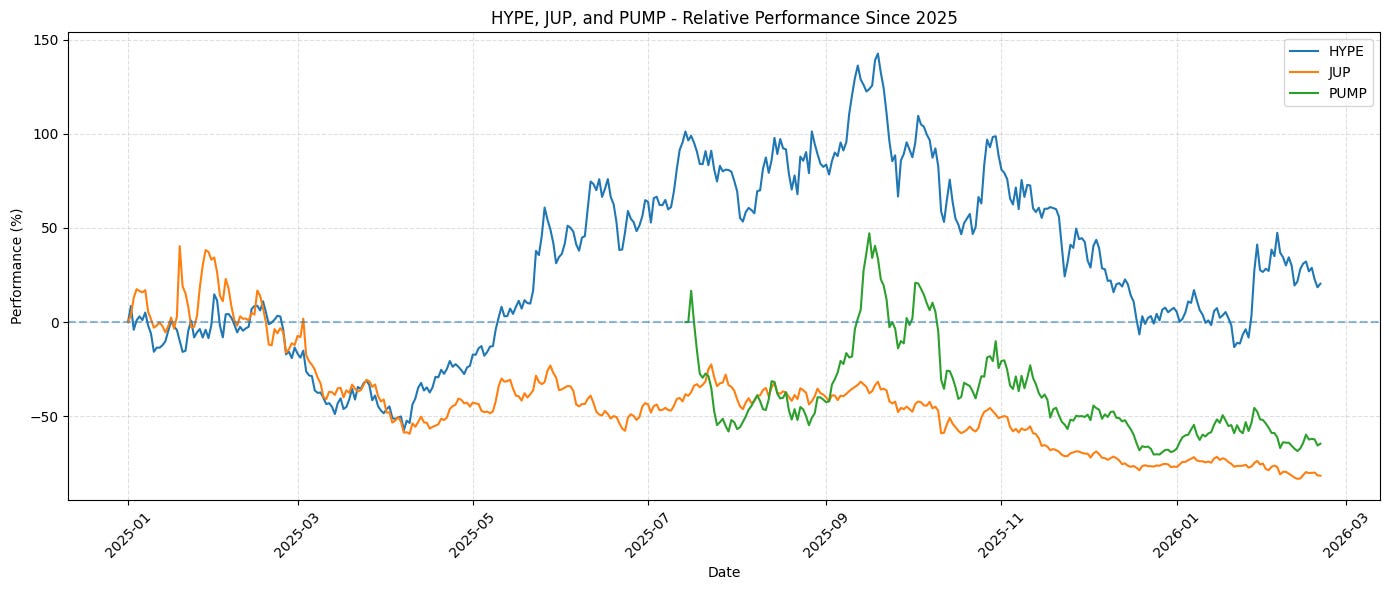

Additionally, when you see the revenue concentration. The top 10 protocols in 2025 accounted for 80% of revenue, and the top 3 accounted for 64%. Tether alone accounted for 44% of total crypto revenue. It’s surprising that, out of these 10 protocols, only 3 have launched a token so far (Hyperliquid, Pumpfun, Jupiter), and upon reviewing their relative performance, only HYPE performed better.

This also points out that launching a token may not always be the best choice.

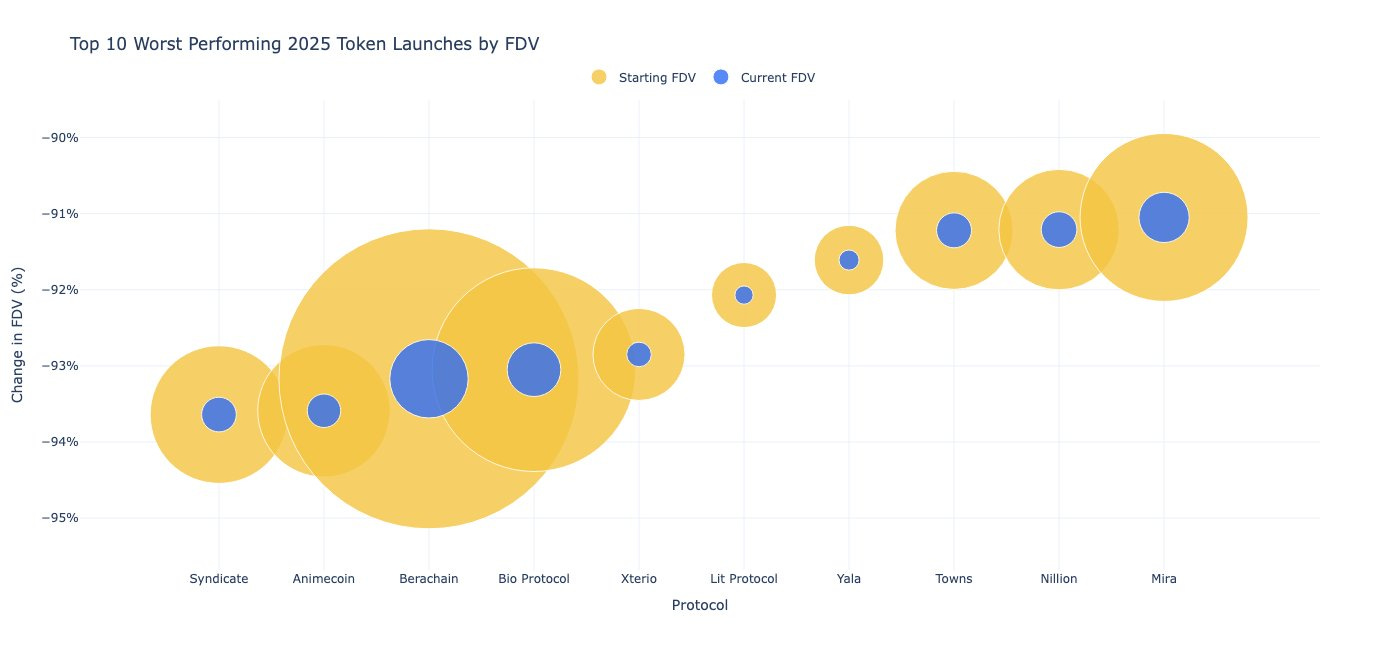

In 2025, there were about 118 major token launches, of which 84.7% were below their TGE valuation. These numbers don’t look very good, and they often disappoint, leading us to question whether it is even worth investing in new tokens. These tokens were launched at ballooned valuations and had very concerning price action throughout the year, and are down even now, as broader market conditions aren’t doing very well either.

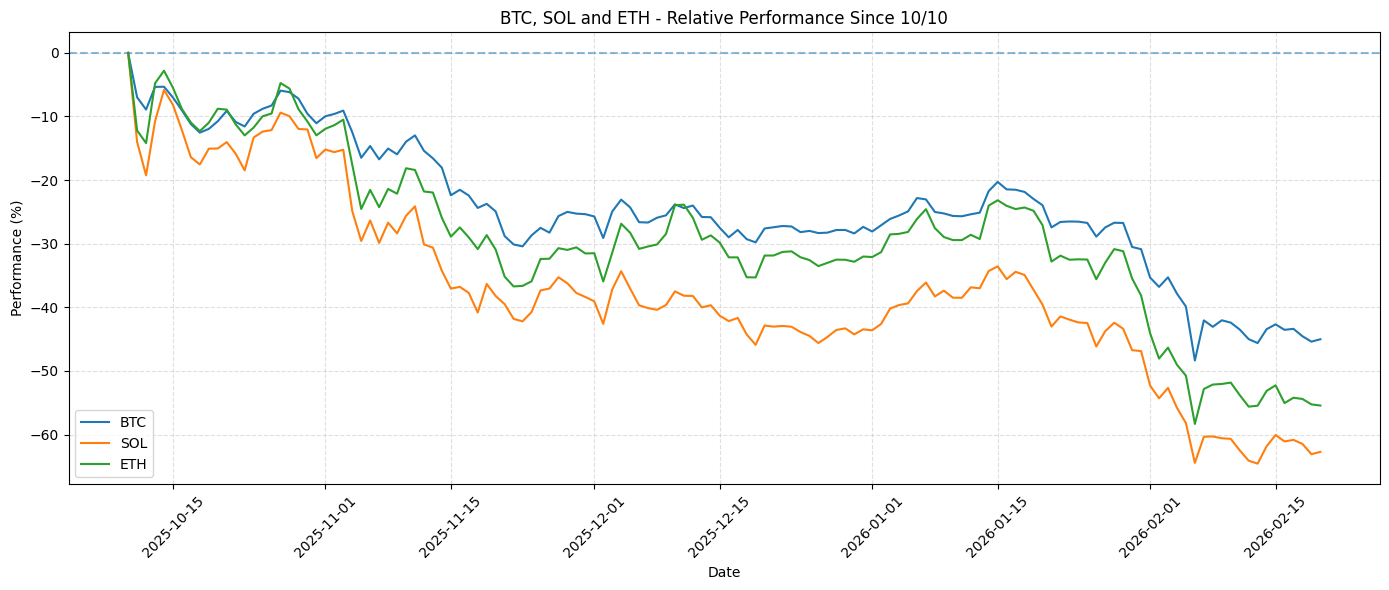

10/10 (The day which changed everything)

The October Liquidation event occurred due to bad designs revealed through macro pressure. It uncovered the weak design of many things across crypto, whether it was CEXs like Binance, which liquidated millions of dollars worth of positions due to incorrect prices of assets like USDe, BNSOL, and wBETH, or lending protocols like Silo and Morpho, which accrued bad debt from the Stream Finance blowup that occurred after a few weeks.

The prices of assets have not recovered since then, and the $19 billion liquidation cascade is still with us. DeFi TVL is down 44% from this event ($165 billion to $94 billion). Protocols revenue has decreased, and the bear market is officially underway.

The Alignment Issue

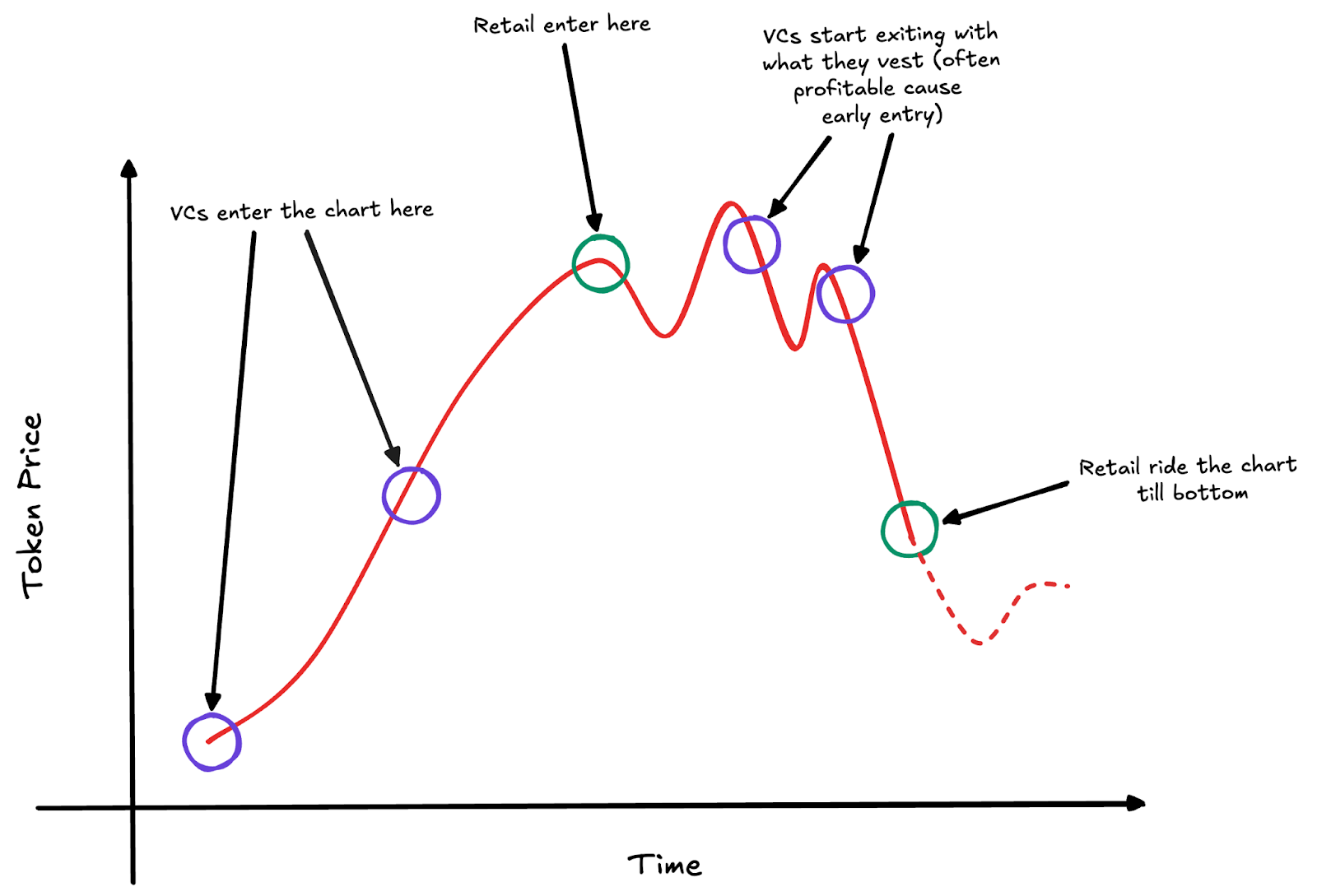

When you drive your car and let go of the steering wheel for a while, does it veer off course? If so, there are alignment issues with your steering wheels and tyres. Similarly, in crypto, this alignment issue is often seen between protocols and the tokens they launch. In December last year, when Circle acquired Interop Labs, the team behind the interoperability stack, Axelar, and the token (AXL) was not part of the deal, and it plummeted right after the announcement. That’s misalignment.

So why does this misalignment arise in the first place? There are always two entities related to a project: Labs and the DAO/tokenholders. Labs are the “team” in the tokenomics; they are the initial developers of the project, and they raise funds by selling a portion of their company and giving tokens to investors at an early stage in exchange for funds they use for growth. In some cases, VCs even get more favourable terms than anyone would expect, such as a “refund right.”

Tokens are not a legal representation of the business and don’t offer any actual rights over the company’s profits, unlike equity. Investors, when they receive tokens, have these rights through the equity they hold. So they are in a better position, but token holders? They are at the project’s mercy when it comes to aligning their product with their token.

This is something very few protocols focus on. They usually show this alignment through token buybacks. Hyperliquid does the buybacks to strengthen this alignment. Some might argue that they should use the collected fees to contribute more towards their protocol growth, maybe incentives, strengthen the insurance fund, and they would be right. These are the things that should be done, but building a moat around a good token is the best marketing strategy. Making your users wealthy is the best thing a product can do, and that’s what Hyperliquid did with its first airdrop.

Aave, the largest DeFi protocol, uses its revenue to conduct buybacks and also faces a similar argument about the better use of funds and directing them towards growth (I am aware of the current misalignment and hope DAO and Labs resolve it for the betterment of the AAVE token). Last year, Uniswap, after over 5 years of its token’s existence, completely aligned with its token and tokenholders.

These protocols are doing what’s right with their holders. There are obviously others; I won’t mention everyone, but still, there are fewer than we need. These are the tokens which deserve to go higher. Everything else should just go down, and people should rotate to the protocols that are generating revenue and are most aligned with their tokens, doing buybacks, growing themselves, and trying out new ways to attract more users.

Now, am I saying these tokens are best to invest in? Probably not. I am not giving any financial advice; I am just telling you what to look for when investing in any protocol. Whether it goes up or down, it comes down to the token unlocks spread across the years (tokenomics), the incentives they are distributing (which contribute to token dilution), and other expenditures. So, even if a buyback program exists, the sell pressure would still be greater.

Closing Thoughts

Crypto is currently going through one of its discovery phases, where speculative tokens will stop receiving inflows, and the real tokens, which have an underlying business supporting their growth, will emerge. Not many people realise this and see the opportunity, but protocols with real revenue are what matter at the end of the day.

They are already growing, they are already trending, if not today, soon.

The era of non-cash-flow-generating tokens has ended, as evidenced by the numerous failed launches over the last year. This is why the MegaETH KPI-based launch makes sense: it first tries to determine the chain’s and its product’s demand, run some revenue numbers, and then launch a token. Another interesting model they adopted is the launch of USDm, in collaboration with Ethena, to prevent the value generated by stablecoins from being routed out of the ecosystem and use it for token buybacks. Time will tell whether their model succeeds, but it’s a good starting point for reconsidering how token launches work today.

So yes, crypto is evolving, and most crypto assets should go to zero, except for a few.

written by Noveleader ✍️

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram guy, you can read all of our research without the noise on our TG channel:

| A guest post by

|