Options from a Builder’s Perspective

A Gap Analysis with Interviews from Rysk, Derive, Panoptic, and GammaSwap.

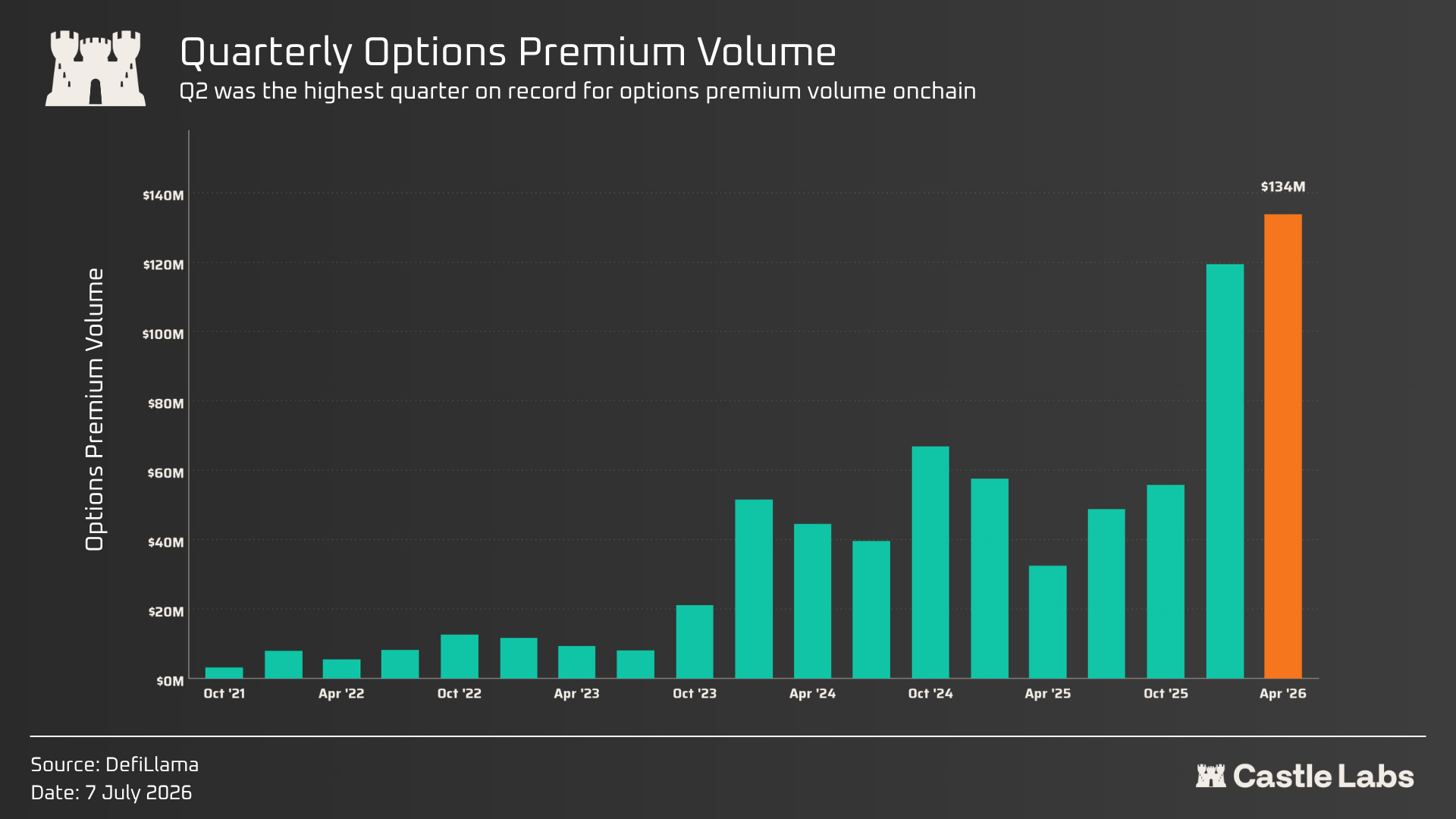

Options just had one of their best quarters in years.

Quarterly premium volume is at an all-time high, and options-linked tokens are beginning to catch a bid. DRV is up 37% from its June lows, while SYN is up more than 10x in a month after Synapse pivoted into Hyperliquid options via Hypercall.

This comes at the same time as Paradex launched its options product, and as Lighter announced plans to expand into options this quarter, shortly after announcing a new Robinhood Chain instance that will be accessible directly through the Robinhood Wallet.

We have had mini options cycles before, and 2021-2023 left behind a graveyard of protocols that never found consistent demand.

So is this time actually different?

We asked four teams building in this market why onchain options never saw the adoption curve of perps, what’s changed this cycle, where the real bottlenecks still sit, who’s actually using these products, and what would count as genuine success moving forward.

Dan, Co-founder of Rysk

Guillaume, Founder and CEO of Panoptic

Devin, Co-founder and COO of GammaSwap

Sean Dawson, Head of Research at Derive

Each team approaches the market from different angles with their product: Rysk packages options into income products; Panoptic builds oracle-free perpetual options from AMM liquidity; GammaSwap is moving from AMM-native volatility into binary markets; and Derive runs a professional options exchange on its own L2. Their diagnoses, on the other hand, were nearly identical.

Dan got straight into the main gaps for options, saying onchain options spent years “copying the perp model,” which was a fatal mistake. Perps combine an entire market’s demand into a single book, while an options exchange splits it across a range of strikes and expiries, fragmenting liquidity into separate, thin markets.

Guillaume at Panoptic highlighted the market maker side. They “have to update hundreds of quotes after every price move, which is quite difficult to do on a blockchain,” he says, and the fragmentation causes traders to get trapped in their trades because the liquidity for deep in-the-money or out-of-the-money positions to exit is not there. Sean at Derive says the gap between options and perps boiled down to the fact that greeks, options boards and “nonlinearity is often overwhelming and turns people off options.”

When it comes to highlighting the key change that has resulted in a revival of onchain options, they all agree it’s yield. Through 2023 and 2024, the appeal of strategies that sold volatility was limited, as other strategies, such as the basis trade and double-digit yields on stablecoins, paid out with greater simplicity. Guillaume reckons it’s “quite difficult to achieve >5% yield nowadays without resorting to looping strategies,” with Sean framing volatility as “the last product left that is unfarmed,” suggesting the category still had a lot left in the tank after only recently being ‘discovered’ by onchain users.

Crypto is a volatile industry, and is likely to stay that way, so selling that volatility is a source of yield that will continue and has yet to become saturated onchain.

Where they diverge in their thinking is on what has been missing to enable onchain options to gain more traction, which explains why each has built a vastly different product.

For Rysk and GammaSwap, the gap is closest to the user. For Dan, specifically, it’s trust. People got burned by products they didn’t understand in the past, and we shouldn’t keep trying to hide the mechanics; instead, we should focus on making outcomes transparent before a user commits. In particular, this concerns the premium shown in the protocol and the RFQ system's final execution. “Options are not the product.” People don’t want an option; they want what the option does for them. Devin, at GammaSwap, agrees: “Complexity is the enemy. Simplicity trumps everything.” The rest will follow: “If the UX is strong and you have retail flow, market makers will inevitably come in.”

Guillaume sees the problem lower in the stack; rather than focusing on the interface or user education, he believes onchain options lack real demand and a greater range of collateral. The institutions he is targeting are not chasing 100x leverage. They need “a mature risk management layer” and “portfolio-wide margin,” in which deposits, assets, and options positions can be netted against each other rather than fully collateralised in isolation. That is also why he is focused on tokenised assets. If stocks, funds and RWAs move onchain, they will need hedging markets where those assets are issued.

Sean sits closer to the exchange view: liquidity has historically been the biggest blocker, because strikes and tenors fragment markets and widen spreads. Some of that has improved, especially as Derive found demand around HYPE options, but education remains a major gap. “Reading an options board for a newbie is impossible,” he says.

As expected, there are a multitude of gaps, with each builder’s perspective shaped by their own experiences building, but we do keep coming back to the same core themes: UX, demand, collateral, and education.

Each product has a separate core group of users. Rysk’s are holders earning income on what they already own, from individuals to treasuries, DAOs, and institutions. Panoptic has advanced users and market makers for now, but aims to widen that through its vaults. GammaSwap has historically been for sophisticated retail investors, but it wants to expand beyond crypto by offering non-crypto-correlated assets and a simpler interface. Derive was built for professionals but recently rose to prominence due to retail demand for HYPE options.

They also define success differently. Dan wants to see volatility yield widely referenced and quoted on terminals, alongside lending and staking. Guillaume wants funds and treasuries to use options to manage risk rather than retail chasing pure speculation. Sean wants onchain volume to increase to a level comparable to CEXs, the way Hyperliquid now stands next to Binance. Devin thinks options have already found PMF onchain through prediction markets, but nobody noticed, as they are binary options in all but name. He now wants to see substantial growth in fees across the sector.

The demand for options is growing. Traditional markets show this across both retail and institutional channels, while recent onchain traction suggests the same demand can emerge when the right strategy is paired with the right asset and presented to the right user, with HYPE options as a prime example.

The early iterations of option protocols focused on education, teaching users about the value of options. In the current forms, protocols are instead focusing on simplifying options and framing them in terms of their utility and what they can do, ideally reaching the point where users don’t even know they are using options in the back end, while fully understanding each outcome.

If this has interested you, make sure to check out our flagship report on The Renaissance of Onchain Options, published in collaboration with @BlockScholes.

You can find all our research published directly on our website at: https://castlelabs.io/research

Also, don’t forget to join our Telegram channel for the latest updates and reminders of our publications: https://t.me/castlelabsreads