Pre-IPO Markets are Moving Onchain

2026 is one of the most eventful years for IPOs, with the biggest IPO calendar in a generation.

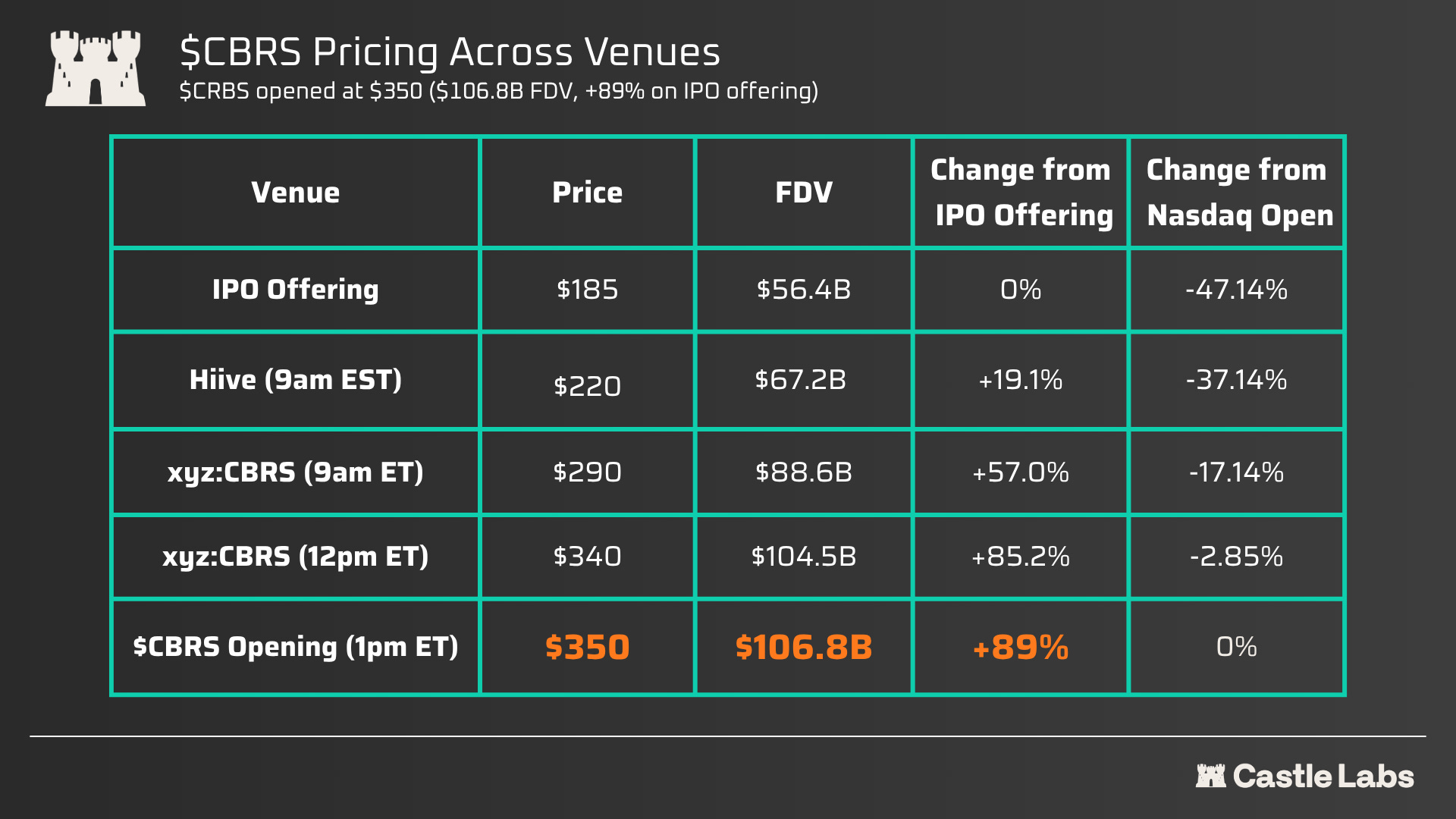

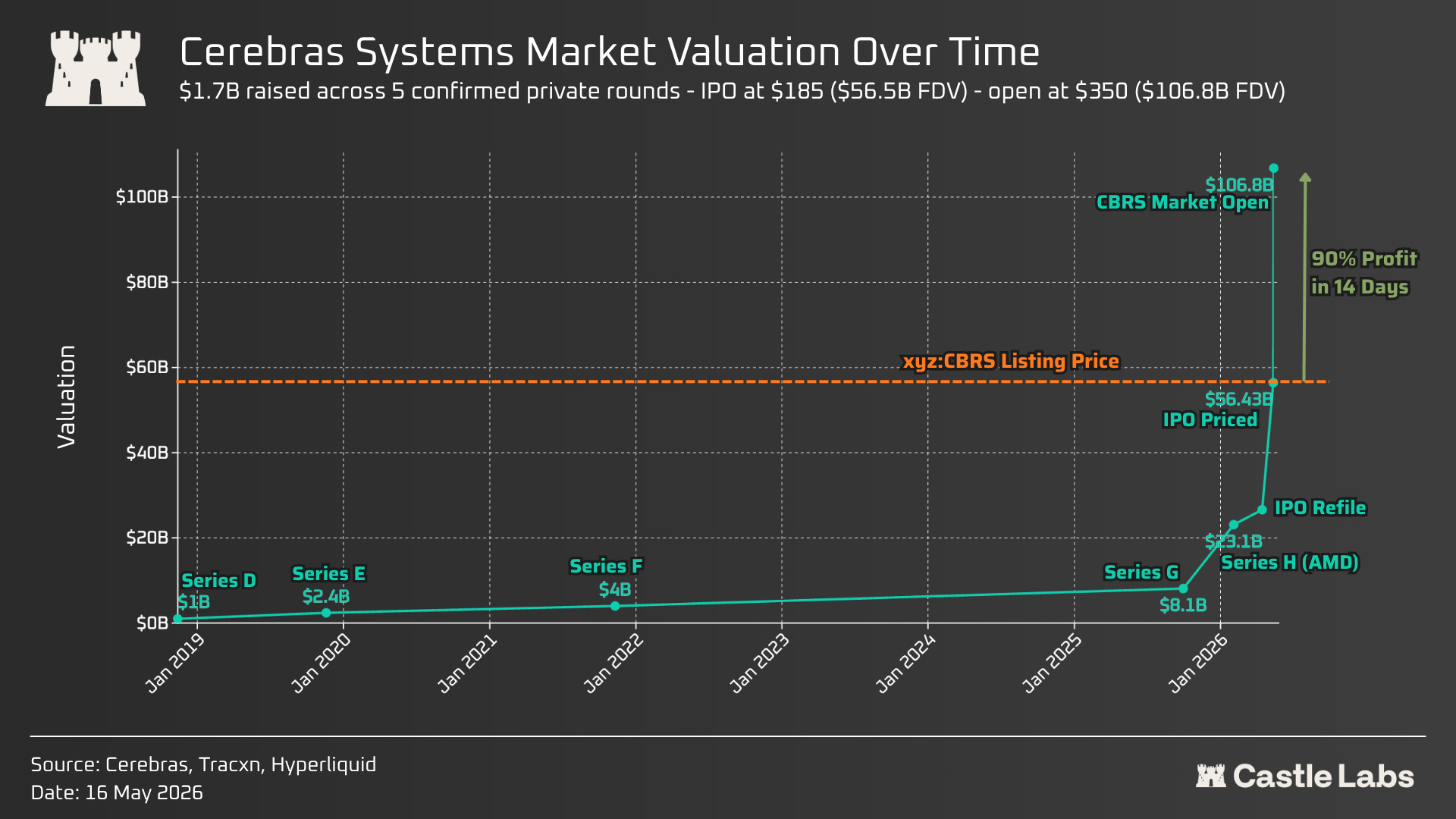

On Thursday of last week, Cerebras ($CBRS), the first Pre-IPO Perpetual Market (IPOP) from TradeXYZ, opened on Nasdaq at $350, following a repriced IPO offering of $185.

An IPOP is a synthetic perpetual that reflects the implied value of a private company before it goes public. The traditional IPO book has been oversubscribed by more than 20 times, leaving both accredited and retail investors unable to secure the level of exposure to the asset they wanted. In contrast, an IPOP for Cerabras had been active on Hyperliquid for two weeks prior, with prices dipping below $200 during the first few days of May, guaranteeing broader accessibility to these assets.

While these onchain markets primarily offer access, it was the pricing that captured the world’s attention. Morgan Stanley, the lead book-runner of the IPO, was observed tracking the price on Hyperliquid before the stock went live.

On the morning of the event, Hiive, the primary offchain platform for accredited investors, was valuing the stock at $220. In contrast, TradeXYZ was the only venue providing real-time pricing for the asset, with ~$290 in the morning and ~$340 one hour before the Nasdaq opening.

Cerabras was TradeXYZ’s first IPOP test, and after a successful conversion to a standard perp (which follows an external oracle pegged to the official pricing of traditional markets during open hours), more assets are being listed on the platform.

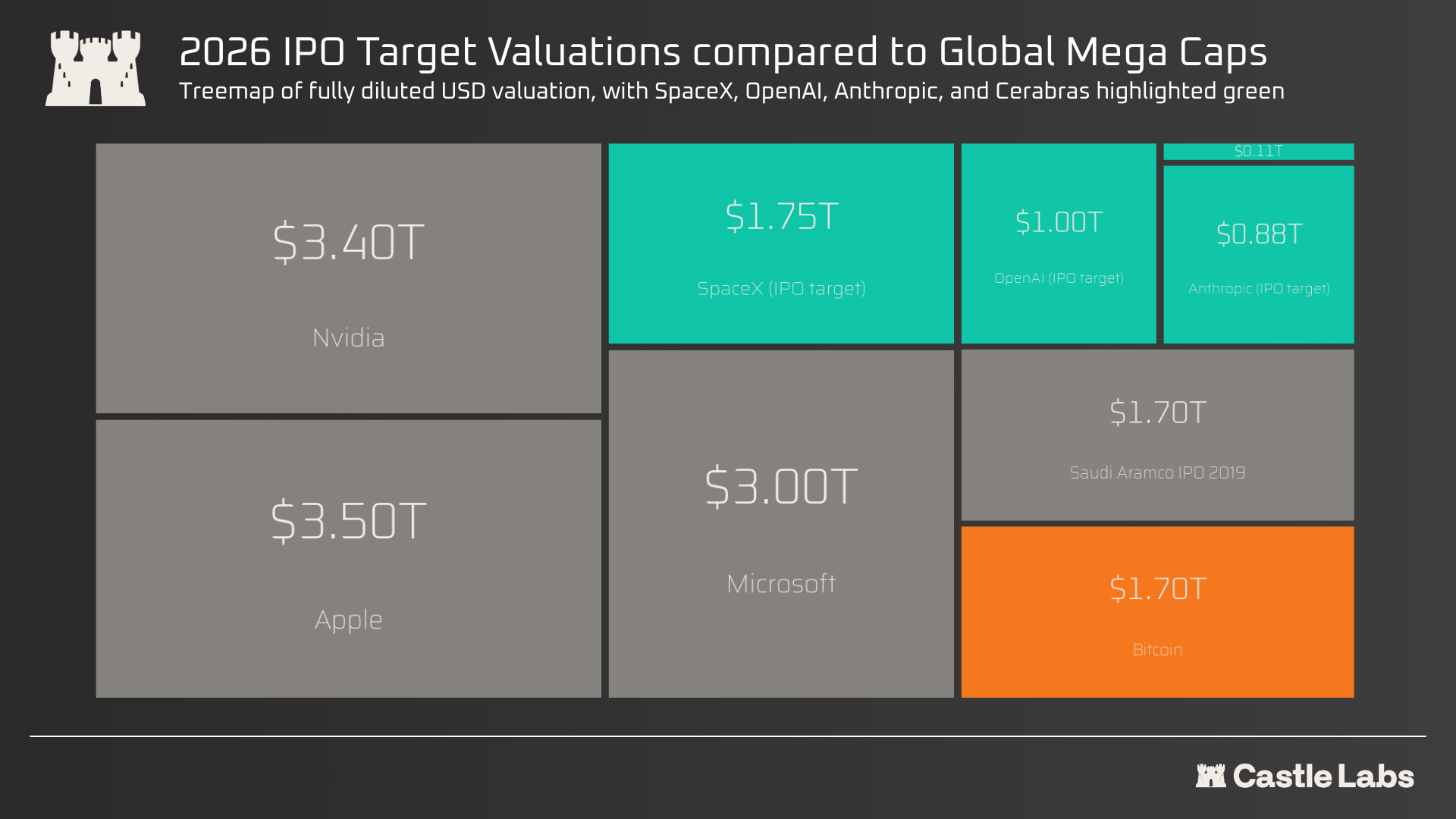

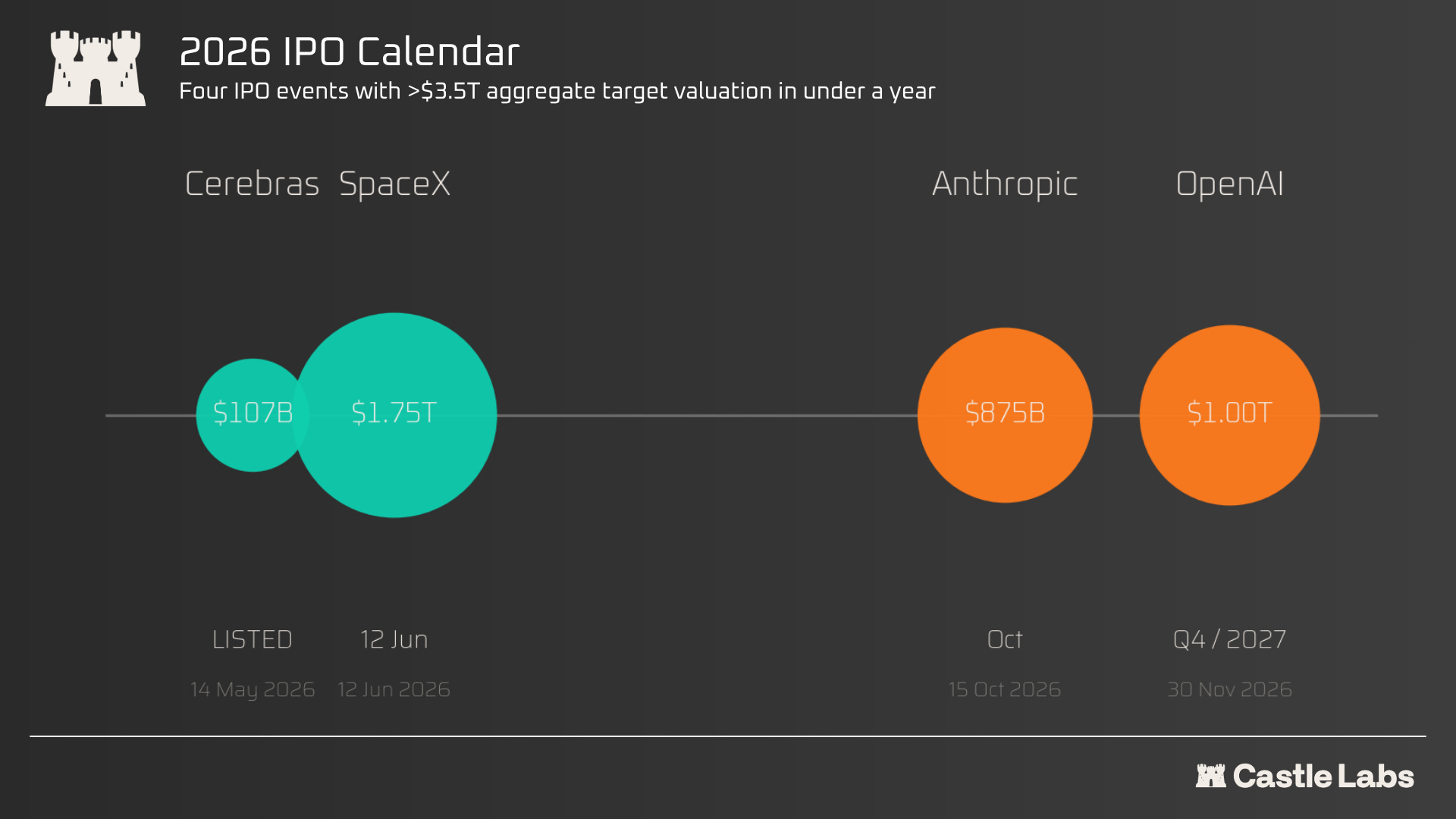

Among those, SpaceX was listed ahead of its Nasdaq target of June 12th. This will be the biggest IPO of the upcoming years, with an offering over 30 times Cerebras’s, making it the largest IPO in history and outsizing Saudi Aramco’s 2019 $1.7 trillion offering.

CBRS: The warm-up

Cerebras raised $1.7 billion across five private funding rounds over seven years. However, retail investors had limited opportunities to participate, facing challenges in accessing the IPO for exposure. This changed with the IPOP on TradeXYZ.

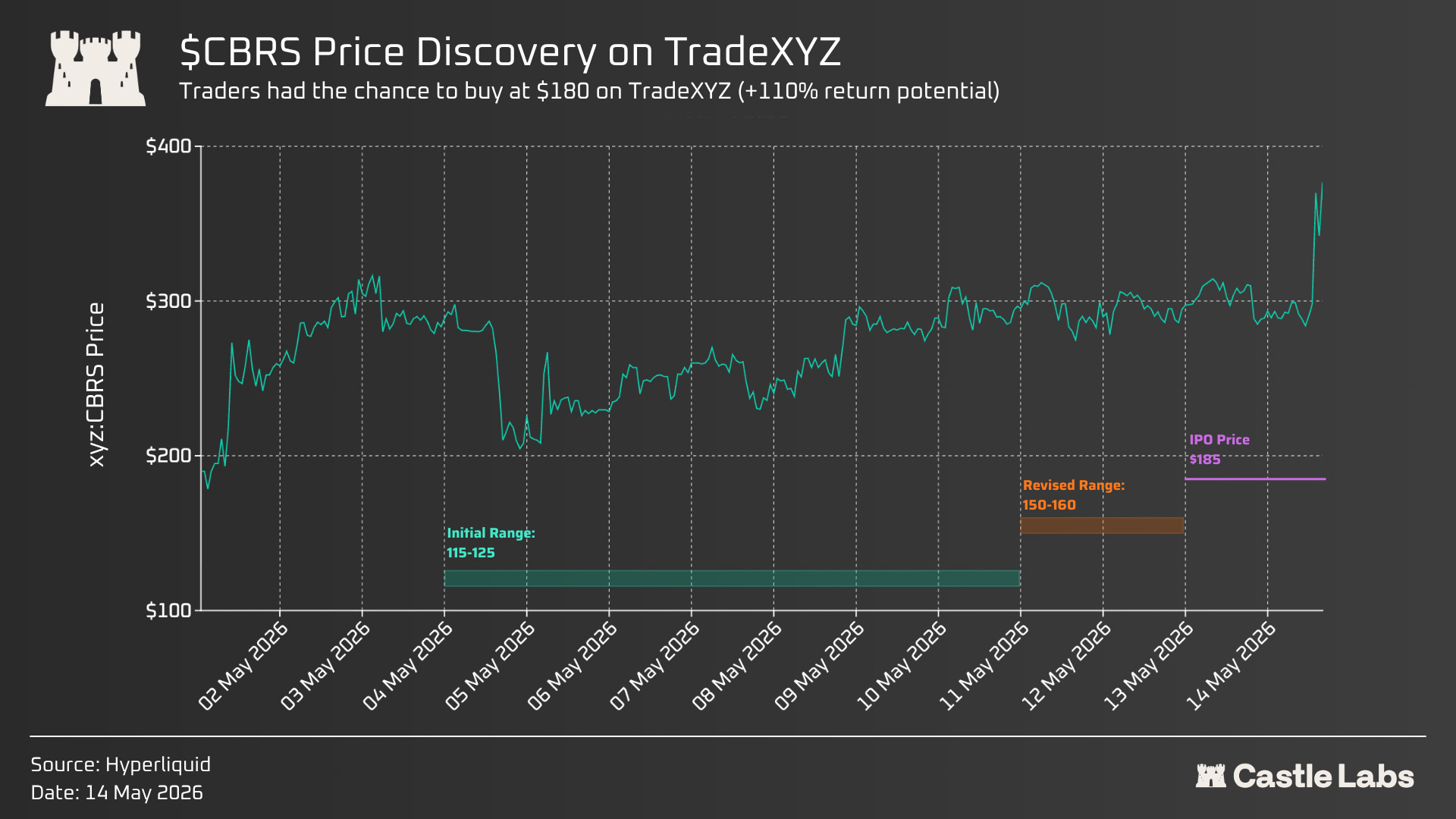

On May 1, TradeXYZ launched xyz:CBRS at a reference price of $175, reflecting an implied valuation of $48.9 billion. At this stage of the market’s lifecycle on TradeXYZ, there is no external price influence, as the price is driven entirely by order-book demand and expectations around the Nasdaq open. Traders on the platform consistently valued the stock well above the initial IPO range of $115-125, both as it was revised to $150-160 and as it was finally priced at $185.

TradeXYZ allowed anyone with a cryptocurrency wallet to gain exposure, potentially yielding over 90% profit if held until the Nasdaq opened at $350, just 14 days later.

This represented the largest valuation increase the company had achieved in such a short time. In essence, it was the best period to leverage perpetual exposure, captured entirely onchain on Hyperliquid.

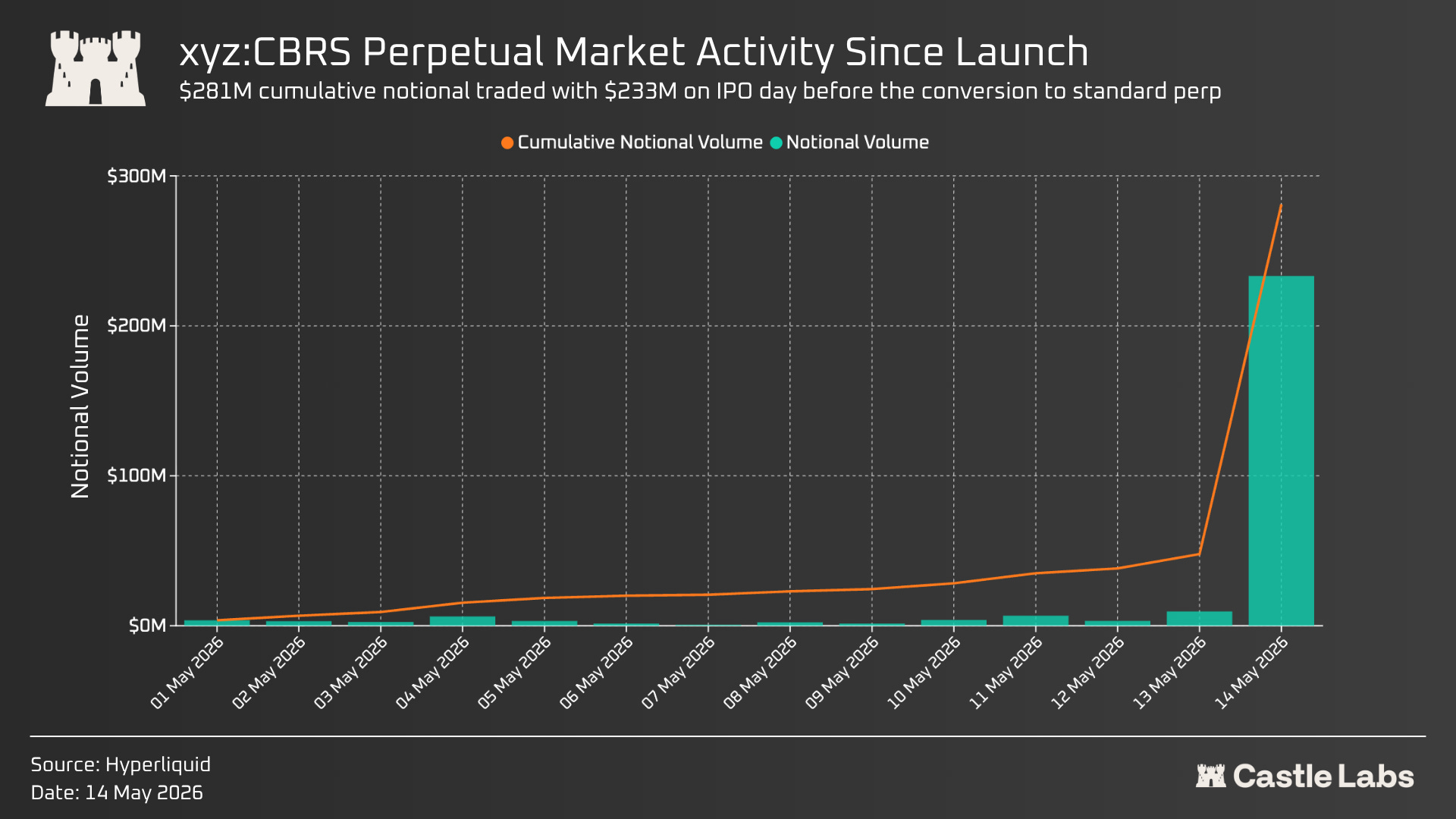

xyz:CBRS traded $281 million of cumulative notional across its 14-day pre-IPO window, with almost all of it landing on the listing day itself. Daily volume sat between $1.5 million and $9.5 million over the first 13 days as discovery built up with little attention, before 14 May printed over $207 million, 80% of the market’s lifetime volume.

Spreads, on the other hand, were wide by listed-equity standards, but tightened into the listing.

The median bid-ask spread across the IPOP window was 61.4 bps, with median visible depth within 50 bps of mid of just $2.3K, as shown by Shaunda Devens, Research Analyst at Blockworks. Both numbers improved sharply through 14 May as the market approached the Nasdaq open and even more so post open. Even after Nasdaq halted just after the opening bell, TradeXYZ remained open and closely aligned with Nasdaq as soon as it reopened minutes later, maintaining tight pricing relative to the Nasdaq over the following hours.

Why can’t this be done with shares?

The traditional pre-IPO market is built on share transfers. Every transaction is a legal transfer of equity from one holder to another, creating huge friction for efficiency due to the following constraints:

Issuer permission: Private companies control their cap tables. Every secondary trade either gets board approval or uses a structure that the issuer tolerates.

Accreditation: A share transfer is a securities transaction. US law requires buyers to be accredited.

Settlement is discrete: Legal review, the transfer agent, and escrow are all involved, and the process can take weeks or months.

Minimum lot sizes. Transaction costs make it worth it for brokers below a certain amount.

These constraints remain intact, regardless of the wrapper used.

Direct marketplaces such as Hiive and Forge facilitate these share-transfer transactions.

Closed-end funds (e.g., ARKVX, VCX, RVI) wrap shares in exchange-traded or interval vehicles.

Pooled Special Purpose Vehicles (SPVs) such as Hiive Funds and EquityZen single-company funds issue LLC membership interests against the shares the SPV acquired.

Tokenised SPVs (e.g., PreStocks, Jarsy) issue onchain tokens against the same type of LLC.

Furthermore, IPO companies are also taking steps to preserve these markets for investors. On May 11, Anthropic took significant action by directly targeting its stock transfer mechanisms. The company declared all unauthorised secondary transfers of its shares null and void, naming eight platforms across the stack. In the same week, OpenAI issued a related warning. Crypto lawyer Gabriel Shapiro flagged the legal mechanism: a voidable transfer can be ratified in court, whereas a void transfer is considered never to have existed. This means that chains of secondary trades can be entirely erased from a company’s cap table.

The action did not target a specific wrapper; instead, it targeted the underlying share transfer on which all wrappers rely. If the transfer is legally non-existent, then the claims linked to it are effectively claims against nothing. PreStocks tokens tied to Anthropic and OpenAI dropped roughly 40% in the days that followed.

The synthetic perpetual model is unique as no shares are exchanged at any point in the chain. This also has legal implications: the contract refers to the implied value of a company without representing ownership in that company. There is nothing for the issuer to invalidate, nothing for regulators to claim ownership of, and nothing for broker-dealers to incorporate into a financial pipeline.

Now, this model comes with its own risk surface. The contract has no legal claim on the underlying. The mark price is derived from the order book itself rather than anchored to a tradable spot market, so pricing depends on venue liquidity. As Borja Neira put it: the trade is “long implied valuation +/- funding + liquidity risk + mark-price risk + settlement risk + the absence of clean arbitrage against real shares.”

This is not the cleanest way to buy equity by any means. However, IPOPs go beyond offering exposure, serving as a price discovery venue for the world’s most inaccessible private companies at a time when their hype has never been higher.

Whether this architecture effectively facilitates real-time pricing, continuous discovery, and retail access at real scale is a separate issue. Currently, three venues are implementing this model onchain, with OKX joining the category in the last weeks, but only Tradexyz has completed a live IPO conversion, pricing within 6% of Nasdaq’s open.

The next section explores these models and the reasons behind TradeXYZ’s early success.

What pre-IPO perpetuals have to offer

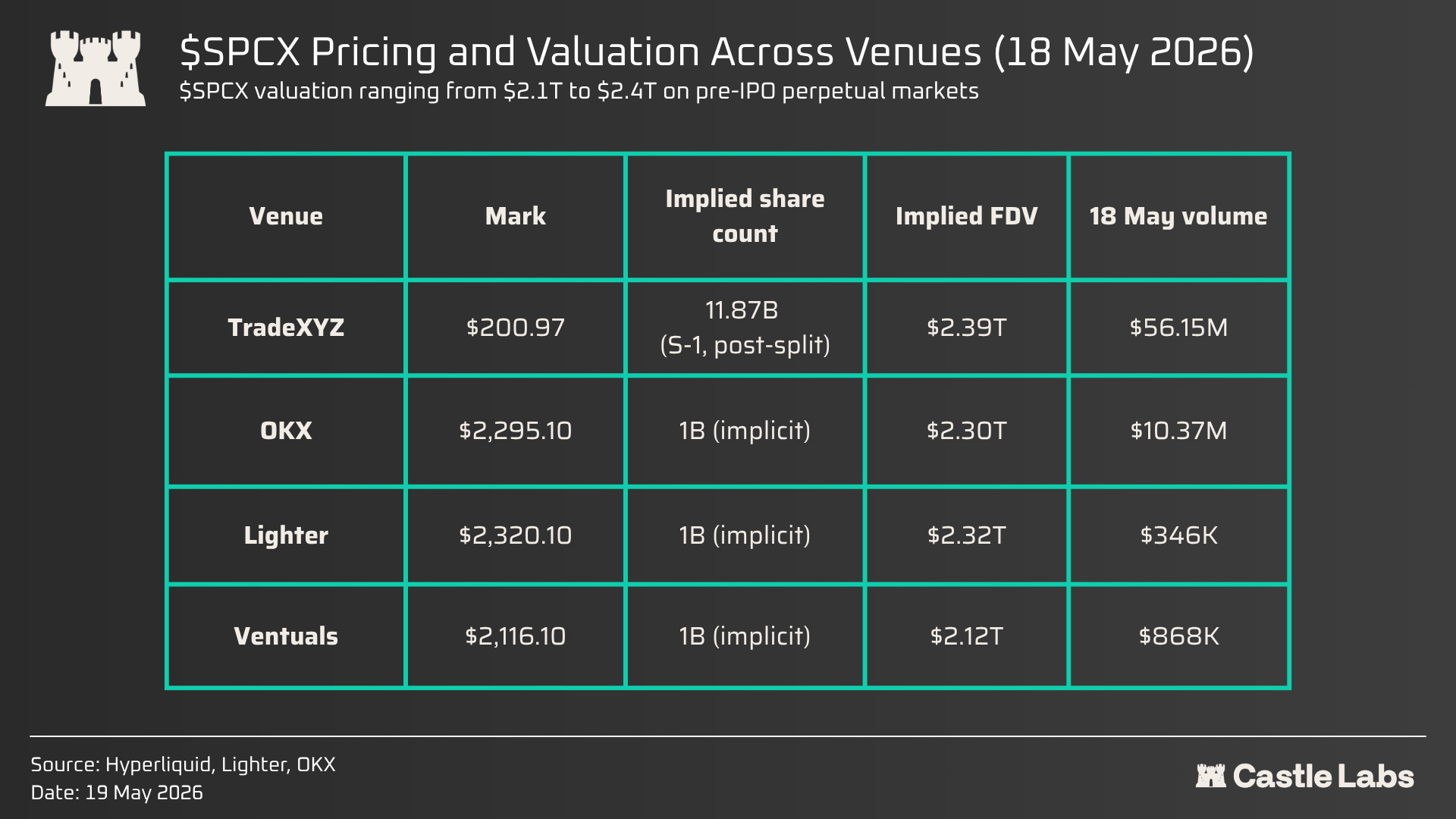

Four venues run synthetic pre-IPO perpetuals: TradeXYZ and Ventuals on Hyperliquid HIP-3, Lighter on its own L2, and OKX as a CEX.

We can observe price discrepancies across venues due to differences in share counts. Trade XYZ uses the actual post-split share count of 11.87 billion from SpaceX’s S-1; everyone else uses an implied 1 billion, since they opened their markets earlier.

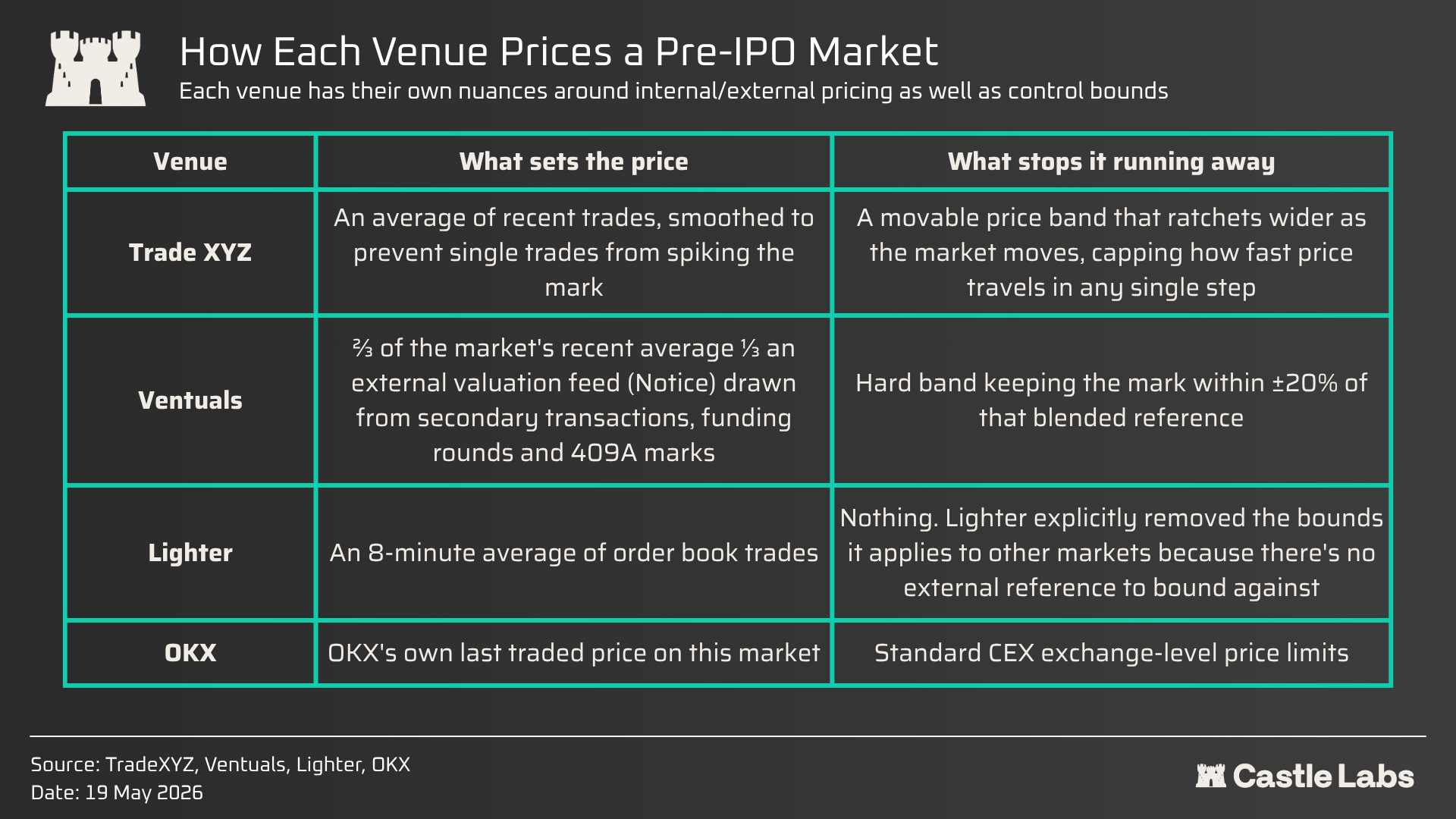

How each venue prices a pre-IPO asset

Every venue is solving the same problem: what should the mark price equal when there’s no public spot market to reference?

TradeXYZ, Lighter, and OKX use internal pricing only, whereas Ventuals strongly pushes prices back to an external valuation. However, pulling from external references, whether Hiive bids, Forge transactions, quarterly 409A marks, or last-round valuations, means importing their inherent staleness. When internal pricing is used, the trader is the source of price discovery.

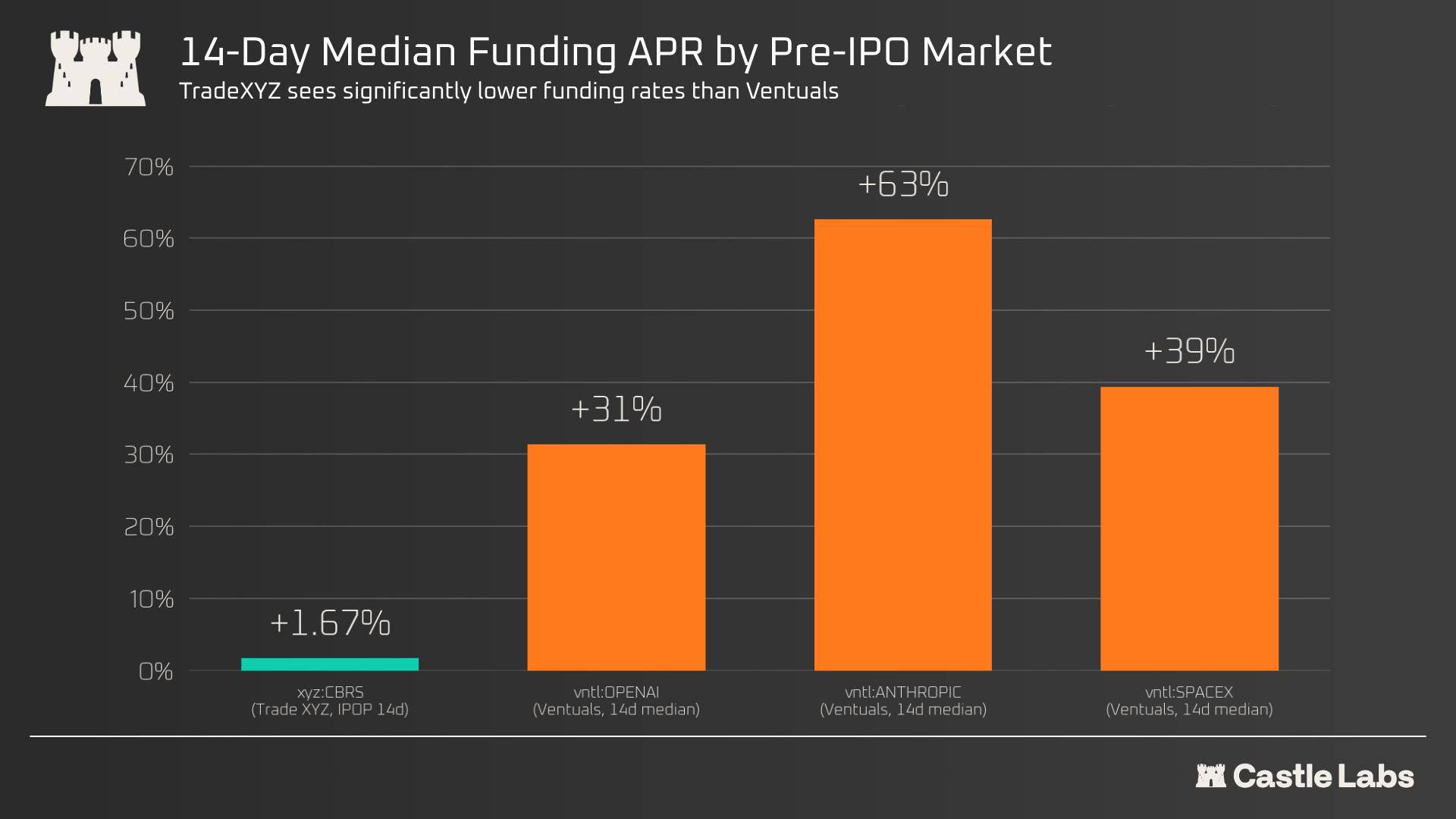

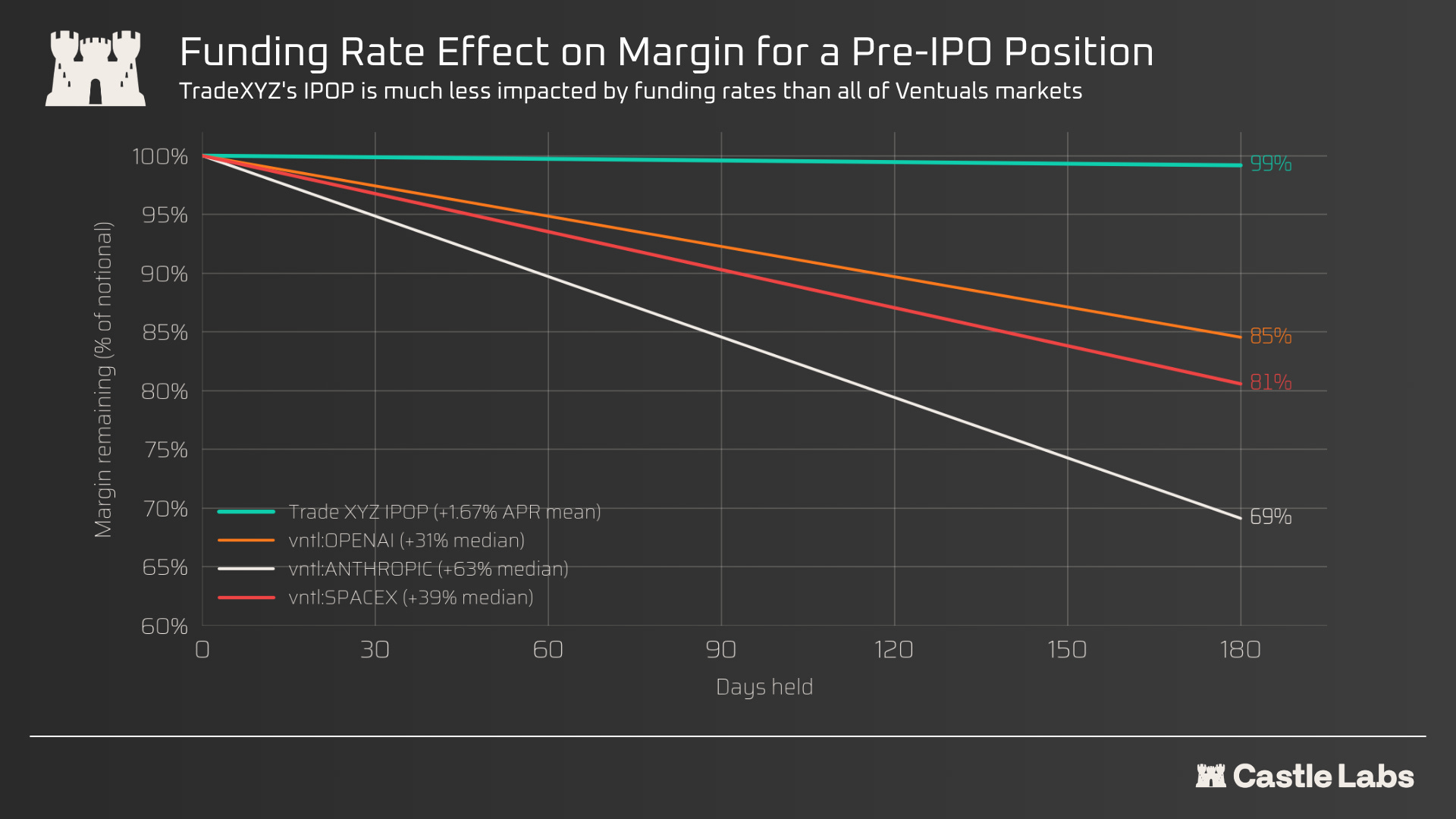

If pricing mechanics are one half of the equation, funding rates are the other half. For a trader holding a position during a volatile period, such as an IPO, the cost of carry is extremely important. Trade XYZ applies a 0.005 funding multiplier to IPOP markets, which is 1% of their standard perp rate. As a result, xyz:CBRS averaged +1.67% APR across its 14-day pre-IPO window. In contrast, Ventuals, Lighter, and OKX use their standard funding in a market with one-way directional demand, producing significantly higher APRs: +31% for vntl:OPENAI, +64% for vntl:ANTHROPIC, and +39% for vntl:SPACEX, all 14-day medians.

As an example for SpaceX: a trader holding xyz:SPCX from today to the 12 June Nasdaq open pays roughly 0.1% of their notional in funding. The same position on vntl:SPACEX at its 14-day median APR of +39% would cost ~2.7%.

Why TradeXYZ is seeing the flow

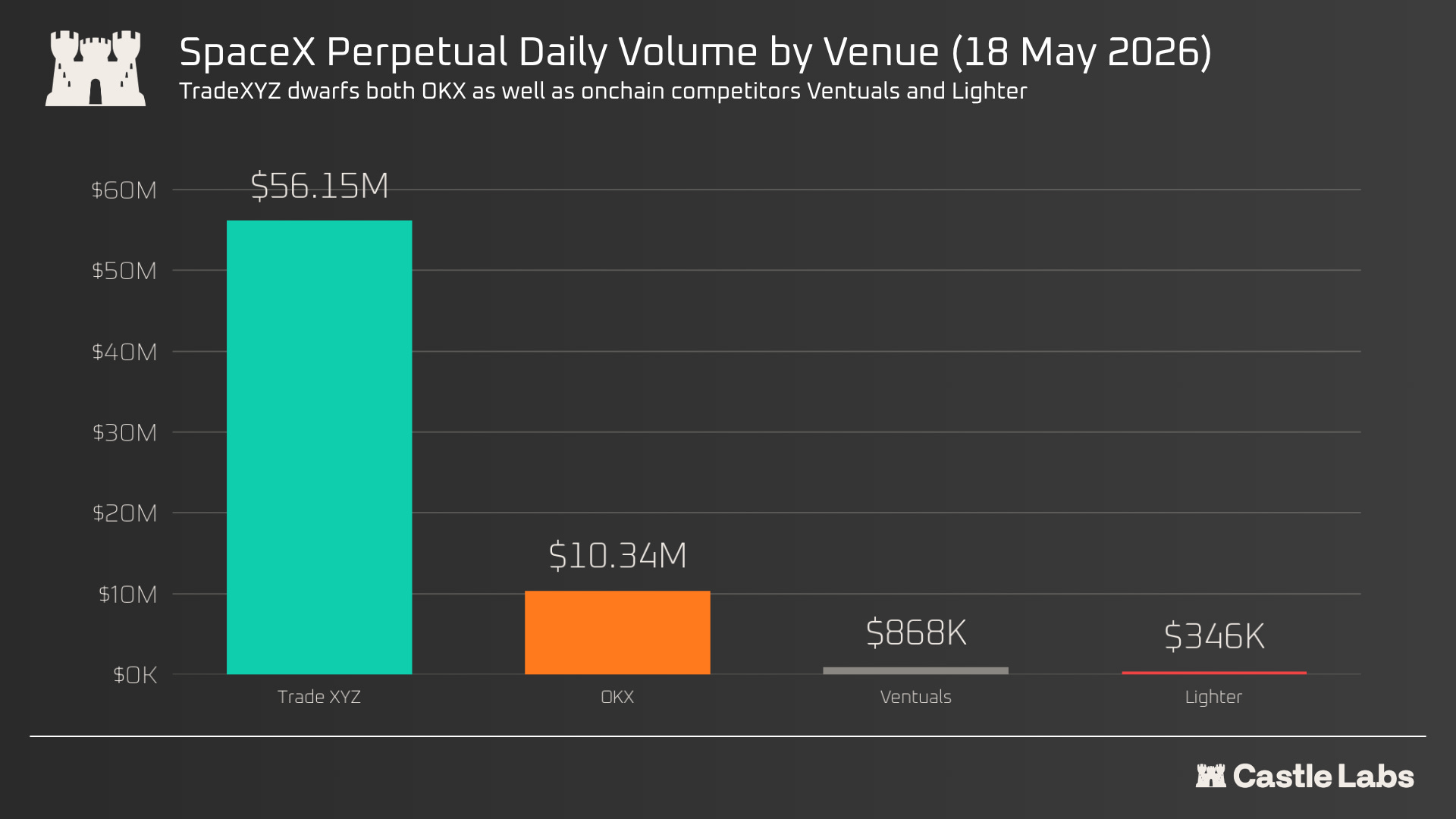

Both Ventuals and Lighter have struggled to keep pace with the IPOP activity on TradeXYZ. Even OKX, a top-five CEX with a substantially larger global user base than Hyperliquid, is seeing lower volumes.

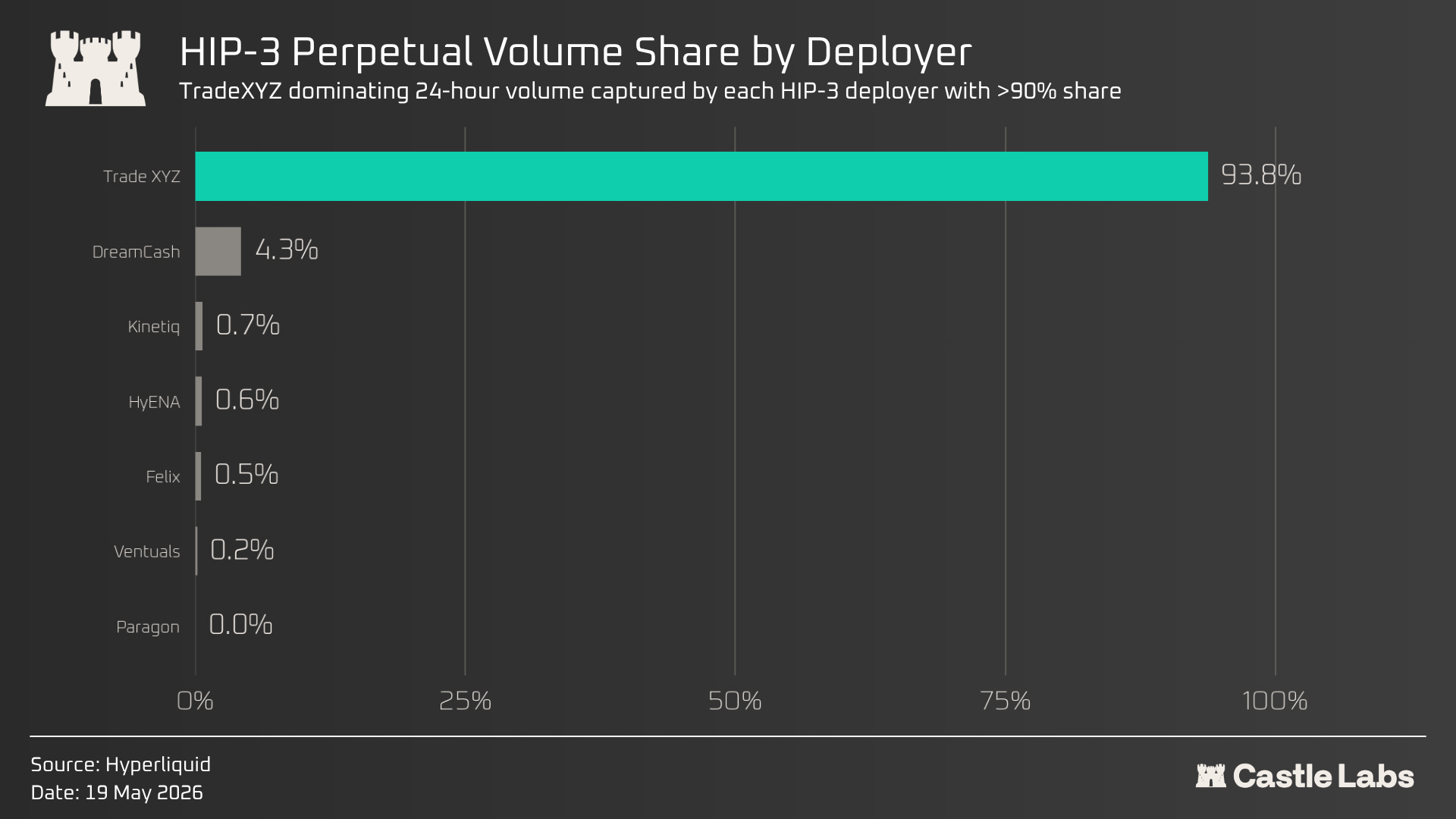

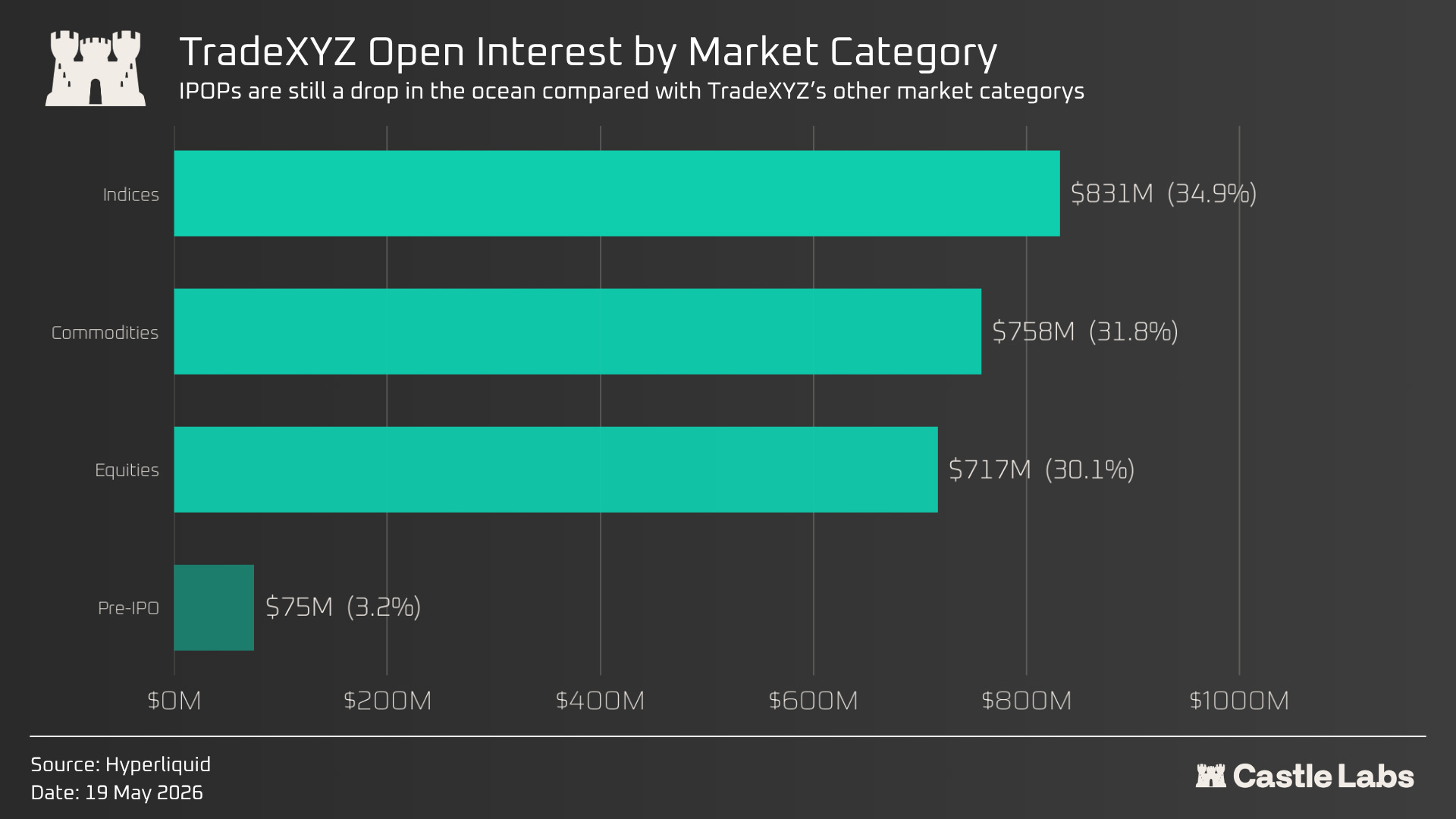

What TradeXYZ had that the others didn’t was an existing trader base. Since launching on Hyperliquid in October 2025, Trade XYZ has built the largest RWA perpetuals venue onchain. As of 18 May 2026, it accounts for ~93% of HIP-3 daily volume and ~95% of HIP-3 open interest across 77 markets covering commodities, equities, indices and pre-IPO.

This is also reflected in the growth in open interest (OI) on the platform for RWA markets as of May 18th, 2026: xyz:SP500 ($489M OI), xyz:XYZ100 ($371M), xyz:BRENTOIL ($316M), xyz:CL crude ($167M), xyz:GOLD ($114M).

The flow was built in stages. Gold and silver came first. Then crude oil, which during the late-February Iran conflict saw $1.62 billion in 24h trading volume and briefly outtraded ETH on Hyperliquid as traders piled into a market that was open when traditional venues weren’t. Then Brent. Then MAG7 equity perps. Then the officially licensed S&P500 perpetual in March (XYZ100), which has grown from $213 million OI at launch in early March to $371 million today.

By the time xyz:CBRS went live on 1 May, the audience was already there. They had a venue they knew and a team they trusted. They were being offered a new market on infrastructure they already used daily for gold, oil, and S&P 500 exposure. Pre-IPO on TradeXYZ succeeded because it was the next product in a GTM sequence rather than a standalone launch.

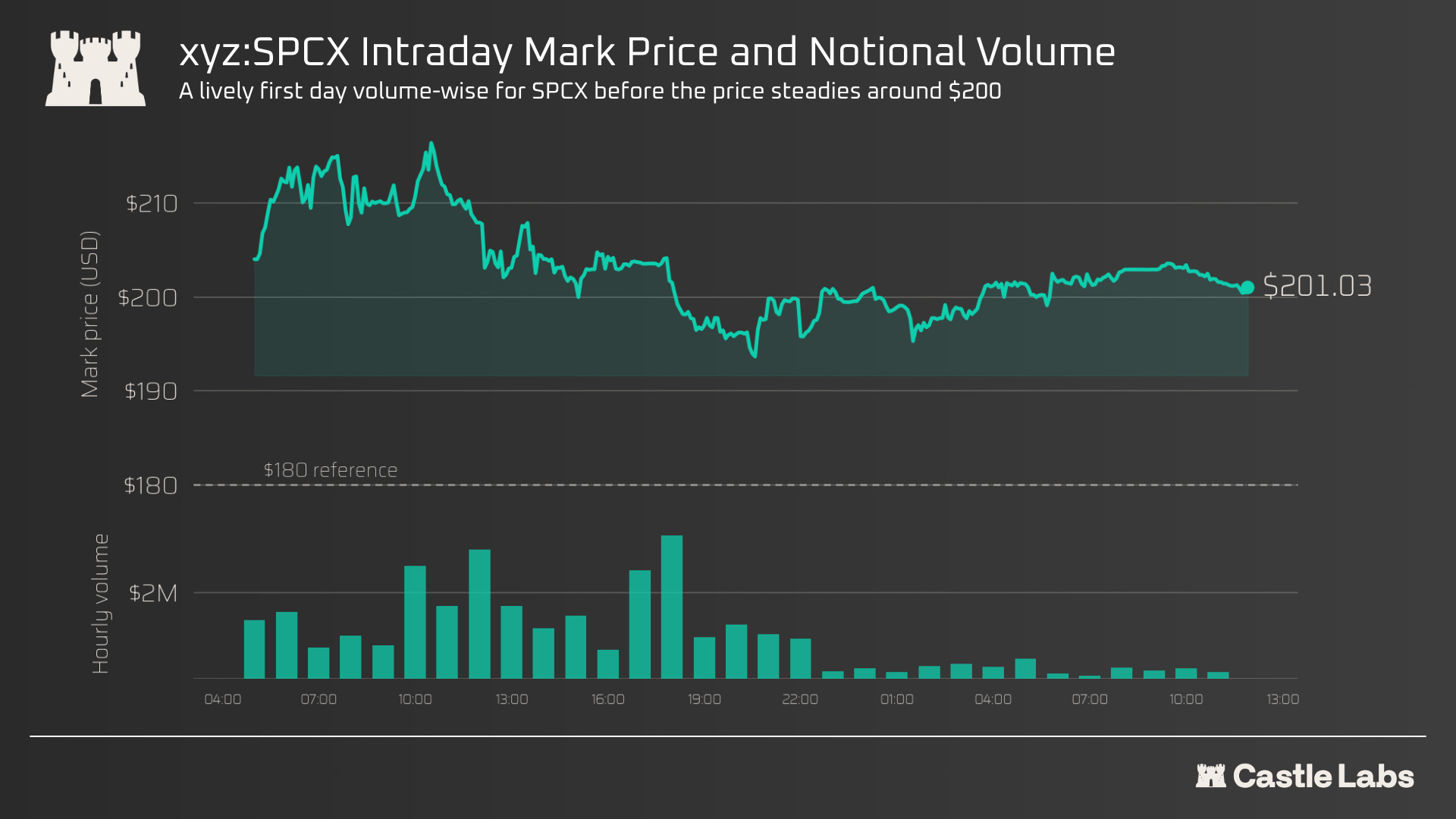

SpaceX and what comes next

At 05:16 UTC on May 18th, 2028, Trade XYZ listed xyz:SPCX with a reference price of $180. Within the first minute, it printed $204. By the end of the first hour, it had ranged from $204 to $218, settling at $211.75. As of this writing: mark $203.14, cumulative session notional $50.67 million, open interest $25.49 million, roughly 42k trades.

SpaceX is queued to list on 12 June 2026 at a $1.75 trillion target valuation. Behind it: Anthropic in October 2026 at $850-900 billion and OpenAI by Q4 2026 or 2027 at $1 trillion+. A total of $3.5 trillion.

To put that in context, between 2015 and 2024, the US IPO market raised an average of roughly $50 billion per year.

Whoever manages to capture volume in secondary markets and broader financial mindshare through price discovery will be hugely successful, and TradeXYZ is set to be the front-runner.

What makes this stock particularly interesting for an IPOP is Elon, the CEO of SpaceX. He is the most followed individual on X, a platform he himself owns, and has a track record of moving markets with his posts. He just approved a 5-for-1 split of SPCX on 15 May and announced a 30% retail allocation in the IPO, well above the institutional norm. Let’s see if he brings any eyeballs to the xyz:SPCX market.

Whatever happens, the SpaceX IPO will be monumental and priced live onchain.

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram person, you can read all of our research without the noise on our TG channel: