Prediction Markets: From Curated Platforms to Open Protocols

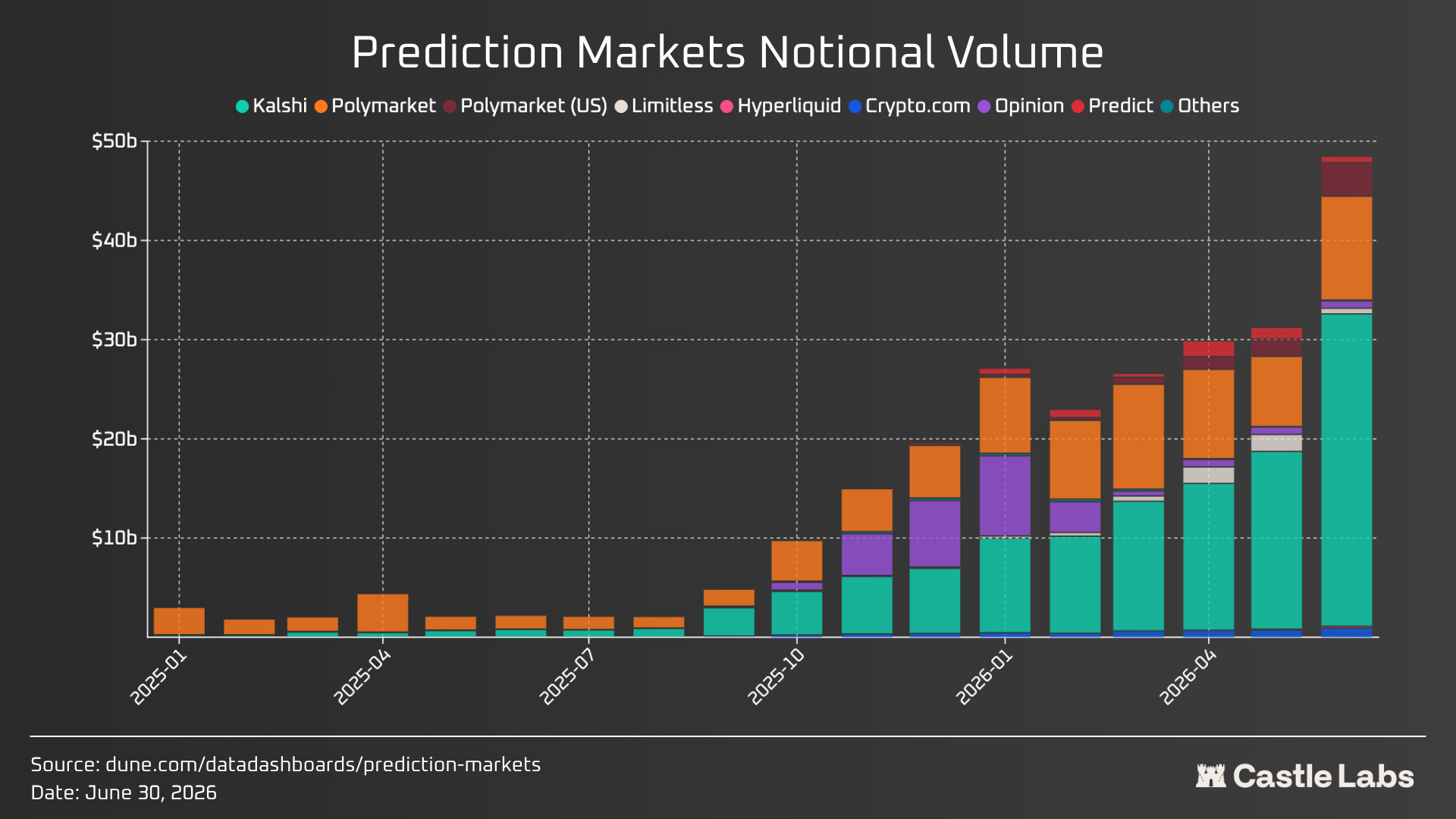

In the last 18 months, Prediction markets (PMs) grew from roughly $2 billion in monthly volume to more than $30 billion, scaling rapidly from a niche category to a mature ecosystem.

PMs have slowly become a combination of information markets, a differentiated hedge tool, and a way to trade and predict on categories such as sports, politics, macroeconomics, and more.

From trading niche categories like “What will be said in a particular podcast” to predicting “Fed rate cuts decision”, a user can choose to trade anything and everything.

This growth came almost entirely from the curated model, in which a small set of platform-appointed entities determines which markets exist. Polymarket and Kalshi, the incumbents, built themselves within this model by tightly controlling what gets listed, and the market rewarded them for it.

The curated model works, but it isn’t the same vision as that adopted by earlier product iterations in this category. PMs initially targeted the permissionless creation of markets, where anyone could launch one on any topic. But most products (Augur, Omen, Zeitgeist, and others) built around this vision failed due to recurring problems with liquidity, resolution, creator incentives, and regulation.

The lesson the industry drew was that open curation doesn’t scale, but this conclusion is being tested again. A new wave of products is entering the market, aiming to solve issues earlier iterations faced through better oracle infrastructure, scalable liquidity models, and more deliberate designs.

This report traces this evolution, examines why permissionless curation failed in the first place, why permissioned curation won, and how current products are trying to restore the permissionless nature of PMs. Additionally, we use Limitless as a case study, which has recently expanded into permissionless user-generated markets (UGMs), and examine how it has adapted to fit UGMs.

Early Prediction Markets: The Permissionless Approach

The power of PMs was first brought to the spotlight when Polymarket and Kalshi showed more accurate odds for the 2024 U.S. elections. Since then, PMs have evolved into much more than that.

Since the start of the year, prediction markets have consistently produced a notional volume exceeding $20 billion, and last month crossed $40 billion, with the largest contributions coming from the sector’s current duopoly: Polymarket and Kalshi.

PMs were among the first experimental primitives in crypto, and they started with a permissionless approach given the crypto ethos of decentralisation and permissionless participation.

Augur was one of the first products to launch in this category in July 2018.

Founded in 2014, its ICO was the first in the space and raised $5.5 million.

On Augur, market creation was fully permissionless.

This permissionless architecture came with its own problems as, within weeks of launch, Augur’s UI surfaced markets on political assassinations, plane crashes, and other legally toxic event types. Additionally, the problem set expanded to include technical limitations, such as high gas fees on Ethereum and settlement delays (resolutions can take up to 90 days due to disputes).

An interesting aspect of the product was its native REP token, which enabled holders to report outcomes by staking.

Augur is now rebooting in 2026 under the Lituus Foundation, as a resolution infrastructure which other PMs can utilise. They are competing on infrastructure now. In their new resolution engine, participants commit their own capital in support of an outcome. Every time a dispute occurs, the commitments increase, making it progressively more expensive to sustain a dishonest position.

Gnosis, another early participant in this category, developed the Conditional Token Framework in 2017, which allowed anyone to curate markets and turn event outcomes into tradable tokens. Polymarket later adopted this framework. Gnosis closed its product due to issues similar to those Augur faced, including high Ethereum gas fees, scalability issues, and a lack of user-friendly tools.

Using the same framework developed by Gnosis, Omen launched in 2020, offering permissionless market creation with an Automated Market Maker (AMM). However, one of the challenges it faced was liquidity fragmentation: anyone could curate a market on any niche, producing hundreds of near-identical markets for the same event, most of them totally illiquid.

Apart from this, they also faced Oracle-related problems. Omen used Kleros for resolution, an external, decentralised oracle infrastructure. Kleros crowdsourced jurors were incentivised to vote with the majority, and the majority consensus did not necessarily reflect the truth or market outcomes. Apart from this, the resolution process was also very slow and high gas fees were common.

The problems so far have been a combination of technical and liquidity problems, but the platform’s economics and design also play a huge role.

In early 2018, Stox launched a permissioned prediction market for sports, finance, and news and raised $33 million in its ICO. The core failure of Stox was the lack of a revenue model and tokenomics alignment. While the platform collected fees, they were insufficient to sustain market-maker incentives. Moreover, holders of STX, the platform’s native token, were supposed to benefit from platform revenue through a fee split, but it was never mechanically enforced in a way that could attract more users and liquidity to the platform. In terms of technicalities, the Stox resolution oracle was centralised and company-dependent, raising concerns about centralisation.

Another permissionless platform, Hedgehog Markets, was built on Solana, allowing users to curate their own markets. They introduced “no-loss prediction markets” using principal-protected deposits. Users would stake either $100 or $1000 in USDC and get game tokens against their stake, which were used for actual predictions, and the yield from the pooled USDC was distributed to winners. While this model sounds unique, it reduced users’ earning potential from the market because only the yield was at stake. This created an asymmetry for users who were genuinely interested in participating in the market and were willing to risk their capital, as the yield was the maximum amount they could earn.

All these products highlighted problems in different areas, surfacing issues around liquidity, event curation, resolution, regulatory compliance, and more.

Discoverability Problem

Permissionless market creation allows users to produce any number of markets, which can lead to multiple identical markets, resulting in hundreds of low-liquidity, oddly worded, partially redundant markets for every major event.

This redundancy creates a bad UX and confuses most users. Sophisticated users may allocate funds to the market with the most liquidity, but this gap can only be fully addressed either by not creating similar markets or by building a frontend that effectively excludes low-liquidity markets and makes them available only via search.

Resolution Dispute

“A prediction market is only as good as its ability to determine truth.”

Augur REP staking-based oracle and Kleros (Omen) incentivised stakers to vote in line with the majority. Similarly, in UMA, the optimistic oracle (used by Polymarket) faces the same resolution issues as in any market dispute: UMA token holders vote to make a final decision, and these same voters can trade on Polymarket, creating a bias towards a decision in favour of their position.

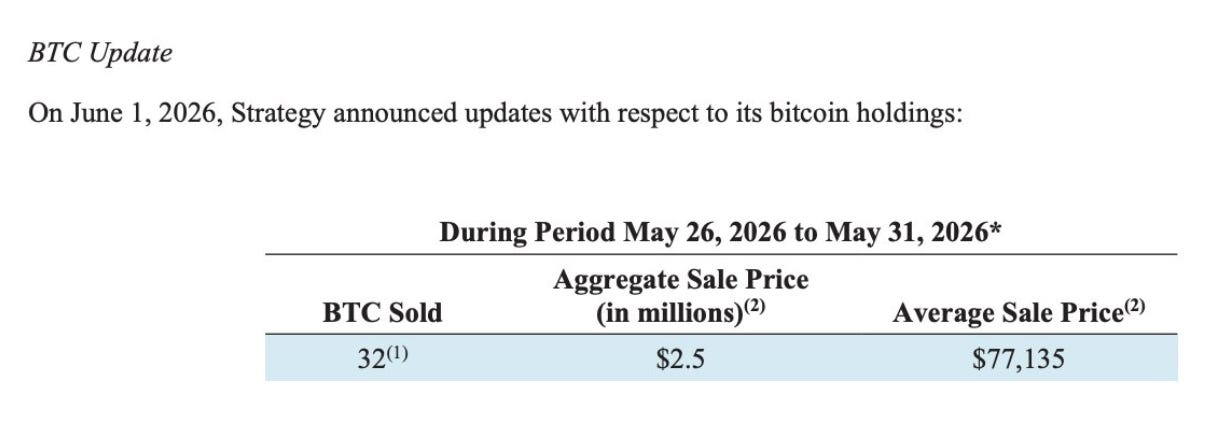

In Polymarket, for example, the dispute resolution is currently dominated by 9 whale addresses whose decisions have consistently aligned with the winning outcomes. These addresses can easily manipulate a market in the direction of their own trade.

One recent example of such a case is the MicroStrategy BTC sale market. The market should have been resolved to “Yes”, given that Strategy sold 32 BTC during May 26th to May 31st in the market, but it resolved to “No” even after being disputed 2 times.

Liquidity Fragmentation

A permissionless curation model creates liquidity fragmentation as users curate across multiple competing markets on the same topic, dividing liquidity among them. For Omen, the biggest challenge was liquidity fragmentation, as users curated near-identical markets.

This can only be solved by having a stricter curation process, for example, allowing only 1 market for each event, or it can also be handled through the frontend, where the UI shows a topic and all the different markets in the same place, and the user can choose which one to trade in while it recommends the one with the most liquidity.

Manipulation Surface

PMs are inherently manipulable either with economics or information.

A user could dramatically move a market’s price by buying a large position, gaining significant voting power on the Oracle, and steering the decision in their favour.

This problem is replicable in both permissioned and permissionless models, but the attack surface expands far more quickly in the latter as users continue to create markets.

Recently, a Google employee was caught by the SEC for trading in Google search-related markets on Polymarket. He utilised information arbitrage since he already knew the correct resolution, making millions in the process.

Regulatory Issues

CFTC treats event contracts as futures contracts that require registration with a designated contract market (DCM) under the Commodity Exchange Act.

Many older PMs weren’t compliant, which was a major problem for scaling.

For non-compliance, Polymarket was fined $1.4 million in 2022. The U.S. is a huge market due to active sports betting and trading happening. This is why Kalshi always took a regulatory-first approach, and Polymarket followed by acquiring QCEX in 2025 to become U.S.-regulated.

No Curator Economics

Earlier iterations of permissionless market curation didn’t focus much on the economics of market curation or on how curators could benefit from building the market. This created an asymmetry between the platform and the market curators, as they had less motivation and no financial benefit if the market grew in popularity and liquidity.

But some of these were problems that newer platforms, now incumbents, understood and pivoted to by adopting a permissioned curation approach.

Permissioned Curation: Polymarket and Kalshi Approach

Polymarket launched in 2020, while Kalshi launched in 2021. Both platforms have taken different approaches, but recently they have begun to converge on regulatory compliance and on winning the U.S. market.

Kalshi and Polymarket have become strong competitors over time.

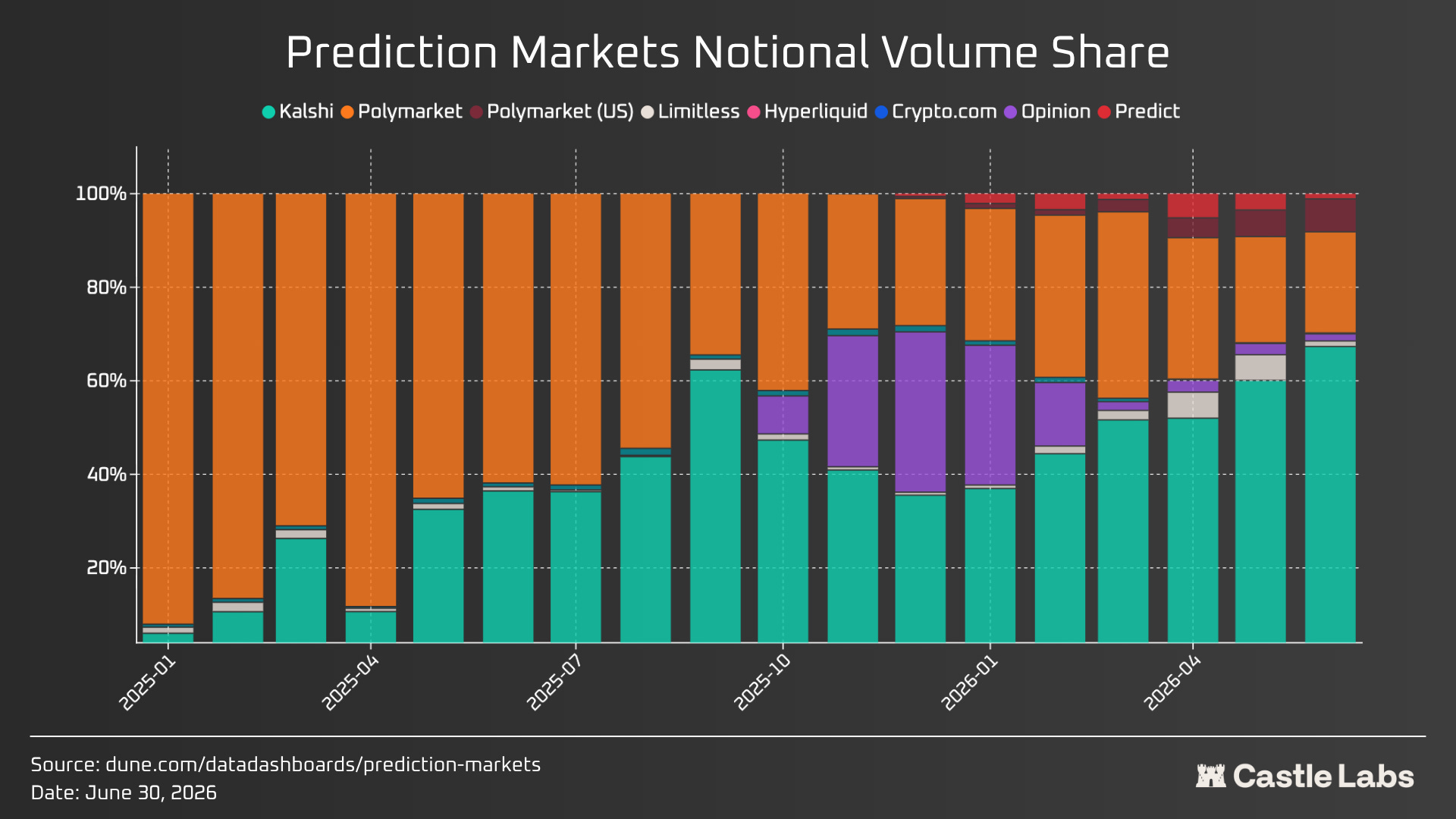

Until mid 2025, Polymarket maintained an 80% market share. Then, Kalshi established its own dominance through partnerships with platforms like Robinhood and now accounts for the majority of the volume PMs handle.

In terms of fees, Kalshi is currently generating annualised fees of ~$2 billion, compared to Polymarket’s ~$300 million. Additionally, in recent rounds, Kalshi and Polymarket were valued at $22 billion (Kalshi is currently targeting a $40 billion valuation) and $15 billion, respectively, making Polymarket overvalued relative to its competitor, as measured by their P/S ratios.

To scale to this level, both Kalshi and Polymarket solved most of the issues we highlighted above for early prediction markets.

Starting with regulatory compliance, Kalshi’s regulatory-first approach has been fruitful and has helped it grow in the U.S. Polymarket is also following up with Polymarket U.S., which is undergoing a phased rollout.

In terms of market curation, both platforms have active market curation teams and are permissioned, helping prevent problems such as liquidity fragmentation and duplicate markets.

While the permissioned nature of these platforms has been a successful approach so far, it doesn’t mean a permissionless model cannot co-exist in this category, as it is still required by many users to have control of the market, creating niche markets about the topic they are interested in, share curator revenues, and participate in building liquidity.

The permissionless model and early iterations of PMs surfaced multiple problems that incumbents addressed.

Even as incumbents have existed for some time and scaled sufficiently, users still cannot create and trade in the market of their choice, which is the ultimate goal for a Prediction market to become a source of truth for any and every topic backed by a financial stake.

Given that, as the solution space grows, permissionless curation is witnessing a great revival.

In the following section, we discuss how permissionless market creation is emerging as a category and how user-generated markets (UGMs) could scale.

The Permissionless Turn: New-Gen PMs

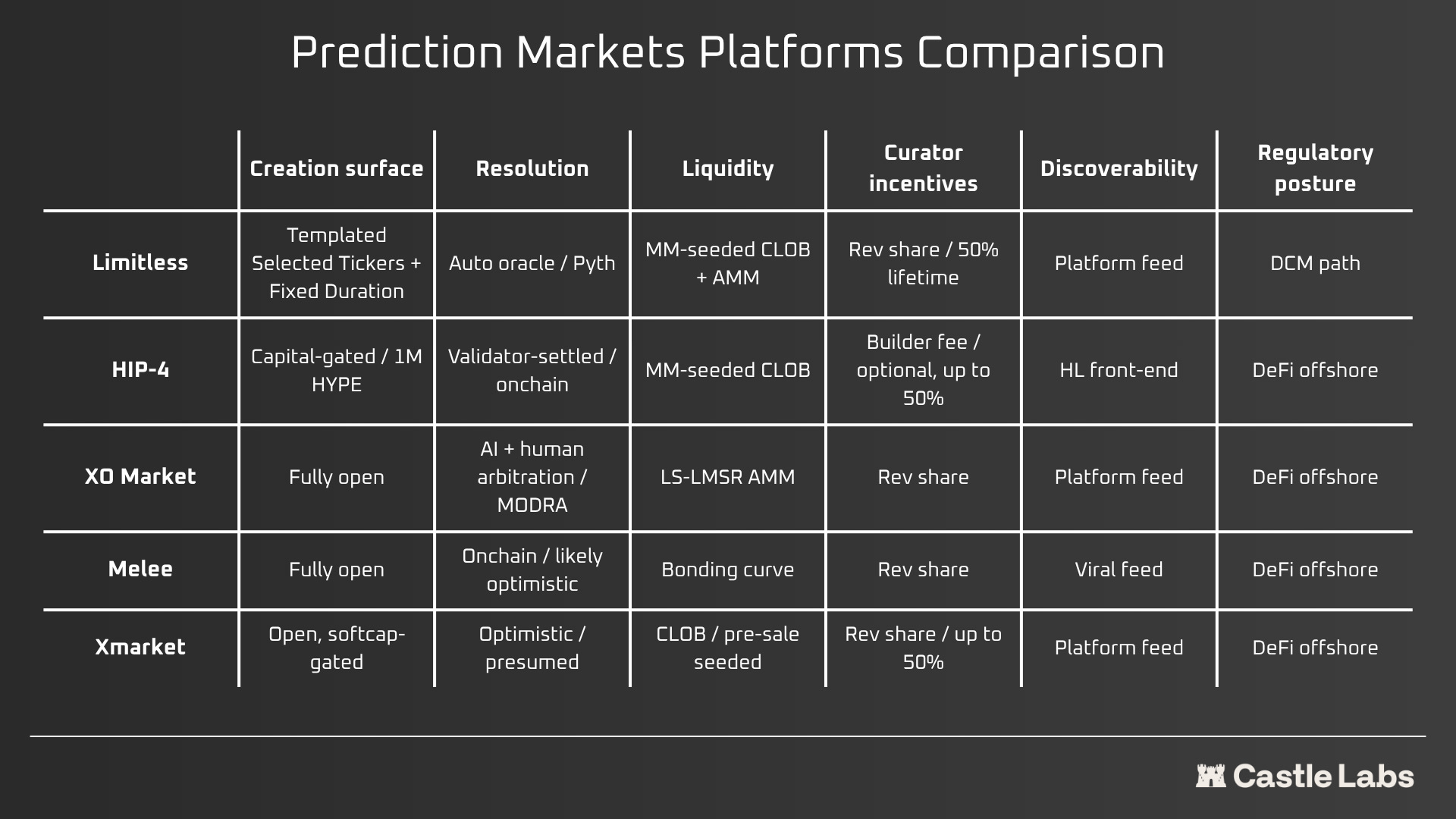

The permissionless curation sector has grown over the last year, with new players entering the market (Melee, HIP-4, XO Market, and more), and older products like Limitless also entering the category as they expand to provide UGMs.

Limitless recently went live with permissionless markets. They haven’t fully opened permissionless curation yet, but are initially allowing only crypto-related markets and will gradually expand into other categories to better understand demand and scale accordingly.

Additionally, Curators on the platform receive 50% of the revenue from the markets they curate, creating direct alignment between the platform and the market curators.

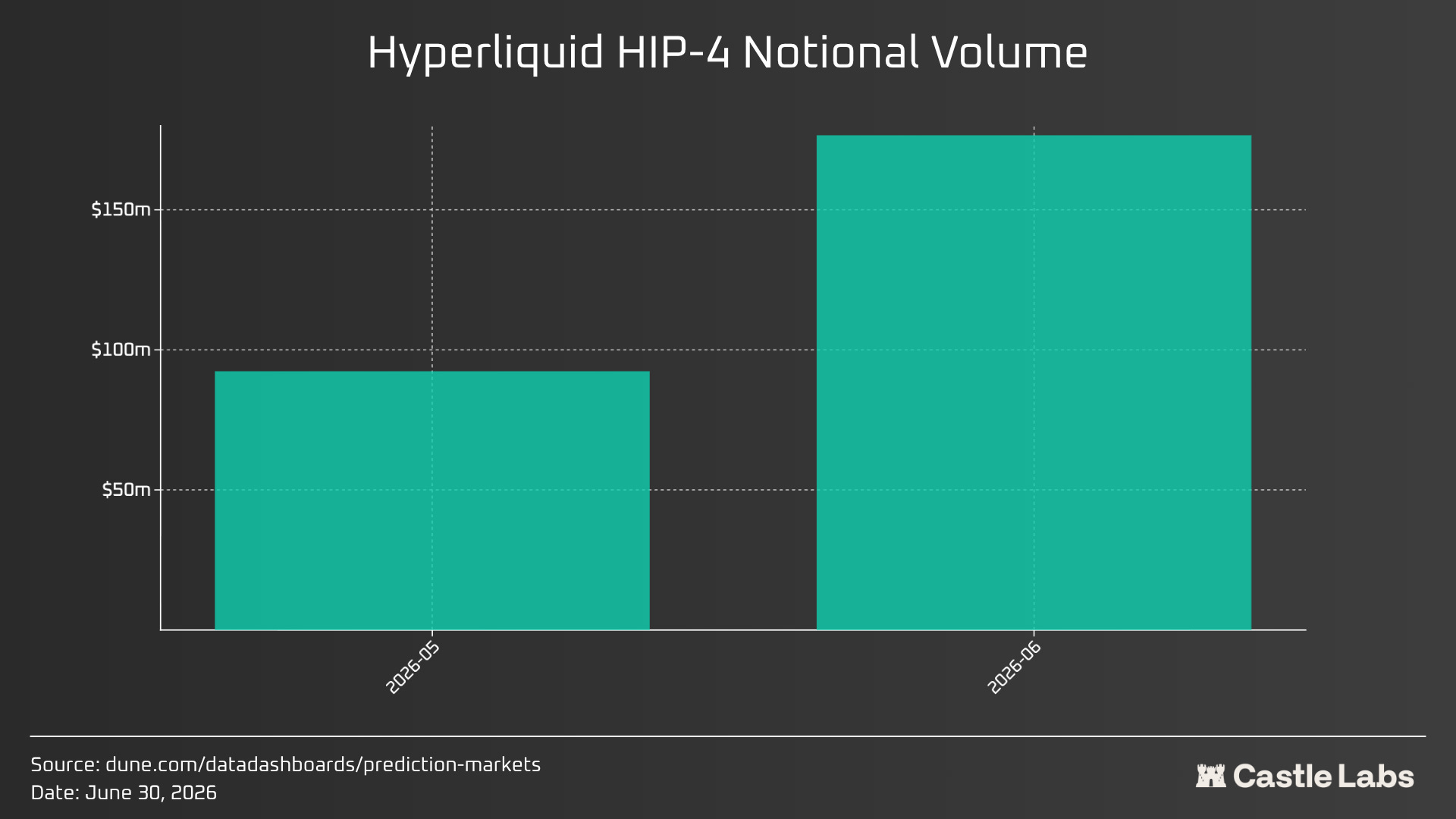

HIP-4, Hyperliquid Bounded Markets are capital-gated and require market deployers to stake 1 million HYPE to access a deployment slot. Builders can set an optional fee share of up to 50% on top of Hyperliquid’s base fees (fees are currently zero to incentivise trading in this initial phase, as they launched in early May). This approach helps Hyperliquid completely remove spam markets, as the threshold for deploying outcome markets is very high.

An additional structural advantage HIP-4 markets have is that they run natively on Hypercore, sharing the same orderbook, account structure, and margin engine as Hyperliquid’s spot and perpetual markets, meaning traders can access prediction markets and hedge their portfolios without fragmenting capital across separate accounts.

Both of these platforms support orderbooks, and liquidity is seeded by market makers (MM).

Other platforms target liquidity differently.

XO Market uses a Liquidity-Sensitive Logarithmic Market Scoring Rule (LS-LMSR) AMM model, an evolution of the standard LMSR used in most prediction markets.

The key difference lies in how liquidity is managed: in standard LMSR, the market curator must set a fixed liquidity parameter upfront, effectively estimating how much trading activity the market will attract. Setting this parameter too low makes prices overly sensitive to trades, while setting it too high requires excessive capital commitment. LS-LMSR removes this burden by making the liquidity parameter dynamic, allowing market depth to adjust automatically as trading activity accumulates.

It also requires users to bootstrap initial liquidity when creating the market, which helps deter spam and reduce illiquidity, thereby earning it the label “conviction market,” as users must provide liquidity.

On resolution, XO takes a unique approach by utilising a three-layer system. The first is the AI-first path through MODRA (Market Outcome and Dispute Resolution Agent), which uses AI to autonomously resolve clear-cut cases quickly. After that comes the Senate court and a Supreme Court appeal, which require human review. It has traded over $250 million so far, enabling 2800+ markets and 30,000+ trades.

Melee, another PM on the list, is expanding the parimutuel market model, which they call “PMM.” In a traditional parimutuel market, all wagers are pooled, and payouts are determined by the total amount wagered and the number of winning participants. While no traders can enter or exit after a certain period, for example, it is used in horse racing; bettors cannot exit when the live match starts.

Parimutuel markets create a set of problems, such as the need for constant liquidity, because users can exit only after the market is resolved. Being unable to exit mid-market pushes traders away due to a lack of flexibility. Additionally, to exit, traders might need to buy tokens in the opposite direction while the market is open, and the market’s value can change at any time, given the PM’s nature. Moreover, in this design, markets need to close before the event begins, as during the match, market participants might buy only the winning side, thereby gaming the market’s mechanics.

Melee is actively working to adopt the parimutuel model by eliminating the caveats by enabling continuous trading, but hasn’t launched publicly yet.

Products like Xmarket handle the initial market liquidity differently from others.

Markets can be curated with a minimum seed of $1, but they go live only after reaching a $100 soft cap in the initial liquidity. If any market fails to do so, every participant gets a refund. This essentially removes basic spam, filters for attention and determines whether users are interested in the market. However, this threshold is easy to game as it is pretty low: market curators can push for a softcap to make the market live, but it still helps initiate initial liquidity and activity.

In the graphic below, we make the distinction between these products more concrete by comparing them based on the problems the first generation of PMs encountered. There are multiple approaches to solving the key problems of curation, resolution, liquidity, economics, and regulatory path, showing a willingness to experiment in the category.

UGMs have faced a ton of challenges in the past, and there is no concrete evidence of which approach works best, as no UGM has achieved significant scale so far.

In the next section, we focus in detail on one of the recent products, Limitless, highlighting its approach to UGMs and to the problems highlighted in the initial section.

Financial Prediction Markets: How Limitless UGM Works?

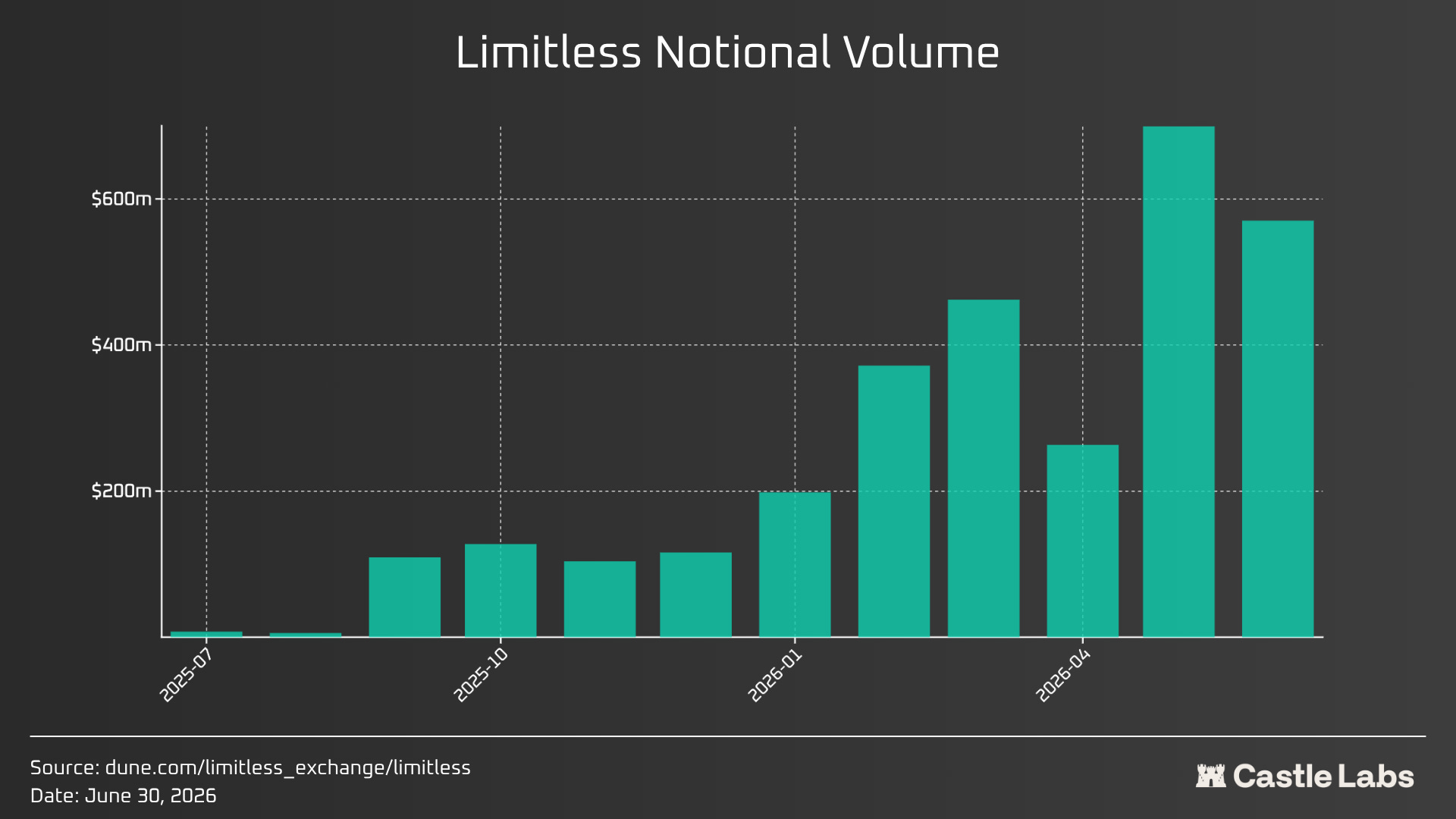

Limitless has been in the PM space since 2024 and has been growing gradually. This growth can also be attributed to the use of their token as a distribution tool for user incentives.

Limitless platform follows a permissioned curation process, and markets are designed internally by the team. The resolution process is also structured, with Pyth and Chainlink serving as oracles for financial markets like crypto, stocks, commodities/FX, and manual resolution for Sports, Politics, and other categories handled by the Limitless team. If the market is unable to resolve, users are refunded.

Given their already built infrastructure, they are expanding their offerings towards permissionless curation.

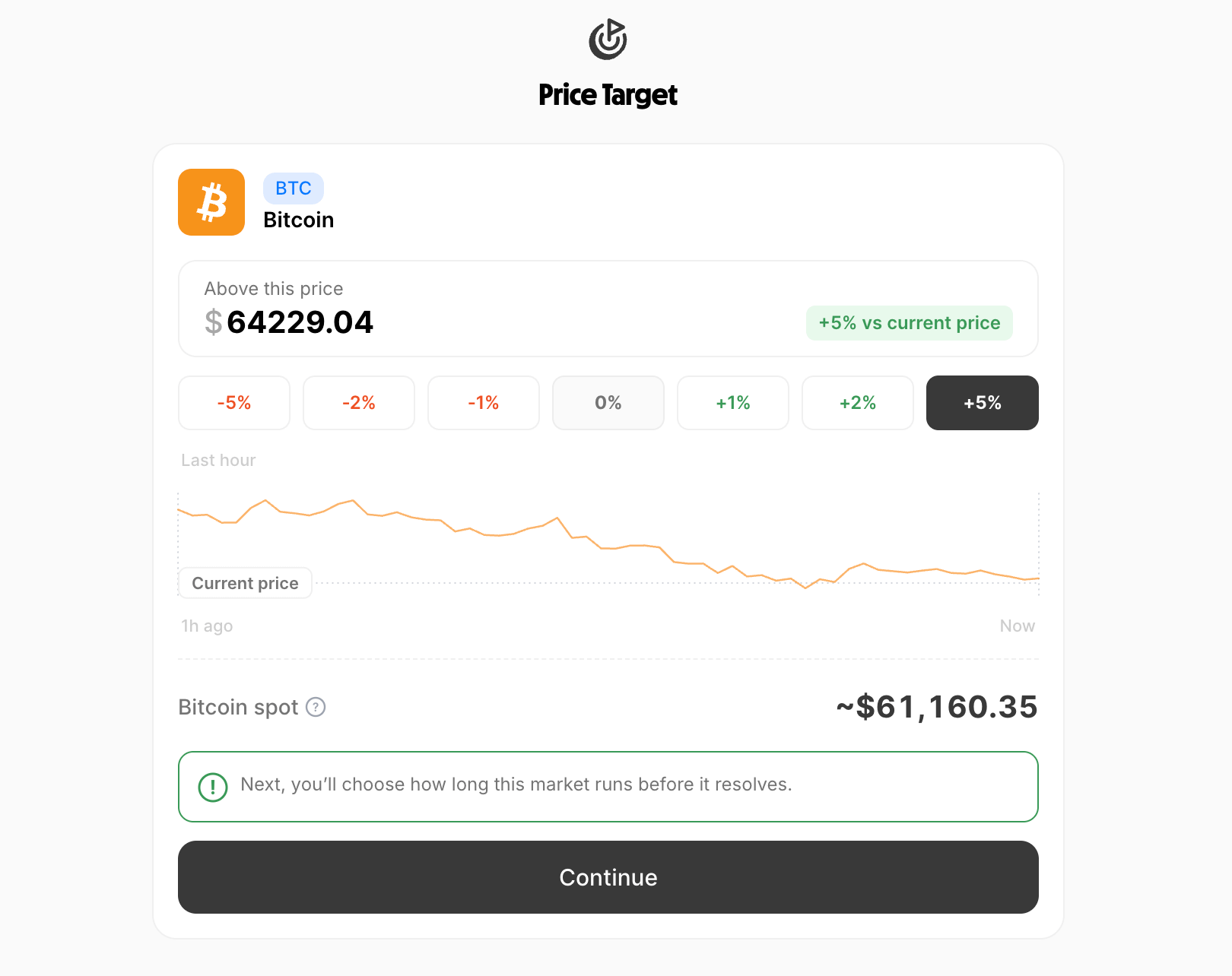

On June 2, 2026, Limitless launched its first permissionless market type. To scale this, they are deliberately taking a templated, finance-scoped approach rather than opening curation for any topic. In this initial phase, creators can choose from a fixed set of crypto assets (BTC, ETH, SOL, XRP, and DOGE), set a bounded price target (between -5% and +5%), and pick a duration from 15 minutes to 1 day. The goal behind the templated approach is to leave no room for ambiguous or oddly worded markets.

In the initial first month of rollout, these markets have generated $2.2 million in volume.

UGMs run alongside the platforms’ internally curated markets, making Limitless a hybrid platform. Additionally, this initial phase is crypto-only, with other categories added in the future as the team validates demand and maintains platform standards.

As these markets scale, UGMs can evolve into custom hedge instruments, allowing users to curate their own markets based on their perp/spot positions. The use case expands further as additional asset classes and PM categories, such as sports and esports, are added to the platform.

Limitless adopts a unique approach to address the distinct problems early PM implementations faced.

Creation Surface: Limitless approach starts with a limited scale and focuses on fewer financial markets, starting with crypto (BTC, ETH, SOL, XRP, and DOGE). Users choose the price and market duration in a templated configuration, leaving less room for oddly worded markets that might cause problems during resolution.

Resolution: Since they are starting with crypto-related markets, the oracles used are the same as their permissioned offering. They utilise providers such as Chainlink and Pyth to maintain consistent price feeds on their platform. Having an automated oracle removes the need for constant monitoring, allowing markets to be created and closed more fluidly.

Liquidity: Limitless bootstraps the initial liquidity. UGMs are created in CLOB to facilitate an open infrastructure, allowing any market maker to enter and provide liquidity, thereby enabling efficient price discovery.

Curator Incentives: One of the major things that matters for a UGM to succeed is curator economics and how curators make money in the whole process, because without a substantial revenue exposure, they won’t treat the curation process within parameters and create a lot of ambiguity, which isn’t good for market discoverability and attracting volume. This symmetry between the platform and curators is essential to keep the interests aligned. On Limitless, curators pay fees between 100 and 1,000 LMTS (depending on market duration; the longer the duration, the higher the fees) to create the market and receive a 50% fee share from the market they curate. Additionally the team is exploring different pricing models based on user feedback.

Discoverability: Since markets are price-only for a few assets, the possible market surface is bounded in terms of asset, duration, and price target, limiting market fragmentation and the creation of near-duplicate markets.

Regulatory Compliance: At the beginning of May, Limitless applied for CFTC approval to operate as a federally regulated derivatives exchange in the U.S. (an application the CFTC has since deemed materially complete, moving it into formal review). Once approved, this will provide a clear regulatory path for Limitless to scale in the U.S. as a prediction market and to actively compete with Kalshi and Polymarket U.S., and crypto.com derivatives.

The Limitless approach provides a good set of solutions to the different problems that surfaced in earlier PM iterations. Their templated configuration maintains platform integrity and mitigates issues related to ambiguous markets. While they charge fees to create markets, this effectively removes the problem of spam, as requiring a threshold to create the market would make it expensive for someone trying to push for spam. The 50% fee share gives creators a real incentive to participate and attract activity. Additionally, Limitless, pending CFTC approval, offers a clear regulatory path that sets it apart from its peers.

But the fees the platform charges also create the “chicken-and-egg problem”: it expects users to pay fees to create these markets, so users have to balance their investment against the potential return from the 50% market-fee share. The latter can only be increased with enough activity, while the former stays stagnant.

In the current limitless model, the fees users initially pay are static and accounted for in their native token, LMTS. While this is good for avoiding spam, the platform could consider adding dynamic fees based on curation demand, so that when demand for certain markets or assets is lower, fees are lower, and vice versa when demand is higher.

What Comes Next?

PMs started early, with initial iterations such as Augur and Gnosis launching during the crypto ICO era. These products faced very similar issues, mostly surrounding fragmented liquidity, slow or disputed resolution, weak curator economics, and regulatory exposure.

The new wave of products in the permissionless curation space recognises these gaps and adopts distinct designs to address the problems PMs face today.

XO market enables creators to bootstrap initial liquidity and adds a tiered resolution model to achieve the most accurate conclusion. Melee reworks the parimutuel model for continuous trading. Xmarket tries to filter spam with a soft-cap funding threshold. HIP-4 gates creation behind a large stake to only allow quality markets. Limitless introduces a 50% fee share and a curation fee to enhance curator economics and prevent spam.

But what separates them isn’t the solutions they provide, but the completeness of them in different directions. A product that solves liquidity but not resolution, or solves resolution but not creator economics, won’t be good enough to scale.

Given that, permissionless markets are being revisited and are worth keeping an eye on.

Over time, it will be discovered which design choices scale best and become the most optimised venues for opening a market in any given niche, and finding the truth, PMs are made to source architecturally.

written by Noveleader ✍️

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram person, you can read all of our research without the noise on our TG channel:

Disclaimer: This article was produced in collaboration with Limitless. Castle Labs applies the same standard to sponsored content as in our independent research. We strive to be accurate, unbiased and educational. Commissioned partnerships provide resourcing and distribution, not editorial control.