Prediction Markets Have Never Been This Strong

This report is an excerpt from the EOY Report we published together with OAK Research and Hazeflow in collaboration with Kraken.

Prediction Markets (PMs) really received their due in 2025, validating the thesis that skin in the game creates better data than polls. Following the 2024 Presidential Elections, where they consistently led broadcast polls in accuracy, the sector transitioned from a gambling novelty to a recognised source of alternative financial data.

Financial dashboards (Google Finance and Yahoo Finance) have integrated these markets because they have become reliable indicators of global sentiment. Since users express their opinions by putting their money where their mouth is, it makes more sense to trust them than traditional polling institutions.

There is still ongoing debate over whether prediction markets should be classified as gambling. In practice, the distinction matters less than it seems. As a user, if you are trying to make money on a sports outcome or the result of the next election, you are betting on a future event that has not yet happened, and you are, de facto, gambling. However, what ultimately matters is your opinion on the probability that the event will occur, because it directly contributes to understanding broader market sentiment.

Whether prediction markets are gambling or not, they fit into a broader trend: speculation has always been the primary driver of crypto adoption, and prediction markets are no exception. What sets them apart, however, is that they are broadly accessible, unlike many other onchain finance use cases.

Everyone has, at some point, enjoyed predicting how an event will play out and, more broadly, everyone holds at least one opinion. That is precisely what explains their rapid adoption, especially beyond the crypto-native ecosystem. As a result, prediction markets appear less like an exceptional innovation and more like a natural evolution of onchain speculation. In 2025, they emerged as a new territory at the intersection of information, investment, and speculation.

State of Prediction Markets 2025

A Rapidly Expanding Sector

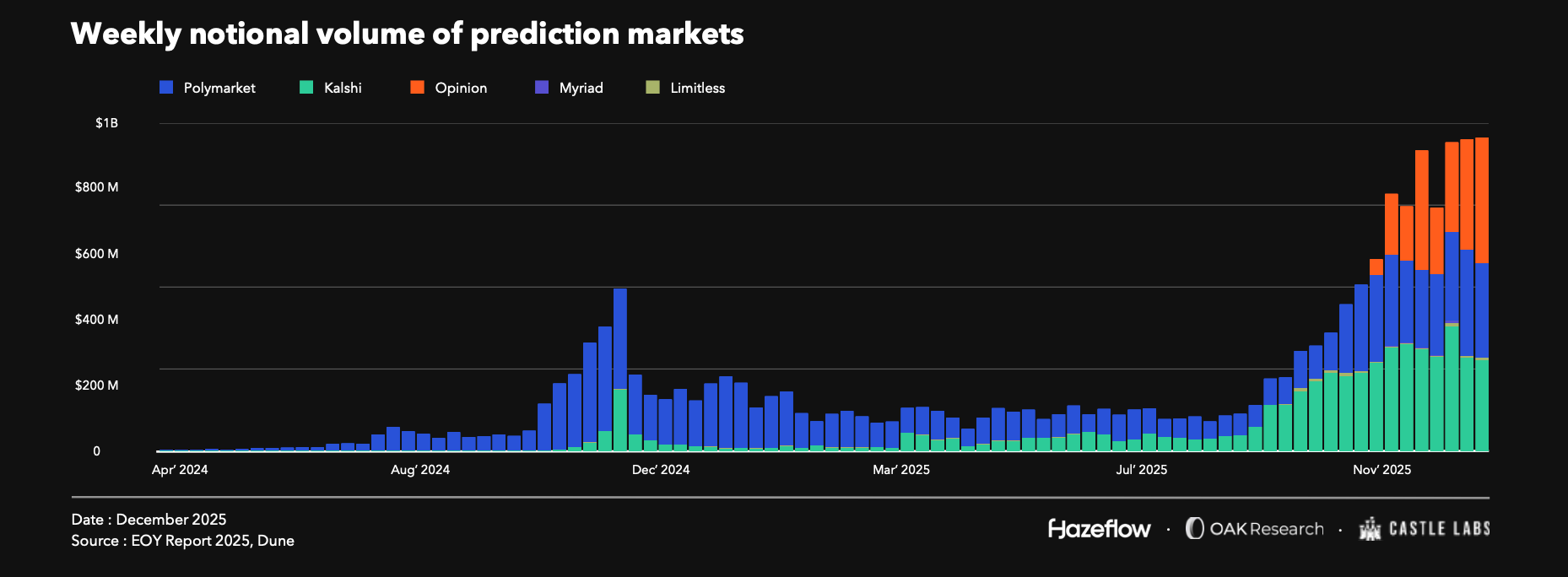

After the exceptional peak observed during the 2024 U.S. presidential election, prediction market activity slowed sharply at the start of 2025. Volumes then stabilised for several months around $500 million per week, before accelerating meaningfully again from late summer onward.

The sector experienced explosive growth in Q4 2025, with monthly volumes approaching $10 billion across platforms, far surpassing 2024 highs. In December, weekly volumes reached $3.8 billion, representing a roughly 660% increase from the beginning of the year.

Transaction counts followed the same trajectory, rising from roughly 1.2 million per week early in the year to more than 12.7 million in December. The relative growth in transactions (10.5x) compared to volumes (7.6x) suggests reasonably organic activity. In other words, airdrop farming remains moderate or at least comparable to real usage.

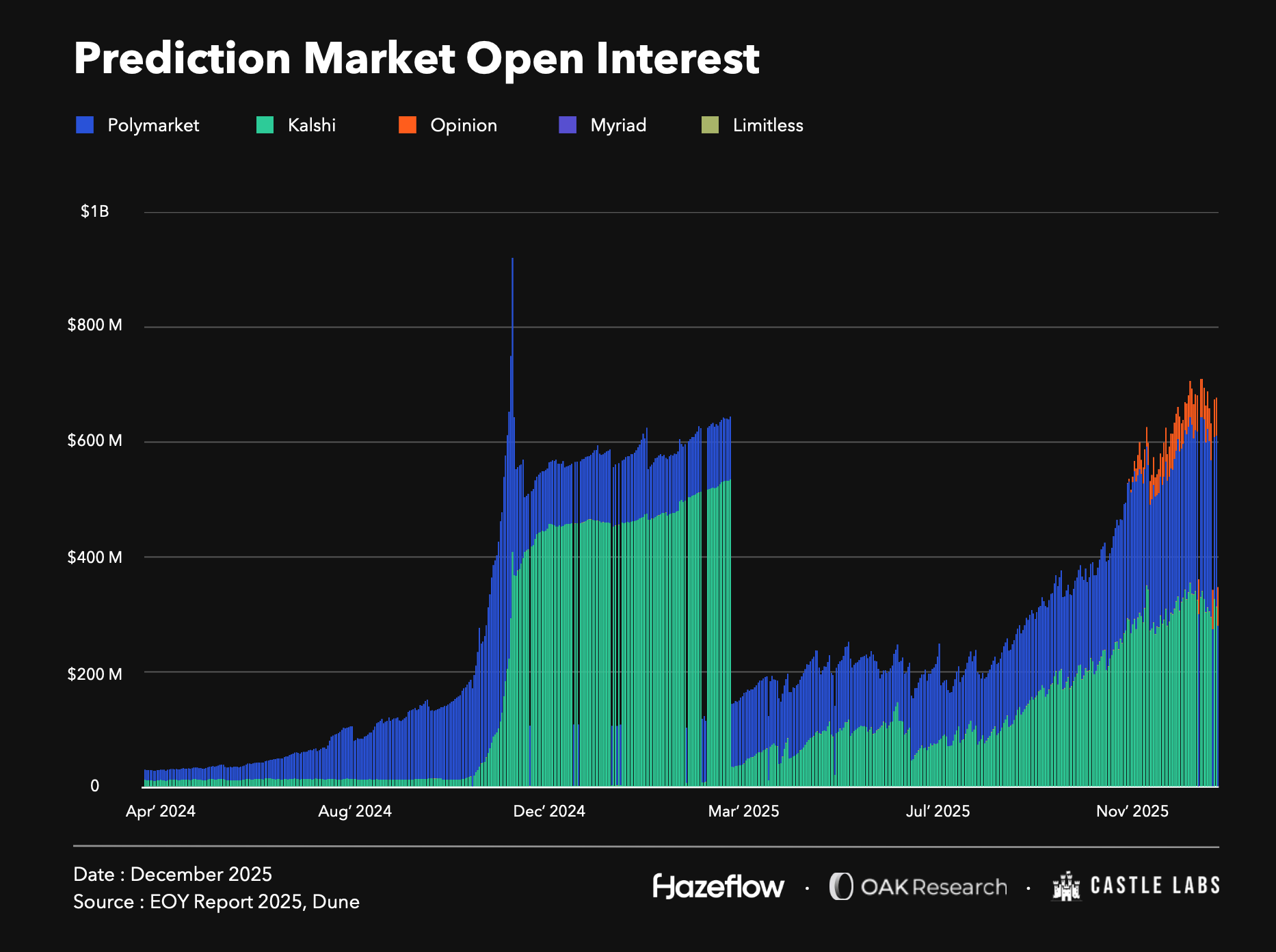

Another key metric to monitor is Open Interest. It rose relatively linearly throughout 2025 and ultimately surpassed $700 million by year-end. This remains below the 2024 election peak, when open interest reached nearly $900 million sector-wide, underscoring the unique nature of that event, characterised by unusually deep liquidity and participation from professional actors or large portfolios.

Several factors help explain the explosive growth of prediction markets in 2025. Chief among them was the direct competition between Kalshi and Polymarket. On October 7, Polymarket announced a $2 billion investment from ICE, the parent company of the NYSE, valuing the platform at around $9 billion. On October 10, Kalshi responded with a $300 million round, before announcing a $1 billion Series E on December 2, bringing its valuation to $11 billion.

Another driver was the partnership between Robinhood and Kalshi, which enables retail users to access Kalshi markets directly from their Robinhood accounts. For Polymarket, airdrop farming also pushes their metrics, as the platform has shown signs of the $POLY token launch, and the airdrop seems to be based on volume creation.

While the 2024 U.S. presidential market remains the largest single event ever recorded with $3.6 billion in volume on Polymarket and $2.4 billion on Kalshi, certain NFL weekends in 2025 have already posted daily volumes above $275 million on Kalshi. This shift highlights the sector’s growing reliance on recurring markets, particularly sports.

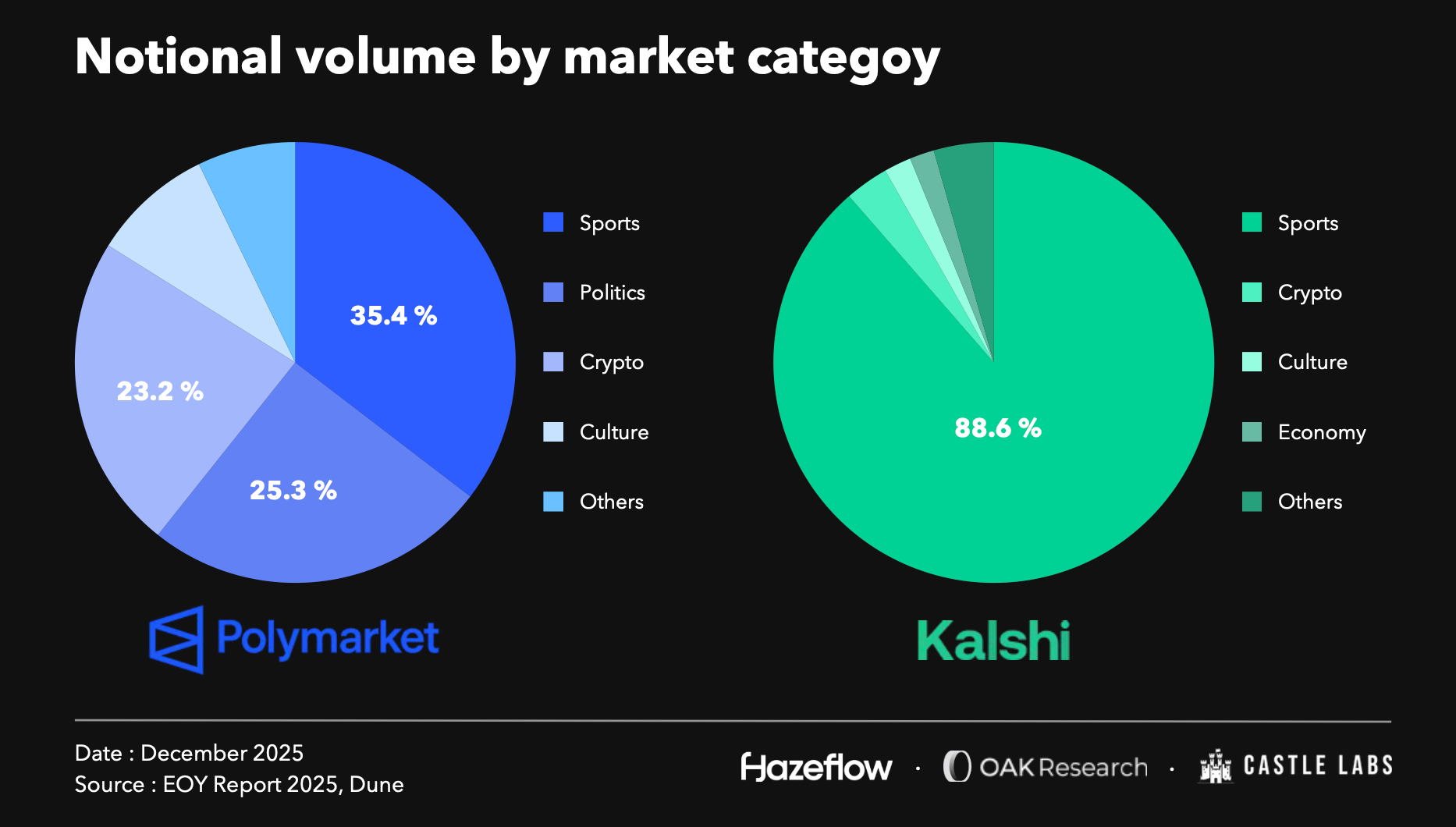

Beyond aggregate volumes, activity composition differs sharply between the two platforms. Kalshi has found a clear product-market fit in sports betting, which accounts for up to 98% of its weekly volume. Polymarket, by contrast, has remained far more diversified and general-purpose, with a more balanced split across sports (37%), politics (26%), crypto (25%), and culture or societal events (9%).

A Polymarket-Kalshi Duopoly?

Over the past three months, prediction markets have been the segment that raised the most capital across the broader industry, thanks in particular to Polymarket and Kalshi. In practice, the two platforms form a duopoly that captures most of the sector’s volume and open interest, forcing other players to offer heavy incentives to compete.

In November, Polymarket processed more than $4 billion in notional volume, its best month to date, while Kalshi posted roughly $5.2 billion, becoming the first regulated U.S. platform to cross that monthly threshold.

Their dominance is undeniable: they hold 44% and 47% of total open interest, respectively. The distribution of notional volume, however, is more mixed. By year-end, Kalshi represented about 22% of traded volume, Polymarket 33%, while Opinion captured nearly 43% of activity.

Opinion launched in late October 2025 and is backed by YZi Labs, Changpeng Zhao’s investment fund. Its volumes surpassed Polymarket’s within a matter of days. In line with what we previously observed with Aster (YZi Labs’ trading platform launched to compete with Hyperliquid), it is not unlikely that Opinion’s volume is at least partly inflated, beyond the ongoing airdrop campaign itself.

Which Prediction Market Will Win?

Polymarket

Polymarket established itself in 2025 as the undisputed leader among decentralised prediction markets, with cumulative volume exceeding $13 billion. Monthly volume reached around $4 billion in November, indicating that activity is no longer driven exclusively by major political events.

Strategically, Polymarket strengthened its position through the $112 million acquisition of QCEX and by obtaining a CFTC-validated framework that enables a limited return to the U.S. market. This allows the platform to move toward regulatory compliance without undermining its onchain infrastructure status.

But the most significant event of 2025 remains ICE’s $2 billion investment in Polymarket (ICE, the parent company of the New York Stock Exchange), at an estimated valuation of $8-$9 billion. Beyond capital, the deal primarily aims to enable broader distribution and integration of Polymarket data into traditional financial infrastructure, particularly for forecasting, risk management, and market intelligence use cases.

Kalshi

Kalshi overwhelmingly dominated the centralised and regulated segment of prediction markets in 2025. The platform recorded $5.2 billion in November volume and now exceeds $25 billion in cumulative annual volume. Its key competitive edge remains its unique status: Kalshi is the first CFTC-regulated prediction market platform, allowing it to acquire U.S. users at scale legally.

In December 2025, Kalshi raised $1 billion at an $11 billion valuation, doubling its valuation in less than two months after a prior $300 million round. The platform also set new records at the start of the 2025 NFL season, with daily volumes exceeding $260 million.

Kalshi also launched a tokenisation initiative to distribute certain markets onchain. Its “Builder Codes” program, reminiscent of Hyperliquid’s namesake mechanism, allows any application or front-end with an existing user base to offer prediction markets natively through Kalshi. For now, this remains marginal and raises regulatory questions around intermediaries that distribute these markets, but it is still an important acquisition strategy in its competition with Polymarket.

Emerging Players

Several newer platforms gained visibility at the end of 2025, largely driven by incentive programs and differentiated models.

Opinion emerged as the year’s outsider. Within two weeks of launch, the platform reached nearly $748 million in weekly volume and captured around 42.7% of onchain market share, third globally behind Polymarket and Kalshi. As with other heavily incentivised platforms, these figures should be interpreted cautiously, as activity is primarily tied to airdrop expectations.

Limitless raised a $10 million seed round in October 2025, led by 1confirmation and several major ecosystem players, ahead of the LMTS token launch. The platform now totals more than $515 million in cumulative volume, with activity that remains meaningful but still largely opportunistic.

Myriad Markets adopted a different approach, focused on distribution rather than maximising volumes. Its browser extension enables media outlets such as Decrypt to surface contextual prediction markets directly alongside their content. This white-label model separates infrastructure from user acquisition and prioritises integration rather than head-on competition with the most prominent venues.

Melee offers a pumpdotfun-inspired design based on bonding curves that dynamically adjust outcome prices. Early participants get lower prices, while later entrants pay increasingly more as collective conviction rises. The platform targets permissionless markets where users create their own Yes/No bets, rather than trading only on curated events.

XO Market: XO Market lets anyone create a market based on their conviction and opinion by setting up the market resolution path and seeding the initial liquidity. The platform has integrated AI to help market creators navigate the process smoothly and also set a creator fee for their market. The platform also made enhancements to liquidity sourcing, transitioning away from the traditional Logarithmic Market Scoring Rule (LMSR) and order book model. For outcome resolution, it utilises AI-powered resolution agents that autonomously handle a large number of markets, with an option for users to dispute the resolution.

Lightcone: Lightcone enable users to trade on the event’s impact. Let’s suppose you consider that a drug is going to be approved by the FDA, and now you can bet on how the S&P 500 is going to perform after that. This creates a new category of PMs, called the “Impact Markets,” in which participants are not interested in the outcome alone but in the impact it has on a specific asset.

Trendle: Trendle converted attention into an asset class by calculating an attention index from social and engagement data, enabling users to trade the attention of listed markets such as Bitcoin, Elon Musk, Donald Trump, and more. It also features trading with up to 5x leverage on these markets, which simply involves predicting whether attention on a specific individual or asset will increase or decrease.

What’s Next for Prediction Markets?

TGEs: The Variable That Can Change Everything

The battle between prediction markets will not be decided solely by current volumes, but by their ability to sustain activity over time and generate genuinely durable revenue streams for their tokens. In the crypto industry, the final verdict on a product’s success is often delivered through the performance of its token, and very few protocols have managed to succeed on that front over the long term. The airdrop leverage Polymarket holds relative to Kalshi could just as easily turn into a poisoned gift if the market rejects the token at launch.

As is often the case with emerging narratives, it only takes two factors to trigger a euphoric phase: an established leader capturing most of the attention, and the rapid emergence of credible competitors. This classic crypto pattern usually leads to the same outcome: accelerated activity, intensified innovation, and ultimately value redistribution in favour of users, primarily through incentives and airdrops.

The primary catalyst for 2026 will therefore be the launch of Polymarket’s POLY token. The airdrop is expected to coincide with the release of the U.S. application, making it a structurally important event for the entire sector. POLY’s market performance will largely shape the trajectory of prediction markets, especially if it manages to maintain a high market capitalisation in an environment that remains broadly unfavourable for altcoins.

In parallel, the TGEs of Limitless, Myriad, and Opinion are also expected in 2026, though their success remains uncertain. Current activity levels are still too low to support meaningful revenue generation and justify a durable valuation at token launch.

Sports as the Winning Category

Sports betting has been the major contributor to the PM’s volume. At the time of writing, Sports represent more than 40% of the volume on Polymarket, and on Kalshi, the share exceeds 90%. The reason to focus on Sports as a category is apparent because Sports betting is expected to grow at a CAGR of 10% over the next 4-5 years, reaching a market value of $198 billion by 2030, up from about $108 billion in 2024.

There are simply more users willing to participate in sports betting, thereby increasing the Total Addressable Market (TAM). Moreover, the growth rate of this sector also ensures that, if these platforms capture a decent market share, they can generate recurring revenue for their businesses as Sports events occur regularly.

Despite the volume, PMs still struggle to beat traditional sportsbooks (FanDuel/DraftKings) due to the Parlay problem, which helps users place leveraged bets. A simple 3-leg parlay can abstract away three bets into one, and if all these bets win, it increases the payout, but if one of the legs fails, the payout will be zero. This is risky, but it also adds the intended leverage to sports betting.

The difference between PMs and traditional sports orderbooks is that the latter manages risk centrally. At the same time, the former requires liquidity across every market to support such bets, making enabling parlays highly expensive and capital inefficient.

On Polymarket, Politics and Crypto rank second after Sports, accounting for the other 50% of the volume, and on Kalshi, these two categories account for 4-5% of the platform’s volume. Markets apart from these typically do not exhibit the same volumes and liquidity because fewer people are interested in trading in them, as they might lack the knowledge (or simply the interest) to trade in such niche markets. It is also essential to understand that the platforms are positioned to serve a niche category, as volume from other categories can be seasonal. On the other hand, it helps them reach new audiences.

The Integration Race

The next major challenge for prediction markets in 2026 will be distribution. To achieve that mainstream impact, PMs need the best integrations with industry leaders. Kalshi and Polymarket have recently been integrated into Google Finance, allowing users to access odds from both platforms. This integration will help Google answer users’ questions, such as “What will GDP growth be for 2025?” Additionally, Robinhood announced its Kalshi integration in August this year, which helps their users to access and trade on the outcomes of NFL and college football games. This partnership with Robinhood drives a significant share of the platform’s volume.

These integrations help PMs reach an audience that would otherwise be very hard to get, which is also their target market as they scale into the mainstream. Robinhood and Google Finance users are likely to be interested in them as a news source or for betting on these platforms. On top of this, two recent integrations have been between Polymarket and Yahoo Finance, and between Kalshi and CNBC, both for embedding market odds and showcasing sentiment.

Embedding is the core strategic challenge for prediction markets in 2026. These products monetise opinions that are formed outside trading platforms, across social networks, media outlets, and existing communities. By integrating markets directly where information is consumed, rather than forcing users to switch context or interface, one of the leading platforms could unlock exponential user growth.

Polymarket recently partnered with X, signalling that this type of integration is clearly part of its strategic thinking. Kalshi, meanwhile, is exploring a different route through its Builder Codes, which are tokenised versions of its markets deployed on Solana and distributed via third-party applications with their own user bases.

While technically different, sports and media partnerships also play a key role in normalising the product and increasing visibility. Polymarket signed an agreement with the UFC around co-branded markets and broadcast-related integrations, while Kalshi, through partnerships with CNN and CNBC, is positioning its economic and political markets as real-time tracking tools for a broad audience.

Oracle Manipulation

Oracles are the core part of PMs and the “source of truth” for resolving markets. Every platform has its own way of curating this source of truth, with platforms like Kalshi relying on human oversight and Polymarket relying on optimistic oracles, such as Uma. The Kalshi approach might make this part of their system a scalability bottleneck. However, it has worked fine until now. While the Polymarket approach has already revealed some of its weaknesses this year and in the past.

One advantage of the optimistic oracle approach on Polymarket is that users can simply disagree with the resolution during the 2-hour challenge period and propose an alternative resolution with a $750 bond. However, if their resolution is unsuccessful, they can lose this bond.

In some cases, these challenges may not fully meet user expectations. When the user disputes a resolution, the UMA protocol’s voters vote and reach consensus on whether the dispute is legitimate. This gives UMA voters or whales disproportionate power, allowing them to skew the market resolution in their favour.

A similar incident occurred during the Zelensky suit market on Polymarket, where the market ultimately resolved in favour of UMA whales, highlighting the weakness of such a system.

The Liquidity Problem

Another central challenge lies in liquidity. Unlike derivatives markets, prediction markets rely on expiring contracts and binary outcomes, which makes hedging strategies highly complex for professional market makers. Liquidity providers are therefore exposed to significant asymmetric risk and suffer from a form of structural impermanent loss.

These are some of the reasons why MMs might not want to be involved:

High Inventory Risk: PMs move significantly in response to certain news. A market which is going well in one direction can go in the opposite direction at a fast pace, and at that moment, MMs, if priced in the opposite direction, can lose big. It can be mitigated through hedging, but these instruments often do not offer such an option across all the markets supported by PMs.

Insufficient Traders and Liquidity: Markets lack sufficient liquidity. Now, it might sound like the “chicken and egg” problem, but the market needs frequent traders or takers who can keep making MMs money on bid-ask spreads. Currently, PMs feature several “long-tail” markets where there simply isn’t enough volume or trading activity, which doesn’t incentivise MMs to perform their operations.

As long as this problem remains unresolved, market depth will stay limited, preventing large-scale institutional participation and hindering any direct comparison with more mature derivatives infrastructures. Without deep liquidity, prices react poorly to new information, and the “wisdom of the crowd” that prediction markets theoretically promise remains only partially fulfilled.

Some products are actively working on solving this problem, like Kalshi, which utilises third-party MMs and also has an internal trading arm to maintain liquidity. On the other hand, Polymarket provide USDC rewards to compensate those who provide liquidity near the spread. For certain eligible events, the platform also pays holding rewards that accrue when providing liquidity in specific event markets at a 4% holding APY. Similarly, Kalshi reward its users on their cash and open position holdings with an interest rate of 3.5%. These rewards ensure that users are incentivised to participate in the market for the long term.

Several teams are also experimenting with new market designs to improve capital efficiency, event resolution, and market automation, including AI-assisted market-creation tools, automated resolution mechanisms for subjective events, and hybrid formats inspired by perpetual futures.

The Rise of AI

AI plays an increasingly important role in providing accurate information at the right time, helping traders make better decisions. For this, there are products built on top of Polymarket as part of their builder program, like Polyfactual, which provides deep AI research on any market and a live feed of the latest news on crypto, politics, and sports. Additionally, protocols like Polymtrade are building a trading terminal on top of Polymarket, powered by AI. Beyond using AI, this program includes other products that aim to add new value, such as tooling or improvements to the polymarket’s trading UX.

As PMs evolve, the share of automated trading is expected to increase, making a bag out of inefficiencies or mispricing across markets. Recently, these bots have started to grow, trying to capture equal shares of “Yes” and “No” in a particular market at a discounted or mispriced rate, combining them when the market resolves to get the full value of the share that won.

Prediction markets remain a relatively young concept and still face many structural challenges. Over time, however, solutions are likely to emerge. Major platforms such as Polymarket and Kalshi have already reached escape velocity, building audiences well beyond the crypto ecosystem, drawn primarily by the products themselves.