Prediction Markets: The Race to Predict Everything

Predicting the future everyday.

Introduction

As humans, we love gambling or anything that gives us that dopamine or adrenaline rush. That hit of winning or the edge of something that could change our lives is what most of us crave.

Prediction Markets (PMs) provide just that feeling: the thrill of taking a risk, and the satisfaction of being right when you successfully predict something, with making a profit being the cherry on top. Through their development, they expand what we can bet on to politics and other events previously marked as safe from gambling.

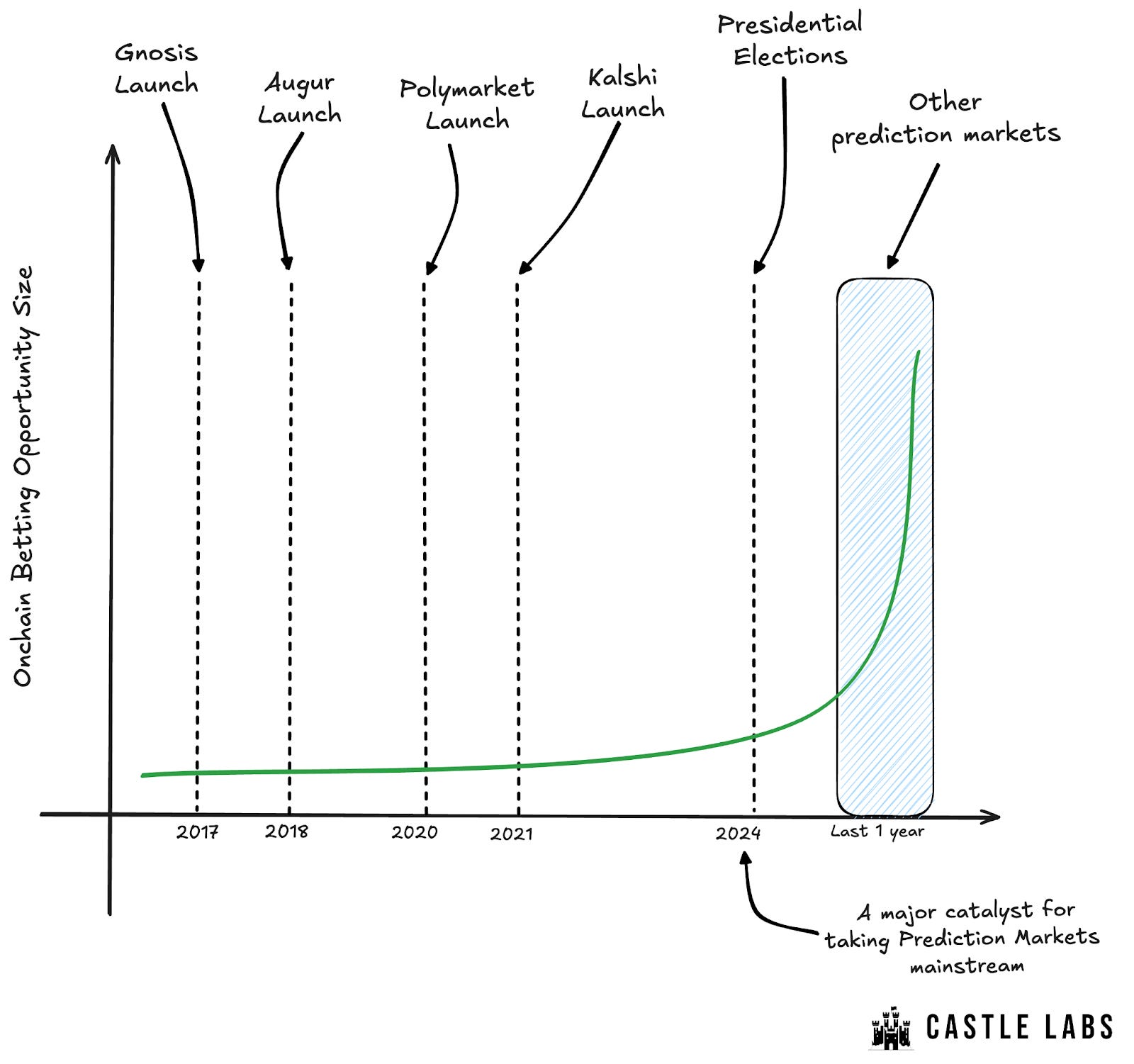

Nowadays, we have seen the emergence of platforms that let us predict almost everything, from mindshare and onchain metrics to real-world events like presidential elections. Polymarkets and Kalshi have achieved mainstream adoption, but none of this happened in a vacuum.

Decentralised or onchain PMs date back to 2017-2018, when Gnosis and Augur launched. Following that, Polymarket and Kalshi launched in 2020 and 2021, respectively, and now we are swimming in options for platforms that let you predict everything, from real-world events like presidential elections to mindshare and onchain metrics.

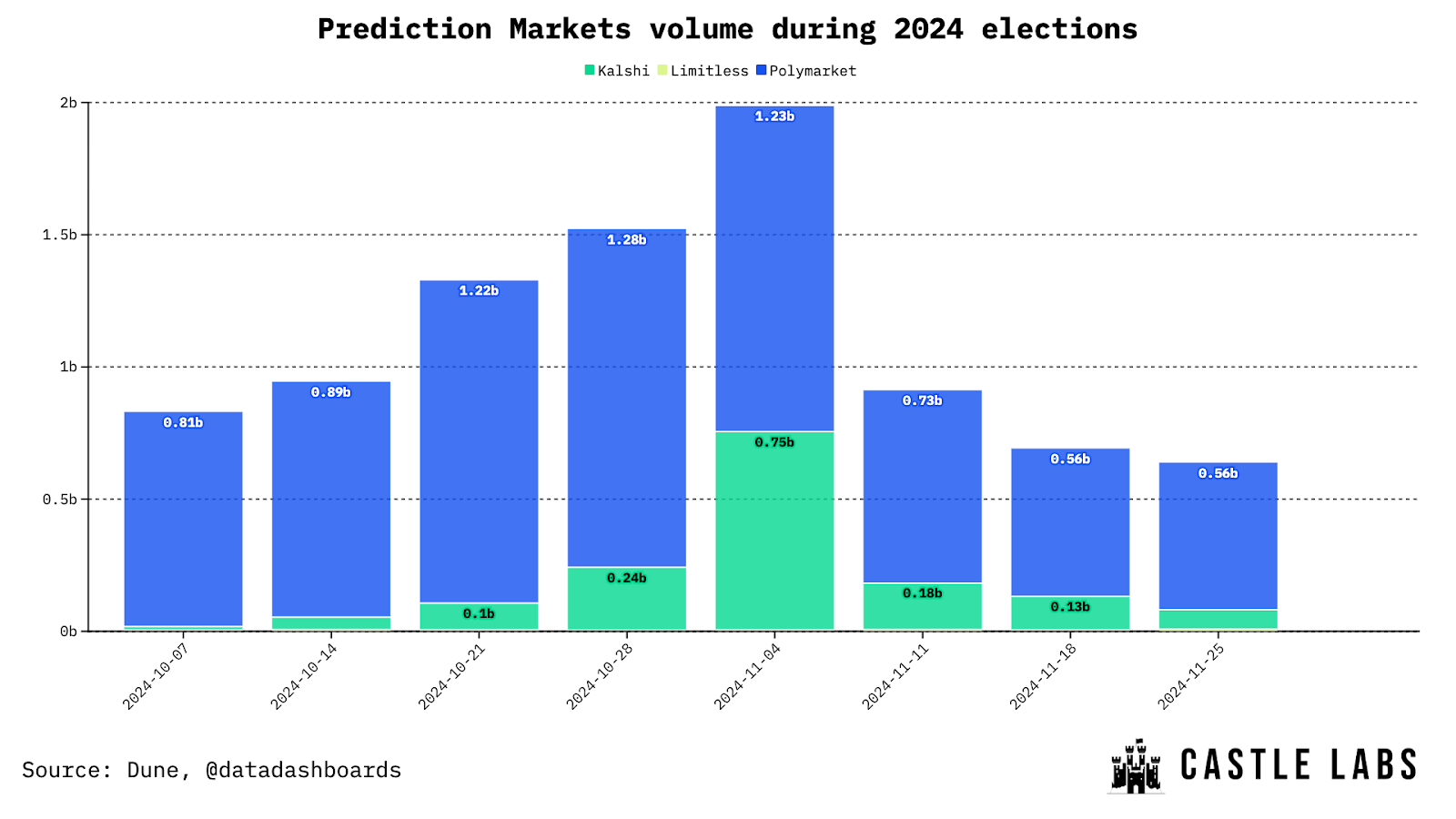

The primary catalyst that propelled the PMs into the mainstream was the 2024 US Presidential Election, which showcased the potential of prediction markets to reflect the interests or biases of the broader retail market and served as an indicator of public sentiment on elections.

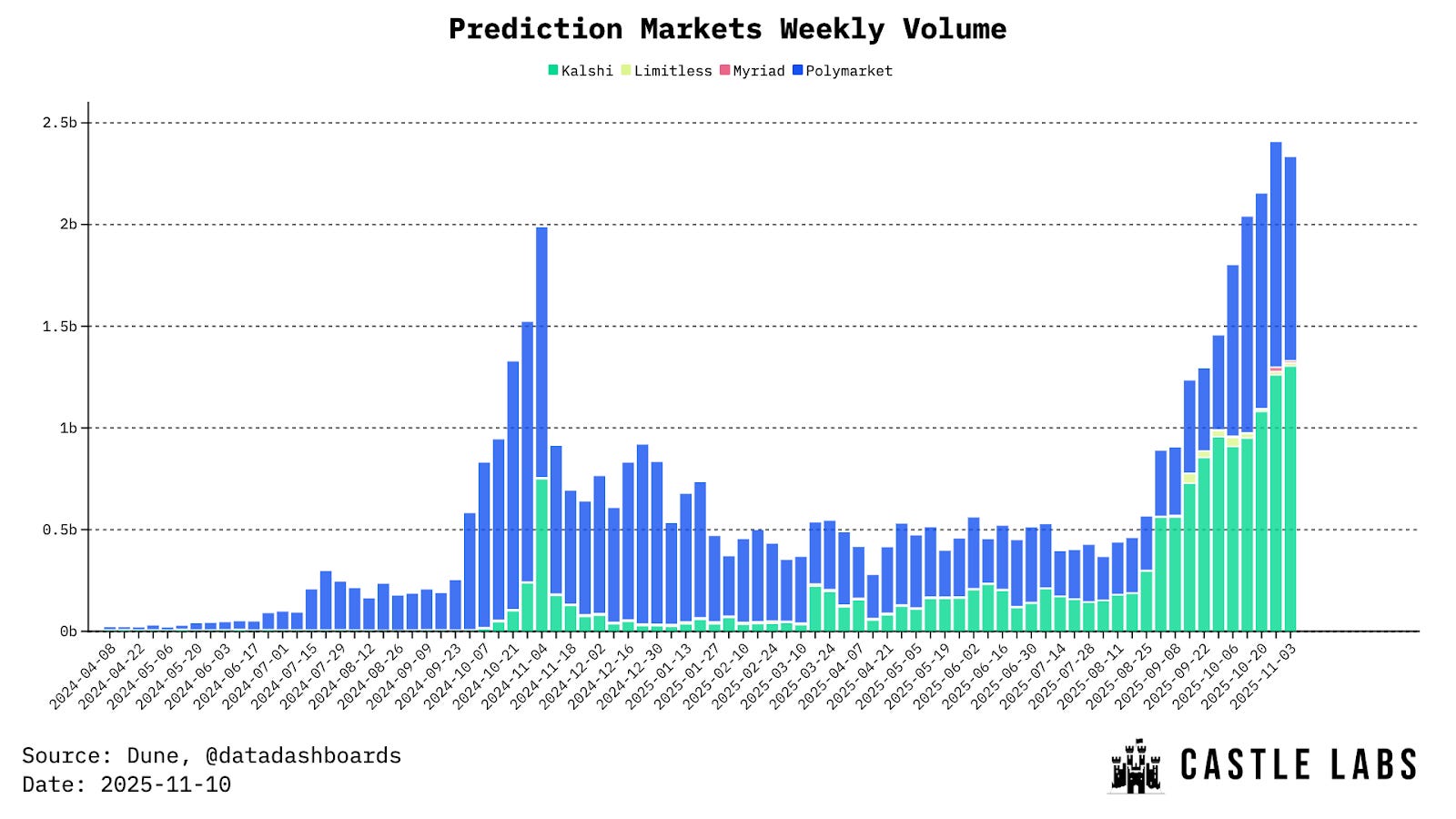

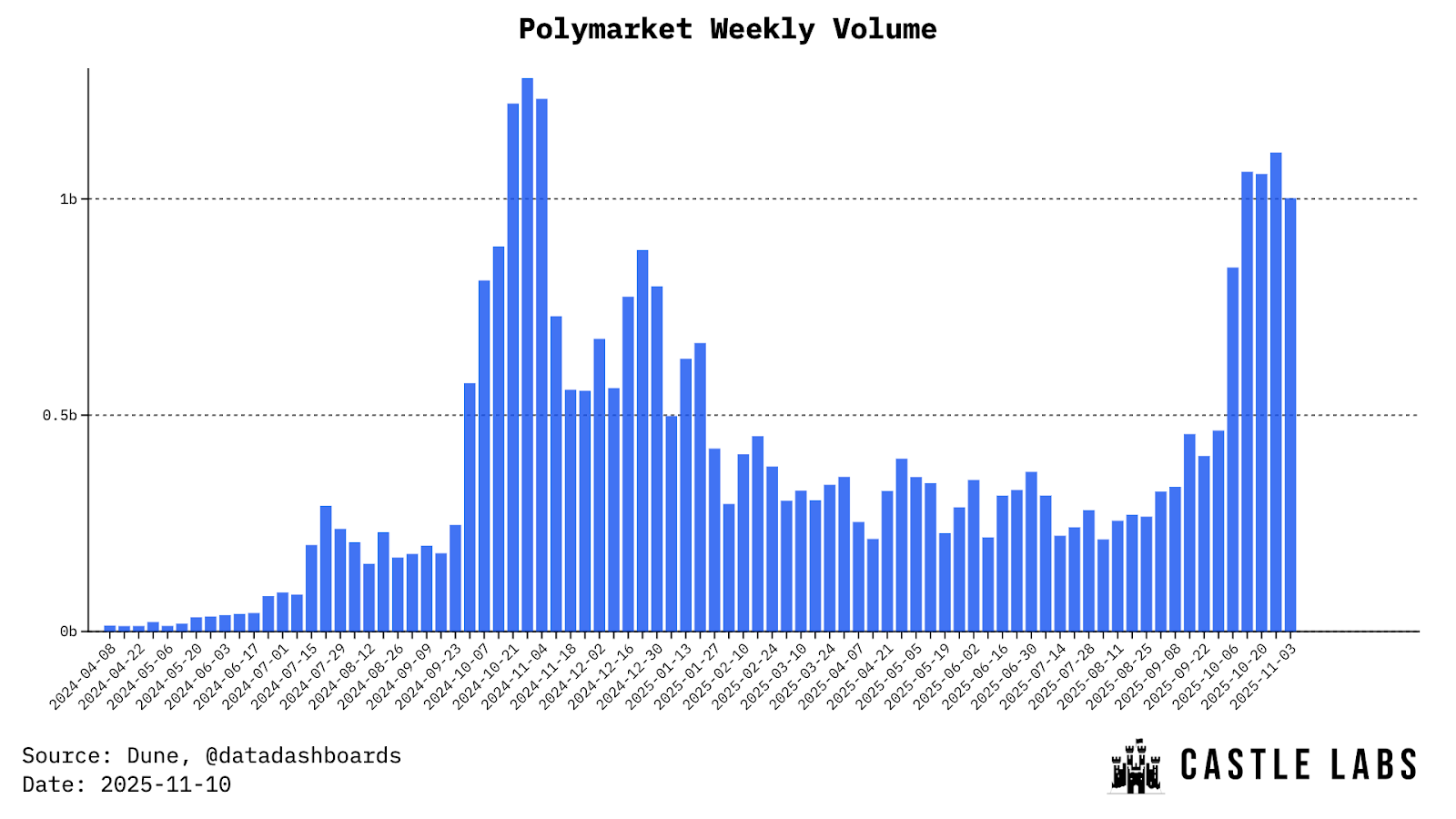

Based on current volume statistics, PMs appear to be approaching escape velocity and achieving volumes even higher than last year’s peak during the elections.

The growth of prediction markets, driven by increasing user and investor interest in this category, has led to the emergence of several new venues beyond the incumbents, Polymarket and Kalshi.

This report begins by providing an introduction and overview of prediction markets, followed by a comparative analysis of the selected platforms, which focuses on their design choices, unique offerings, and relevant data points.

We conclude by highlighting the main current and future trends and drawing insights on how the sector is likely to evolve, including additional emerging PM platforms.

All the data in this report is sourced from the Dune dashboard of datadashboard.

Deeper Look Into Prediction Markets

Before diving into PMs’ design, it’s essential to contextualise their development in relation to the value they provide.

Why prediction markets?

What’s unique about them?

Prediction Markets are an excellent tool for capturing the broader retail sentiment on events that are otherwise difficult to predict.

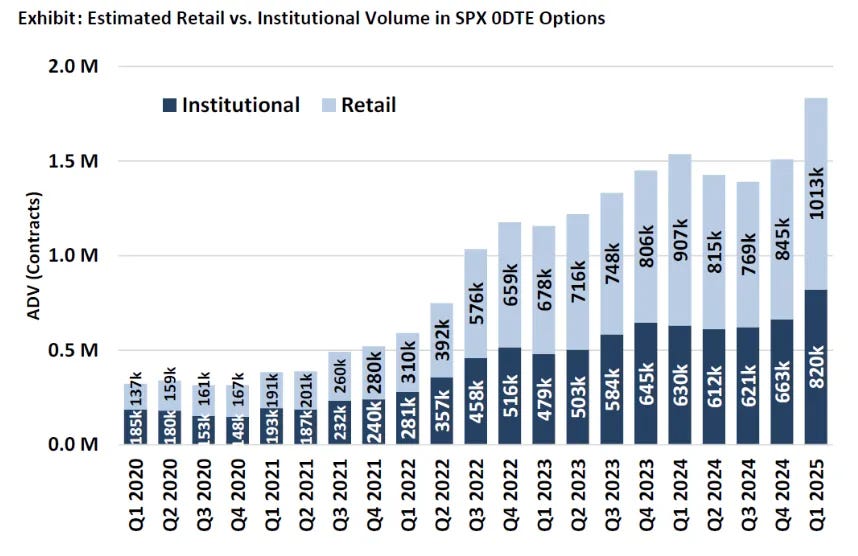

Aside from this, PMs expand the number of markets where retail sentiment can be gauged, including markets that settle faster and would otherwise be hard to track “traditionally”. This is also evident from the increasing share of retail volume in 0DTE (Zero Days to Expiration) options. 0DTE options are replicated in PMs through markets that settle in a single day, around ETH or BTC prices.

“To win and win big, retail is ready to walk through mud and get dirty rather than sit on a boat and cross the river.”

Another key aspect of prediction markets is that this sentiment is easier to trust than that in traditional “surveys” or other sentiment analysis, which might be distorted by deception or inaccurate opinions. Instead, on PMs, users back their opinions with their money, that is, with actual skin in the game.

Within the crypto space, PMs fit right in the middle of users’ propensity to gamble, their interest in leverage and fast settling markets, giving access to a broader range of markets where they can bet on, whether that’s sports betting, an asset price touching a certain level at the end of the day, an artist releasing a new album, or which products Apple is going to unveil at the Worldwide Developer Conference (WWDC), just to name a few.

While Polymarket has brought the sector into the mainstream, PMs have been around for a long time. The following section provides an overview of the history of prediction markets and their evolution into the current implementation.

Brief History of Prediction Markets

Early testers of prediction markets included Gnosis and Augur.

Augur was founded in 2014 and launched in 2018 as a decentralised prediction market with a native reputation token (REP, ICO in 2015) and an oracle system for reporting outcomes. But their system faced several issues, some of which are:

High gas fees on Ethereum

Unreliable and slow access to the blockchain data

L1 UX issues

Launching the token way too early

On the other hand, Gnosis was founded in 2015 and developed the Conditional Token Framework, which allowed anyone to create markets and turn event outcomes into tradable tokens in 2017 and 2018. Polymarket later adopted this framework. Gnosis closed its product due to issues similar to those Augur faced, including a poor onchain UX.

After these experiments, it took some time before Polymarket and Kalshi became the face of PMs and accounted for a significant share of volume.

Polymarket, utilising the conditional token framework from Gnosis, took the crypto-native path with a clean UI and a lower threshold for users to enter by launching on Polygon. Additionally, Polymarket is ready to set its foot in the US through its acquisition of QCEX (a CFTC-compliant derivative exchange) for $112 million.

Kalshi adopted a regulation-first approach and secured approval from the Commodities Futures Trading Commission (CFTC) in 2020 to become the first regulated PM in the United States (US).

As part of their expansion efforts, both companies raised significant funds.

Polymarket recently raised $2 billion in investment from Intercontinental Exchange (NYSE parent firm) at a post-money valuation of $9 billion. Following the announcement, Kalshi also unveiled a $300 million raise at a $5 billion valuation, led by investors such as Sequoia Capital and Andreessen Horowitz.

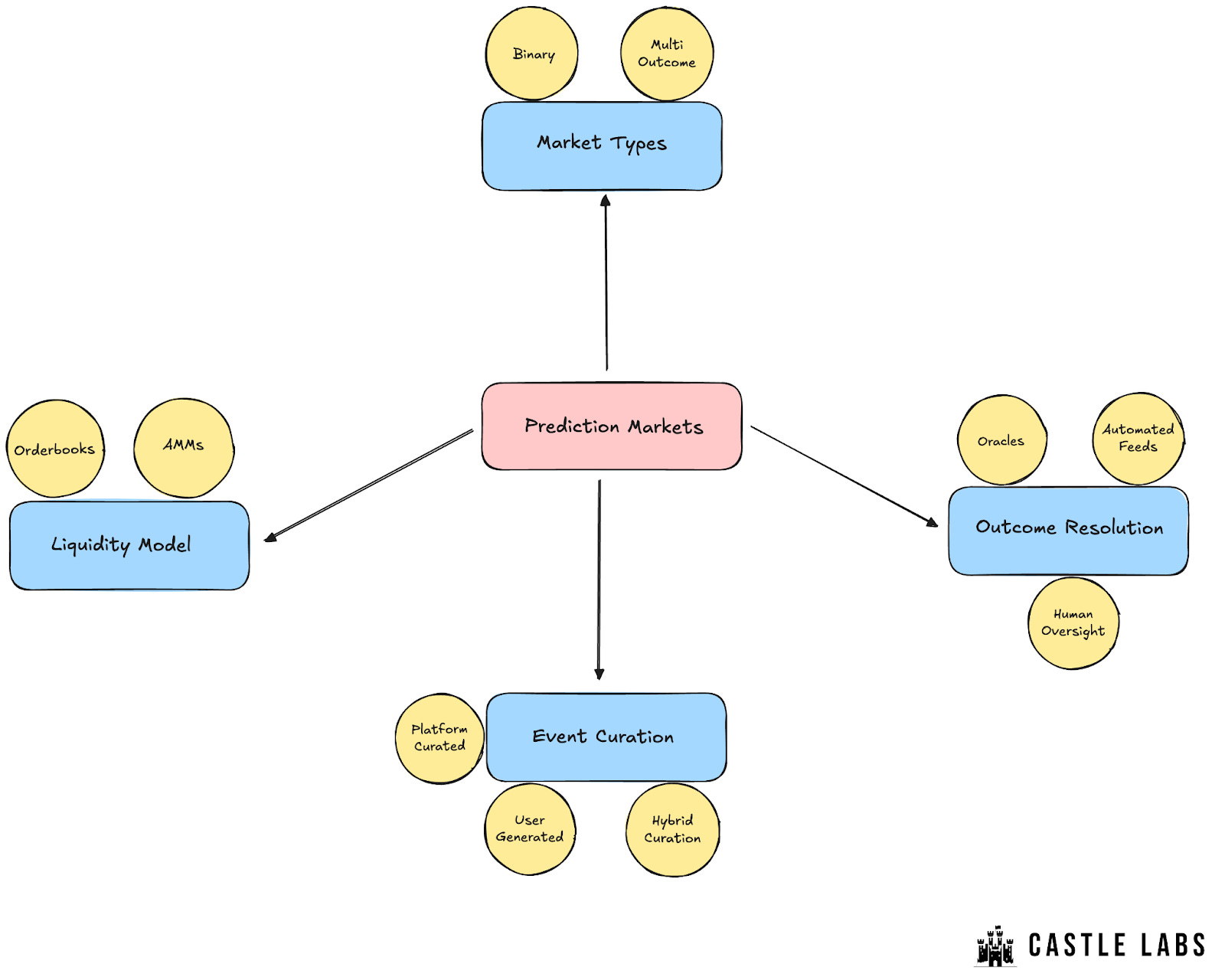

The Unique Design of Prediction Markets

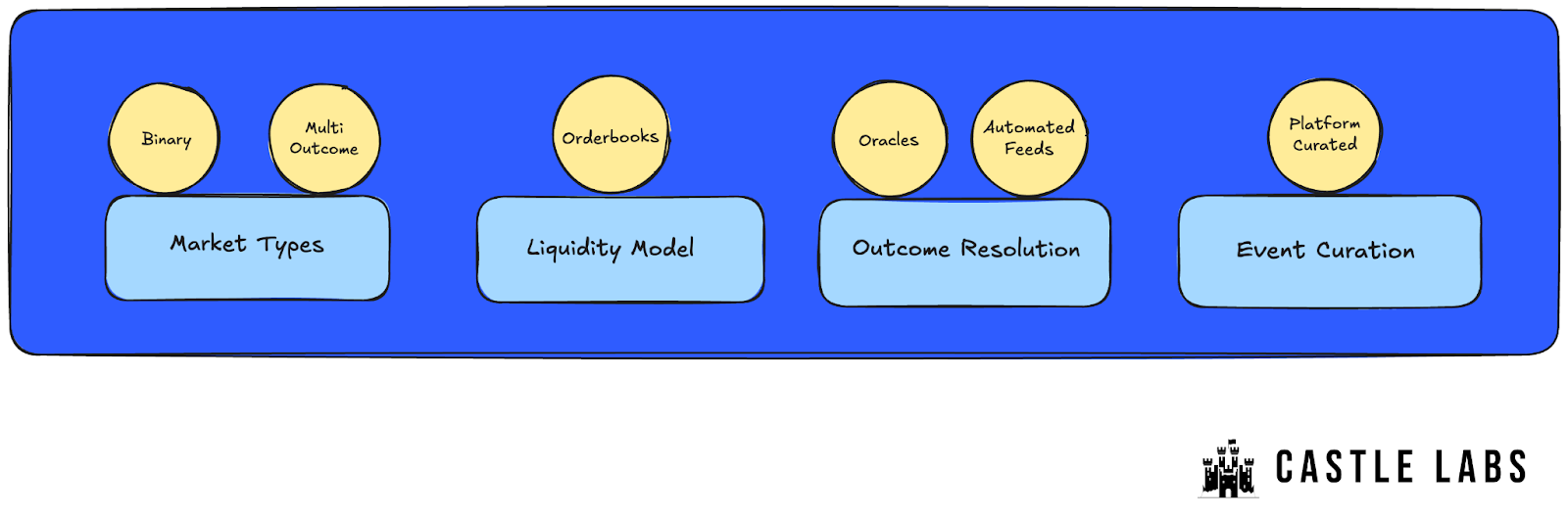

While every platform has its own design choices, we will try to set a common ground for them in this section, focusing on the following aspects:

Market Types

Liquidity Model

Outcome Resolution

Event Creation Mechanism

Most of this section is sourced from Baheet’s piece on Prediction Market Typology.

Market Types

Primarily, PMs support two market types: a binary market and a Multi-Outcome Market.

A binary market is a market that offers traders two choices: “Yes” or “No”. A user can choose to buy either “Yes” shares of that market, betting on the event occurring, or “No” shares to bet that the event will not occur.

The 82% in the chart above indicates that people are betting on the high probability that Ethereum will be up the next day, and it also means that buying the “Yes” or “Up” shares costs $0.82 each. The simple unit economics of binary markets make it easier for traders to understand the direction of the probability incline.

A multi-outcome market has more than two possible outcomes, with only one outcome being considered the winning outcome. Now, at the end of the day, a user will still be buying “Yes” or “No” shares, but for a particular outcome rather than the whole market.

Outcome Resolution

As we mentioned above regarding the different market types, when they are resolved, they require a source of truth. This information, which helps dissolve a market, can come from oracles, human intervention, or automated feeds. They can even be used in combination on the platform and are not mutually exclusive.

Oracles: The work of an oracle is to provide accurate information about any real-world event and sometimes asset prices. A group of validators usually reaches consensus on specific data pushed onchain to resolve a market. Polymarket is a good example here, as it utilises the UMA protocol’s optimistic oracles for outcome resolution. There is also a challenge period involved, during which the user can dispute the outcome.

Human-Intervention: The other resolution path is through human intervention, where the team can review and decide on the market outcome based on predefined rules. This can harm scalability and lead to high centralisation. Platforms like Kalshi utilise human oversight in certain markets if needed in accordance with CFTC guidelines.

Automated Feeds: The third or last type is a specific automated feed used in combination of both the above paths, where an external feed or API is responsible for resolving a market. Since certain markets, such as those we showed in the above section, that depend on the Ethereum price can be accessed via specific price APIs. Additionally, markets like “Will Apple announce AirPods Pro 3 in WWDC this year or not?” can be resolved through news APIs.

Liquidity Model

Prediction markets source the liquidity usually in two ways:

Automated Market Makers (AMMs): AMMs ensure that liquidity is always available to trade. The platforms utilising this source of liquidity often rely on algorithms like the Logarithmic Market Scoring Rule (LMSR).

Central Limit Orderbooks (CLOB): Orderbooks require active traders or market makers (MMs) to maintain liquidity. Polymarket and Kalshi utilise orderbooks in their platforms.

While AMMs solve the cold-start problem, they often come with certain limitations, the major one being capital inefficiency, as it requires the initial capital to be locked to initiate a market. On the contrary, orderbooks are great for scalability as they match bids and asks directly and depend on the actual user flow and don’t lock the capital, hence they are used by almost all the platforms.

Event Creation Mechanism

The Event Creation Mechanism reflects how markets can be created on a platform. There are usually three ways to go with this:

Platform Curated: A permissioned nature of market curation where the platform and the team decide and vet the markets carefully before they go live. Kalshi and Polymarket are primarily using this model.

User-generated / Permissionless: A permissionless model, allowing anyone to create a market by following the rules set by the platform. This is less seen, as it comes with some risks —the biggest being liquidity fragmentation and platform overload, which may also lead to spam.

Hybrid Curation: This approach falls between the above two, as users can propose markets, but they go live through a community-based governance process or a voting system.

PMs as Source of Truth: The Presidential Election Push

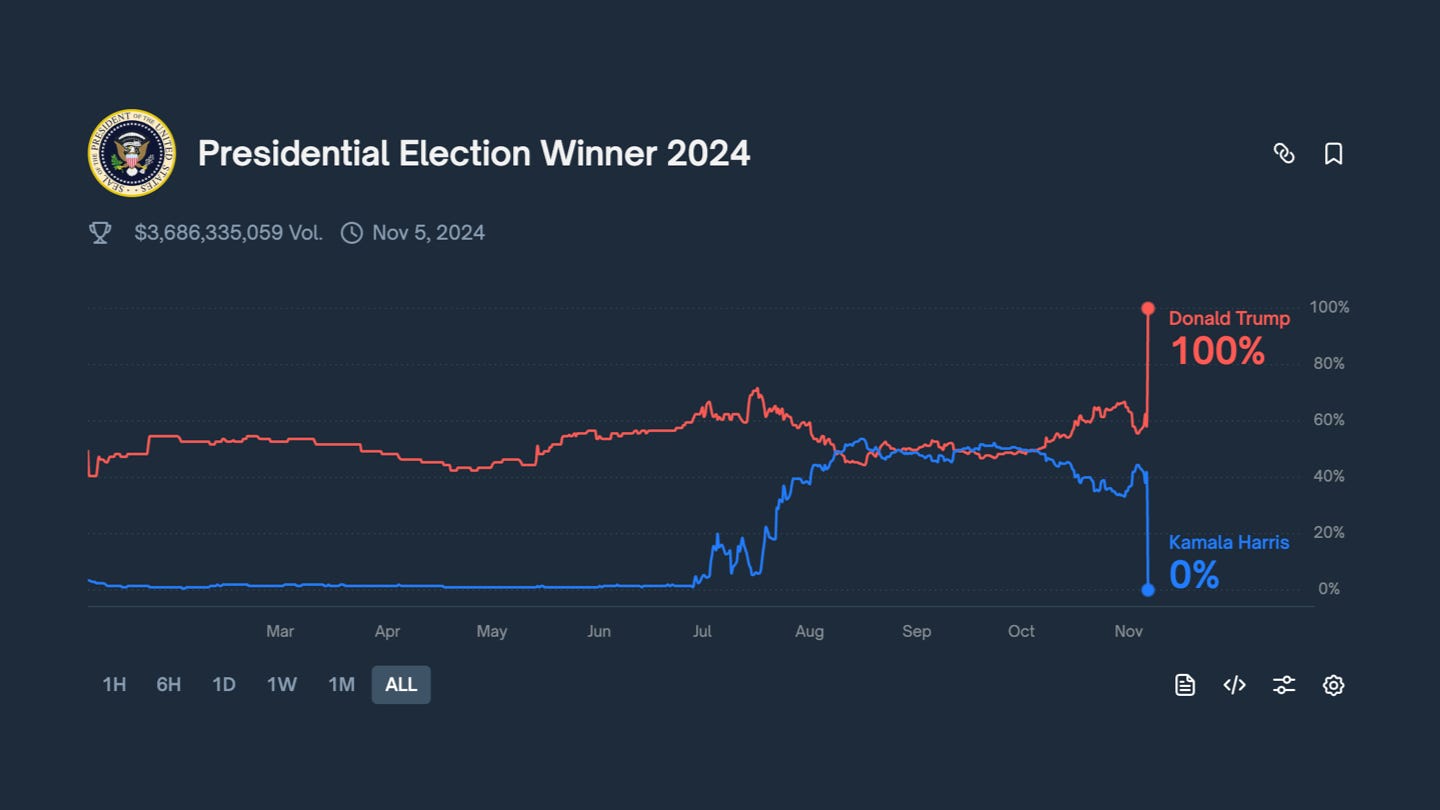

We have emphasised this point in the introduction: the 2024 presidential election propelled PMs into the mainstream. It also established them as a sentiment source that can reflect the decisions of the majority of the market or users.

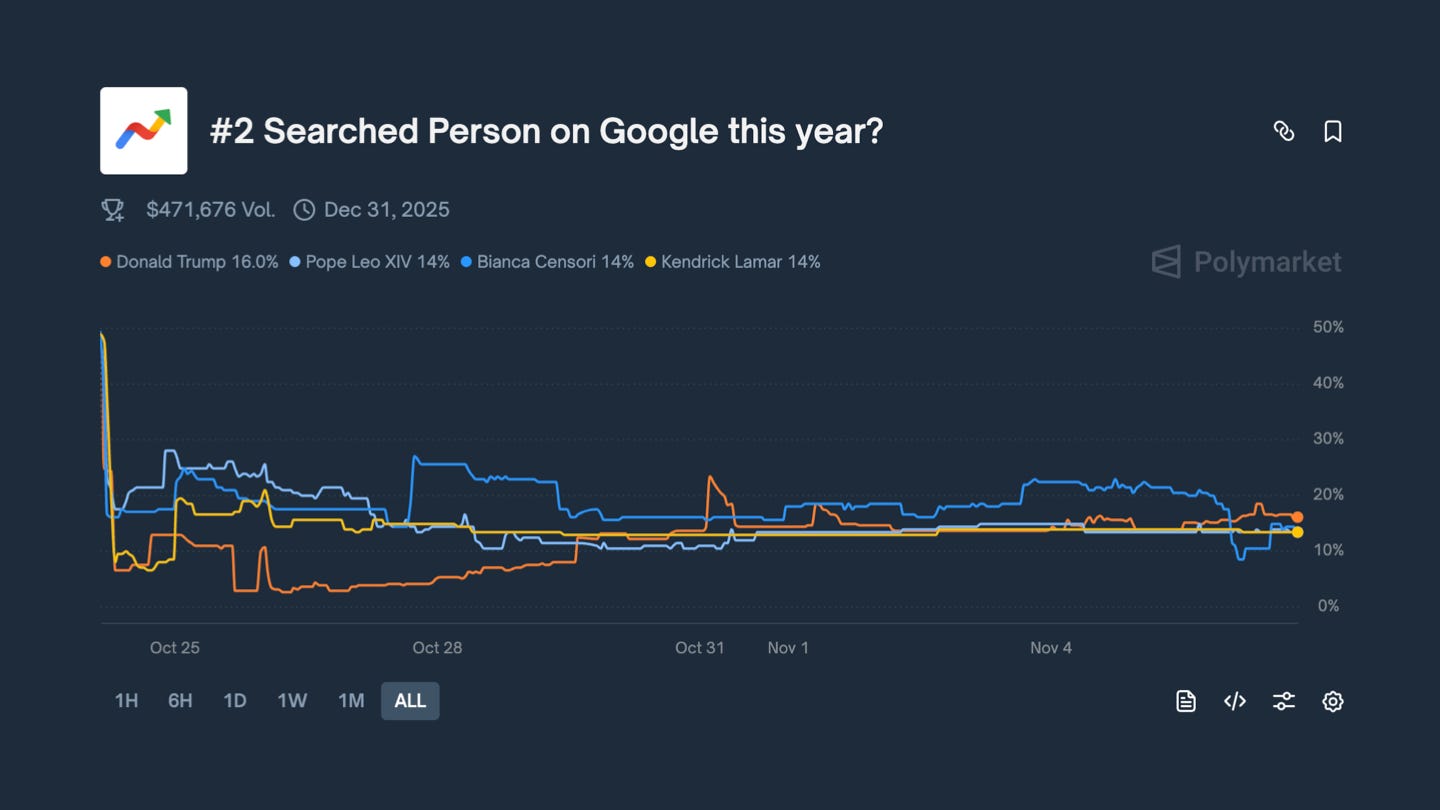

Because Polymarket (screenshot below) displayed what people were thinking in real-time, several news channels broadcast these charts and even relied on them for their reporting. Before the official numbers were released, you can see in the chart below that Donald Trump’s winning probability was already on the rise. At the same time, the legacy media reported that the competition was neck and neck.

“A Prediction Market is as good as the markets on it.”

PMs offer two unique use cases which are interdependent:

Making Your Opinion Worth Something: This is the core motivation of a PM, encouraging more people to use it by having them back their opinions with funds.

A News Source: This is the secondary use case, which often develops when the first one is achieved at a larger scale. A prediction market is a valuable source of information, particularly in markets where traders can contribute in real life to diluting the market in their favour (e.g. in elections where traders are also voters).

There are many arguments suggesting that we have achieved the former fairly well; however, the latter, as a great news source, requires more effort. Achieving these two use cases should be the outcome of a great PM.

The second one comes from a relevant market with sufficient volume, high liquidity, and a large number of users trading in it, thereby representing a significant sample. A good example of this was the election market from last year, which saw substantial volumes, high user interest, and was highly relevant to everyone.

A Comparative Analysis of Prediction Market Venues

As the PMs have grown and are now a broadly adopted category, we see different protocols emerging and testing how much people are willing to bet. While covering all of them would exceed the scope of this report, we will highlight a few, including the dominant platforms such as Polymarket and Kalshi, as well as emerging protocols like Limitless and Myriad.

For each analysed protocol, we will discuss its Market Positioning and design choices, reflecting how it approaches liquidity, market curation, outcome resolution, and other aspects. On the other hand, Market Positioning will aim to highlight what users these protocols are fighting for and how they have positioned themselves to attract more of their target market.

Polymarket

Polymarket launched in 2020 and has been building on the crypto rails since day one. It is the first prediction market to scale. While creating over the years and testing different models and designs, they reached the inflexion point during last year’s elections, and since then, they have been consistently gaining higher volumes. However, it is fair to say that the current volume increment is also due to the expectations of an impending launch of their token, POLY, and a potential airdrop, which will be dependent on the volume a user creates.

Market Positioning

Building for years following the pro-crypto ethos, Polymarket positioned itself to be the go-to place for crypto-native users, as it doesn’t require them to perform KYC, accept crypto deposits, and have deep liquidity.

Since building on crypto rails, they were not specifically positioned to serve heavily regulated demographics, such as the United States. However, with their acquisition of QCEX this year, they have now filled this gap and can serve US customers, though Polymarket US is yet to launch.

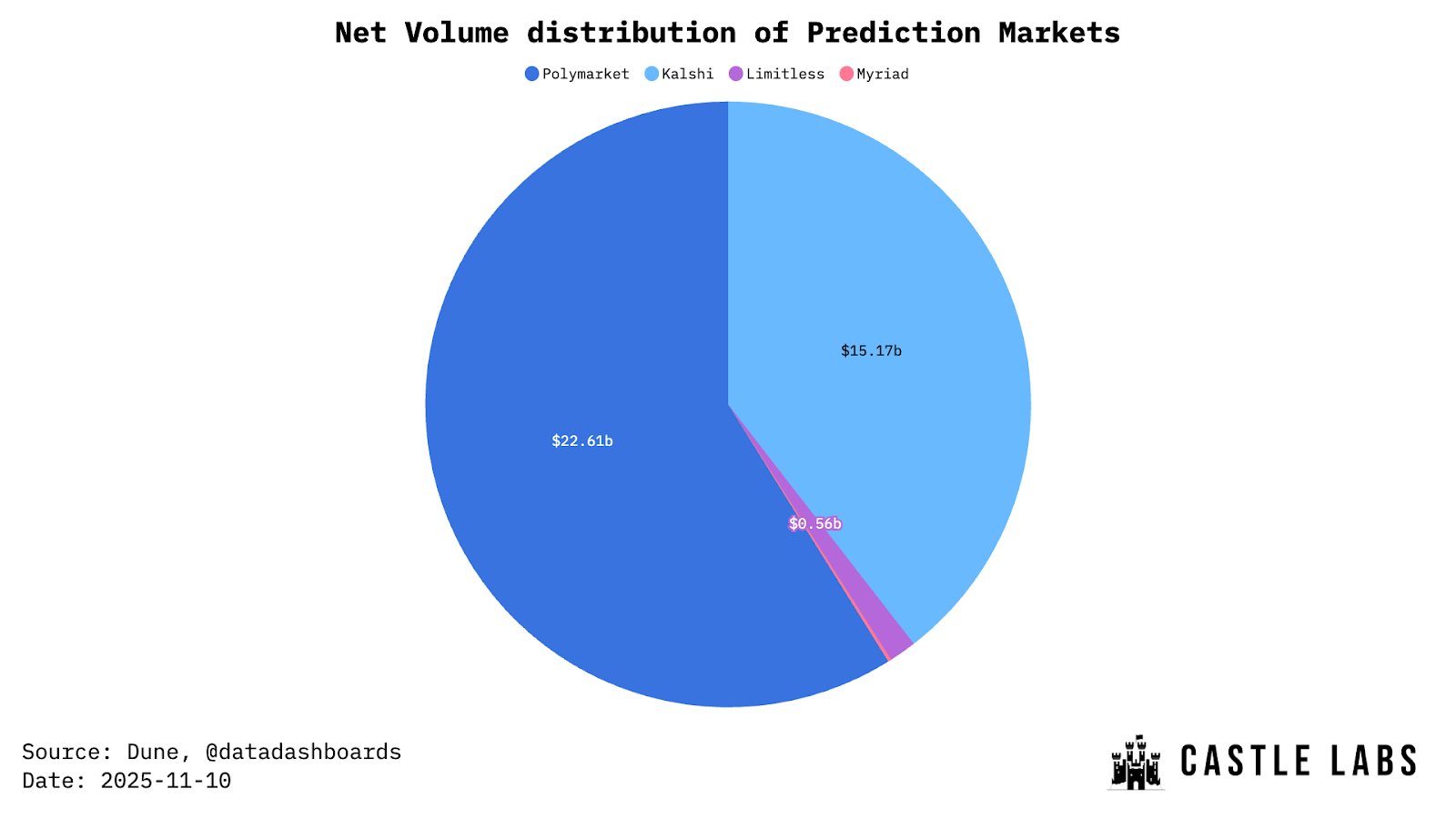

Since its inception, Polymarket has achieved a cumulative volume of ~$22 billion on its platform, serving over 1.5 million unique users.

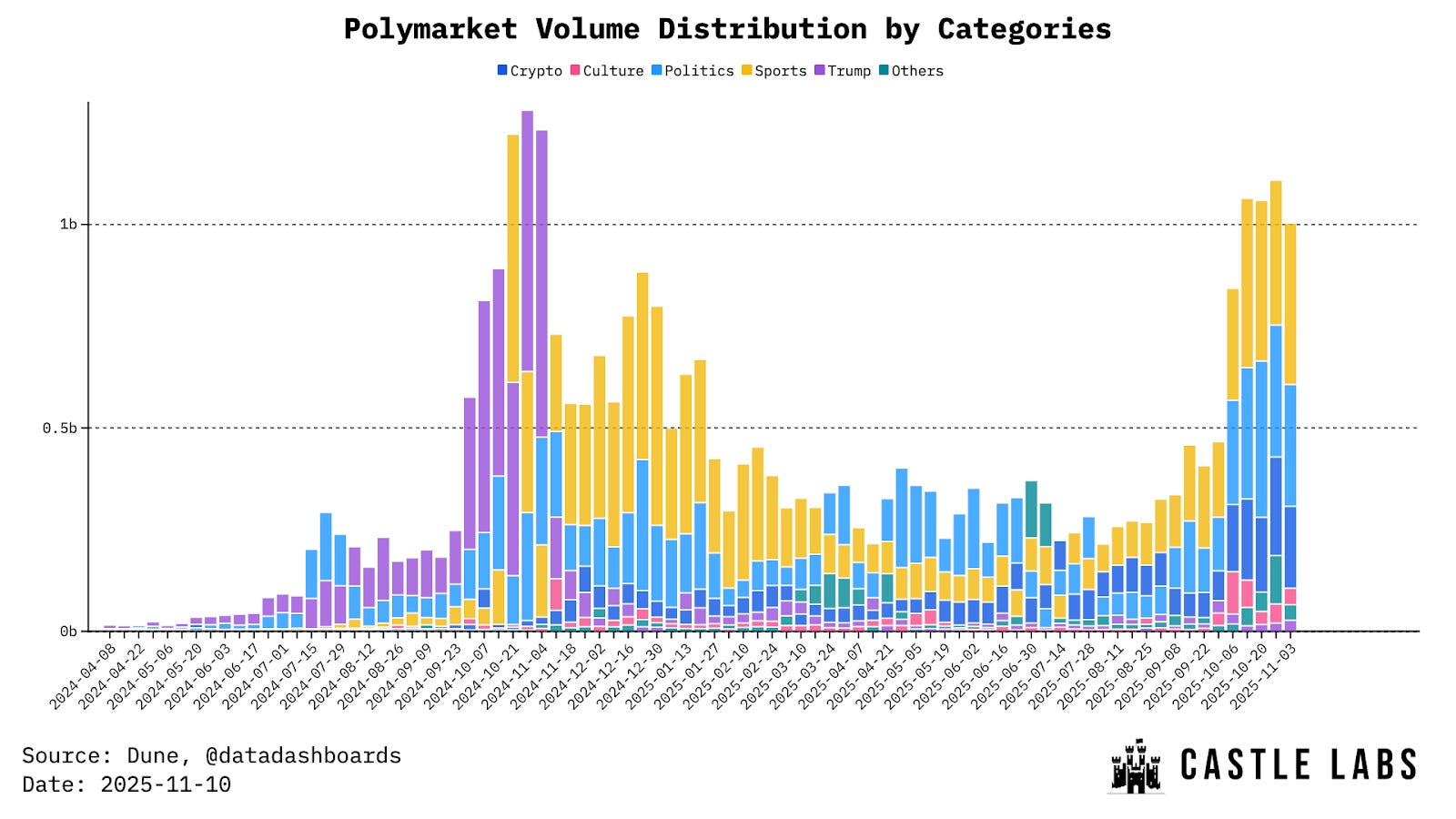

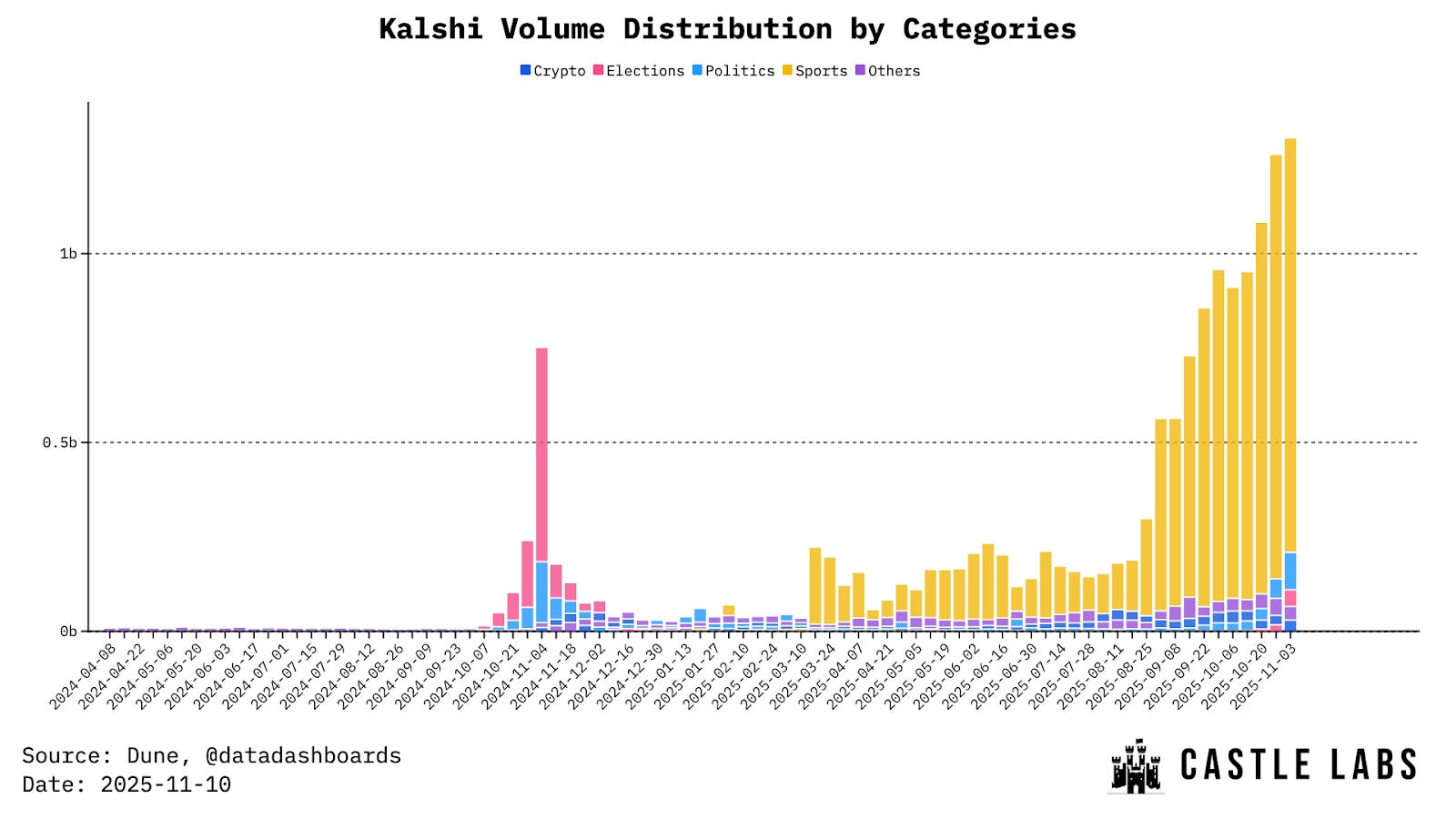

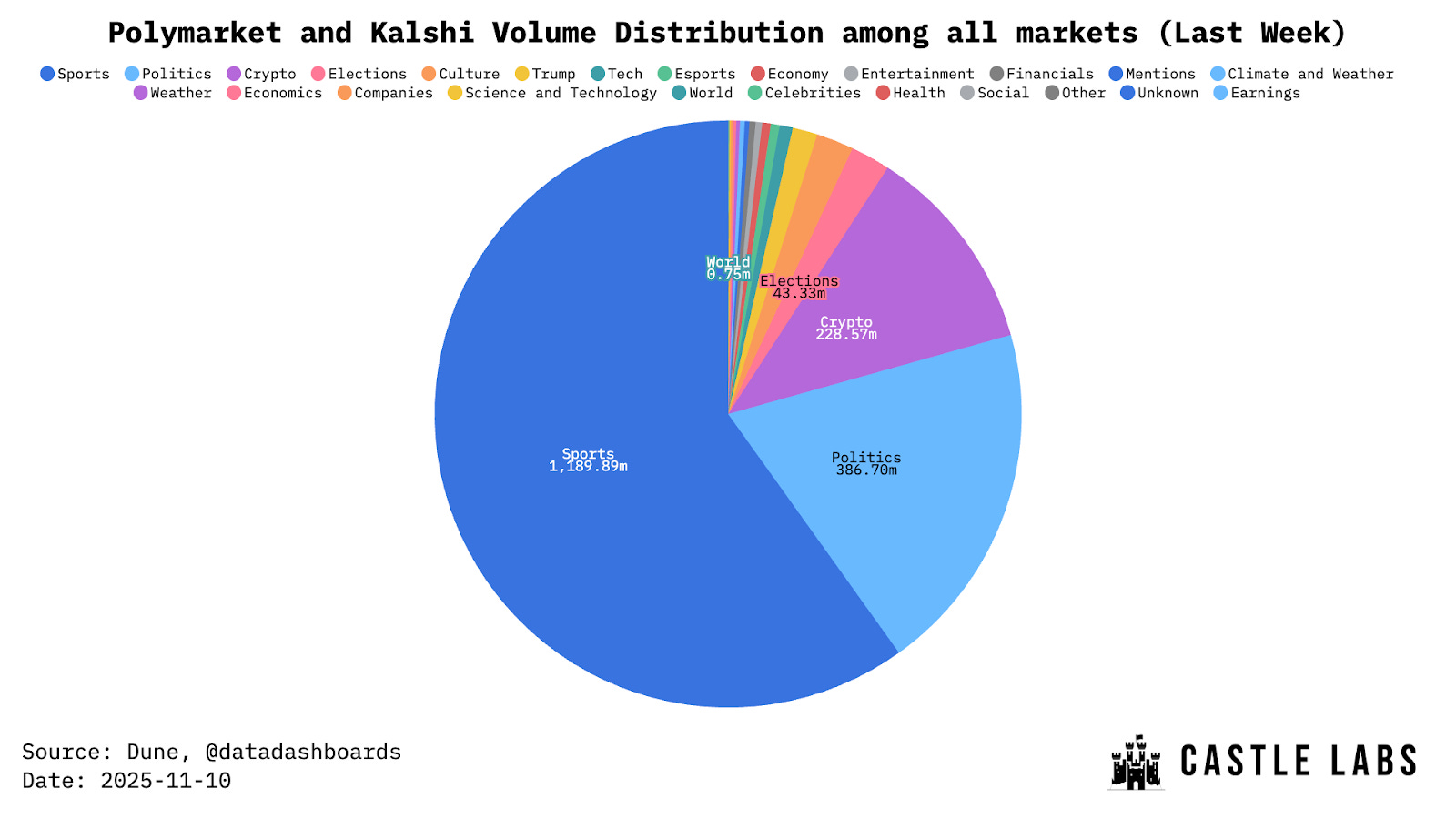

Polymarket gains its position in the headlines through its markets around politics, which contribute significantly to its volume. The platform volume is currently dominated by sports, followed by Politics, Crypto, and Culture-related markets.

Design Choices

Covering the design choices made by Polymarket, which reference the mechanics mentioned in the sections above, the platform offers both binary and multi-outcome markets to its users. It sources liquidity through an orderbook structure, with events curated by the platform and outcome resolution determined by optimistic oracles from UMA. Additionally, Polymarket charges no fees on depositing, withdrawing, or trading in its markets.

Kalshi

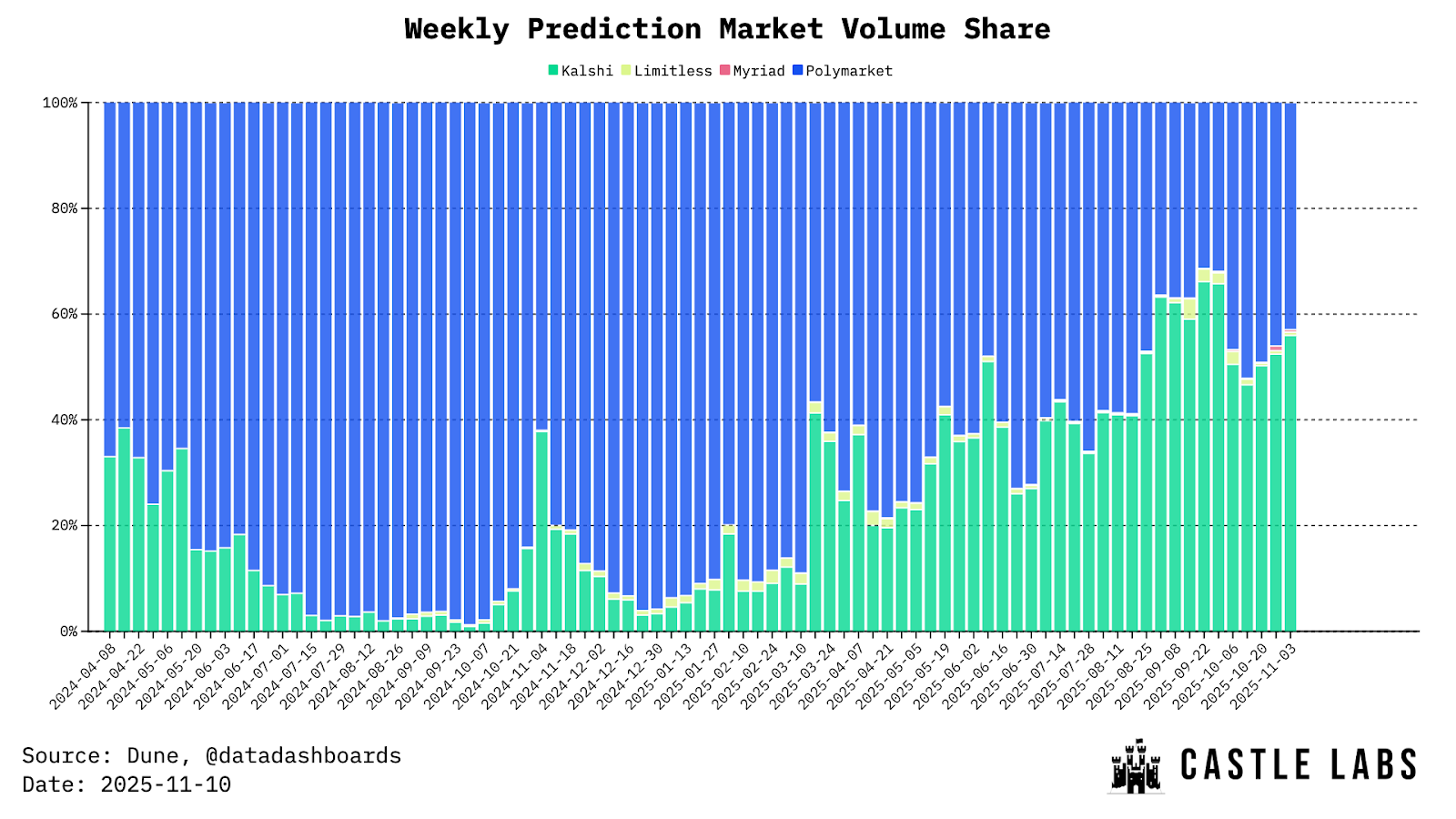

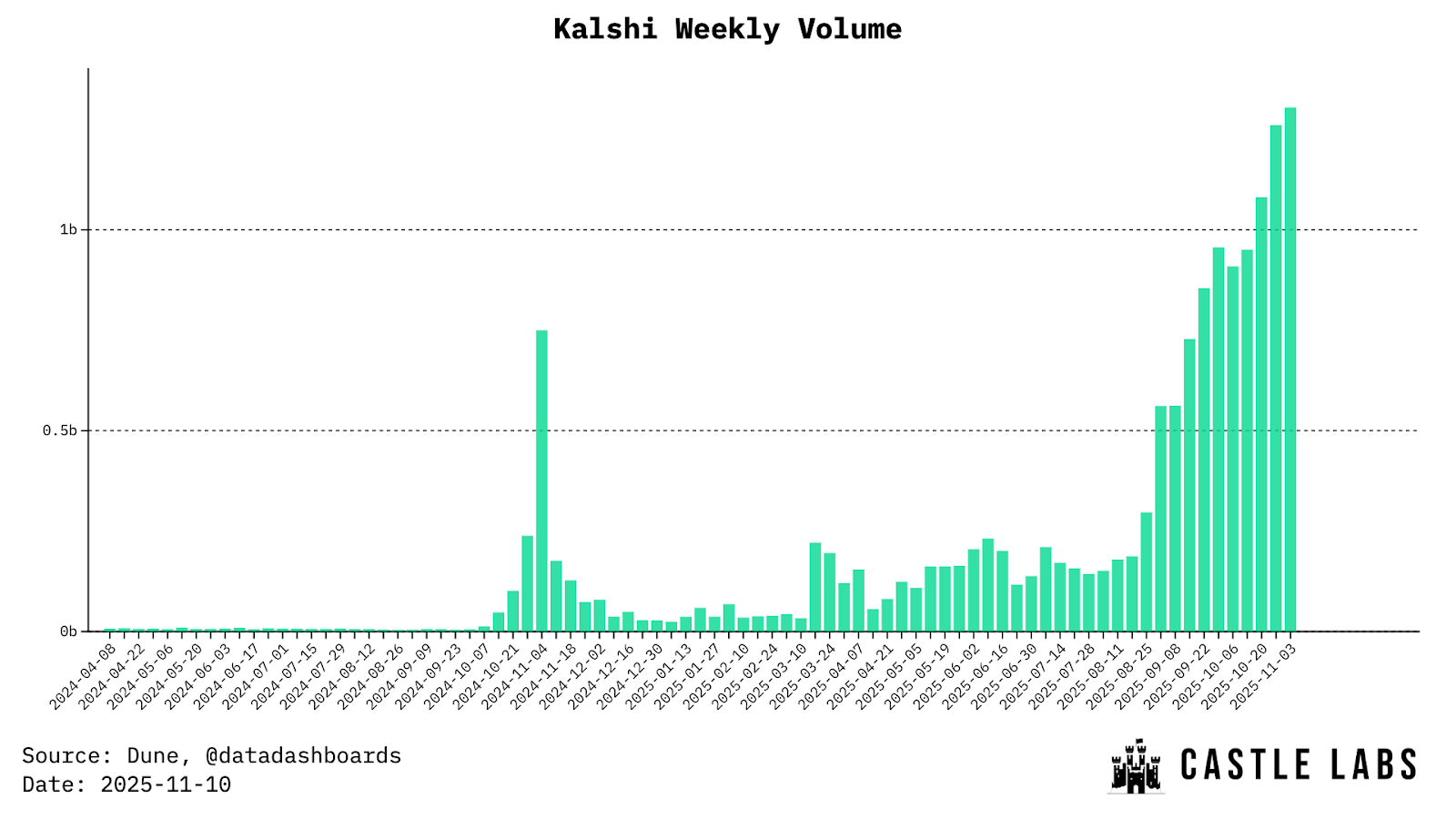

Kalshi was launched in 2021 and has consistently adopted a regulatory-forward approach, positioning itself as less crypto-native compared to Polymarket. Only once it has firmly established itself as a regulated PM, and it is now leading a vigorous campaign to set afoot among crypto-natives. This approach for Kalshi has been fruitful so far, and they are seeing a continuous incline in the platform’s volume metrics. In terms of cumulative volume, Kalshi has done over $15 billion.

Market Positioning

As a CFTC-approved PM in the United States, they hold a significant market share, enabling users to access the platform in a regulatory-compliant manner. This approach for Kalshi sets it apart and has given it an edge in the space. Competitors like Polymarket have even acquired a derivative exchange, QCEX, to earn this title and run their operation smoothly in states.

The race to launch a great PM in the US is driven by the large market for sports betting, and capturing a larger share of this market is beneficial for anyone in the business. With that being said, Kalshi’s primary volume driver has been its sports betting markets, accounting for over 80% of the platform’s volume. Having positioned itself for sports betting, Kalshi ensures recurring revenue, rather than relying on one-off, significant events such as the US elections.

To capture more of the crypto natives, they are slowly providing support and have recently been on a spree of hiring crypto Twitter (CT) figures who can contribute to their vision. This has been great so far because they needed a better image between degens, as they were perceived as too regulatory-friendly, which generally goes against the core crypto ethos.

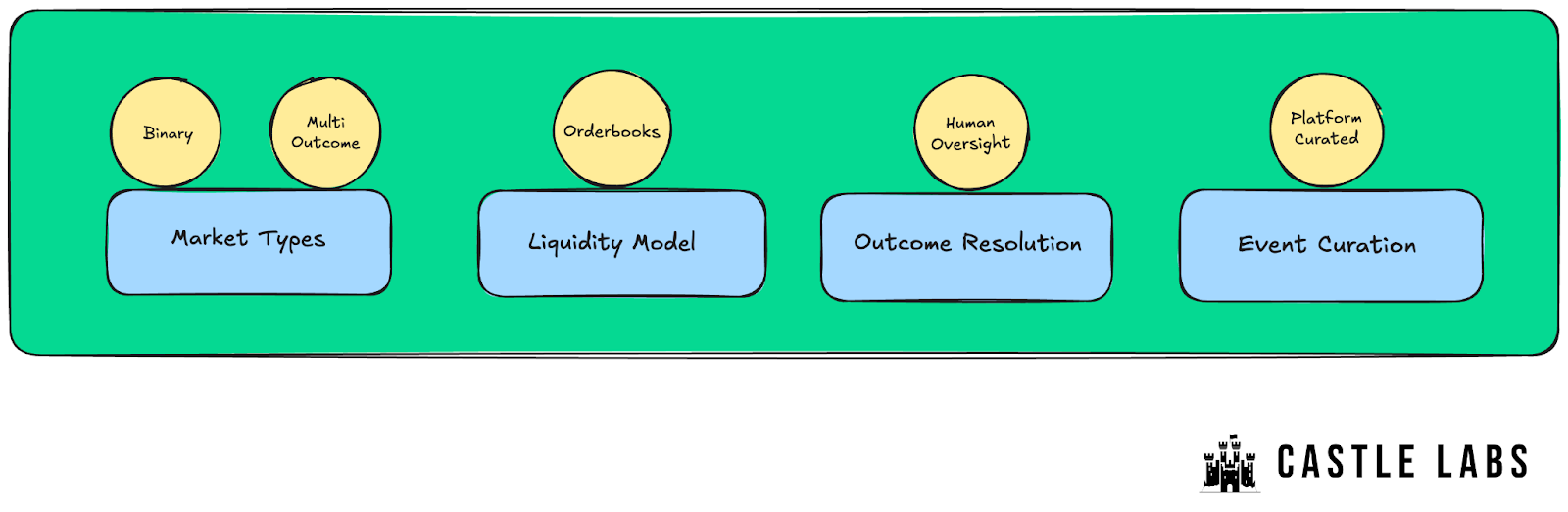

Design Choices

Kalshi’s design choices and offerings are similar to those of Polymarket. They offer two market types, binary and multi-outcome, and provide liquidity through an orderbook model. It is essential to highlight that they have a dedicated trading desk for market making and also support third-party makers, as mentioned above.

When it comes to outcome resolution, Kalshi utilises human oversight as required to be CFTC-compliant. Additionally, the events on the platform are curated by the team. Moreover, Kalshi charges its users with transaction and maker fees. These fees vary depending on the market.

Limitless

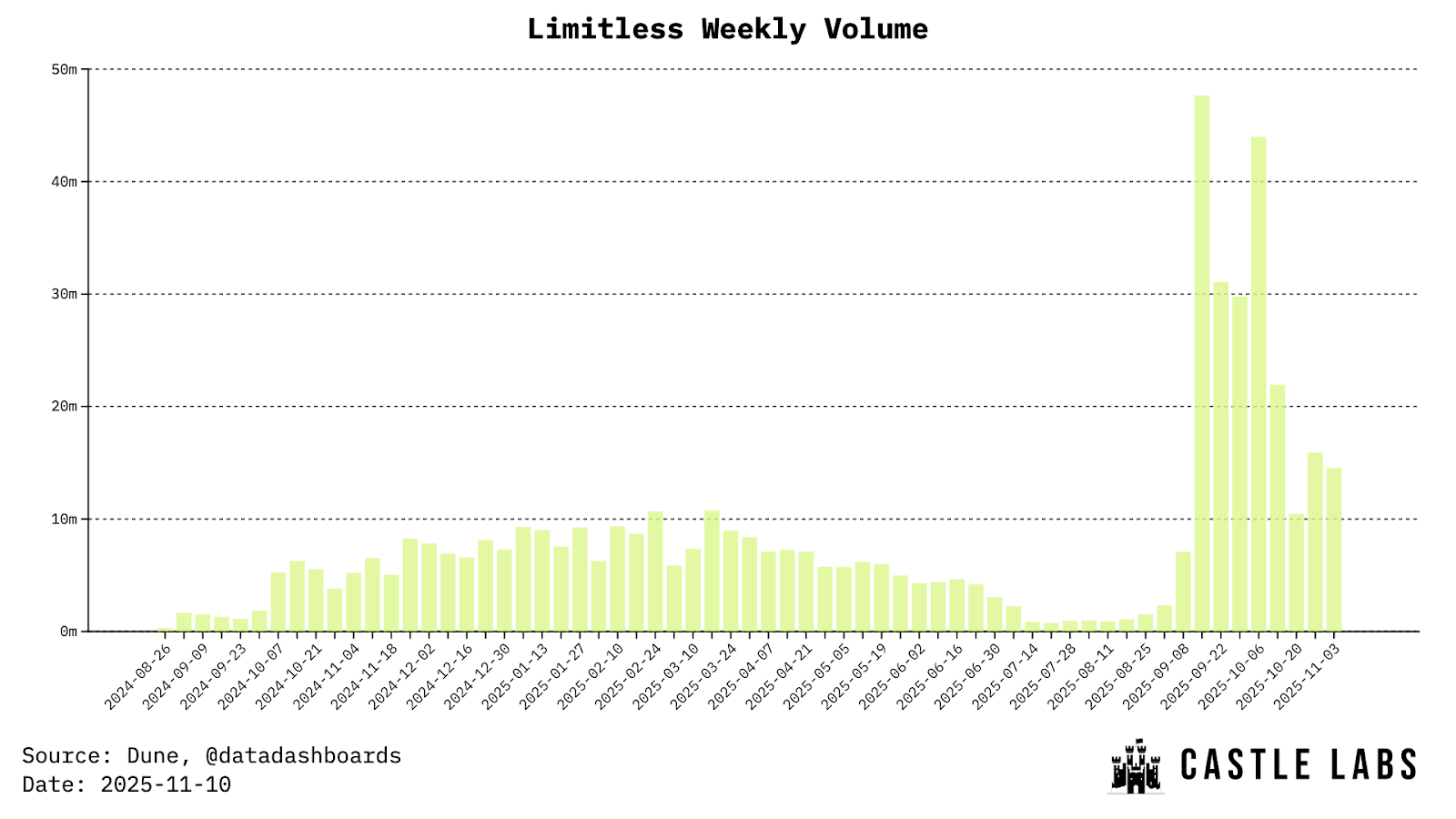

Limitless has also been following the path of a decentralised PM. Their volume metrics have recently spiked again following the launch of their token, LMTS. Upon launching the token, the team is heavily utilising it to incentivise the platform’s traders, as reflected in their metrics.

Limitless is deployed on base and has ~70k cumulative unique users, with an all-time volume exceeding $500 million. Their metrics are significantly lower than those of Polymarket and Kalshi. Still, they have taken a different approach to their offerings, which we will discuss in the upcoming sections.

Market Positioning

Limitless has focused on providing a market that settles faster and is closely tied to crypto prices. They offer markets with settlement times of 30 minutes, hourly, daily, and weekly. However, most of these markets, even when replicating 0DTE options in even more crypto form (trading below the settlement time of day), still struggle with low volume and user interest.

Markets related to crypto on Limitless have been the primary driver of their volumes, primarily due to their high composition, followed by markets related to the economy, politics, and general news.

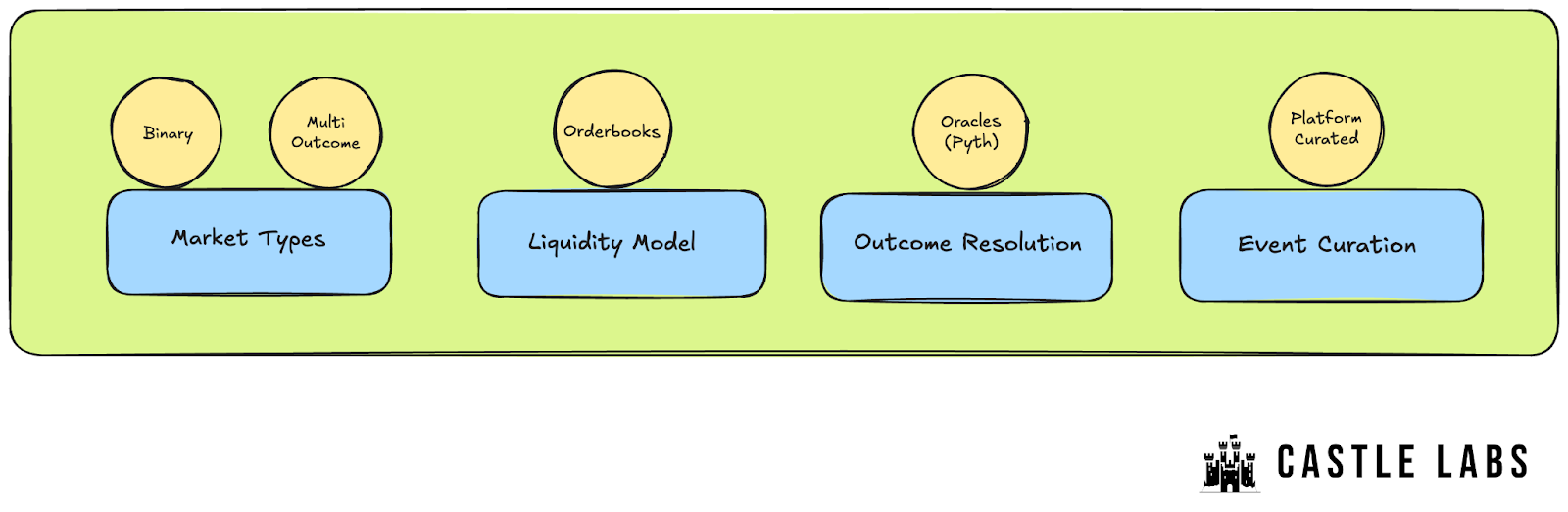

Design Choices

Since Limitless operates across multiple markets, it uses a decentralised oracle provider, Pyth, for the price feeds. They offer both sorts of markets, which are binary or multi-outcome. They also allow users to convert “Yes” shares of a market to “No” shares, and vice versa, improving capital efficiency and preventing capital from being locked up. The liquidity of a market is sourced from the orderbook model and event curation performed by the platform itself.

The fees on the platform vary from 0.03-3% based on the returns of that trade; the lower the return, the lower the fees. The fees on the buying side of the trade are paid in outcome tokens, and the selling side in collateral tokens like USDC.

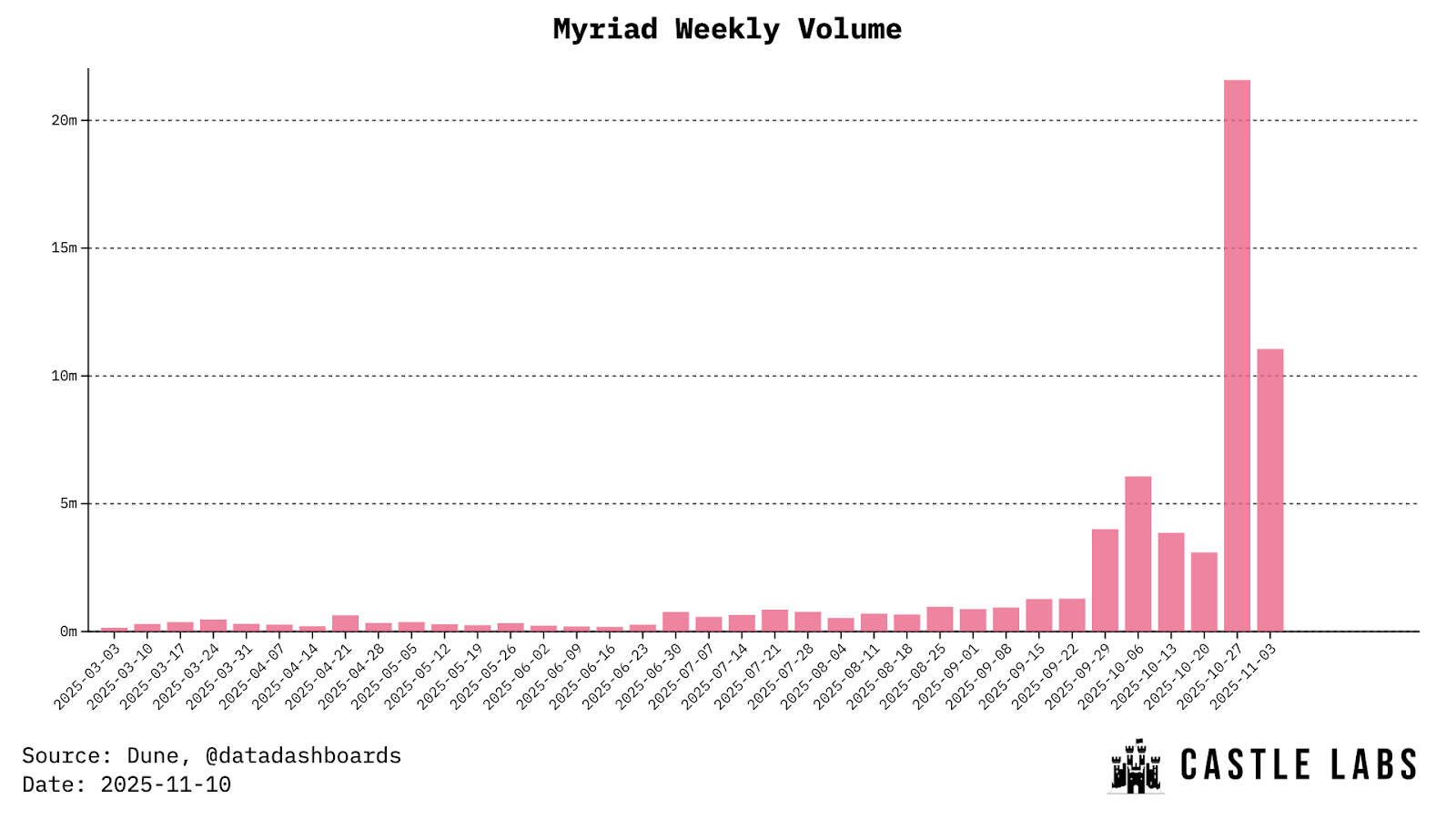

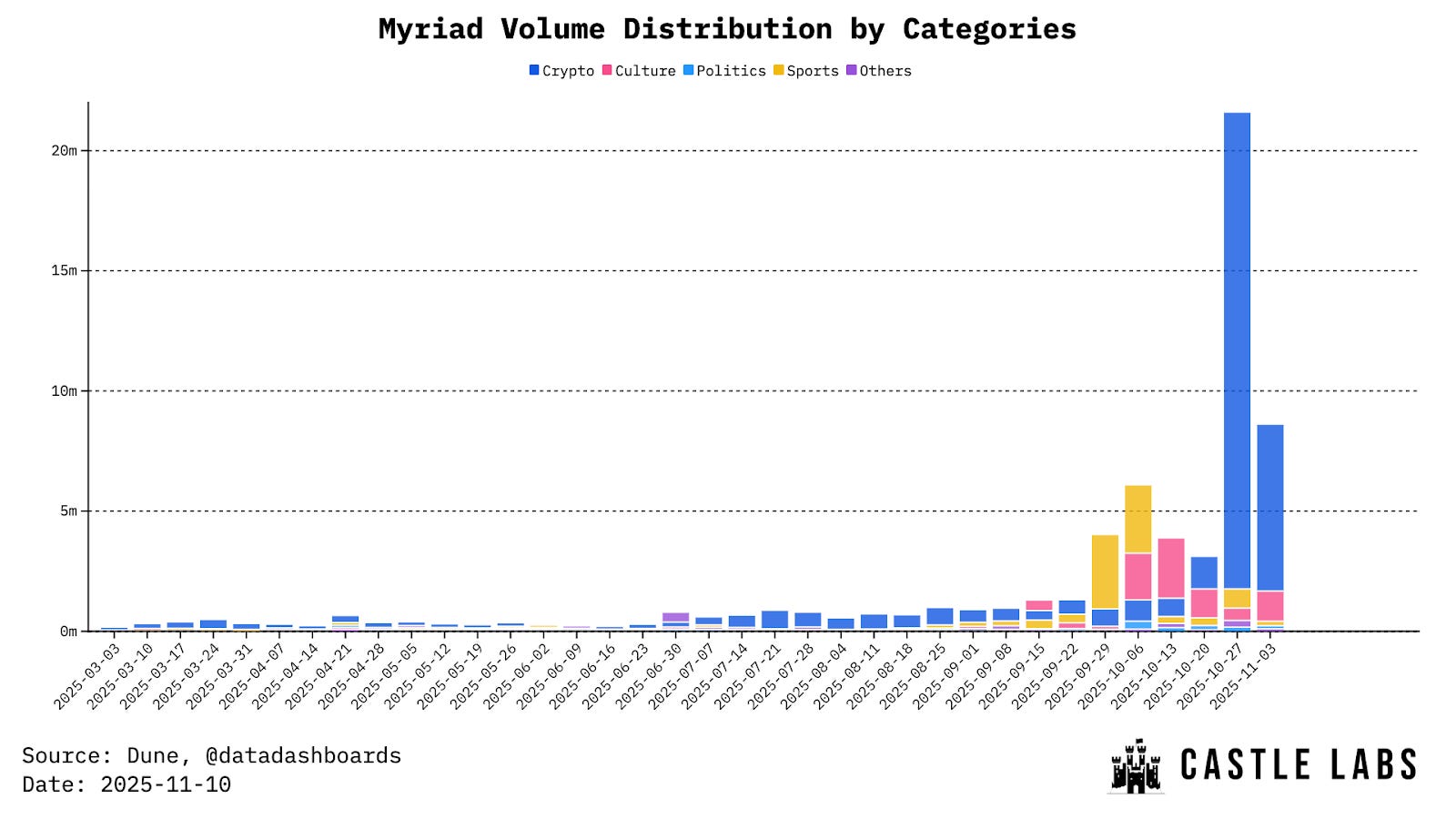

Myriad

Myriad was launched by Decrypt’s parent company, DASTAN, and went live on the BSC chain at the end of October 2025, already having a presence on Linea and Abstract since early this year. This move has led to an increase in its volume as it is serving a newer audience and contributing to their multi-chain expansion. It has achieved a cumulative volume of over $60 million with ~45k unique users over time. Most of this volume came in the last few months.

Market Positioning

Most of the myriad volumes come from the crypto category, followed by sports and politics. This is also justified by their continuous efforts to build products that particularly improve the experience around PMs in crypto.

The platform recently went live with Automated Markets during their launch on BSC, with Mandarin language support coming soon, in line with the demographics of the BSC chain. These markets are built autonomously every 5 minutes and settle through Binance APIs.

Additionally, Myriad supports external AI agent integration through its platform, such as Quantrix, Prediqt, and Tator. All of these agents are designed to make the prediction experience smoother and provide services such as sentiment analysis, news research, and chat interfaces.

Design Choices

Myriad supports only binary markets and sources liquidity from AMMs, ensuring liquidity is always available for trading. They utilise Binance APIs and official sources, such as a project’s X and Defillama dashboards, for market settlement. The events are either autonomously generated or curated by the platform.

Myriad charges a 3% fee on buy and sell transactions, a part of which is used to fund the protocol deployment and the rest is the protocol revenue.

Battle for Dominance

There is no doubt that PMs are an excellent venue for gambling and betting on real-world events. However, what primarily enables them to thrive are the “High-Impact / High-Interest Markets.” A great example of such markets is the market related to:

Sports

Politics

Crypto

Culture

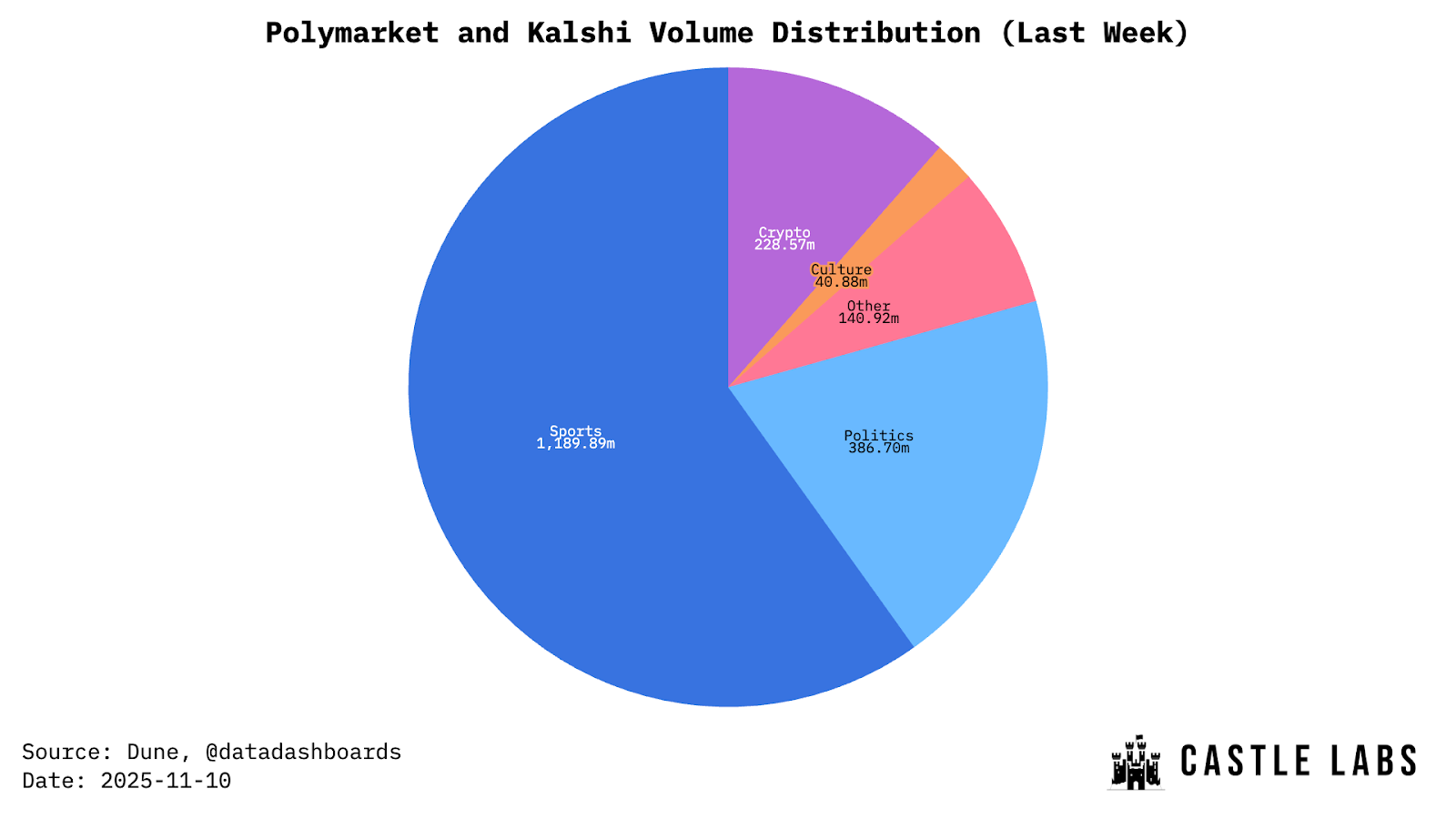

The sports betting industry is the hardest to penetrate due to high competition. Sports betting is expected to grow at a CAGR of 10% over the next 4-5 years, reaching a market value of $198 billion by 2030, up from about $108 billion in 2024. Kalshi and Polymarket are competing to capture a larger share of this niche category. While the other categories mentioned above hold similar importance, there are simply more people who are interested in betting on games they are watching, sitting on their couches. The growth rate of this sector also ensures that, if these platforms capture market share, they can generate recurring revenue for their businesses.

Based on volume data from the last week on Polymarket and Kalshi, the sports category was the major contributor, followed by Politics, Crypto, and others. This demonstrates how these major PMs aim to expand into traditional offerings and abstract the entire betting opportunity space into a simplified PM design.

At the same time, it is hard to replicate how the sports betting industry works and help users use parlays to gain leverage. A simple 3-leg parlay can abstract away 3 bets into one, and if all these bets win, it increases the payout, but if one of the legs fails, the payout will be zero. This is risky, but at the same time, it adds the intended leverage to sports betting. This implementation is challenging to perform in PMs, as MMs or counterparty would need to lock up the winning collateral in the market, even if the chances of winning such bets are negligible, resulting in high capital inefficiency.

The Integration Race

To hit that mainstream impact, PMs need to have the integrations with the best in the industry. Kalshi and Polymarket have recently been integrated into Google Finance, allowing users to access odds from both platforms. This integration will help Google answer users’ questions, such as “What will GDP growth be for 2025?”. Additionally, Robinhood announced its Kalshi integration in August this year, which helps their users to access and trade on the outcomes of NFL and college football games. Robinhood drives a lot of volume on Kalshi.

These integrations help PMs to reach an audience that would otherwise be very hard to reach, which is also their target market as they scale in the mainstream. Robinhood and Google Finance users are likely to be interested in them as a news source or for betting on these platforms.

Becoming a Hedge Tool

Every platform whose volume drives its growth needs to unlock use cases beyond its basic offerings. One such use case is hedging. On a perpetual DEX, such as Hyperliquid, users can hedge their spot holdings by opening a 1x-leverage short position on the same asset, or even hedge their airdrop by shorting a pre-market.

But what if you could hedge against real-world events?

The answer to this question is not straightforward and comes with caveats, but PMs can serve as a hedging tool under certain conditions, provided they have sufficient liquidity. Suppose a user with a stock position in a specific pharmaceutical company wants to hedge their position against a particular event, such as an FDA approval that could alter the stock’s dynamics. They can do that on a PM. This can be expanded to multiple use cases and markets.

The only problem is: Liquidity.

If a prediction market has sufficient liquidity to perform the hedge, it can be a valuable tool; otherwise, with a lack of liquidity, it won’t attract trades of sufficient size or, altogether, won’t attract any volume related to hedging.

Risks, Food for Thought, and Conclusion

Oracle Manipulation

Oracle are the core part of PMs and the “source of truth” for resolving markets. Every platform has its own way of curating this source of truth, with platforms like Kalshi relying on human oversight and Polymarket relying on optimistic oracles, such as Uma. The Kalshi approach might lead to this part of their system becoming a bottleneck for scalability. Still, it has worked fine till now. While the Polymarket approach has already revealed some of its weaknesses this year and in the past.

One advantage of the optimistic oracle approach on Polymarket is that users can simply disagree with the resolution during the 2-hour challenge period and can propose a resolution with a $750 bond. However, if their resolution is unsuccessful, they can lose this bond.

In some cases, these challenges may not fully meet user expectations. When the user disputes a resolution, the UMA protocol’s voters vote and reach consensus on whether the dispute is legitimate. This provides disproportionate power to UMA voters or whales, who control most of the voting power, allowing them to skew the market resolution in their favour.

A similar incident occurred during the Zelensky suit market on Polymarket, which reached a high volume; however, the market ultimately resolved in favour of UMA whales, which shows the weakness of such a system.

The Liquidity and Incentive Problem

We briefly touched on the liquidity issues in PMs and how their design can introduce different risks to counterparties (MMs). In this section, we will look into that problem in more detail.

Market making is more challenging in binary market setups, such as Polymarket or Kalshi, due to the differences between traditional markets and event contracts in PMs.

These are some of the reasons why MMs might not want to be involved:

High Inventory Risk: PMs move significantly in response to certain news. A market which is going well in one direction can go in the opposite direction at a fast pace, and at that moment, MMs, if priced in the opposite direction, can lose big. It can be mitigated through hedging, but these instruments often do not have such an option readily available for all the markets supported by PMs.

Insufficient Traders and Liquidity: Markets lack sufficient liquidity. Now, it might sound like the “chicken and egg” problem, but the market needs frequent traders or takers who can keep making MMs money on bid-ask spreads. Currently, PMs features several “long-tail” markets where there simply isn’t enough volume or trades, which doesn’t incentivise MMs to perform their operations.

Some products are actively working on solving this problem, like Kalshi, which utilises third-party MMs and also has an internal trading arm to maintain liquidity. On the other hand, Polymarket provide USDC rewards to compensate those who provide liquidity near the spread. For certain eligible events, the platform also pays holding rewards, which accrue when providing liquidity in specific event markets at a holding APY of 4%. Similarly, Kalshi reward its users on their cash and open position holdings with an interest rate of 3.5%. These rewards ensure that users are incentivised to participate in the market for the long term.

Ghost Markets and the Prediction Market Winner

PMs’ volume is strongly concentrated among a few market categories. Markets apart from these typically do not exhibit the same volumes and liquidity because fewer people are interested in trading in them, as they might lack the knowledge (or simply the interest) to trade in such markets due to their niche nature.

As shown in the data above, only a few selected categories account for the majority of the platform’s volume over the last week. It is also good to understand that the platforms position them to serve a niche category because the volume from other categories can be seasonal sometimes, and on the other hand, it helps them reach a newer set of audience.

This leaves us with a question: “Which PMs win at the end?”

To gain volumes and users, it is necessary to build the market everyone is looking for and wants to be a part of, a market which encompasses three characteristics:

High Leverage: This is not readily achievable in binary markets with a Yes/No question, as users can’t utilise leverage to target a larger payout. There are platforms like Flipr which provide leverage trading on prediction markets, but they often witness lower volumes.

High-Frequency Markets: Supporting a high volume of recurring markets increases the likelihood of user retention and converting visitors into loyal customers. Generally, having similar markets appear on the platform creates a great loop for users interested in such markets, and they continue to visit the platform. A great example of such a market is the daily strike markets for ETH or BTC prices.

High Market Outcome Value: If the market’s impact is substantial, it will drive significant volumes. It is particularly true for markets around elections and drug approvals, whose outcomes have a high impact on how the broader market reacts.

Closing Thoughts

“Prediction Markets are going to be the most dependable news source”

PMs are made to take two simple ideas to fruition:

Betting and monetising opinion in any niche market, whether it is economics, culture, politics, or sports.

Creating an abstracted source of news that isn’t dependent on a few polls or voices like legacy media, but on the real people with a bunch of opinions backed by their money.

The growth of PMs is linked to the two ideas above. It can also be correlated with their straightforward nature and their ability to represent the standpoint of thousands of traders in a single number or percentage.

Competition in PMs isn’t that brutal, and for someone who has particular needs, can stick to the following two options, or even only one of them in a few cases:

Choosing Polymarket: Looking for a liquid venue for predicting a future outcome in a decentralised manner.

Choosing Kalshi: Looking for a liquid venue for predicting a future outcome in a regulatory-friendly manner.

In the long term, it seems even more complicated for new participants to build prediction markets because, as the size of the winners increases, boosted by their recent funding rounds, helping them reach mainstream at an exponential speed, with a significant presence covering both the general and crypto audiences. Polymarket and Kalshi are more on the path to becoming a duopoly in the PMs space, and the only differentiators in their growth will be the integrations they have, stronger liquidity, and the regulatory landscape as they expand into multiple regions.

At the same time, the market remains open for anyone to put up a shop, build niche PMs, and work on a new primitive that might yet be undiscovered.

There are already a few products or experiments working in this direction:

XO Market: XO Market lets anyone create a market based on their conviction and opinion by setting up the market resolution path and seeding the initial liquidity. The platform has integrated AI to help market creators navigate the process smoothly and also set a creator fee for their market. The platform also made enhancements to liquidity sourcing, transitioning from the traditional LMSR and order book model. For outcome resolution, it utilises AI-powered resolution agents that autonomously handle a large number of markets, with an option for users to dispute the resolution.

Lightcone: Lightcone enable users to trade on the event’s impact. So, let’s suppose you consider that a drug is going to be approved by the FDA, and now you can bet on how the S&P 500 is going to perform after that. This creates a new category of PMs, called the “Impact Markets”, where participants are not interested in the outcome alone, but in the impact of it on a specific asset.

pAMMs (Prediction AMMs): Users can bet on markets that can be resolved onchain, such as TVL rises, governance approvals and decisions, ETH price increases, and much more. All these events are deterministic in nature and will have a single Yes/No outcome depending on the market definition, which can be verified and settled onchain. A more interesting aspect of pAMMs is that the ETH deposited in these markets is automatically staked in Lido and earns yield from wstETH while the market is resolving, thereby increasing the reward.

These are just two examples among many new emerging PM designs, which we will cover separately in the future.

The idea of gambling on everything might sound super addictive and contribute to the state of hyperfinancialisation and overstimulation. Still, if there is demand, there must be supply, so the platforms will continue to build the experiences users crave, whether it is trading mindshare with leverage on noise or predicting post engagement through Tweem.

At the end, the race of predicting everything has just begun.

If you want to get into the Prediction rabbit hole, here are some other great resources:

Prediction Markets: A World Truth Engine in Beta by Delphi Digital

XO Market: Transforming Predictions Into Conviction-Backed Markets by Blocmates

Dune dashboard by datadashboards

Technical Topology of Prediction Markets: Mechanics and Tradeoffs by Baheet

| A guest post by

|

Lovely report on PMs

Can tell you that majority of the problems we have with current PM products are already been solved.

Appreciate you mentioning XO Market, would love to chat more about our product and the solutions we bring

Incredible report. I loved the part on how companies can hedge on their own stock using PMs.

Would be interesting to understand the dynamics of the war against sportsbooks like DraftKings and regulators. Would regulations catch up to Kalshi since they're effectively becoming more of a sports betting platform (see: parlays just launched)? Or would platforms like Robinhood or Fanduel who own their own users take meaningful market share away from the duopoly?