Secrecy and Grand Designs

The DEX Arena

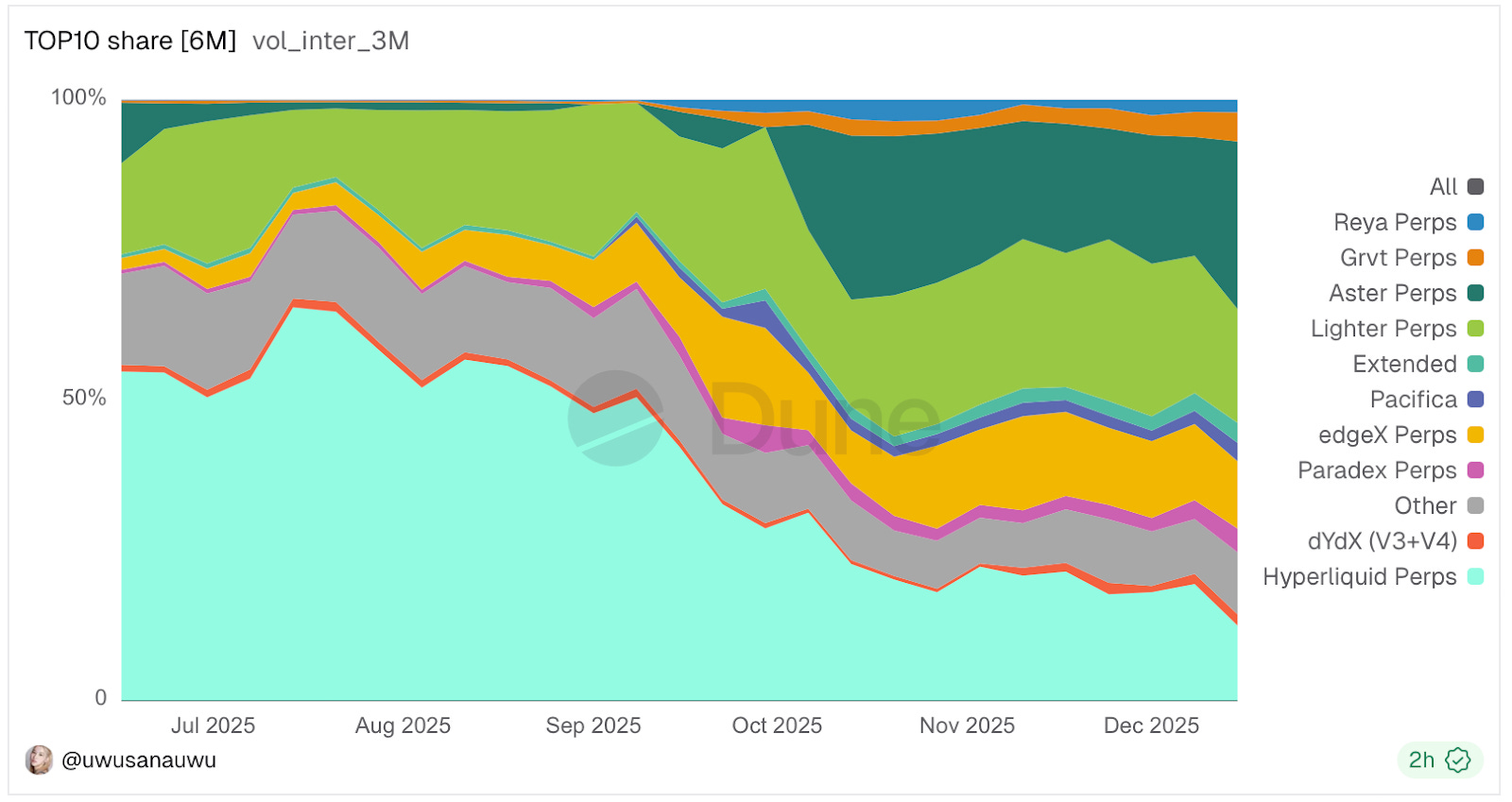

As 2025 comes to a close, the perp DEX war rages on, and it seems the mania is not ready to abate just yet. The most recent peak, measuring $78 billion in volume on October 10th, flattened in the following weeks, but tens of billions of dollars still flow despite the current depressing spell.

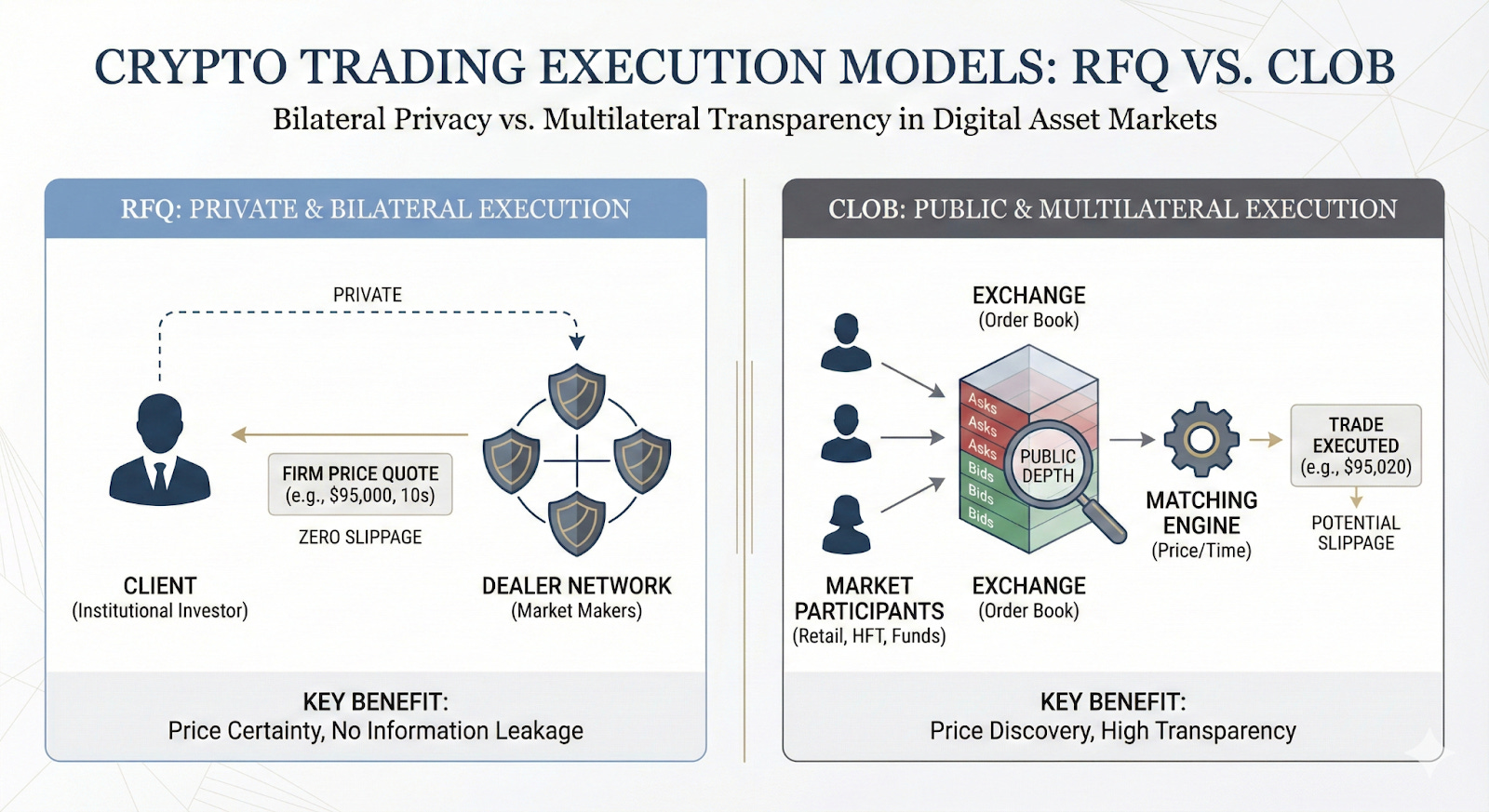

Each protocol boasts different mechanics, chains, visions, and UIs, but the most differentiating aspect lies in the order structure: CLOB vs. RFQ, or, put simply, public vs. private orders.

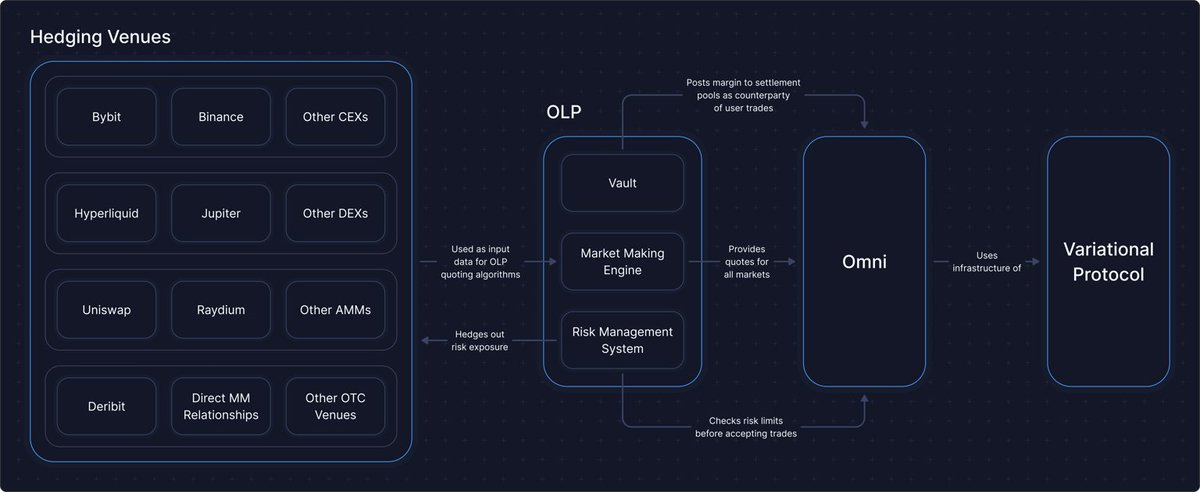

One ingenious protocol, Variational, has taken up the challenge of making the RFQ model accessible to all by turning their in-house engine, Omni, into a single internal market maker: the only counterparty to every trade. By doing so, Variational has effectively eliminated leakage to third parties, creating a novel model focused on revenue sharing rather than dispersing incentives to external actors.

Other perp DEXs, equally compelling yet functionally different, compete for the throne. Before we focus on Variational’s features, we will briefly examine the current DEX landscape.

The Holy Trinity

Since 2024, Hyperliquid has dominated both volume boards and online mindshare, owing to its spectacular TGE in late 2024. Once the market for perp DEXs matured, other contenders emerged, enticed by a vast liquidity pool willing to splurge.

Lighter and Aster recently ate into Hyperliquid’s market share, owing to the intense, somewhat artificial farming on those contenders. The feverish rush of new protocols flourishing on Hyperliquid will help it cement its position, helped by a hardcore fanbase whose pockets have been generously lined by Jeff.

Lighter and Aster represent two distinct approaches to dethroning Hyperliquid, yet both rely on models structurally and even ideologically different from Variational:

Lighter is a ZK-Rollup order book that prioritises cryptographic fairness. It uses ZK proofs to verify that its offchain matching engine respects price-time priority.

Aster, conversely, is a multi-chain hybrid often criticised for its inflated metrics. Backed by Binance (officially or not), it aggregates liquidity across chains and offers up to 1000x leverage alongside hidden orders that mimic dark pools.

While Lighter fights on verification and Aster on retail accessibility, Hyperliquid dominates through performance and the first-mover advantage. By building its own L1, Hyperliquid brute-forced the latency problem, successfully moving the entire CLOB onchain. Its custom consensus (HyperBFT) mimics the Binance experience by prioritising speed and throughput, while its HLP vault offers passive liquidity.

All three, however, are ultimately fighting for the same order flow. Variational removes the public aspect of price discovery. Instead of fighting for position in a visible order book (Lighter/Hyperliquid) or routing through a gamified liquidity pool (Aster), Variational users trade against a private, guaranteed quote.

The user’s intentions are effectively hidden.

A Protocol’s Craftsmanship

It is no secret that Variational has accrued quite a fervent coterie of followers, its cult-like band of patient traders who have been pounding the table for months, even though the protocol is still in closed beta. This was a gamble until one morning, some loyalists woke up to a 5-figure pre-airdrop structured as referral bonuses. Delivering significant returns on top of potential organic gains was a brilliant method to show the protocol’s value: see it as a tour de force, a challenge to other DEXs struggling to differentiate themselves.

A completely different design was thus created by Lucas and Ed, the founders of Variational, backed by stellar funding from Coinbase, Bain, Hack VC, Mirana, and Dragonfly.

Initially operating in stealth mode as a proprietary market maker for two years profitably, Variational later pivoted to build its own DeFi protocol:

The protocol’s founding insight is that you cannot fix exchange architecture by simply rebuilding the past. Variational rejects the standard fee model and the reliance on external liquidity, replacing them with the Omni Liquidity Provider (OLP), a single, internal counterparty that doesn’t treat users as prey.

Revenue is generated solely from the spread, not trading fees. Crucially, this spread doesn’t vanish into the pockets of third-party market makers. Instead, it recirculates within the protocol to capitalise insurance funds and pay rewards. By eliminating the leakage to DeFi’s middlemen, Variational ensures that trading volume reinforces the system rather than draining it.

Two innovations drive this resilience:

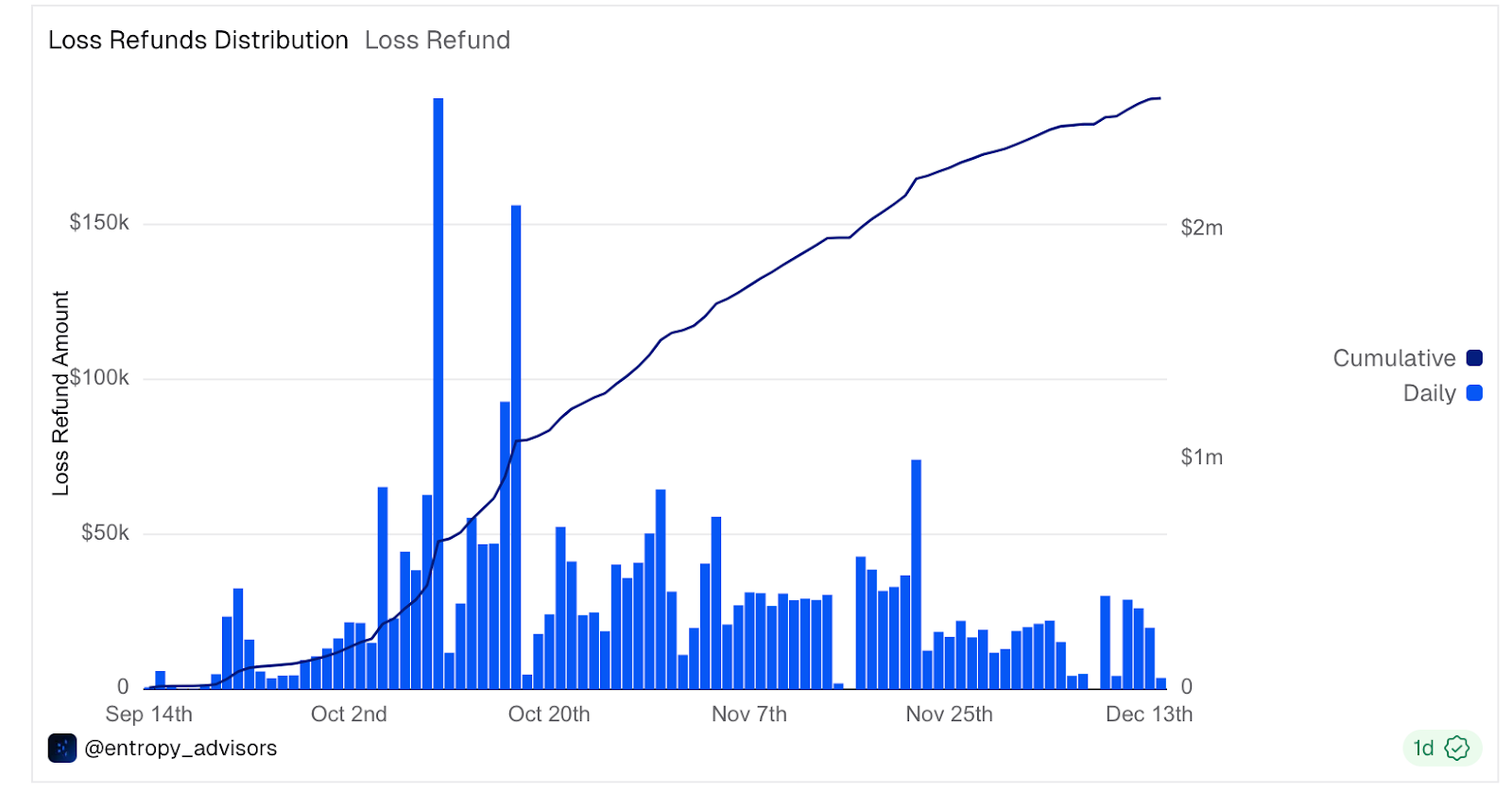

First, the Loss Refund Pool acts as an autonomous stabiliser, funded by one-sixth of the OLP’s spread revenue. This creates a self-reinforcing loop: trading activity builds the safety buffer, which in turn attracts more liquidity.

Second, the protocol employs Exponentially Weighted Moving Average (EWMA) settlement. Instead of relying on the instantaneous oracle price, Variational uses a smoothed, time-weighted valuation. This design prioritises accuracy over immediacy, effectively immunising the protocol against flash crashes. It explains why Variational remained solvent during the recent downturn.

They simply built a resilient product and let the users handle the marketing.

Against CLOBs, Privacy For All

The rationale behind Variational is that OTC trading should be provided to both retail and institutional users through the RFQ (Request for Quote) mechanism, which is dear to the quants behind the infrastructure. The CLOB infrastructure that has defined perps thus far has been entirely superseded by a private peer-to-peer system.

“As active participants in crypto OTC trading, we saw a number of risks and inefficiencies in the manual nature of bilateral trading”. This resulted in Variational’s vision: “that any two people in the world should be able to execute a customised derivartive contract to execute a customised derivatives contract using automated infrastructure seamlessly.“

For Variational, privacy is liquidity: large market makers hate trading on fully transparent CLOBs because they get front-run. The protocol is betting on RFQ because it protects the Market Maker (MM), allowing them to quote tighter spreads on larger sizes.

On Variational, traders do not post orders publicly. The MM (Omni Liquidity Provider (OLP) or Pro MM) sees this request privately. Because nobody else knows the trader is buying, the MM can provide a tighter price and larger size. They aren’t afraid of being front-run by a third-party bot because the third party doesn’t know the trade is happening. Once the quote is accepted, the trade is settled onchain.

For retail, the OLP is the sole counterparty to every trade. For institutional investors dealing in Pro, the OLP becomes one of many participants.

As per the docs:

Institutional derivatives trading currently occurs either through manual, direct channels (e.g., Telegram groups) or on platforms like Paradigm and Deribit.

Direct channels are highly manual, inefficient, and risky.

Platforms like Paradigm and Deribit lack customisation and only support options on majors (BTC, ETH, SOL), yet still process upwards of $1T in annual volume.

Pro automates the entire flow of institutional trades, from booking and clearing to settlement, and brings it onchain. Institutions can create completely customised derivatives, set specific margin and liquidation rules, escrow collateral in segregated contracts onchain, and use the Variational Oracle for pricing.

As Jung said, “the meeting of two personalities is like the contact of two chemical substances: if there is any reaction, both are transformed.”

The Arbitrum Connection

Variational is inexorably bound to Arbitrum’s ecosystem. The “Three Arrows of the Arbitrum Renaissance“ serves as the visible spearhead of a grand scheme to restore Arbitrum’s supremacy within the L2 ecosystem. The first arrow, DRIP, was a basic instrument that used treasury subsidies to incentivise capital to return to Aave and Morpho. It worked to inflate TVL, but it failed to solve the “vampire problem“ mentioned earlier (currently, nearly 70% of all USDC on Arbitrum sits idle in the Hyperliquid bridge, generating billions in volume that yields absolute zero for the Arbitrum ecosystem). Hyperliquid is a parasite on Arbitrum’s liquidity, and the Foundation endeavoured to redirect liquidity toward the chain.

Variational can be seen as a calculated response to this revenue leakage. By supporting Variational directly, the Foundation is attempting to build a path outside Hyperliquid, a DEX where settlement, yield, and liquidation fees remain onchain. The protocol’s OLP acts as a centre of gravity, keeping real money circulating within L2’s economy rather than bleeding out to an app-chain. Thus, a symbiotic relationship emerged between the Foundation and Variational.

Let the Numbers do the Talking

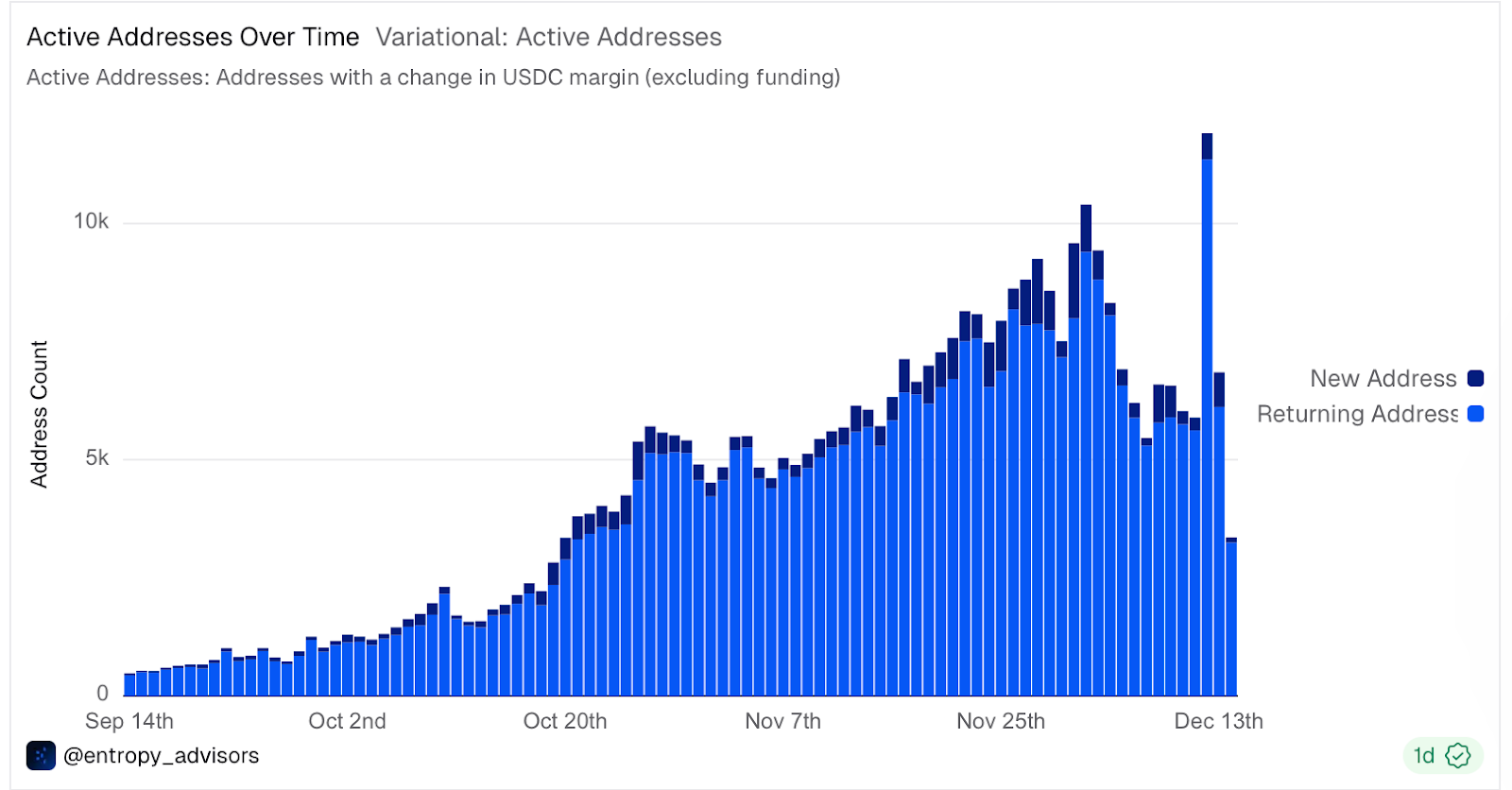

Variational has experienced explosive growth. After the 10th of October wipeout, one would have expected a severe decrease in metrics across the board. After having refunded close to $200,000 in losses to traders in a single day, the number of traders only increased.

Variational’s design has a socialist ring to it. It is the first DEX that refunds losses, pays massive referral rewards and grants platform credits, without even a point system in place.

The feature that retained most people’s loyalty is precisely the loss refund, which is automatic and instant. It was quite spectacular to see hundreds of thousands of losses being refunded directly to distressed traders, caught up in the liquidation cascade that annihilated many a whale and a shrimp alike.

Variational’s trajectory has shifted from linear structuring to parabolic expansion, an organic growth one rarely sees in DeFi. The initial proof-of-concept phase (Q2) scaled rapidly, with the OLP sustaining >300% APY. By Q3, the protocol demonstrated serious capital efficiency, supporting $6 in Open Interest for every $1 in TVL. November triggered the parabolic phase everyone is gloating about on CT. Following a flawless performance during the October mother-of-all-catastrophic-annihilations stress test, daily volume exploded to $1.1B, matching previous cumulative months combined.

With TVL doubling to $69M and OI hitting $397M in weeks, Variational (still in closed-beta mode) is already becoming a major player within the Arbitrum ecosystem and among DEXs.

A last important detail about Variational is the future release of Pro. Unlike the Omni product released to the public, Pro will be the most comprehensive venue for exotic products and derivatives traded among institutional users. In Variational Pro’s Peer-to-Peer RFQ model, the exchange doesn’t decide the market; the big boys do. Two parties (a hedge fund and a market maker, let’s say) agree on terms offchain, cryptographically sign the deal, and settle it onchain. Pro is basically a workshop for whales, a venue where they can order anything they like, buy any sort of asset, and create the most complex instruments known to man.

A Symbiotic Alliance

With the massive, almost daily creation of new L1s and L2s, competition is turning into a frantic manufacturing of chains to extract as much liquidity as possible before incentives die out and capital rotates. We have seen this tale unfold recently with Aptos, Sei, Sui, Berachain, or Plasma. Once the chain appears devoid of further upside, traders pull out and farm elsewhere, driven by a lack of novelty or an intolerable ennui with the hectic flows of crypto money.

Arbitrum offers a different approach: it posits that if something is good, it should work, and apps should leverage the efficiency and safety of a chain that has been tested numerous times. Arbitrum has a good reputation: it continues to attract innovative protocols (USD.AI is the new wunderkind of the chain) and caters to serious businesses (such as Robinhood).

Variational chose Arbitrum because, unlike Hyperliquid, it didn’t need a dedicated L1 to perform. It leverages Arbitrum’s innate qualities to deploy a top-tier product that satisfies day traders and whales alike. It is thus a universalist DEX, sharing its revenues with its userbase and encouraging loyalty through incentives everyone can understand: money.

Arbitrum will remain a blue-chip for all of us. Ostium, Variational, USD.AI, Aave, Morpho, Euler, Pendle, or Theo, oldsters and newcomers alike are thriving on Ethereum’s most reliable L2. Variational is bound to attract new capital given its versatility as both an institutional outfit and a retail darling, and the symbiosis with Arbitrum is likely to deepen, creating a virtuous circle.

Hyperliquid will remain a titan in DeFi, but new ideas, new actors, and fresh capital will always seek novel opportunities. The King has a new rival: Variational, which has already amassed its cult of fanatics.

Closing Thoughts

To classify Variational as merely another derivative exchange is to fundamentally misinterpret the evolution of onchain market structure. We are observing a pivot from the transparent, often hostile nature of CLOBS to the tailored, capital-efficient execution of RFQ systems.

By keeping quotes private between the trader and the OLP, the protocol effectively immunises users against front-running. It offers a solid trade-off: trusting one accountable entity, the OLP, rather than navigating a chaotic ecosystem of anonymous, often predatory actors. While effectively more centralised, this system provides structural safety in exchange for reliance on an internal market maker.

This transition represents more than a technological upgrade, for it is a maturation of DeFi liquidity to cater to institutions. By prioritising privacy as a function of liquidity, the protocol bridges the gap between the trillion-dollar traditional OTC market and the decentralised rails of Arbitrum.

As the market shifts its focus from meme incentives to sustainable, TradFi-grade infrastructure, the distinction between retail trial-and-error trading and institutional settlement is blurring. Variational’s parabolic growth metrics suggest that the market is already favouring venues that offer protection, refund mechanisms, and deep, private liquidity.

The architecture for the next cycle of institutional DeFi might happen on Arbitrum, as Ostium, USD.AI and Variational lead the new class of 2025. If so, we won’t trade memes anymore, but barrels of oil, gold, GPUs and Bitcoin on platforms built for Wall Street.