The Builder Momentum: How Chain Adoption Is Evolving and What It Means for Small Builders

written by @chilla_ct and @CryptoNdee ✍️

TLDR, Key Takeaways:

Base and Solana are leading in small-team experimentation and developer growth.

Arbitrum remains strong in institutional DeFi but is losing traction with smaller builders.

Base’s strength comes from its close relation with Coinbase and active developer outreach.

Solana wins in terms of raw user activity and community, although its data are harder to verify and compare.

Arbitrum’s grants are effective, but they require clearer positioning and improved support for builders or incubation.

Optimism’s approach is leading to a decline in interest for both users and builders.

This analysis examines the performance of Arbitrum, Base, Optimism, and Solana across developers, users, and community building. The goal is to understand which ecosystems small builders are most attracted to, as opposed to more established teams.

Developer Activity

When comparing ecos using @ElectricCapital data on chain activity, @Base and @Solana show linear growth in open-source repositories. Instead, @Arbitrum and @Optimism appear to have reached a plateau.

Developer counts tell a similar story. Full-time devs on Base are up 40%, Solana’s up 62%, while Arbitrum has dropped 34% and Optimism 18%. An interesting fact, and slightly out of context from this comparison, is that the overall number of crypto developers has dropped by 4% in the last couple of years, while the number of full-time developers has increased by 9%.

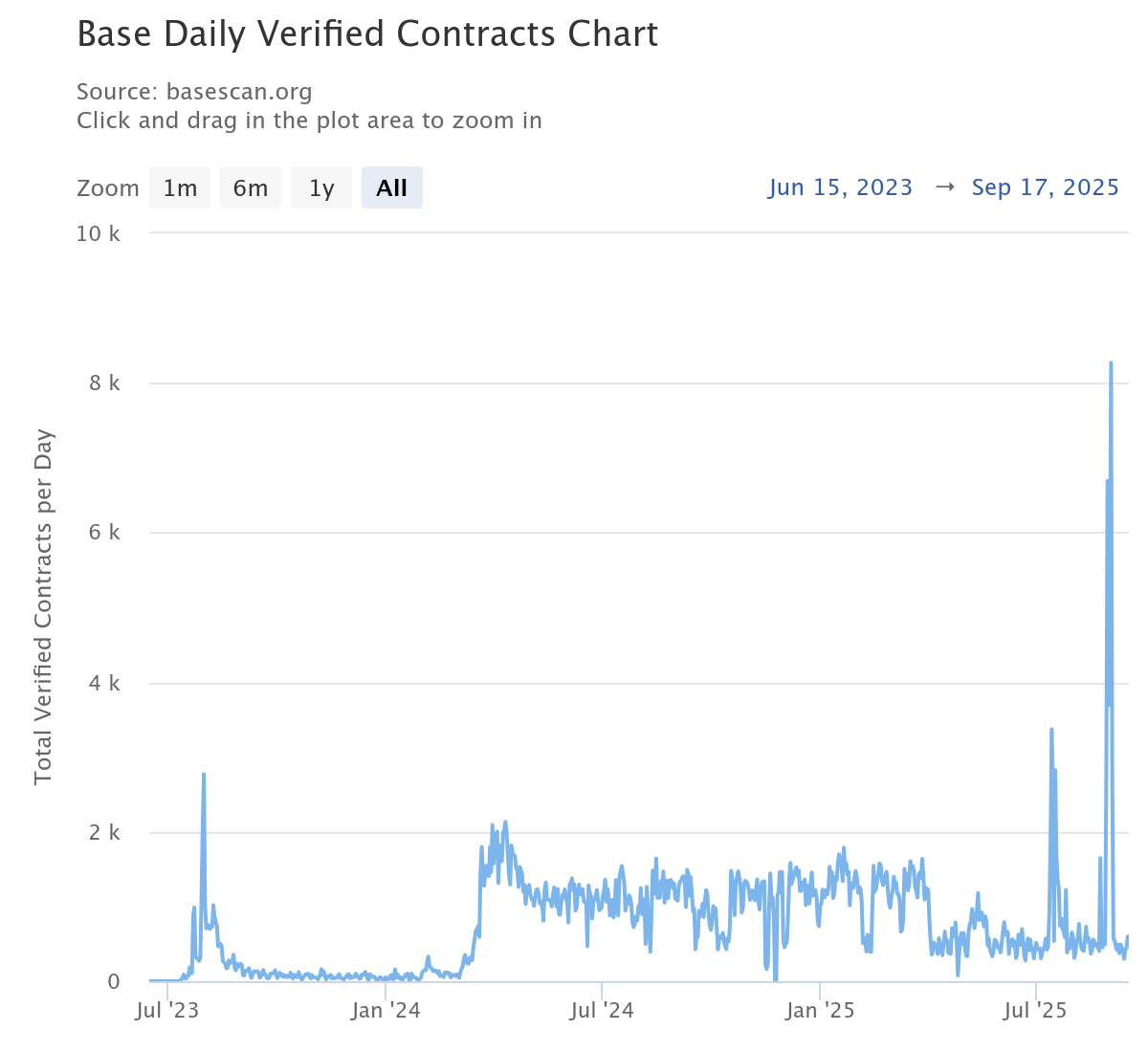

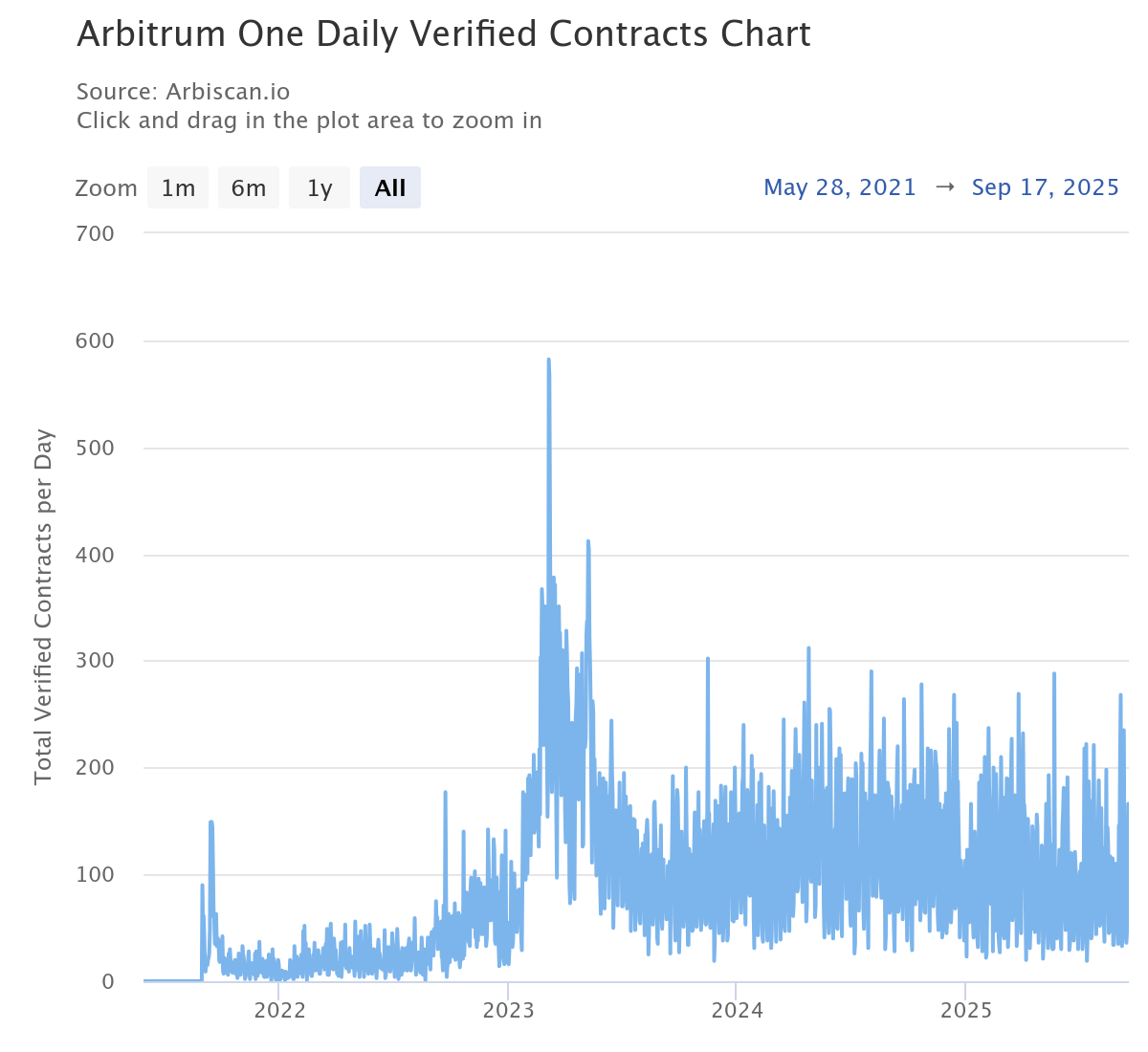

In line with this data, Base deploys verified contracts about three times more than Arbitrum or Optimism. However, we need to consider several key variables here. For instance, this is partly due to external campaigns, such as Coinbase’s Onchain Summer. Some spikes are artificial, as projects like Clanker deploy thousands of contracts simultaneously, and there is increasing activity from AI agents. Still, the trend is more solid than that of competitors. Arbitrum’s verified contract count has been steadily declining since 2024, however, while Base is deploying many new token experiments (now comprising nearly 50% of the total), Arbitrum remains anchored in DeFi protocols, indicating a clear difference in developers’ focus on these chains.

All in all, small teams are moving fastest on Base right now.

Base has captured momentum, while Arbitrum, though still home to leading DeFi protocols, has seen a slowdown in smaller teams launching experiments.

Solana’s open-source ecosystem remains the largest overall, despite its contract deployment data being less complete.

We could say that, at the moment, Base leads with small developers, Solana excels in ecosystem breadth, and Arbitrum dominates in DeFi.

Users

On the user side, Solana leads with about 1.5M daily active addresses. Base follows with roughly half, Arbitrum with close to 300,000, and Optimism with under 100,000.

If we then consider transaction counts, which in itself is a flawed metric given the possibility of spam or differences in value transferred, we see that Solana once again takes first place with around 100M daily transactions. Then comes Base, with approximately 10M, followed by Arbitrum, with close to 5M, and finally Optimism, at a considerable distance with 1.5M. However, we should remember that it’s challenging to evaluate how inflated Solana is by validators voting onchain, which typically accounts for 80%-90% of all transactions.

Even excluding those, it still maintains its lead.

When we then consider the bridging flows, each chain is down, except for Solana. Arbitrum has the largest flows, which is reasonable given its reputation as a DeFi chain, but more than half of the inflow is due to users bridging to Hyperliquid (net flow of $-5.9B, with inflows of $42B and outflows of $48B). For Base, the main netflow is -$4.7B to ETH. For Optimism, netflows are negligible compared to the other two. Finally, it’s interesting to note that the biggest net outflow for Solana is to Arbitrum ($214M).

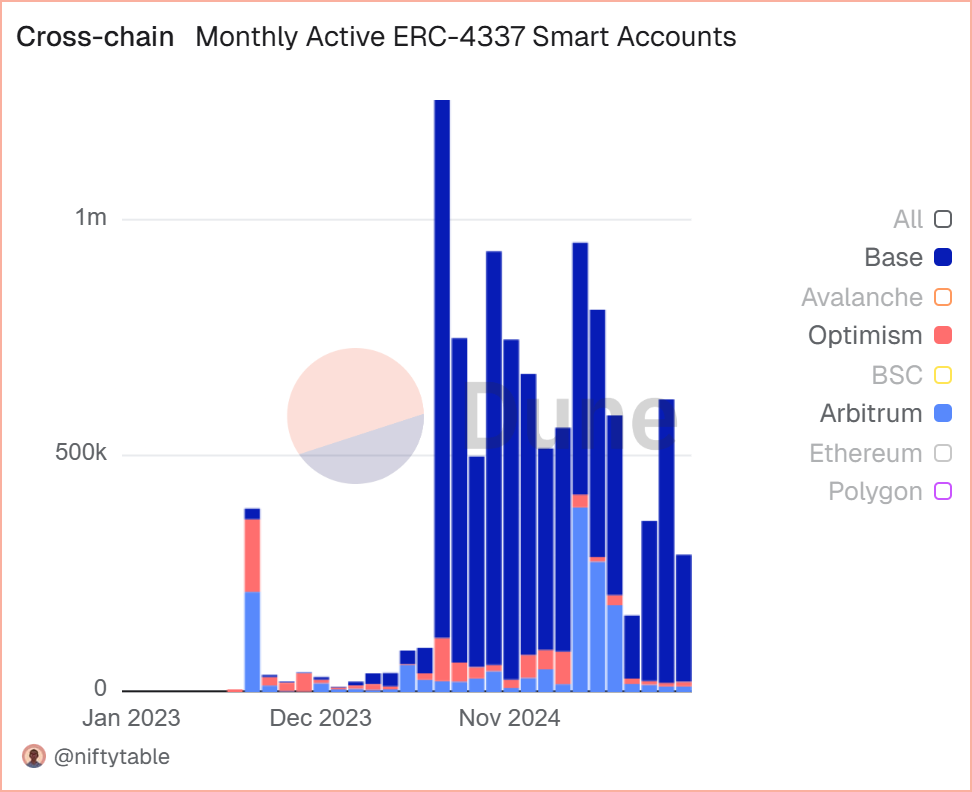

To conclude, we examined the number of smart accounts present on these chains, which generally indicates a better user experience. Base, again, is leading. They have the most monthly active smart accounts, the highest number of successful UserOps (proxy for transactions), and are earning the most fees. These numbers could be explained by Coinbase’s Base Account, which significantly simplifies the developer experience of integrating wallets into dApps. Solana, being non-EVM, plays in a different sandbox altogether.

Developer Relations

Finally, another aspect to consider when understanding an ecosystem’s reach and the typology of builders attracted is DevRel, which can be described as a two-way relationship between a technology provider (chain) and the developers who use its products (builders).

Currently, Base benefits from Coinbase’s reach, structured campaigns, and accessible SDKs. It offers identity services, such as basenames, and frequently incentivises programs that drive visibility, for instance, the Summer League rewards. Solana is different: it’s more focused on education, community, and strong tooling, with initiatives like Solana U and AI-assisted support. Arbitrum’s approach relies instead on grants, workshops, and the Stylus initiative that adds Rust and C/C++ support. Optimism takes a collaborative approach with its OP Stack and retroactive public goods funding.

While each network has a different philosophy and technical stack, they all invest heavily in documentation, SDKs, community engagement, and financial incentives.

Builder Survey

To get a broader picture of our qualitative analyses, we also administered a 13-question survey to our network of builders to gather a quick empirical snapshot of how developers view Arbitrum and other ecosystems. We received 22 responses.

Our questions asked participants to identify their protocol’s stage (emerging, growing, or established), indicate whether they were currently building on Arbitrum, and choose which chain they would deploy a new project on if starting today. We also asked respondents to rank the importance of factors such as liquidity, business development support, technical fit, grants, and community when deciding where to launch.

We do not believe that a sample of this order of magnitude can be exhaustive, but it can give an idea of what the direct opinion of experienced builders in the sector is.

After analysing the responses, we came to the following conclusions:

1. Launch decisions are liquidity/BD-led. Builders go first where users, liquidity, and BD surfaces are easiest to access. In this case, Base proved to be the survey’s top choice.

2. Distribution beats grants. “Grant availability” ranked last of the five launch drivers.

Respondents are more sensitive to distribution (co-marketing, portal placement) and

co-incentives, exactly the levers they say would change their mind to build on Arbitrum.

3. Incubation helps at the margin. Interest in structured incubation is solid (mean 3.68/5).

4. Awareness and fit gaps remain. A non-trivial slice hadn’t heard of the grant program we run with the Arbitrum DAO, or perceived Arbitrum primarily as a DeFi chain, or found the category fit unclear for their project.

Conclusions

The main focus of this analysis wasn’t the builder market as a whole.

Rather, it was to focus on small builders and the ecosystems to which they tend to be most attracted. Indeed, Arbitrum has recently seen some key wins. Having established products like Robinhood, as well as fast-growing projects like USDai, on its network, or already having strong products like Pendle, Fluid, and others among its ranks, wasn’t the basis for this analysis.

In fact, Arbitrum continues to land institutional-grade partners, which strengthens the top of the stack.

This is a crucial clarification for understanding why Arbitrum currently isn’t the go-to ecosystem for small builders.

Our analysis has revealed a consistent pattern: metrics of developer momentum (repos, full-time devs, verified contracts) and on-chain usage (DAU/MAU, throughput, smart accounts) show Base and Solana outpacing Arbitrum in attracting new builders and users. DevRel initiatives and responses to our survey support this narrative.

From a development tooling perspective, important steps forward have also been made with Stylus. However, all of this suggests that the primary focus has been on larger apps, while there has been less emphasis on smaller and disruptive teams.

We therefore hope this will help better understand the overall situation of some of the crypto industry’s leading ecosystems, and also hope that Arbitrum can grow even in those sectors where it currently stands out less than its closest competitors.

Feel free to check our full report for more info here: