The Builder’s View on Onchain Options

PLUS: Lighter's horizontal bet, Prediction Market regulation, and SECZ’s tokenised stock

Welcome back to another edition.

This week we’ll be looking at:

Onchain options, from the builders’ side: we sit down with those creating the options protocols of today to learn what’s being solved and what’s coming next

Lighter’s horizontal bet: why LIT has repriced, and whether its horizontal approach can start to close the gap with Hyperliquid.

Prediction markets under pressure: where real PMF is now running into regulatory, resolution and manipulation risk.

SECZ and issuer-led tokenisation: Securitize’s own public stock is now onchain, but now they need to go even further.

On our radar: Product updates from Variational, Spark, 1inch, Hyperliquid and Ondo.

Options from a Builder’s Perspective

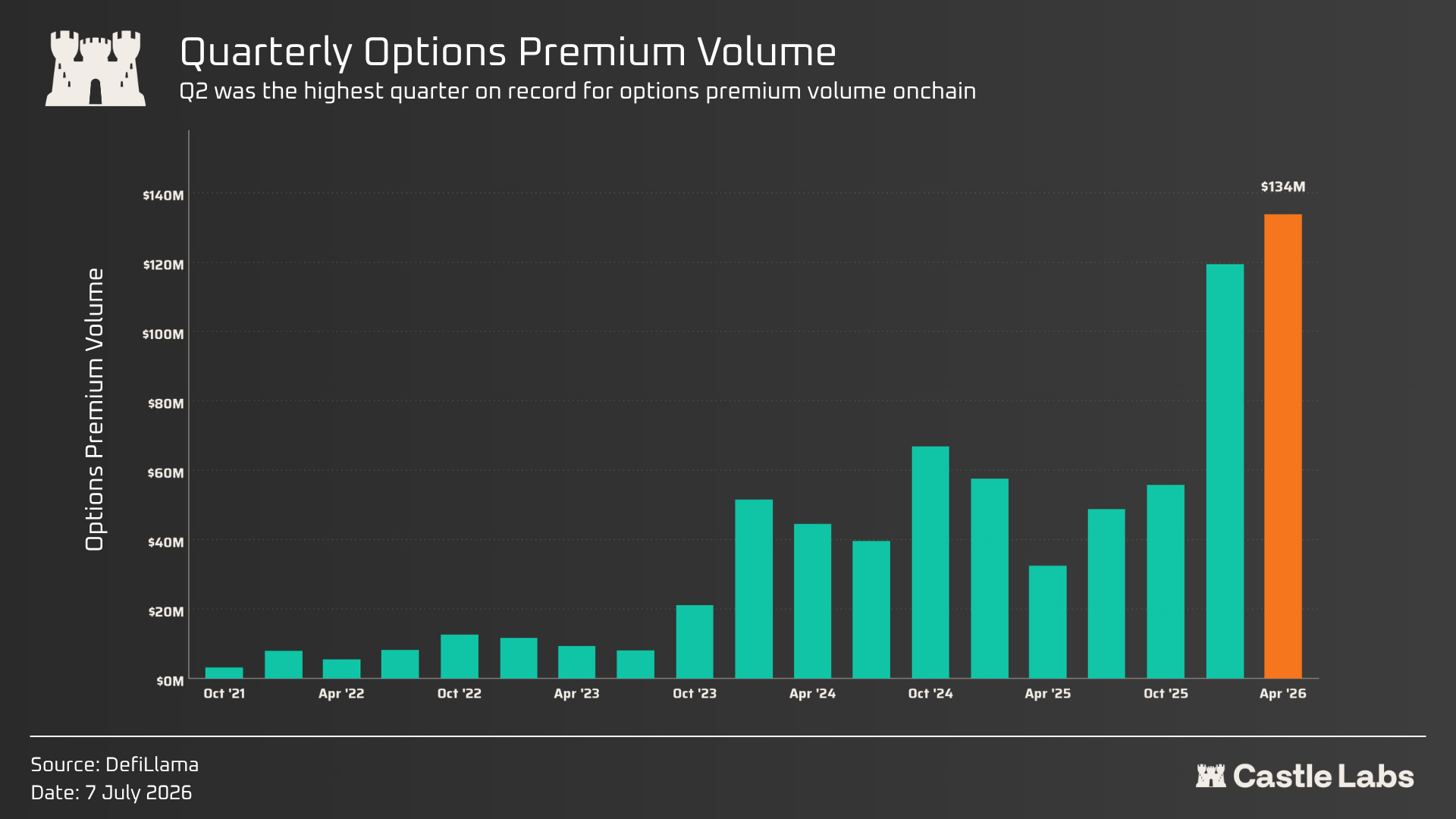

Options just had one of their best quarters in years.

Quarterly premium volume is at an all-time high, and options-linked tokens are beginning to catch a bid. DRV is up 37% from its June lows, while SYN is up more than 10x in a month after Synapse pivoted into Hyperliquid options via Hypercall.

This comes at the same time as Paradex launched its options product, and as Lighter announced plans to expand into options this quarter, shortly after announcing a new Robinhood Chain instance that will be accessible directly through the Robinhood Wallet.

We have had mini options cycles before, and 2021-2023 left behind a graveyard of protocols that never found consistent demand.

So is this time actually different?

We asked four teams building in this market why onchain options never saw the adoption curve of perps, what’s changed this cycle, where the real bottlenecks still sit, who’s actually using these products, and what would count as genuine success moving forward.

Here were the main takeaways:

The category spent too long trying to copy perps: Dan from Rysk argued that onchain options have often been framed as another exchange product, whereas users usually want a specific outcome: yield, protection, upside, income, or defined risk. His stance is: “options are not the product.” People don’t want an option; they want what the option does for them.

Liquidity fragmentation is a real issue: Perps concentrate activity around one market, while options split it across strikes, expiries, calls, puts, collateral types and volatility assumptions. That not only makes options harder for traders, but also for the venues. Guillaume from Panoptic highlighted the problem: market makers are not maintaining a single price; they are maintaining a whole surface that changes every time spot, volatility, or time-to-expiry moves. That is hard enough offchain, but onchain, it becomes much more complex.

The user still has to make too many decisions: Sean from Derive emphasised that most traders do not arrive wanting an “option”. They want to express a view on the market with the best risk/reward possible. If the product starts with an options UI, Greeks, expiries and strike selection, the audience is already narrow.

Prediction markets may already be the mass-market options interface: Devin from GammaSwap describes them as “binary options that mimic a call or put spread,” but with the complexity stripped out. Ultimately, he agreed with Dan: “Complexity is the enemy. Simplicity trumps everything,” even though they are solving this by building different products.

As expected, there are a multitude of gaps, with each builder’s perspective shaped by their own experiences building, but we do keep coming back to the same core themes: UX, demand, collateral, and education.

The demand for options is growing. Traditional markets show this across both retail and institutional channels, while recent onchain traction suggests the same demand can emerge when the right strategy is paired with the right asset and presented to the right user, with HYPE options being a prime example of this

The early iterations of option protocols focused on education, teaching users about the value of options. In the current forms, protocols are instead focusing on simplifying options and framing them in terms of their utility and what they can do, ideally reaching the point where users don’t even know they are using options in the back end, while fully understanding each outcome.

If this has interested you, make sure to check out our flagship report on The Renaissance of Onchain Options, published in collaboration with Block Scholes.

Read it here: https://docsend.com/v/sjv2g/onchainoptions

The Risk within Prediction Markets

In our recent report, we argued that prediction markets are binary options in all but name. They are event contracts with a fixed payoff: a market resolves yes or no, and the position either pays out or expires worthless.

While that framing is a useful comparison, it is becoming a regulatory problem.

This week, the European Securities and Markets Authority (ESMA) released a statement reminding firms of their obligation to assess whether newly offered products fall within the scope of existing intervention measures on binary options.

If prediction markets are treated as financial instruments, the authorities state that they are derivatives and, due to their binary payoff, may be prohibited from marketing, distribution, or sale to retail clients; in some member states, they may also fall under national gambling rules.

Prediction markets haven’t had the greatest public opinion of late, so they aren’t exactly helping themselves.

Here are two of the main areas of contention recently:

Resolution risk: Polymarket’s UMA-based dispute process is consistently in the news. The most recent example is the Strategy BTC sale market, where more than $85M in volume was tied up over whether Strategy had sold BTC by May 31. Strategy’s filing said it sold 32 BTC between May 26 and May 31, but the market resolved No after UMA voters backed the outcome with 98.6% of voting power, citing the sale not being publicly confirmed within the market window.

Data manipulation risk: Prediction markets also create incentives to manipulate the underlying data source, not just trade the event. Last week was another example, where Spotify removed more than 500,000 artificial streams from Malcolm Todd’s Earrings after the song’s rise to No. 1 was tied to bets on Kalshi. The market attracted around $3M in trading volume and had already settled before the fake streams were removed.

As PMs continue to grow adoption, their product-market-fit comes with increasing public scrutiny and the risk of regulatory intervention. Prediction markets have given retail a simpler way to speculate on events, but the same simplicity, along with their mass marketing, has made them a target.

This is definitely a regulatory space to watch, especially in the EU where we can expect heavier intervention.

If you are interested in prediction markets, we published an article last week looking at open and permissionless prediction markets. In this report, we trace their permissionless evolution, examine why permissionless curation failed in the first place and why permissioned curation won, and look at how current products are trying to restore the permissionless nature of PMs.

Read it here: https://castlelabs.io/research/prediction-markets-from-curated-platforms

Lighter’s Horizontal Bet

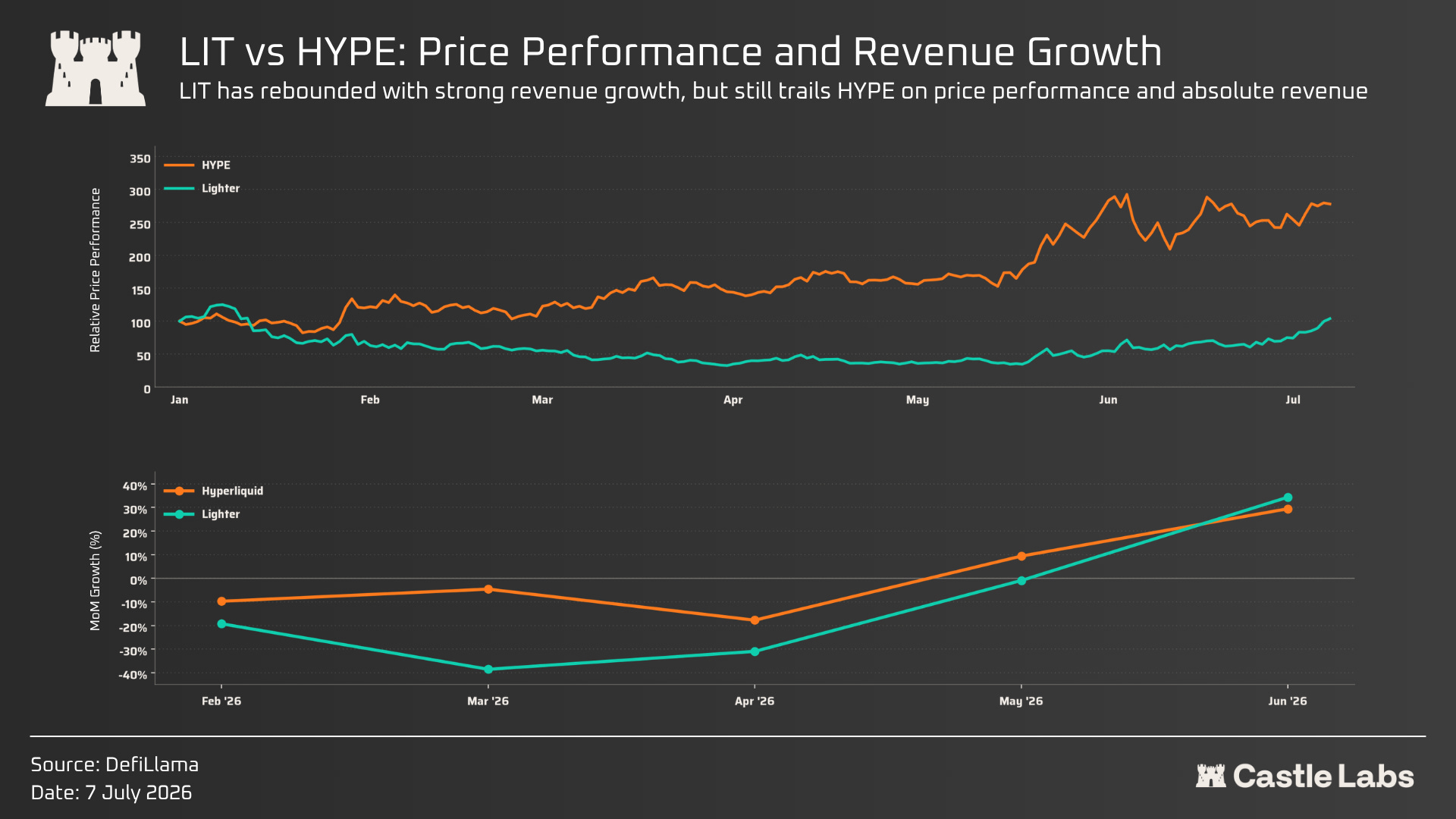

LIT has risen more than 80% over the last 30 days.

Their recent uptick is due to two major announcements:

The first was a tokenomics update. On June 30, Lighter announced that all repurchased LIT from revenue would now be burned, equating to 15.5M LIT, or roughly 6.3% of supply. The protocol is also targeting a 6% staking yield, which at the current staking TVL of ~125M tokens would distribute roughly 7.5M LIT.

The second was distribution. The newly launched Robinhood Wallet will offer perpetual trading with USDG as the quote asset through a Lighter instance deployed on Robinhood Chain. This gives Lighter access to one of the largest retail trading brands without needing to convert every new user through its own frontend.

This is one of the first signs of a strategic difference between Lighter and Hyperliquid. Hyperliquid is pursuing vertical integration: one chain, one execution engine, and one native liquidity environment via HyperCore, which distributors can tap into. Lighter is now taking a more horizontal route, deploying separate instances and trying to meet liquidity where distribution already exists. Whilst this will fragment liquidity and likely require new incentives to bootstrap this instance, it could well suit platforms and brands that want to ensure a separated and contained system.

LIT currently trades around a $650M market cap against roughly $72M in annualised revenue, giving it a P/S ratio of about 9.0x. HYPE, on the other hand, trades around $15.6B against roughly $830M in annualised revenue, or about 18.8x P/S.

Lighter is still much smaller and less proven, but the market is starting to price the possibility that this new approach could close part of the gap. For the first time this year, Lighter has posted a MoM revenue growth figure higher than Hyperliquid’s, at 34%, following consistent negative MoM growth early in the year.

The question now is whether this increase in valuation can be matched by increased activity and sustained revenue growth under this new distribution partnership, and in any other instances they may be cooking in the background

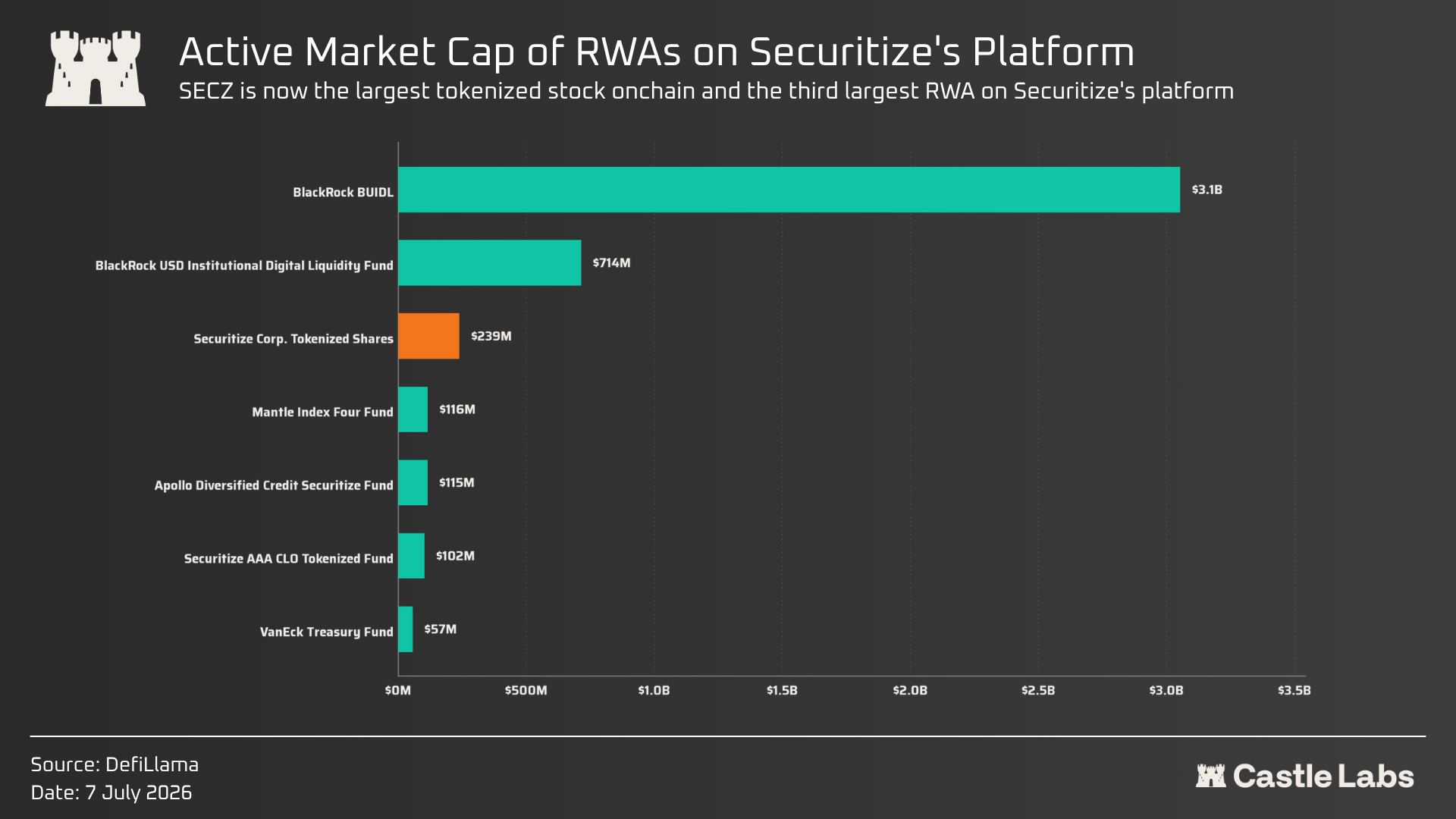

Securitize (SECZ) Opens as Largest Tokenised Stock

The same day Securitize listed on the New York Stock Exchange under SECZ, eligible U.S. investors were able to access a tokenised version of the same common stock through Securitize’s regulated platform.

For Securitize, this is a great marketing campaign. The company’s entire business is issuing tokenised products and running the infrastructure that supports them. By tokenising its own public stock at listing, it is using itself as the case study.

Securitize is a regulated tokenisation platform, transfer agent and infrastructure provider for tokenised securities. Its wider platform already supports roughly $3.5B+ in onchain market cap across a range of products.

SECZ has quickly become the largest tokenised stock by onchain market cap, at roughly $239M. Although access remains permissioned, only for eligible US investors, and subject to onboarding, KYC/AML checks, jurisdictional eligibility, etc.

Securitize now needs to go one step further.

It has shown that a public stock can be tokenised in a way that stays closely aligned with the offchain share. The harder part is proving that the tokenised version has a reason to exist. SECZ needs to become more than Securitize’s flagship stock issuance. It needs to become a working example of what tokenised equities can do differently:

be useful beyond holding

be accepted as collateral

support faster settlement or transfer workflows

expand access across jurisdictions where compliant

develop secondary liquidity or credit markets

That is what would turn SECZ from a strong marketing case study into a real shining example for RWAs, and Securitize is perfectly positioned to do it.

On Our Radar

Variational’s Swaps product: Variational introduced Swaps, a new market type designed to bring more TradFi assets onchain with tighter spreads, larger OI limits and near-flat carry costs. The markets will initially mirror traditional market hours, with 24/7 trading planned later. This is one of the more interesting RWA trading updates because Variational is not just trying to add more synthetic markets; it is trying to solve the underlying liquidity problem. To see the model succeed, it needs to deliver better execution than normal crypto-native liquidity can.

Spark’s stablecoin infrastructure role: Spark’s June update included BitGo institutional wallet access and the launch of its FX Layer on Uniswap v4, which we covered last week, opening with a $150M allocation and processing more than $70M in its first three days. It is also part of Robinhood Chain’s yield stack through spUSDG. We are now seeing Spark expand from a simple standalone yield product into new products and ecosystems.

1inch packages RWA routing: 1inch Business is now offering tokenised RWA and stock routing as a single API integration, bundling compliance filters, pricing feeds and liquidity access. Most wallets and fintechs will not want to build issuer relationships, compliance screens, pricing feeds and routing from scratch. So if tokenised equities become widely distributed, much of the value may reside in the routing layer rather than in the asset wrapper itself.

Hyperliquid’s VALR integration: VALR, Africa’s largest crypto exchange by trading volume, is using Hyperliquid as the onchain infrastructure layer to bring perps to its users. This is the first centralised exchange to do so with the Hyperliquid stack and serves as a useful counterargument to Lighter’s horizontal model, which spins up separate instances for more traditional clients.

Ondo’s execution-quality argument: Ondo compared weekend execution costs for tokenised CRCL, claiming a $100K trade cost $25.55 on Ondo Global Markets versus $1,168 elsewhere. It’s clear that tokenised stocks will not win only by existing onchain. They need to prove they can offer better access, settlement, liquidity, and execution than the offchain version.

Don’t forget to join our Telegram channel for the latest updates from Castle and all our research: Link here

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn’t guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.