USDai: Fuel for the Digital Age?

GPU backed loans

Introduction

Since 1955, when John McCarthy coined the term artificial intelligence, the industry has gone from a fantasy feeding the fantasies of Hollywood screenwriters to a product available to anyone with a computer and an internet connection. In films, AI is often portrayed as an adversarial entity, but in real life, it serves as an ancillary to everything we do, create, produce, and build. It has become an ubiquitous part of our lives

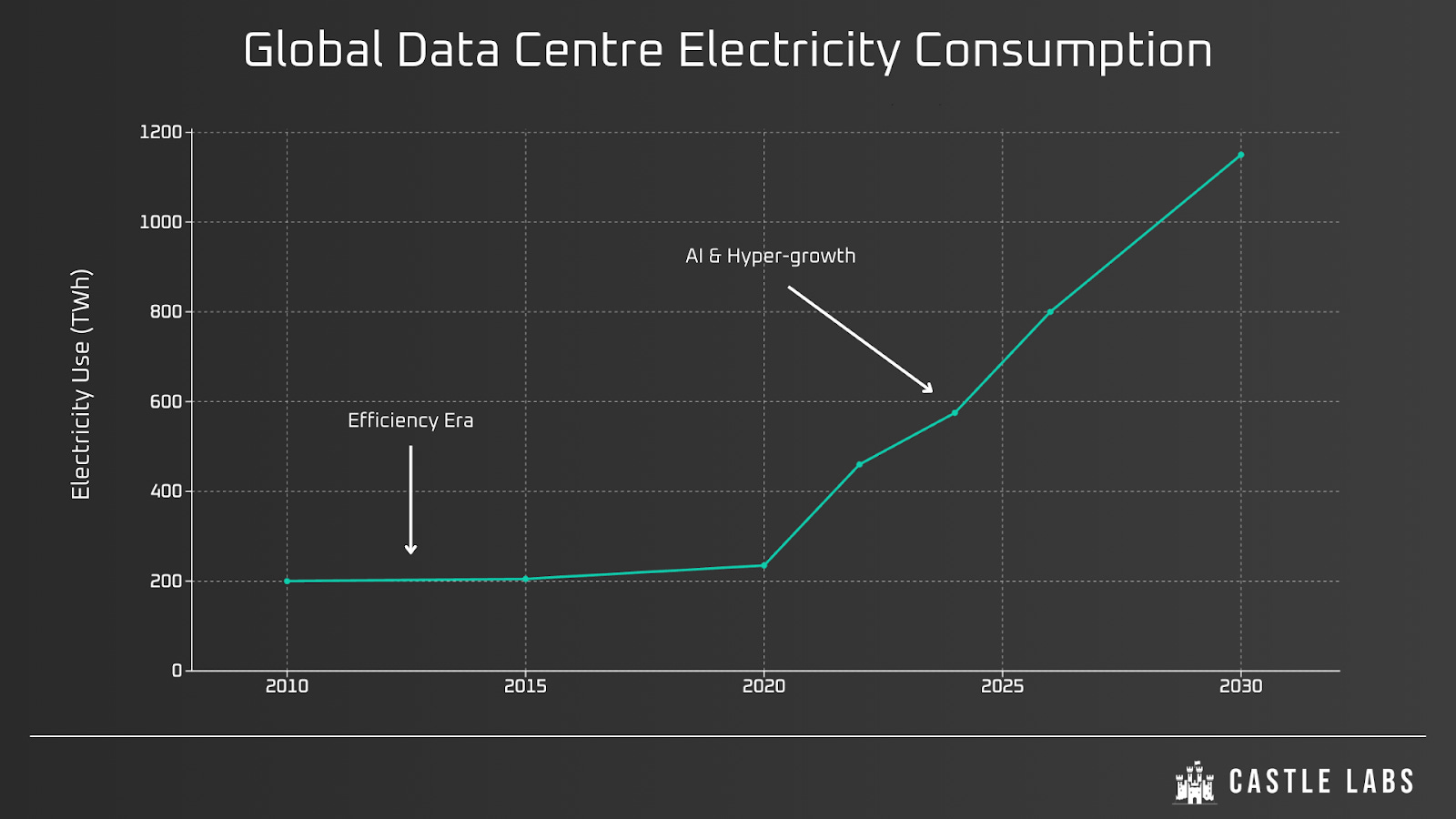

To sustain such a marvel, we need two things: money and energy. Money can be printed, energy needs to be produced, and AI requires a tremendous amount of it. It is so hungry that corporations covet small modular reactors (SMRs) to feed their data centres. Today, approximately 5% of U.S. electricity is consumed by data centres. GPUs are at the core of the AI revolution, and on top of being energy-intensive, they are quite costly.

To finance this demanding technology, we have to be agile and inventive above all.

The traditional banking system is often cumbersome and still does not fully understand the mechanics of AI. A bank might not appreciate the value of a GPU farm, just like they didn’t see the investment thesis of Bitcoin back in 2010.

One way to support AI-native companies is to leverage the idle money stuck in crypto. Stablecoins, the most promising DeFi product, are one option, but they come with quality and safety thresholds.

The first iterations of the stablecoin relied on dollar reserves and crypto collateralisation, exemplified by USDT and USDC.

Stablecoins offer the valuable advantages of instant transfers, low fees, and transparency, whereas bank transfers are often a trial by fire for larger borrowers. Progress is therefore sparked not so much by offer as by an overwhelming demand for liquidity.

If the dollar is to be replaced by gold, silver, or Bitcoin, it is easy to imagine other forms of collateral for consumer credit, stablecoins, mortgages, or business loans.

The prize for the most interesting stablecoin model undoubtedly goes to USD.AI. This novel infrastructure, functioning as a bank for high-tech actors, provides GPU-backed loans to AI companies to fund their operations. In return, USD.AI mints a native stablecoin backed by said loans. Traditional banking lags behind in meeting its clients’ needs, and it is precisely this niche that USD.AI intends to occupy.

Funding the future entails developing new ways to raise funds. In a hypercompetitive environment such as AI, tech, or robotics, money and energy determine a project’s outcome.

Amid unfettered, exponential growth in AI funding, USD.AI recently announced the launch of its governance token, CHIP.

This report will discuss the mechanics of USD.AI and its place in the AI industry. Consequently, both USDai and CHIP will be studied within the context of USD.AI’s rapid expansion. It is indeed currently difficult to invest in USD.AI. The demand for AI-adjacent financial infrastructure is overwhelming, and deposit caps remain closed.

Here’s everything to know about USDai.

What is USDai?

USDai, as its name suggests, converges between USD and AI infrastructure.

The protocol provides access to credit for those with the GPU infrastructure required to run AI models. It helps companies collateralise their GPUs and obtain loans against them, up to 70% of the value, or, in DeFi terms, 70% LTV.

This unlocks a new niche, as AI companies previously did not utilise GPU-backed loans. With the unprecedented rise in chips’ prices and the geopolitical wars surrounding their manufacturing and trade, GPUs are becoming a commodity increasingly harder to obtain, both for retail and corporations.

Given the USDai emergence, companies can obtain loans against the hardware, invest the funds in infrastructure development, expand, and payback the interest. Now, coming to the needle of yield, the interest paid by these borrowers is shared with lenders, meaning the users who minted USDai in the first place.

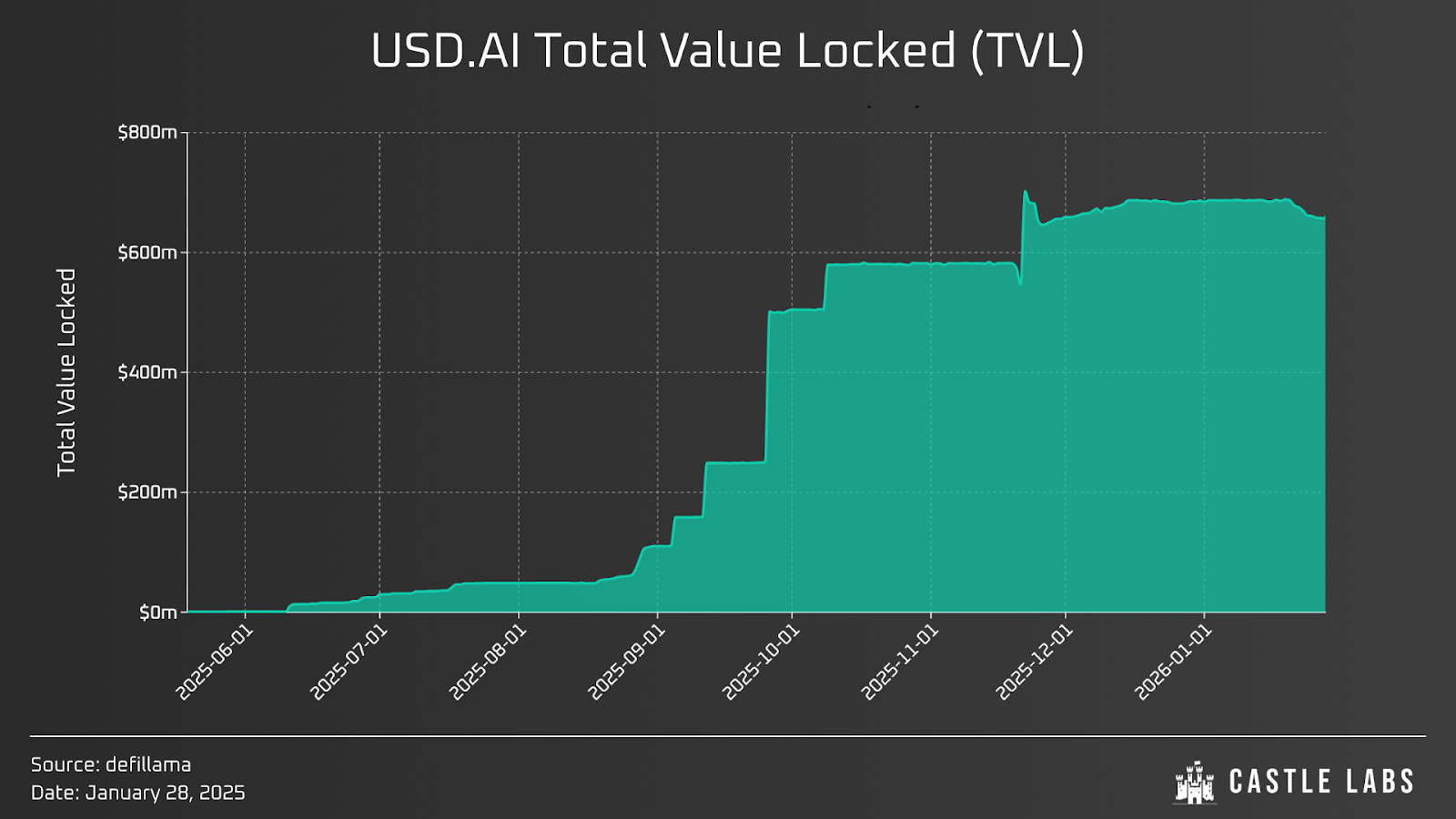

The protocol’s unique positioning and the points program (Allo) attracted good flow, leading to the value locked reaching ~$650 million. The demand for depositing can also be contextualised as caps raised as high as $75 million were filled in just under a minute.

Providing these loans at scale is not yet feasible because it requires extensive processing (as discussed in the sections that follow). Hence, most of the current TVL is backed by U.S. T-bills, and only a small fraction of the yield comes from GPU-backed loans. The team, however, stated that in the future, 60%-80% of the yield would come from those loans.

On the bright side, the team is consistently working to secure new borrowers, including the recently approved $500 million financing for Sharon AI, and currently has $1.2 billion in loans in the pipeline. Users can expect slow deployment of these loans throughout the year.

To us, it is yield; to AI companies, it is their expansion and a move away from dependence on banks and private credit firms.

How do GPU-backed loans work?

USD.AI streamlines GPU acquisition by minimising the upfront capital burden for borrowers, who often struggle with reticent banks. The process is designed to bridge the gap between manufacturer requirements and operational deployment, a gap that the current banking infrastructure does not necessarily address.

Borrowers can secure $1 in GPU hardware for an upfront cost of $0.20–$0.30.

This initial deposit serves as a down payment to the manufacturer. While USD.AI does not provide purchase order financing, it offers 30-day payment terms.

Once the deposit is verified, the chips are manufactured, shipped, and installed. Upon successful installation, the protocol releases the remaining 70–80% of the required funds to finalise the acquisition.

According to Samuel McCulloch, growth lead at USD.AI, three criteria are important for the loan origination.

Which chips do the borrowers intend to purchase, and how many?

USD.AI analyses the specific chips being purchased and their market price. The protocol identifies and avoids inflated prices caused by unnecessary intermediaries.

The compliance of the borrower’s jurisdiction

USD.AI ensures that all legal contracts are enforceable and valid in the borrower’s jurisdiction before lending.

Who is buying the compute?

The interest rate applied to a loan is directly tied to the credit rating of the “offtaker” (the entity purchasing the computing power)

If the compute is being purchased by a government entity or a “Hyperscaler,” the borrower qualifies for lower interest rates, while on-demand or “burst” rentals carry the highest interest rates because they lack guaranteed payment structures, despite their potential for higher short-term revenue.

The loan is disbursed in stablecoins, limiting crypto as a topic of discussion in the sales pitch. USD.AI is acting as a bank, despite its crypto-adjacent qualities.

Finally, once a loan is originated, USD.AI offers significant flexibility by charging no fees for early prepayment or defeasance.

This process and the legalities surrounding it add time to the issuance of these loans, which has led to the majority of current token backing being U.S. Treasuries.

CHIP: The Governance Token behind USDai

CHIP, a reference to the heart of GPUs’ components, is the governance token of USD.AI.

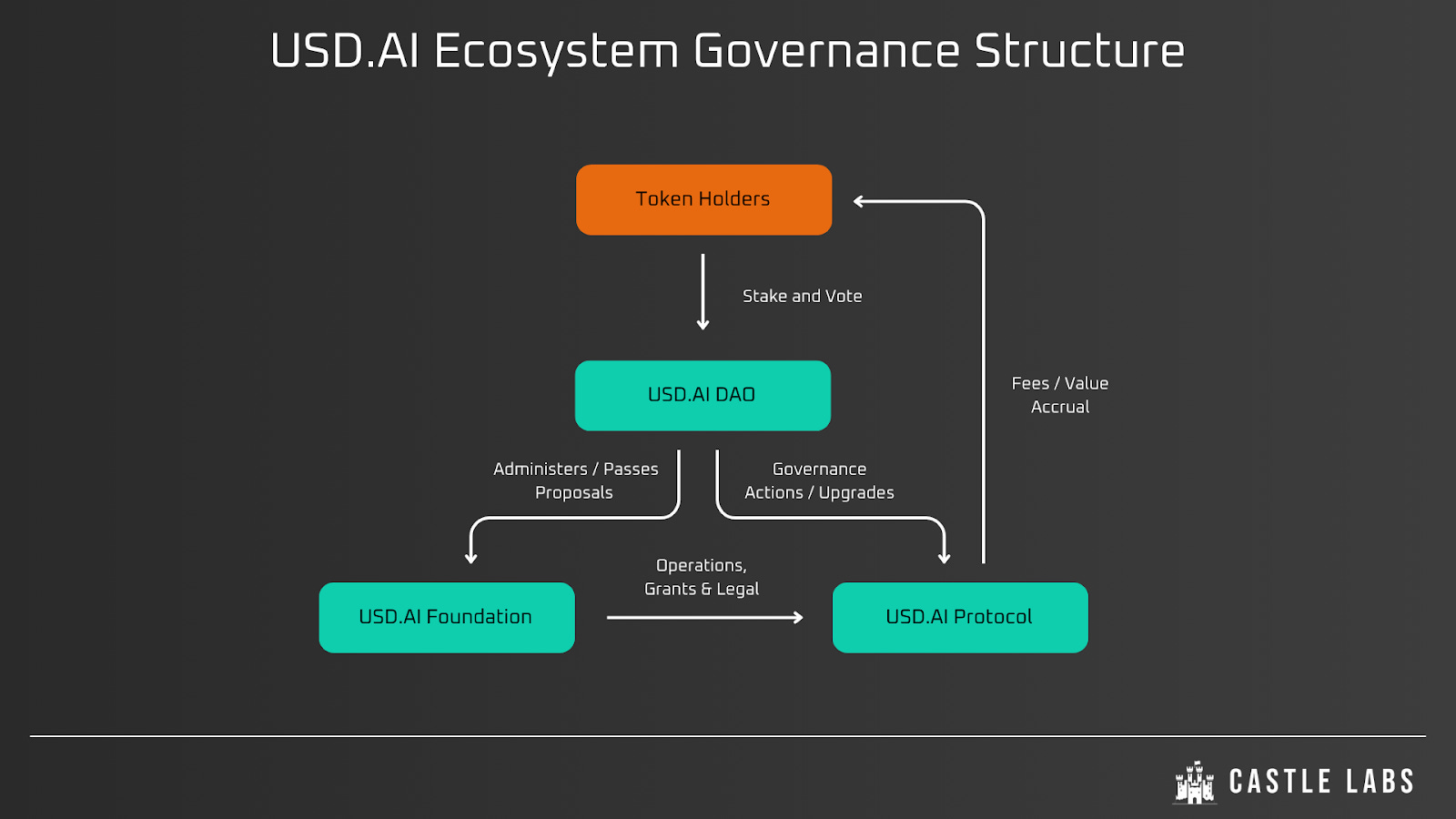

To oversee tokenholders’ interests, USD.AI announced the creation of an offchain steward dedicated to supporting the USD.AI DAO, which in turn receives support from the Foundation.

The Foundation is required to act at the direction of CHIP holders and to execute governance decisions approved through the onchain voting process.

Tokenholders ultimately determine the lifecycle of the company’s deals, selecting curators, adjusting loan parameters, voting on new assets, and supporting external builders and founders, in a manner similar to other DAOs.

CHIP is a peculiar governance token because it aims to “bridge onchain and offchain activity.” By voting on governance matters onchain, the DAO is bound by the vote; however, the Foundation is an offchain entity that supports both protocol development and the implementation of DAO decisions. As the legal and operational arm of USD.AI, the Foundation operates as an executant, bringing to life the will of the DAO’s members, who primarily vote on three matters:

DAO Rights: The members vote on collateral parameters, fee structures, and the creation of new asset types.

Treasury Governance: Tokenholders have a say in how the Treasury is managed; Treasury funds may be allocated to grants, ecosystem development, and protocol initiatives.

Insurance Module: Staking CHIP in the insurance module protects sUSDai holders against bad debt.

Another notable feature is the Quality Execution Value (QEV) model, a novel liquidity primitive within the USD.AI ecosystem. The CHIP token introduces a priority mechanism among borrowers: if multiple borrowers or projects compete for the protocol’s available capital, holding or staking CHIP allows a user to bypass the queue and gain priority access to funding.

It is, however, unclear whether CHIP will provide a future revenue stream for token holders. Although CHIP provides direct voting rights regarding Treasury activities, only sUSDai holders will receive the fees paid by borrowers.

It is therefore important to distinguish between the two tokens:

sUSDai, a native stablecoin, collect the direct fees paid by hardware borrowers for the token holders, whereas

CHIP, the governance token, exerts governance authority over the Treasury and influences the protocol’s underlying economic parameters described above.

Since the CHIP launch is imminent, it is important to ask how the token will accrue value as the protocol grows. While obtaining governance rights is one end of the spectrum, the other concerns the financial incentive for holding the token over the long term.

As the team stated that with $1 billion in origination, they will earn about $30 million in revenue; however, the question remains: will CHIP holders receive any exposure through that?

Food for Thought

The rise of AI is no longer a speculative investment. The current leaders are worth trillions of dollars, and they continue to raise hundreds of billions among banks, States, corporations, and billionaires. The world is rapidly changing, perhaps faster than we are, who may become aliens to a technology that eludes its very creators.

The premise of USD.AI is not simplistic. The model they pursue is acutely contemporary with our needs, well thought out and timely. If banks cannot keep pace with founders’ needs, other financial actors must step in to fill the gaps and provide the funds required to sustain AI development. Like the announcement said: “If you wait for TradFi, your GPU is already well past half its lifecycle.” AI cannot wait.

USD.AI has already proven its worth. $1.2 billion has been approved in facilities to QumulusAI, Sharon AI, and Quantum SKK. This represents real-world capital deployed to fund real-world companies; the link to cryptocurrency is tenuous, only evident in the way loans are disbursed.

The first-mover advantage is obvious: USD.AI has identified a need, and its loans meet the liquid requirements of the demanding AI industry.

Regarding the protocol itself, CHIP provides leverage to holders who want to control the business lifecycle. If the DAO is directly bound by the onchain decision-making, the Foundation safeguards the offchain interests of the protocol through legal and operational backing. But at the same time, the value accrual for the token from the protocol’s growth is in question.

It goes without saying that USD.AI plays a unique role at the intersection of Web3, banking, AI, and crypto.

By integrating these sectors, it addresses the needs of the most important businesses of our era, which are often misunderstood by financial institutions.

| A guest post by

|

Really solid breakdown of how GPU collateral changes the game for AI financing. The insight about banks not keeping pace with AI founders' needs hits hard because I've seen multiple projects struggle with that exact gap. What makes this particularly intresting is the 70% LTV on hardware that traditonal lenders would barely consider as collateral. The risk profiel here is way more nuanced than standard asset-backed lending.