Institutions Are Here, and This Is What They Want

Your girlfriend is gone, the rent is due, the bills are stacking up on the kitchen table, and selling your grandpa’s watch to buy the dip has never been so tempting. Your coins, dubbed “the future of finance”, lose 20% a day. The last phase of grief has passed; you have given up. What changed, you ask yourself?

What used to work before, well, now just doesn’t. No one told you it would be like this when institutions came. Oh, you invested in a revolutionary Proof of Liquidity consensus mechanism? It doesn’t look good.

While you experience the horrors of a bear, J.P. Morgan is building Kinexys, a bank-led blockchain for its institutional clients. Have you never heard of Kinexys? And BUIDL, from BlackRock? How about Ondo’s OUSG, or the tokenised money market funds developed by Franklin Templeton?

Those products have guaranteed APRs of around 4-5%, are virtually risk-free, and are tokenised or digital versions of treasuries. Moreover, their combined value is close to $25 billion. Quite the contrast, isn’t it?

Times are changing, and the data makes it evident. If the value of onchain institutional products is rising, the intrinsic value of the tokens we have become accustomed to so far is decreasing, despite widespread interest in crypto worldwide. This requires adaptation and a change in framework: users need to shift away from gambling to investing.

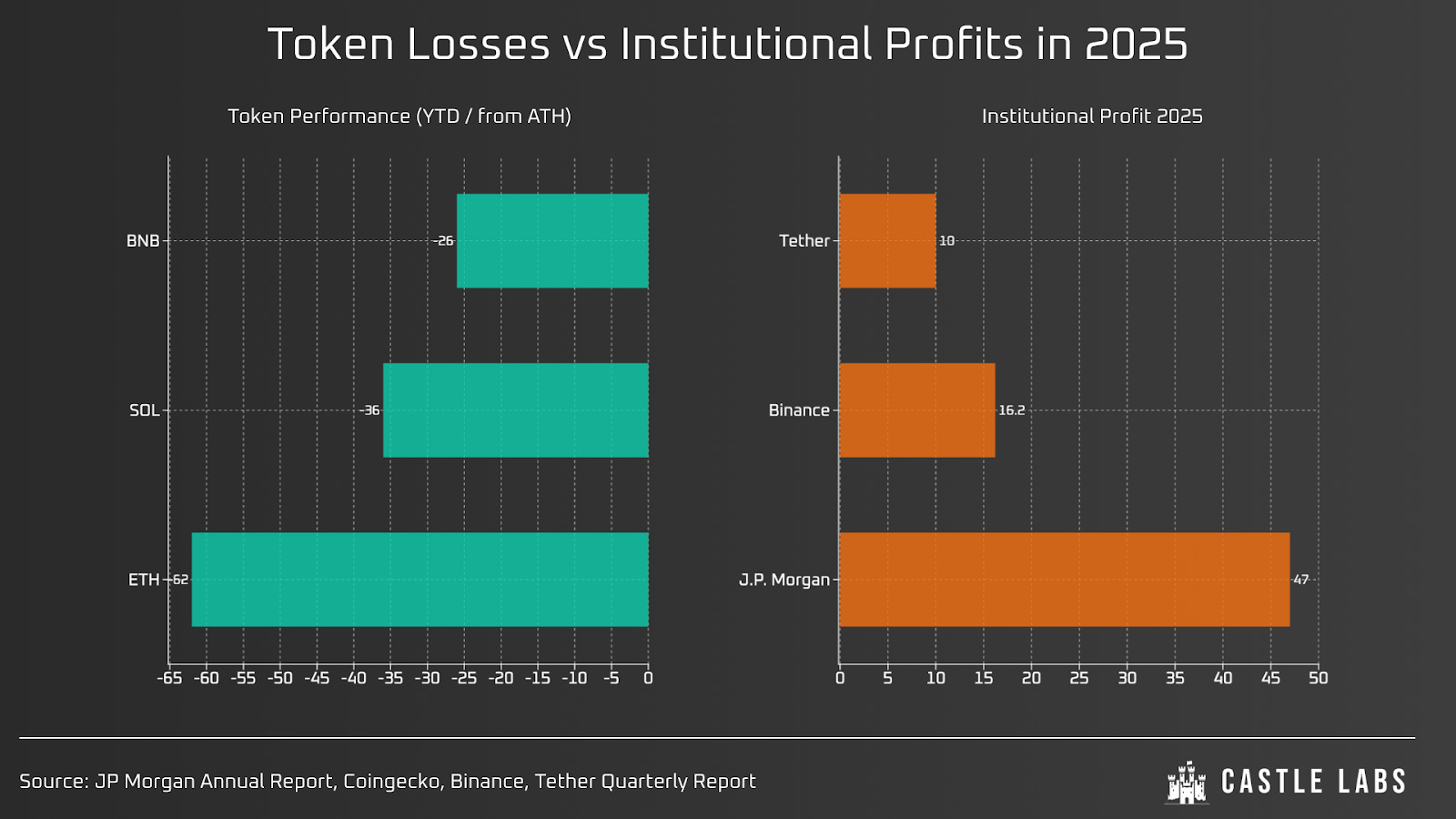

US Treasury debt tokenised onchain is nearing $10 billion, the same amount Tether pocketed in pure profit last year. Meanwhile, Ethereum, the World Computer, generated just $526 million in fees across all of 2025.

Additionally, Ethereum is currently trading below $2,000, while it reached $4,800 5 years ago.

Equally telling, Solana generated $2.39 billion in revenue last year, while the token itself is down 36% year-to-date (YTD). Now more than ever, it is evident that there is no clear link between crypto adoption growth and the value of most of these tokens.

Not even Binance, the king of centralised exchanges, is safe: despite its 38.3% market share in December 2025 and over $16.2 billion in profits in 2025, its blockchain’s native token, BNB, is down 26%.

The institutions generated substantial profits, which retail has yet to capture.

We can stress two main phenomena:

Institutions are coming and are interested in asset tokenisation.

Their main objective is to change the market in their favour.

J.P. Morgan said at the beginning of February that Bitcoin became more interesting than gold: looking at the chart, one would laugh and dismiss the ravings of those pesky suits who don’t know any better. However, they made almost $47 billion in 2025, while most X’s influencers are recording themselves crying.

As 2026 begins with an extinction-level event in crypto, it is time we stop clicking and study the Zeitgeist. A crash of this magnitude, sustained and uncorrelated to any other asset class, warrants a deep study of the actors behind crypto’s rise and fall.

If we are to achieve longevity in this industry, we must face the reality, as despicable as it appears to us now, and adapt to it. If retail does not evolve, it will either miss the window of opportunity or capitulate. Financial Darwinism commands an acute understanding of what is coming next, lest we revert back to monkeys trenching on PumpFun.

Crypto is far from dead; if it is, it has reborn, and we missed its resurrection, focused on blurry headlines, sponsored posts, and bagholders’ delusional rants.

2026 will be the year of tokenisation and enterprise-grade blockchain technology.

This piece aims to examine the institutional landscape of crypto and identify trends we may have missed.

We will explore TradFi’s imprint on DeFi and provide a clear picture of current stakeholders and their financial and cultural impact on crypto.

Future trends will also be discussed, with an analysis of the most recent reports, working papers, and essays produced by the institutions; in doing so, we will determine the actual trajectory. Importantly, this piece will present an objective, data-driven view of Wall Street onchain.

We will then explore the products they have built to date and how they leveraged crypto to upgrade their infrastructure and financial instruments. We will also discuss the new trends we already see flourishing onchain, such as real estate, insurance, and stocks.

Finally, a realistic assessment of past errors will be undertaken to encourage our industry to adapt to the new bosses and make the most of this enthralling revolution.

Comb your hair, put on your suit and look sharp; the big boys have entered the room.

Welcome to crypto, sir.

Are Institutions in the Room with Us?

First things first: what is an institution?

A bank, a corporation, a treasury, a State, a cartel conspiring in the dark?

The very basic definition of a financial institution is as follows: “An institutional investor is an organisation or entity that manages and invests funds given to it by individuals or entities, typically using more advanced strategies and handling larger sums than individual retail investors.”

For the scope of this article, we consider the following categories of institutions:

Financial companies, incorporated by law and overseen by their adequate regulators, are all the large investors who either invest their clients’ money on their behalf (such is the case for mutual funds, VCs or pension funds), or their own money (such is the case for angel investors, sovereign funds or investment banks).

Institutions also encompass other incorporated and non-incorporated entities that don’t necessarily deal directly with markets, such as exchanges, think tanks, companies, or Sovereign states.

A fringe entity, Decentralised Autonomous Organisations (DAOs) like the Uniswap Treasury or MakerDAO manage billions of dollars and operate like institutions, but they are often not incorporated under the law and are not overseen by traditional regulators. Inherent to crypto, these “institutions“ operate in a grey zone.

Finally, Digital Asset Treasuries (DATs), such as Strategy for Bitcoin or BitMine for Ethereum. In 2021, fewer than 10 companies held bitcoin in their treasuries, according to DLA Piper. That number has since jumped to 190 companies.

In summary, crypto has become ubiquitous. But once again, our definition of crypto (trading Solana late at night, hoping that the ETFs will save us) is poles apart from that of the institutions. For them, it means banking applications, instant worldwide transfers, treasuries onchain, yield and Bitcoin-backed loans. To summarise, there are numerous actors moving crypto, from secretive family offices to exuberant billionaires like Tom Lee and Saylor. In between these, banks, VCs, societies and law firms operate, slowly penetrating decentralised financial markets while we persist in the trenches, half-dead already after a decade trying. As we wither, exhausted, the powers that be are already reigning over our empire of dust; in the middle, they built a glimmering golden palace, an endless horn of plenty worth more than all the shitcoins we lost in the battle.

These opportunities will be evaluated once we have gathered what institutions have to say about crypto.

Invented Allies: What the Institutions Want

This section provides a glimpse into how institutions think and what they really want from crypto.

Why are they here?

These institutions, which have operated across decades and continents, understand markets better than retail traders.

At the end of 2025, Citi released a report called “Web3 to Wall Street”, where they set out to “map the future of money”.

As a result, they revised their stablecoin total issuance forecasts in this report to: $1.9 trillion base case (previously $1.6 trillion) and $4.0 trillion bull case ($3.7 trillion) by 2030”

The base case represents an increase of more than 500%.

Ronit Ghose, Global Head of the Future of Finance desk, said: “The evolution of digital assets – stablecoins, tokenised deposits, deposit tokens –feels in some ways like the early days of the dotcom boom…. But we don’t believe crypto will burn down the existing system. Rather, it is helping us reimagine it.”

This report asserts that we are on the verge of a total transformation where digital assets become the primary rails for global value exchange.

Over 50 pages, with no mention of tokens, memecoins or gamification.

Last week, Goldman Sachs’ Global Institute released a report on stablecoins, arguing that stablecoins will be gradually adopted by consumers, thanks to a series of legislative measures implemented by governments around the world. They also foresee the rise of different currencies to support emerging markets. As part of this, they have worked directly with Marquee Digital Assets, their proprietary crypto trading tool, and partnered with Coin Metrics to launch Datonomy, a data platform for classifying crypto markets.

Another core topic of the institutions is the tokenisation of their financial products:

In 2019, McKinsey already suggested using blockchain to reduce operating costs. A year later, the OECD published a working paper promoting blockchain to reduce costs in international payments, before crypto skyrocketed in a straight line until the FTX collapse.

Once again, the report makes no mention of altcoins, L2s or NFTs.

HSBC, the gigantic British conglomerate, has offered tokenised gold since March 2024! In May 2025, HSBC issued the world’s largest digital bond ($750 billion+) for the Hong Kong government.

In the same month, the Canton Network Pilot brought together 45 institutions to test 15 applications on a blockchain. This trend is not contemporary; we have simply been blinded by short-sighted themes and perhaps a sense of pride that we were the first to “discover crypto.”

In its 2026 Thematic Outlook, BlackRock titled a section: “tokenising the future of investing.” Already two years ago, McKinsey wrote about “the transformational power of tokenising assets.” What we believe is a recent trend, stemming from crypto fatigue, is simply the natural outcome of several years of research, progress, and implementation.

While we were trading fiat for bundled marketing slop, banks, funds, and asset managers were leveraging existing technology to deploy their own asset portfolios. What businesses seek is optimisation, low operating costs and high margins. As blockchain technology is largely automated and relies on math and engineering, it enables BlackRock or Morgan Stanley to tokenise existing financial products and make them available 24/7 to everyone at a very low cost.

This exposé demonstrates that although retail has felt abandoned by institutions, they were, in fact, present from the beginning. For a few years, after a brief period of trial and error, institutions have been adopting crypto to make it their own. What we believed was the end product of DeFi was, in fact, a by-product of a far greater ecosystem, where tokenised treasuries, dollars, BTC-backed mortgages, and 24/7 trading were the real endgame for institutions.

In other words, they grafted TradFi’s very soul onto the bones of DeFi, to leverage the technology we dismissed for short-lived, silly narratives.

Building Blocks: What the Institutions Built

Thus far, we have identified the institutions, how they operate, and what they aim to achieve. If it is quite obvious that States wield overwhelming power over crypto through legislation and executive powers, financial institutions also exert influence through funding, subsidies, loans, backing, investments, and other financial support.

As it stands, we have a wide array of applications, protocols, superapps, financial products, and more that are either fully integrated into DeFi or adjacent to it.

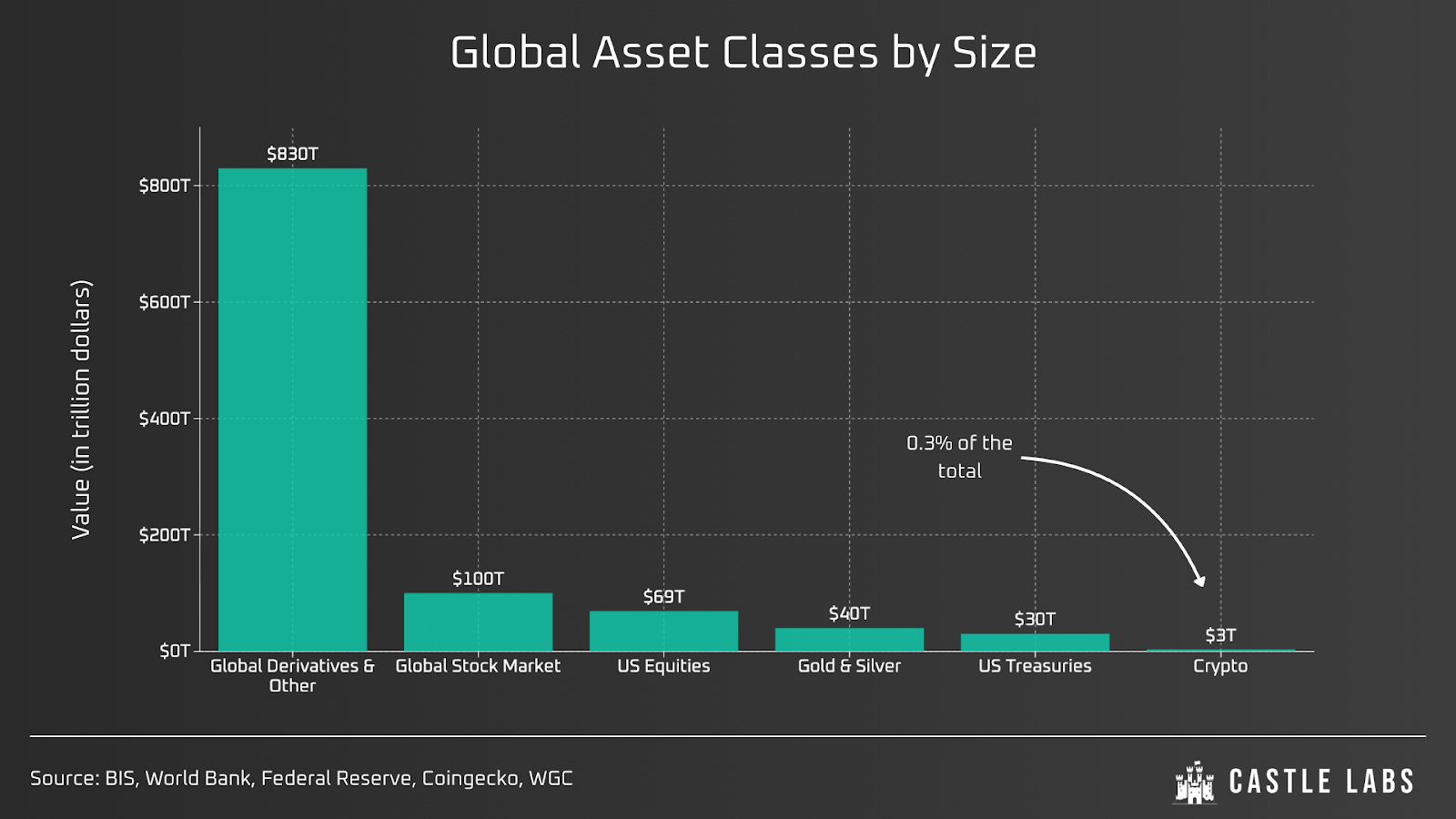

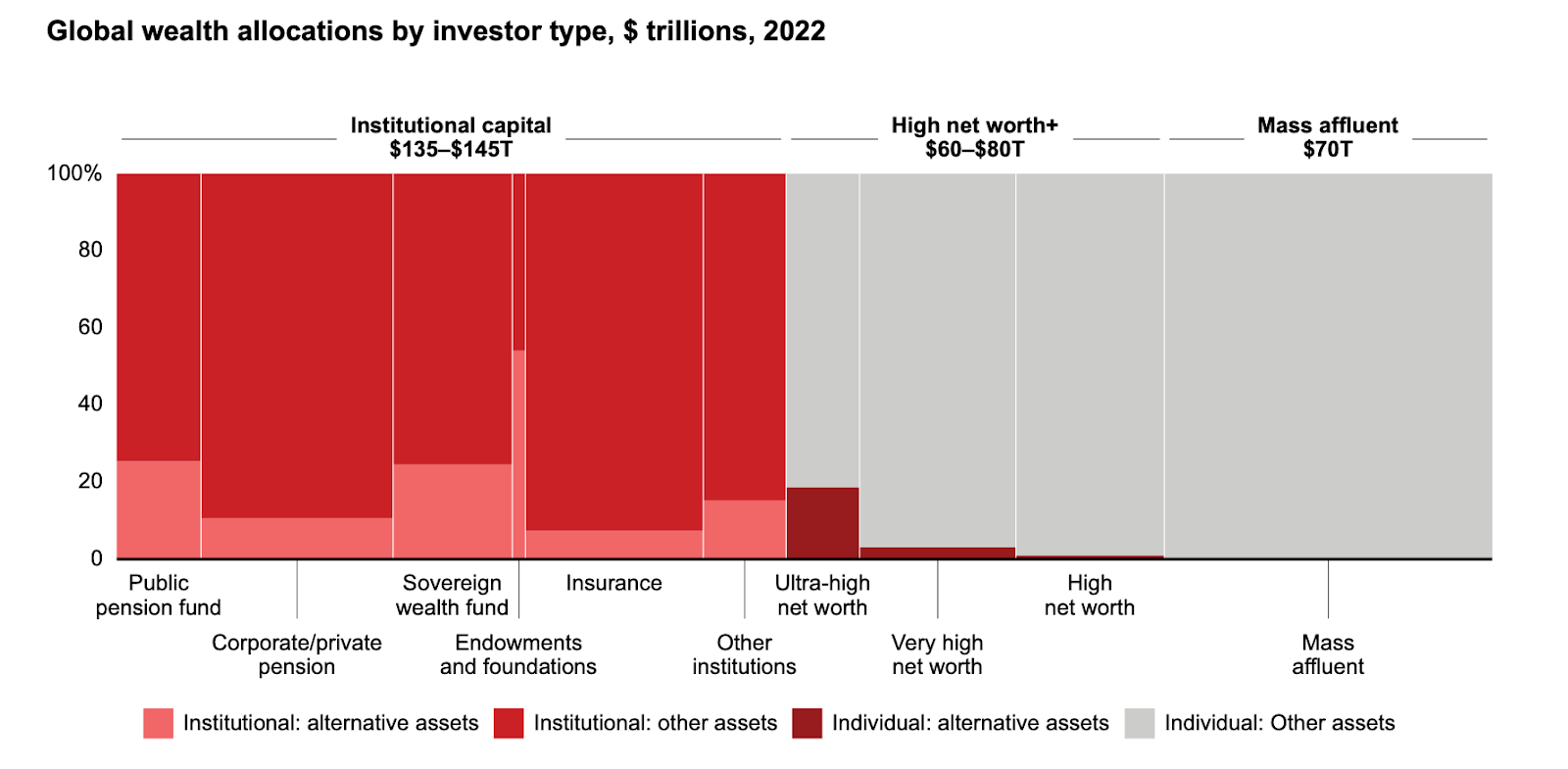

The primary reason institutions are moving traditional financial assets into DeFi is practical: the stock market’s value exceeds $100 trillion, according to the World Bank. The USA’s titanic companies are worth $69 trillion, 25 times more than crypto’s. Gold and silver are worth a combined $40 trillion. According to the Fed, as of late 2025, the total outstanding value of the U.S. Treasury securities is nearing $30 trillion. If we include foreign securities, the insurance market, exotic products of all kinds or derivatives, a quadrillion is on the table. accounts for only 0.3% of this figure.

It is therefore easy to see why crypto tokens are of little interest to international institutions; we’re playing in the kids’ league!

Let us now look at what institutions have been doing in crypto over the past few years and the product classes they have built.

The spearhead of institutional crypto is yield. Banks are Web 2 lending protocols that charge interest on the money they lend. It only makes sense to see how institutions are showing strong interest in curating vaults, protocols, and products that generate yield. For example, Morpho (via BitWise) and Aave (via Blockdaemon) maintain vaults with stable yields, offering near-certain returns for investors.

Another interesting development we already mentioned above is tokenisation. It is likely the pinnacle of blockchain technology, where any financial instrument can be brought onchain. According to J.P. Morgan and Bain, alternative investments such as private equity (PE), private credit, real estate, and hedge funds could derive an additional $400 billion per year using tokenised products. In a major report co-published by Wall Street giants, the authors argue that improved liquidity and simplified investment practices are a boon for asset managers.

To put that into perspective, this is a fifth of the current crypto market capitalisation, earned each year.

As it stands, only 5% of High Net Worth Individuals hold alternative assets, according to the same report, which draws on Bloomberg and SEC filings.

The opportunity to expand into the individual investor segment has led major alternative managers such as Blackstone, KKR, Carlyle, and Apollo to focus on this segment: combined, they represent more than $3 trillion in AUM, according to Forbes and SP500 data.

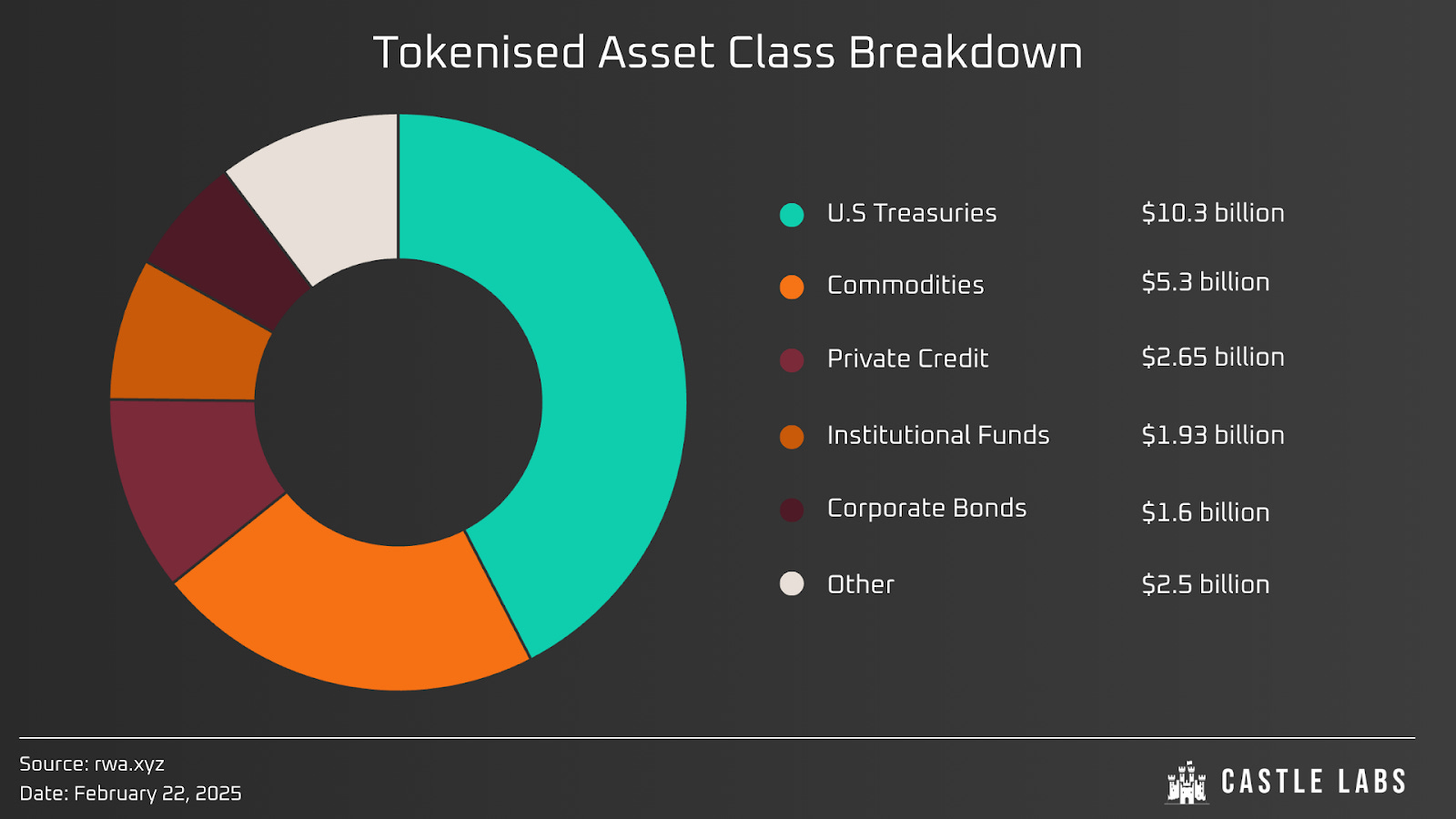

Today, the overwhelming majority of tokenised assets consists of stablecoins, representing almost 93% of the total value. It would, however, be simplistic to reduce RWAs to idle dollars, as they mostly provide liquidity to crypto, fueling runs and collapses. Far more interesting are the commodities, debt instruments, and private credit markets being introduced onchain.

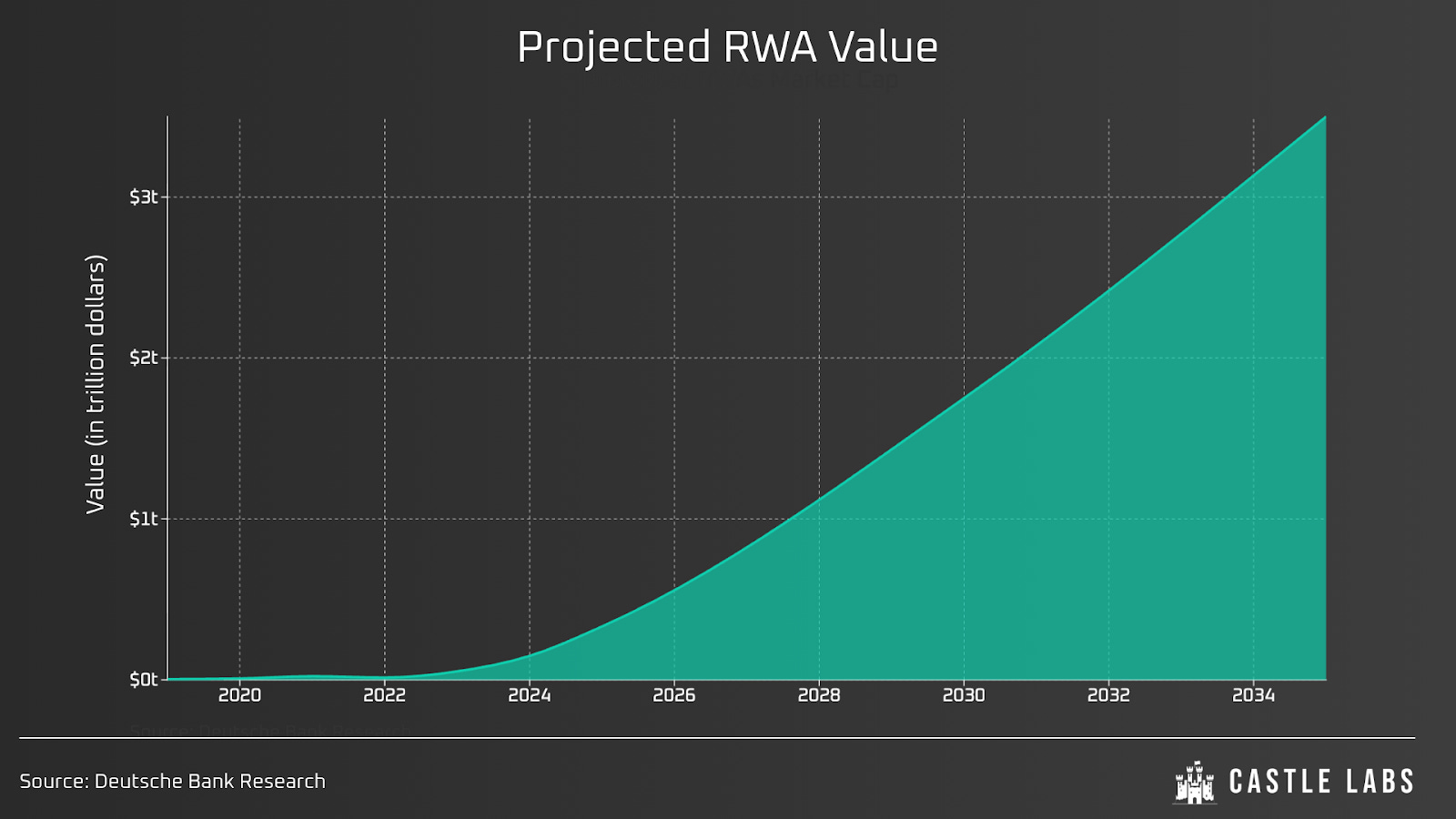

According to Deutsche Bank, tokenised capital markets could become the default infrastructure for issuance and trading, reaching $1.5-2 trillion by 2030 and $3-4 trillion by 2035.

If these figures appear far-fetched, the total market size for tokenised assets has expanded from $4 billion in late 2019 to $331 billion in late 2025, an 8,175% increase. It is therefore feasible to imagine a similar growth in a favourable environment:

Regulations, although slowly, are finally hitting presidential desks for signature, and crypto investors feel less marginalised

Tokenisation is still limited to debt and precious metals, but there is a significant rush to tokenise stocks, which would unlock hundreds of trillions of dollars and make them accessible 24/7 worldwide.

Tokenised bonds and loans take time to mature. When these products become redeemable, billions of dollars will flow. Reputational risk is massive for banks, and they still need the direct approval from regulators and international bodies.

Tokenisation has slowly been endorsed by all. Two years ago, the Financial Stability Board, the global police for banks, said that tokenisation’s risks were similar to those of traditional finance, recommending clear regulation and oversight to allow this new technology to grow, indirectly accepting this new reality. As Larry Fink said in the Economist last December, “tokenisation can greatly expand the world of investable assets beyond the listed stocks and bonds that dominate markets today.”

All we need for these prophets to be right is the final, unequivocal green light from legislators worldwide.

A few products now deserve our attention because they were the first to offer accessible tokenised assets, presented to sophisticated investors by Tether, BlackRock, and Franklin Templeton.

The first major tokenised fund was Tether Gold back in January 2020, even before crypto became a macro topic. It offers investors an ounce of gold onchain, backed by vaulted physical gold

After gold, Franklin Templeton tokenised its money market mutual fund FOBXX. This was the first regulated, registered US Fund to be put onchain. Today, BENJI, the tokenised version, is nearing $1 billion in TVL.

The third is BUIDL, a tokenised money market fund that issues digital shares backed by Treasuries. It has been available since March 2024. Its TVL sits at $2.10 billion.

Curated vaults are another interesting product built by TradFi on crypto-native apps like Morpho. In this ecosystem, Bitwise, managing $15 billion, serves as the curator, essentially the vault’s risk officer. Instead of users overseeing the vault management, they can rely on the risk parameters set by Bitwise.

Besides money markets and commodities, real estate is also coming onchain. Ernst and Young published a report last year, hailing tokenisation as a “new era for property investment”. Deloitte, its counterpart, called tokenised real estate a transformative revolution, poised to explode in the next few years. Long constrained by high costs, slow settlement, and limited investor access, this asset class is often inaccessible to the average investor, whereas a flat or house would become a liquid asset one can buy or sell in the middle of the night. Forecasts estimate that over $4 trillion in tokenised property will be in place by 2034, with the tokenisation market as a whole reaching up to $30 trillion.

Dubai-based properties such as World Islands, DAMAC City tower, Dubai Marina Hotel, Kensington Waters, and Sobha Creeks are already onchain.

Other exotic products, such as corporate bonds (Siemens) or private credit for institutions (Apollo), are available, but what interests us most is obviously tokenised stocks. Equities’ global value dwarfs crypto, to the point where Bitcoin becomes a boring asset among others within the financial sector hierarchy.

Currently, several different protocols offer different mechanisms to get exposure:

Direct tokenisation offered by Securitize is the most basic form of tokenisation, where the share itself is digitised onchain. Here, the issuer uses the blockchain as the primary ledger to register direct ownership. SEC-compliant, but gated by whitelisted registration, which makes such a mechanism antagonistic to crypto’s raison d’être.

Entitlement tokenisation is a tokenised security entitlement in which custodians, such as the DTCC, record ownership within their internal vaults. It is compliant, but it offers the lowest onchain utility.

Indirect Tokenisation, or wrappers like Ondo and xStocks. These are security-based swaps in which a third-party issuer creates a vehicle to track a stock’s value. These offer the highest accessibility and onchain utility for DeFi, the pinnacle of crypto’s approach to making things practical and enjoyable.

For example, Ondo’s Global Markets’ assets have been purchased by over 30,000 investors across 90 countries, with over $9 Billion in total trade volume and over $550 million in TVL. Ondo noted: “The first step was comfort with tokenised T-bills. The next step is broader adoption of tokenised global market assets as settlement, collateral, and programmable financial primitives. We’re seeing a shift of institutions participating at the token/asset level to now participating at the protocol level, with particular interest around vaults and their various applications”. Another issuer backed by Kraken, xStocks offers a bankruptcy-remote structure where, even in bankruptcy, holders receive the value of the underlying asset; TradFi-grade insurance against offchain events.

Perpetual futures on Hyperliquid’s HIP-3 (tradexyz and felix) or Ostium, a derivative with no backing and no ownership. It is mostly built for pure traders, not investors.

Special mention to Ventuals and Pre-Stocks, which offer either perpetual or pro rata claims on equity held in an SPV; these two companies demonstrate how far tokenisation has progressed.

The possibilities with tokenised stocks are endless, but Aave’s Horizon is the summit of crypto’s versatility. They confided,” Institutional interest in Horizon is extremely high. It’s the first lending architecture that integrates RWAs natively and takes into account each asset’s permissioning logic.”

In the old world, if an institution owned $100 million in Apple stock and needed cash, it would have to go through lengthy procedures to leverage its holdings. Now, they just wrap that stock and drop it into Horizon. Institutions can just borrow against their assets in the middle of the night, depositing any tokenised stock or bond as collateral and receiving freshly minted cash in return. Already $100 million has been borrowed!!

In their own words: “V4 will ultimately allow for far more flexibility around Horizon. We anticipate being able to onboard new types of RWAs, create tighter integrations with custodians and other entities that some institutions are forced to use”.

Thus far, we have demonstrated how institutions have deployed their own weapons inside crypto’s infrastructure. This is, however, only a step toward something greater: the total transformation of the financial system, which also includes government administration, healthcare, and even shipping.

Everything Onchain, Literally Everything

The final and perhaps the most shocking finding of this piece is that crypto already belongs to the institutions; onchain finance is here. The idea behind the total transformation of money did not come from the trenches, but from Wall Street boards, corporate research departments, central banks and sovereign States. Beyond adding their native products to the blockchain, the institutions are transforming themselves into a better, faster, sexier version of themselves.

The goal is to put yourself and everything you love on a ledger.

Sarah Breeden, Deputy Governor at the Bank of England, gave a speech on how blockchain technology can “provide the ultimate settlement asset of central bank money.”

Central banks are moving onchain. In lieu of uncertain returns on obscure tokens, we are offered the opportunity to radically transform our wealth management alongside the Fed, J.P. Morgan and the OECD.

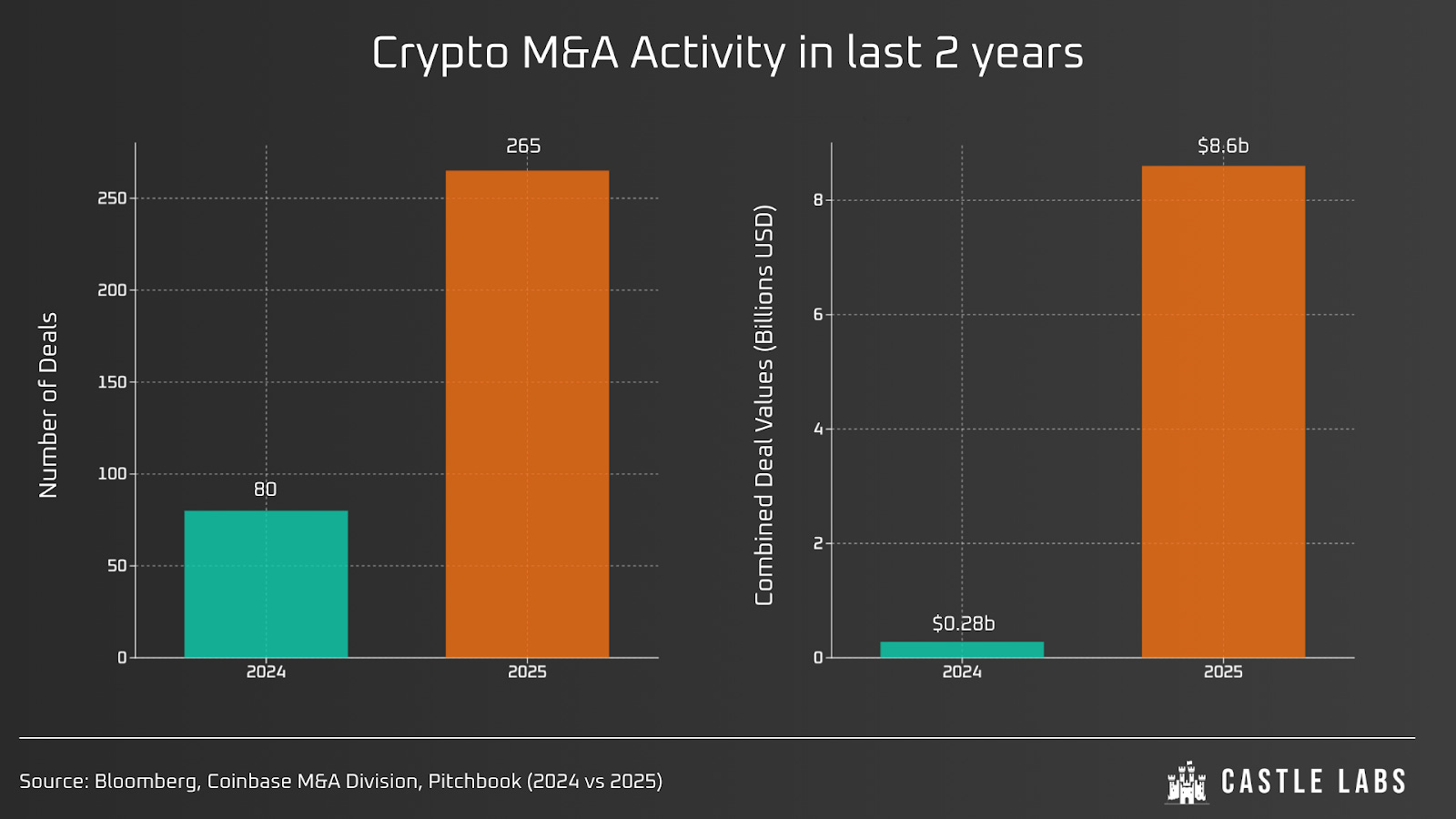

Even within crypto’s bubble itself, 2025 was the year of the mega-deals. More than 265 M&A deals were recorded, representing $8.6 billion in combined value.

Aklil Ibssa, head of corporate development and M&A at Coinbase, noted: “That shift favoured exchanges, stablecoin issuers, enterprise-facing infrastructure providers and other businesses to go public, while more speculative businesses largely remained sidelined.”

Rob Hadick, general partner at Dragonfly, expects listings coming from exchanges, prediction markets, stablecoin companies, custodians, wallet and other core service providers.

Web3 is manifestly being repurposed by TradFi as a rail for their own services. VCs, exchanges, and stablecoin providers are funding payment services, wallet infrastructure, and software.

At the end of last year, Bloomberg titled: “Crypto M&A surges 30-Fold as niche firms shift to mainstream”.

Among the notable deals, we highlight:

Coinbase’s acquisition of Deribit, a derivatives platform

Kraken’s acquisition of NinjaTrader, a futures trading platform

Ripple’s acquisition of Rail, a stablecoin protocol

Notably, the tenth-largest funding round of 2025 goes to Polymarket, a crypto protocol. And none other than the NYSE invested $2 billion at a $8 billion valuation.

Overall deal volume exploded 226% this year compared to 2024, driven largely by massive M&A activity, which accounted for a 1500% increase.

Companies such as the aptly named stablecoin protocol Bridge, owned by Stripe, are completely changing the traditional financial system, which is annoyingly slow and expensive. Bridge turns blockchains into a standardised payment rail that feels like a traditional bank to businesses, but moves at the speed of crypto.

Other crypto-native businesses have also onboarded the outside world:

Rise, the HR platform for the crypto world, built a compliance engine that enables global companies to pay workers in a mix of fiat and crypto. Hugo Finkelstein, Rise’s CEO, confided:” What was once speculative interest is now strategic allocation: institutions are embracing crypto and tokenisation as core infrastructure, unlocking new efficiencies and expanding the universe of investable assets”.

Visa now uses stablecoins to speed up its back-end treasury operations, moving funds between banks via Solana and Ethereum instead of the legacy, slow SWIFT system.

BVNK, backed by Visa, Citi, Tiger Global, and Coinbase, processed $30 billion in 2025.

This frenetic activity reflects an institutional gold rush, not the “death of crypto.”

Other important sectors, such as healthcare and government administration, are migrating onchain to address the data crisis. In healthcare, organisations such as the Mayo Clinic and UnitedHealth use blockchains to provide patients with “self-sovereign identity.” Instead of hospitals owning data, patients hold an encrypted “Patient ID” wallet. When they visit a specialist, a smart contract automatically verifies their insurance and unlocks their history, reducing claims processing from weeks to seconds. In the same vein, government administration, a mythological antagonist for anyone looking to get a paper done, is moving onchain to make everyone’s life easier. Estonia remains the gold standard, having moved its entire judicial and civil registry onchain, but now U.S. states like California have followed, digitising over 40 million vehicle titles on the blockchain. From now on, a car sale automatically triggers a title transfer and real-time tax payment to the DMV, eliminating the need for manual paperwork and useless, lazy legacy intermediaries.

The possibilities are endless. Anything can be recorded in a ledger: patient ID, titles to property, books, financial records, shares of a company, tax records, and everything an individual or an entity needs for their daily activities.

Beyond the financial products mentioned above, institutions are also building their own infrastructure for themselves and their clients. Banks, hedge funds, billionaires and corporations can borrow, settle, wire and repay unlimited amounts of dollars in a second, at any time, at an insignificant cost. The only factor at play is certainty: to achieve widespread adoption, the key requirement is regulatory approval from governments worldwide.

Put on that Suit!

The data we have compiled above, coupled with statements from central bankers, CEOs, executives, and international organisations, provides a clear picture of what is happening.

New technologies achieve mass adoption only when they solve a specific “pain point“ rather than offering a philosophical vision. For retail, the pain points were access and fees, which were addressed by the 2024 launch of spot ETFs and the proliferation of payment apps mentioned above. For institutions, the carrot is efficiency and liquidity.

Mainstream status is finally reached as the technology becomes the standard. In this phase, the public uses blockchain not because they “believe in it,” but because it is the fastest, cheapest way to move capital, and, suddenly, one wakes up one fine morning to find crypto as the only way of doing business.

We have already reached that phase, and it is our responsibility to adapt. We have been trying to strike a balance between gambling and investing for 15 years, while institutions leveraged our naivety to extract not just capital but also human output, technology, and know-how.

The nature of society has barely changed since the days of Machiavelli and Hegel, and the natural dynamics of a competitive system are unfair, ruthless, if not cruel. Instinctively, unsophisticated retail will push against the trend because it breaks their tenet of infinite gains. There is no cheat code for free money in a world of finite resources, and even if money is printed to support the debt junkies of the West, we are not the beneficiaries.

Whether we like it or not, the future is in the hands of institutions, and the strange era that lasted from 2010 to 2021 is over.

The transition from playground to global financial network Leviathan has already happened. From all the evidence gathered, we can affirm that:

Institutions have long been interested in crypto.

They always kept their distances with tokens, treating them as speculative plays; they focused on blockchain as a financial infrastructure.

The infrastructure we helped them erect is almost fully operational, and finance 2.0 is already a reality.

The message from the WEF is clear:

Business leaders must integrate blockchain technology with their asset base, operations and capital structure

Investors and asset managers must explore tokenised assets

Policymakers and regulators must clear the air and support businesses

Technologists must design standards for everyone and make crypto simply universal

And we need to adapt, lest they get all the benefits of the very ecosystem we nurtured for so long. As the suits have entered the room, we can either sit at the table or wait outside in the hallway, sidelined beyond relief.

Yet to declare total institutional victory would be defeatist. While Wall Street tokenises treasuries, crypto-native innovation continues in domains institutions cannot easily penetrate, because they are legally unable to do so.

Privacy protocols like Monero processed 43,000 transactions per day in 2025, designed to be immune to institutional predatory practices.

Decentralised physical infrastructure networks like Helium now operate 1.3 million hotspots globally, creating a $2.8 billion telecoms network without a single corporate board

DAOs like Uniswap’s treasury, which we mentioned above, control $4.7 billion with no CEO, no board, and no entity that BlackRock can acquire or regulate.

While institutions may set the agenda for tokenisation, we are not arguing that they will mandate the adoption of permissionless protocols meant to exist in the dark. These markets are smaller, less profitable, but they are all we have left that remain feral.

The dilemma is whether we will choose the cypherphunk way of life, endangered by Vanguard, State Street, and Goldman Sachs, or mature and become the Nemesis we once swore to defeat, in order to stay profitable and preserve our wealth.

We believe that wearing a tie is a survivalist, strategic choice akin to descending from the trees some millions of years ago in Africa.

Apes or suits, you choose.

written by TradFiHater ✍️

Every week for the last 3 years, we have shared our research for free, directly in your email. Not a subscriber yet? Let’s fix it:

If you are more of a Telegram guy, you can read all of our research without the noise on our TG channel: