Why Bitcoin is Not (Yet) Digital Gold

From the Golden Fleece to South African mines, humanity has endlessly chased this sublime, mythical treasure.

Resembling captured sunlight, it may indeed come from the cosmos, as scientists believe gold results from the collision of dying stars, called supernovas. While most of Earth’s gold lies trapped in the planet’s core, the rest was delivered to the surface by meteorites.

Throughout all of our history, gold has been the commodity at the centre of commerce.

If you were to gather all the gold ever mined by humans, it would form a cube measuring roughly 20 meters on each side, weighing approximately 176,000 tonnes.

It is baffling that such immense wealth can be contained in a single warehouse. While stocks, art, oil, or collectables occupy gargantuan geographical or administrative space, gold possesses the unique quality of portability.

Gold serves as the ultimate store of value because it carries no counterparty risk. It is the only asset that is not someone else’s liability. “Gold is money, everything else is credit,” said J. P. Morgan. Its high stock-to-flow ratio ensures scarcity, making it immune to arbitrary fiat currency debasement. From ancient Lydian coins to modern Central Bank reserves, gold has preserved its role as a store of value for millennia, acting as a liquid, immutable anchor against financial, political, and social chaos.

But recently, a new contender for the title of money has emerged.

Although different from previous metals, due to their volatile and encrypted nature, cryptocurrencies like Bitcoin have been touted as gold killers.

Bitcoin is often referred to as digital gold. Could it ever replace gold in the future? And if so, is it desirable to do away with the elder asset?

This article examines gold and Bitcoin in the context of the modern economy, DeFi, and the properties of money. Then, we will run a comparative analysis to ultimately determine whether both assets can coexist in a highly competitive macro environment, and analyse current trends to determine whether Bitcoin presents the properties of “digital gold”.

Ultimately, a diversity of assets may only benefit the global economy, and it is likely that fiat, an asset whose value largely depends on arbitrary monetary policies, will indeed be superseded by purer forms of money. Gold, or an asset yet to be devised, might escape the inherent erosion of fiat, a currency fatally flawed in our current economy, reliant on debt.

The Legacy of Gold in Finance

For centuries, gold has been the backbone of the system, as the only reserve asset, a status solidified not by legislation, but by the physical laws of the universe. As former Federal Reserve Chairman Alan Greenspan famously testified in 1999, “Gold still represents the ultimate form of payment in the world. Fiat money, in extremis, is accepted by no one. Gold is always accepted.”

Gold’s universal acceptance flows from its intrinsic qualities, which set it apart from all other materials. These qualities established its enduring role as a store of value, what Aristotle referred to as sound money:

Durability: Gold is a noble metal, making it virtually immune to most chemical reactions. Unlike silver, it does not oxidise or tarnish, ensuring that its physical properties remain stable over time. This chemical uniqueness makes it reliable for both economic storage and high-tech infrastructure (electric cars, drones, defence systems, rockets). What’s more, gold doesn’t rust.

Fungibility: Because gold is soft and malleable, it is easy to shape, mould, and divide. This allows it to be standardised into interchangeable coins or bars, where one unit of equal weight (traditionally an ounce or a gram) and purity (14k, 18k, and 24k being the most common) is essentially identical to another.

Stability: Gold functions as a reliable store of value. Its rarity and utility (being the best choice for critical industrial applications despite the cost) help it maintain its worth over time, unlike fiat currencies, which universally suffer from inflation. Also, gold serves as the ultimate store of value because it carries no counterparty risk

Portability: As a dense, expensive metal, gold retains significant value even in small quantities. This high value-to-weight ratio makes it easy to transport significant wealth efficiently, unlike silver, art or other commodities. One can carry half a kilo in their pocket.

Recognizability: Gold’s unique properties make it relatively easy to verify. Modern instruments like the Sigma can immediately detect fake gold.

Gold is thus the perfect store of value, with one exception. Gold is not an interchangeable credit card or a line of code. To transport gold, even for a citizen with a modest amount of bullion, is akin to moving uranium; if one forgets to fill out the paperwork, customs officials can seize the gold and keep a large portion of it as a fine. It can be stolen, clipped, hidden, repurposed, and more. Because humans are fallible, it can also be lost.

The 1940 Operation Fish serves as a notorious case study of this logistical nightmare. As Nazi Germany advanced, Britain had to secretly ship £2.5 billion in gold reserves to Canada to prevent capture, requiring the largest movement of physical wealth in history. Today, a click can move trillions of dollars.

The most infamous example of State predatory practices remains Executive Order 6102, issued by Franklin D. Roosevelt in 1933, which criminalised the possession of monetary gold by American citizens. Unlike a password or a seed phrase, gold cannot be memorised; it must be held, and if it can be found, it can be robbed. It has no yield, pays no dividends, and incurs high storage and insurance costs. Most of the world’s gold is stored in vaults in London, Switzerland, Singapore, or Manhattan, sitting in the dark, like an old, forgotten mythical sphinx.

Naturally, because humans are fallible but ingenious, one had to come up with a better alternative to the barbaric relic. Although gold is close to perfection as it is, the frighteningly rapid evolution of our financial system made it necessary to create a modern equivalent. Born of frustration and a will to refurbish a decrepit access to traditional finance, Bitcoin was invented to spite the system. Yet, it soon created a new paradigm far more formidable than its original intent: the possibility of being considered the equivalent of digital gold!

The Advent of Cryptocurrencies

In 2008, during the Global Financial Crisis, Satoshi Nakamoto published his whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System”. It proposed a solution to the double-spend problem without requiring a central trusted authority.

If gold was money by nature, Bitcoin was money by computer engineering. It was scarce, hard to mine, limited, and indestructible.

The invention of the blockchain sparked a Cambrian explosion of various digital assets, some interesting, many worthless. While Bitcoin quickly assumed the mantle of digital gold due to its fixed supply of 21 million coins, other tokens emerged to fill different economic niches.

In 2011, Litecoin marketed itself as the “silver to Bitcoin’s gold,” prioritising faster, cheaper transactions. Four years later, in 2015, Ethereum introduced the concept of a world computer, replacing gold’s passive storage of value with active, programmable smart contracts. It has become the second-most-valuable cryptocurrency and remains unbeaten despite its disappointing price action.

Privacy coins like Monero (XMR) and Zcash (ZEC) attempted to replicate the anonymity of physical cash and gold, a feature that Bitcoin’s public ledger lacked. This year, due to the privacy narrative, they exploded while traditional tokens collapsed. Alts, majors, and Bitcoin alike fell while ZEC, and now Monero, began a run, claiming many bears’ lives in its wake. The combined market cap of such tokens is still insignificant to seriously challenge Bitcoin.

Finally, high-performance chains like Solana or MegaETH later sacrificed decentralisation for speed, aiming to process transactions at the speed of Nasdaq rather than the speed of a wire transfer (internet capital markets). They managed to attract founders, institutions, and banks, but the L1/L2 landscape has become so vast that it is difficult to say which one will outlast the others.

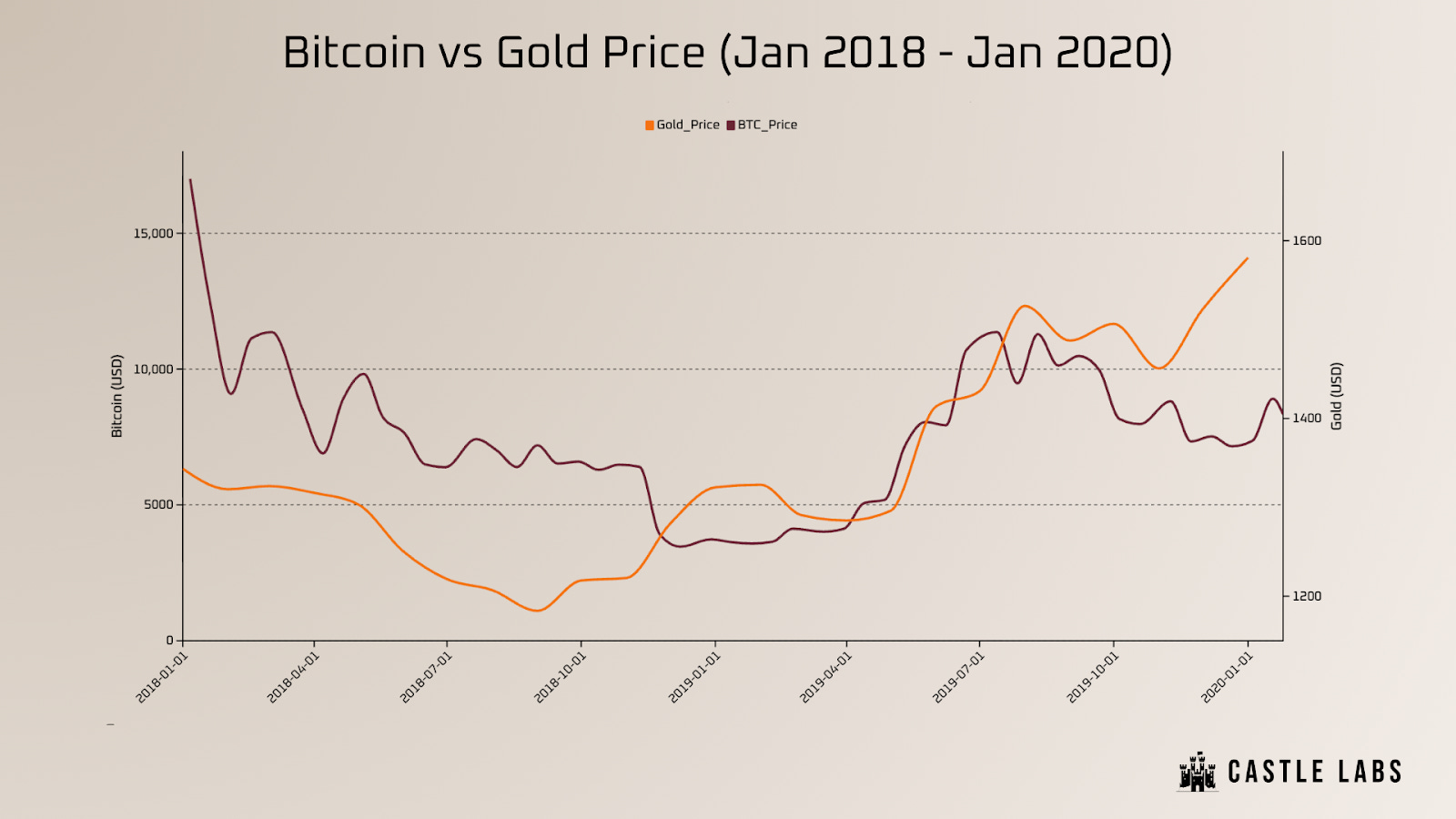

The defining narrative of the 2010s was not coexistence but mutual annihilation, for each new trend erased the other. The industry’s rabid will to erase precious metals was captured perfectly by Grayscale’s questionable 2019 Drop Gold campaign, which depicted gold investors as exhausted suits dragging heavy rocks (shiny rocks), while dandy millennials raced past them carrying digital wealth.

Gold is heavy, physical, and analogue, while crypto is weightless, digital, in a few words, the money of the future. However, pushing the idea that gold was dead while Bitcoin was still largely a cypherphunk fringe asset was probably a cheap, ill-thought-out marketing trick, but the masses followed suit once Covid hit. It took some time for Grayscale to be redeemed, but the next Bitcoin cycle would give them reason.

This newly-found appetite for risky assets suggested that scarcity could be engineered rather than mined.

It remains unclear whether a man-made, artificial commodity was supposed to replace physical properties in the eyes of sovereign states, but the 2020’s showed that investors took the bait.

The Formative Years of Bitcoin

Between 2010 and 2025, Bitcoin escaped the obscure circles of cypherpunks and became a topic of discussion in Wall Street offices, turning from a novel asset worth nothing into a trillion-dollar asset. This fifteen-year period was not a walk in the park, but each time Bitcoin collapsed, it came back to life only to hit a new all-time high. The media were more than sceptical, declaring Bitcoin dead around 450 times.

The narrative arc was thus far from being straightforward. It began with the retail frenzy of 2017, where some people even sold their homes to buy more. Bitcoin surged from under $1,000 to nearly $20,000, driven by retail mania, ICO speculation, and perhaps a general attitude of recklessness. It finally collapsed the same year, taking down the entire crypto market with it (it did seem over at the time).

The macro-hedge era of 2020, championed by legends like Paul Tudor Jones and Michael Saylor, once again revived the litigious asset. Bitcoin found the talking heads it needed to become a macro asset capable of challenging gold. The true breakthrough happened in January 2024, when the SEC approved Spot Bitcoin ETFs.

In the span of 15 years, Bitcoin went from a libertarian internet token to a regulated ETF churning billions of dollars. BlackRock, Fidelity, and VanEck ended up being the voice of Bitcoin; it is possible that the basement rats became billionaires, and their anticapitalist ideology may have been set aside to buy a yacht or two.

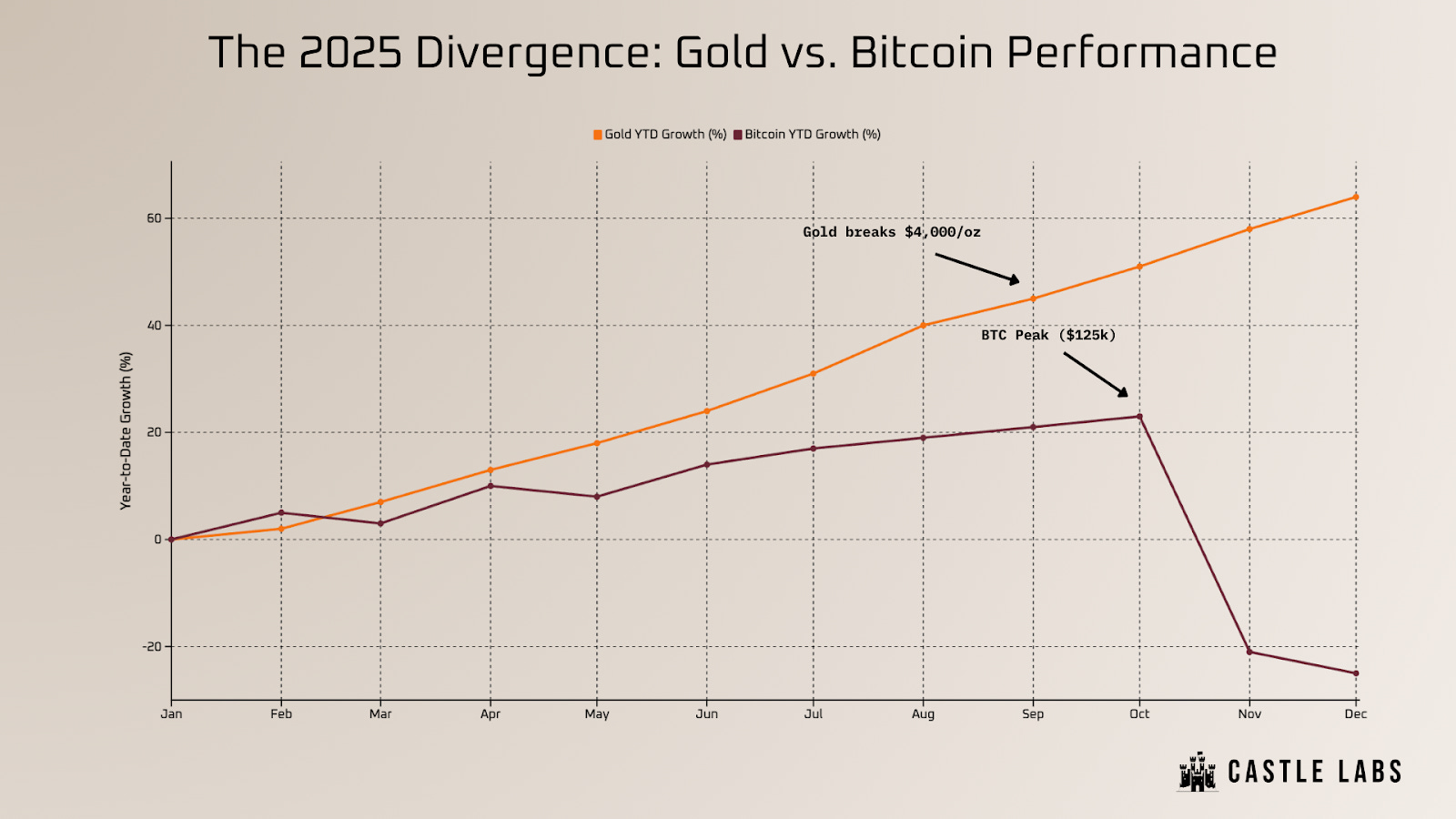

The institutional embrace propelled Bitcoin to break the psychological $100,000 barrier in December 2024, culminating in the euphoric peak of $125,000 in October 2025. For a brief moment, the supercycle theory seemed irrefutable. The USA discussed Strategic Bitcoin Reserves, and crypto traders were over the moon.

But then, in October, a bug in Binance’s USDe pricing caused all leveraged long positions to collapse. If a recovery began shortly after, the wicks eventually filled, and Bitcoin began a slow bleed toward a probable critical level; whispers of 67k could be heard.

The cycle that was supposed to last forever suddenly looked very different in late 2025. While Bitcoin hit new highs, the rest of the market, including blue chips like Aave, Ethereum, Solana, and Ethena, never recovered. Once again, Bitcoin remained undefeated, and its relative strength did not translate into shared support.

This divergence reinforces Bitcoin’s status not merely as a novel asset, but as a reliable, enduring one. It successfully replicates the monetary premiums of precious metals through absolute scarcity and, above all, its first-mover advantage. Unlike fiat currencies prone to endless debasement, Bitcoin offers a decentralised lighthouse that is durable, divisible, and instantly portable. It has effectively digitised the inherent qualities of gold and achieved a total monopoly in its class, despite the high volatility that goes with its immaturity.

By November 2025, a brutal correction saw Bitcoin retrace to $80,000, dragging the rest of the market. To everyone’s dismay, stocks, gold, silver, collectables, and everything in between were following a parabolic phase. Was the rest of crypto dead this time?

Did we trade the promise of true money for an ETF ticker and a pump and dump? Was the institutions are coming narrative just a marketing ploy? A regulated, taxed, and surveillance-heavy asset, unable to follow the rest of the market, appeared now more boring than gold.

Gold was going parabolic, silver, too, and even copper, a cheap metal used for electronics and weapons, was just out of control.

Was gold the only sound money all along?

Triumph of Gold in 2025

Even though Bitcoin fits the sound money test, the latest developments have shown it does not yet behave like digital gold.

Gold outperformed Bitcoin in 2025 as a hedge against inflation, geopolitical chaos, war, and, above all, as a really good investment.

The global gold rush was defined by a massive accumulation of official reserves, led by the National Bank of Poland’s aggressive buying spree and consistent purchases from the Reserve Bank of India, Turkey, and China, with Brazil making a late-year entry to diversify its holdings. While Central Banks drove the strategic shift of metal from West to East, consumer demand for jewellery and physical bullion remained highest in China and India, followed by the United States, Turkey, and Iran, where citizens prioritised gold as a hedge against local currency devaluation and economic instability. Just in 2025, the currencies of Turkey, Argentina, and Iran reached new all-time lows.

If you think the run is over, the institutions pivoted from “gold is dead” to “gold is going to 5k”.

VanEck now argues that persistent geopolitical volatility, fiscal instability, and inflation could push gold toward $5,000/oz by 2030, while undervalued gold miners will, too, ineluctably explode.

J.P. Morgan, the Wall Street titan, forecasts gold averaging $5,055/oz by late 2026, driven by a structural shift that should not be ephemeral. The bank identifies two primary causes for this rise: accelerated central bank accumulation (a continuation of 2025) to diversify away from the U.S. dollar, and a resurgence of Western ETF inflows triggered by Federal Reserve rate cuts. Gold is actively trading as a debasement hedge against currency loss, proving once again that old customs might come from wisdom.

Gold is a way of going long on fear, indeed.

For crypto, the regulatory stranglehold worsened globally, from the EU’s MiCA regulation reaching full enforcement to the aggressive crackdown by the US Treasury on privacy coins and non-compliant stablecoins.

Finally, the mirage evaporated.

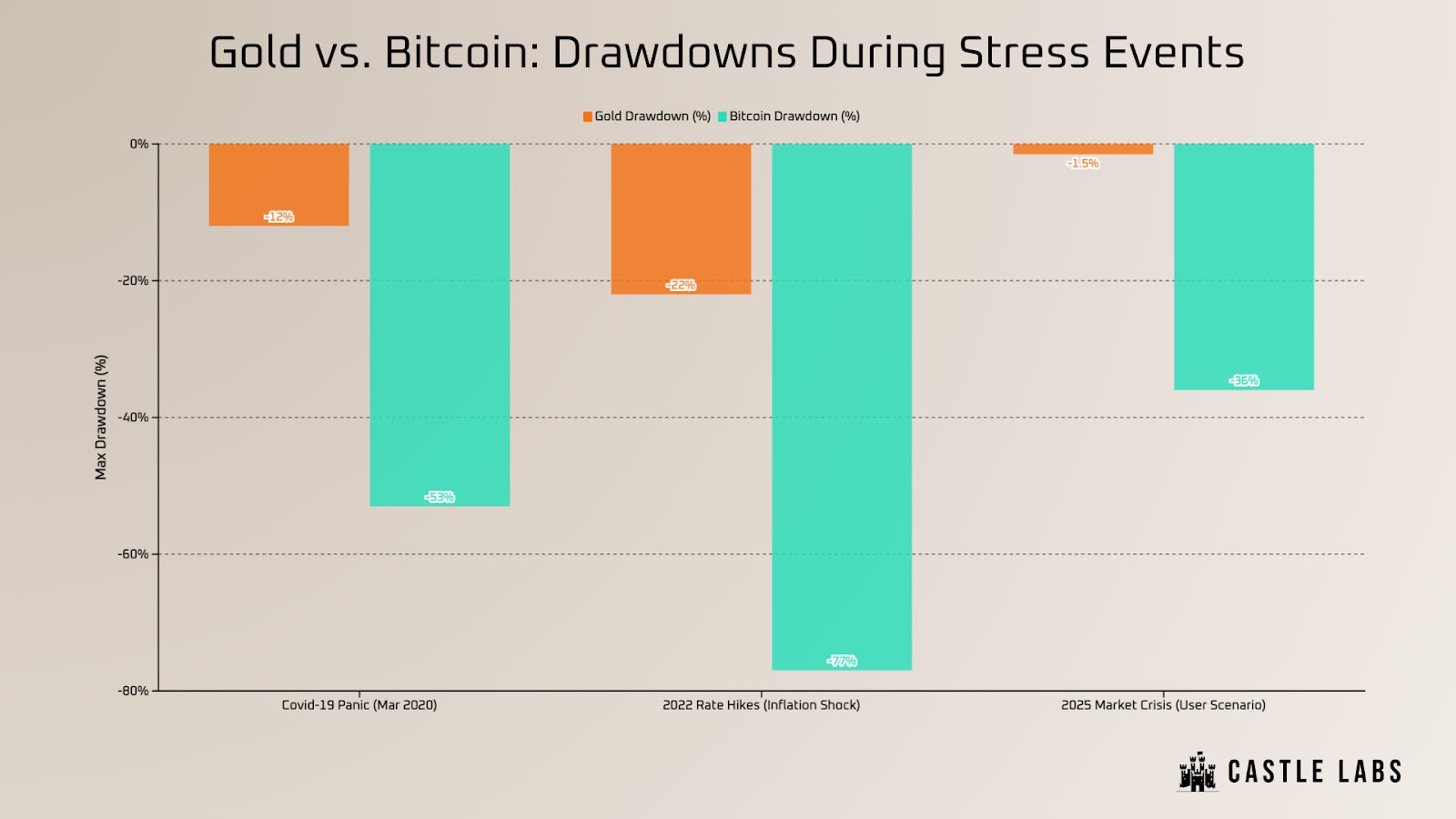

It is difficult to assess the situation, seeing as we are still in the middle of a tumultuous shift. One could cynically argue that Bitcoin has failed its test as digital gold, and we are merely reverting to the mean. After a lengthy experiment, Bitcoin did not pass the sound money test in the eyes of public and private institutions, who, despite a favourable opinion of the digital gold, preferred reverting to a familiar, reliable asset already owned in vast quantities by central banks. The relative stability of gold’s price may have been another advantage that risk-averse investors favoured over Bitcoin; although precious metals wax and wane with global economic conditions, they rarely drop violently. It is in part because influencing the price of such a tremendous asset is difficult, even for institutions equipped with the necessary capital to move precious metals through derivatives. Most of this market cap is, however, dormant (jewellery, central bank vaults, private hoards). It does not move. On the other hand, Bitcoin is naturally leveraged by retail and institutions alike to capture its intraday movements. It is, indeed, much easier to move an asset whose dynamic liquidity defines its direction than a physically inert commodity.

While investors believe in the inflation-hedge narrative, Bitcoin behaved like an immature asset, defined by high volatility and unpredictable swings. The behaviour one expects from a reserve asset did not match Bitcoin’s.

The de-pegging scares of various stablecoins reminded us that if you can’t hold it, you don’t own it. On one hand, gold is the ultimate physical asset; on the other, it is difficult to keep. It would be rash to condemn Bitcoin outright, but short-sighted to crown gold as the one and only sound money in the digital era.

For now, the bulls have gone back to the stable, and boomers are, once again, making all the profits.

It is safe to say that no one could have predicted that Bitcoin would not behave like a reserve asset after 15 years of maturation and frenzied adoption. At the same time a titan who has been ruling over our imagination, senses, and desires for thousands of years was bound to wake from his slumber, some day.

The Herculean Task of Dethroning BTC

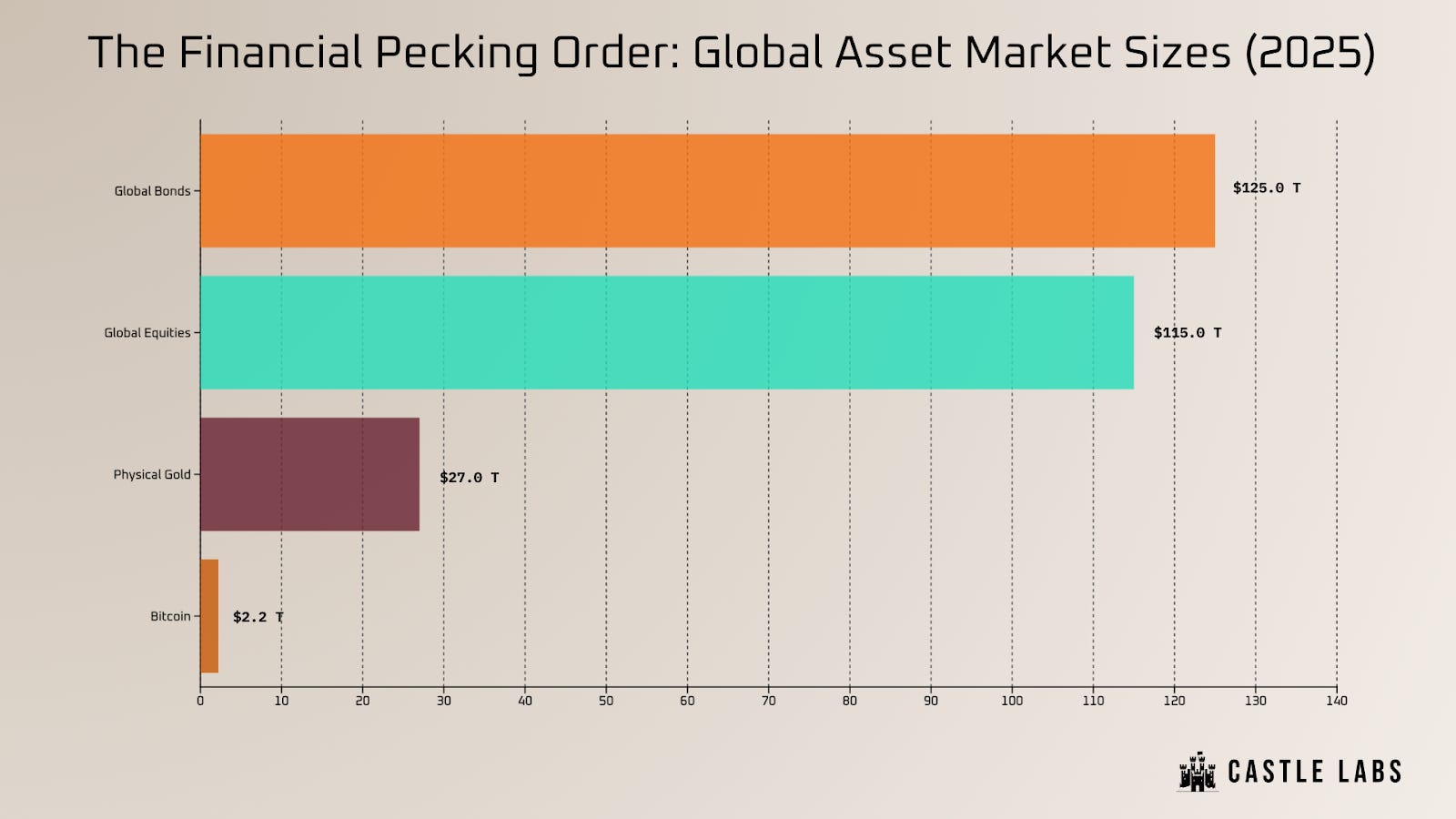

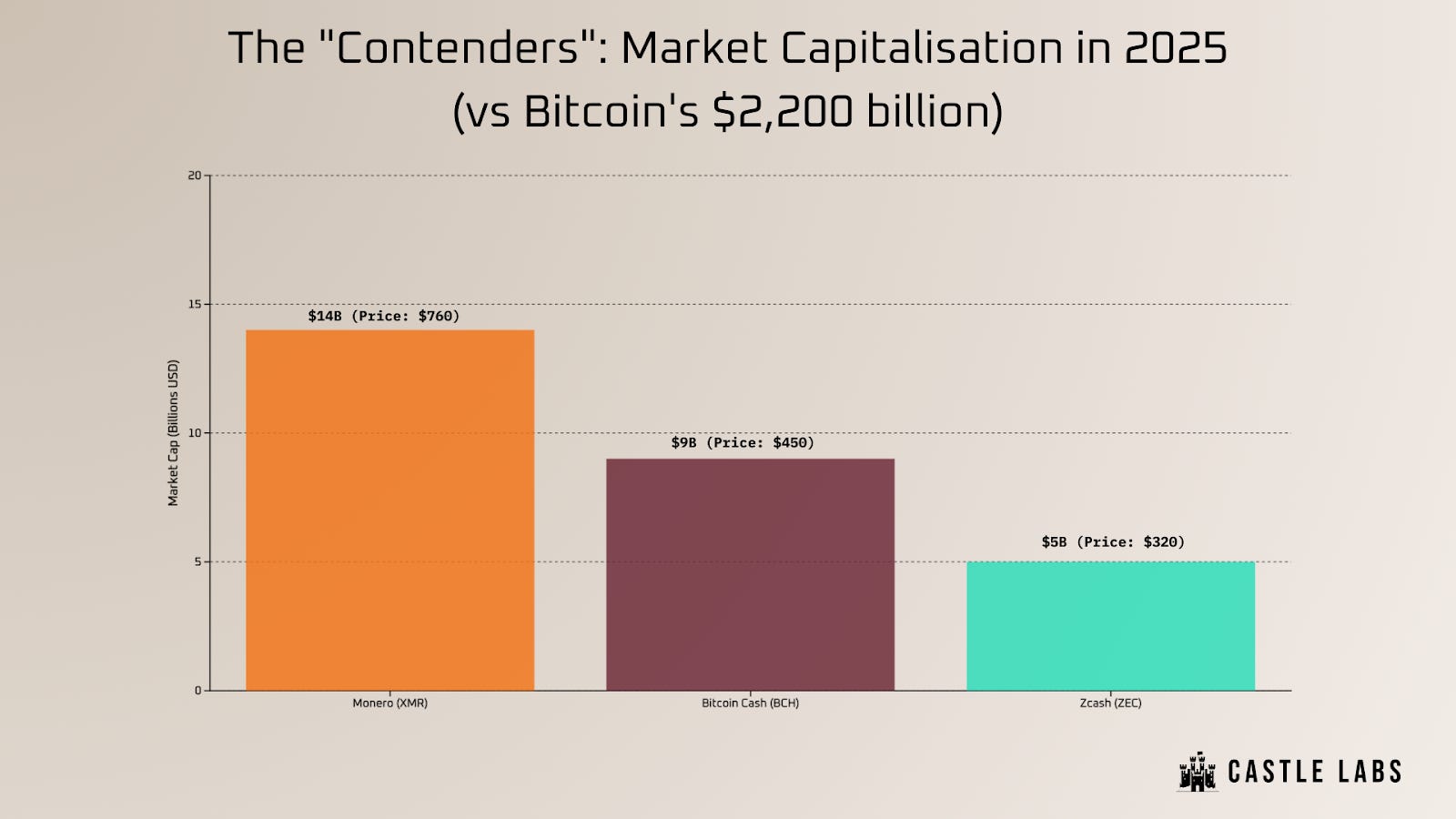

The notion that privacy coins or Bitcoin forks could replace gold as a global store of value had a comeback in late 2025, but the data shows a different reality: while gold commands a market capitalization of around $32 trillion, the combined capitalization of Monero and Zcash struggles to break the $20 billion ceiling, amounting to a small fluctuation in Nvidia’s hourly chart.

In Q4 2025, Zcash briefly caught CT’s attention, not because of its sound money properties, but because of a change in narrative: its auditability features allowed it to survive the purge of privacy assets from compliant exchanges under the EU’s MiCA framework and the US GENIUS Act. On top of that, Solana’s founders launched a marketing campaign, triggering a somewhat organic rush into ZEC. This type of price action is not particularly indicative of sound money and falls into the pump-and-dump category, if one is to judge ZEC’s vitality against gold, silver, stocks, or private equity.

Privacy coins, conversely, became regulatory contraband in 2025. They serve a niche for short-lived narratives, but they might not amount to much in the current boom-and-bust phase. If surveillance fears and a latent aversion to State intrusion drive sporadic rallies, these coins cannot attract the sustained institutional capital crypto is currently trying to absorb. It is paradoxical that coins designed to avoid institutions may only survive thanks to the money said institutions hold, but longevity comes at the price of publicity. It is unconscionable that funds and banks would support an asset designed to bypass them.

The alternatives fail the sound money test completely:

Bitcoin Cash lost the store-of-value narrative years ago; it is a payment network, more or less forgotten by institutions and retail. As stablecoins emerged, Bitcoin Cash became irrelevant, replaced by heavily capitalised tokens specifically designed for payments. After two forks and a lack of community interest, Bitcoin Cash was dwarfed by Bitcoin.

Zcash is valued for secrecy. No sovereign nation can build a reserve on assets that global regulators are trying to kill or that are subject to fluctuating hype. This token is a tool for private trade, not for a public treasury, lacking the liquidity and stability required to replace the $32 trillion gold market. Zcash is limited to 21 million tokens, but despite this attractive, familiar feature, it is still living in the shadow of Bitcoin.

Monero is the alternative to Zcash, but Monero’s privacy is mandatory. In terms of scarcity, because the amount of new XMR minted is fixed (0.6 per block) while the total supply keeps growing, the inflation rate constantly drops, trending toward 0% but never quite reaching it. At least with regard to this property, Monero acts more like physical gold than Bitcoin does, as it has a steady, low annual inflation rate similar to gold (miners digging up new gold). However, XMR cannot replace gold as a reserve asset because it lacks auditability. Its ledger is opaque, and it is impossible to prove reserves to the public without revealing private keys or compromising the very privacy features the coin is built for. Instead, Central Banks need public trust and transparency regarding their reserves, even if the real accountability for the USA’s and China’s currency reserves is debatable.

From this analysis, we can conclude that, structurally, only Bitcoin may indeed replace gold in theory. It passes the sound money test, is well-capitalised and recognised by most, both at the institutional and individual levels. It has clearly established itself as the heart of crypto, despite relentless competition.

It is the only digital asset legally knighted by the US Administration: In March 2025, the United States issued an Executive Order establishing a Strategic Bitcoin Reserve (SBR) by formally designating over 200,000 seized BTC as a national asset rather than auctioning them off. This gave Bitcoin legal legitimacy, and other States, such as El Salvador (~6,000 BTC) and Bhutan (~13,000 BTC mined via hydropower), also established a more or less official SBR. No other asset currently benefits from the support of a world government.

However, replacing gold remains an impractical fever dream, not only because Bitcoin is highly volatile (in 2025, Bitcoin’s annualised volatility hovered around 45%, three times that of Gold’s 15%), but also because its current market cap is dwarfed by gold and silver. Sovereign states need deep liquidity and a massive buffer to support their monetary policy, and unless Bitcoin resumes its growth to $1 000,000 apiece, it will never be as commanding as gold.

The Best of Both Worlds?

For fifteen years, the most ardent debate has revolved around the clash between the titanic precious metals and the ambitious digital assets. Gold versus Bitcoin. The events of 2025 have postponed the debate: Gold is still real money, and Bitcoin remains a risky asset. If volatility is at an all-time high, Bitcoin did not crash enough to warrant a cautious approach. Bar none, the whole ecosystem suffered tremendous losses.

Gold has reaffirmed its role as the millennia-old money of the kings. It is the asset of nations, the last resort insurance that requires no electricity, no internet, and no permission. As we have seen with the aggressive buying from Poland, China, and Brazil, which completely ignored Bitcoin, gold remains the most sought-after commodity in times of trouble.

Bitcoin, conversely, has matured into a high beta asset with a semblance of institutional authority. It is an asset for traders above all, leveraging its brutal swings in each direction. Its high volatility, high portability, and high liquidity allow capital to teleport across borders in seconds, bypassing the outdated rails of traditional banking.

While Bitcoin’s image as a frontier asset weakened, gold’s perfect reputation is even stronger: it is the clear winner of the last year.

The Herculean task of replacing gold was always a false marketing trick. The system now needs both, not least because Bitcoin has birthed a trillion-dollar industry that depends on its good health. But crypto remains the explosive asset we chase relentlessly.

In the volatile years ahead, the prudent investor will not choose between the yellow metal and the line of code, for it is impossible to assimilate one into the other.

If gold is the guarantee of legacy wealth on which lineages and empires are built, Bitcoin is the eccentric darling asset; elusive, sometimes unhinged, yet enigmatically intoxicating. Whether it will metamorphose into the reserve asset we want it to be will only be revealed through further stress tests and years of trial and error.

Since over 3 years, we also run a weekly free newsletter to keep you updated on narratives, alpha, and anything happening in the markets: https://castlelabs.substack.com/

If you are more of a Telegram guy, you can read all of our research without the noise on our TG channel: https://t.me/castlelabsreads