Real Stock Ownership Just Came Onchain: The Castle Chronicle

PLUS: Coinbase post Q1 earnings loss amidst layoffs, stablecoin rewards decision heads to a Senate vote, Aave's new listing standards, and more!

Welcome back to another week!

We’ll start this 171st Edition with a tokenised equity story, then cover the CLARITY Act stablecoin compromise heading to markup, the Coinbase outage and Q1 loss, and Drift’s recovery token plan, before visiting Aave’s new asset listing standards.

Tokenised equity becomes regulated and US-accessible

“Tokenisation is … the defining infrastructure trend of the next 25 years.”

This was Bullish CEO Tom Farley’s statement after digital asset platform Bullish acquired global transfer agent Equiniti for $4.2 billion. In the same week, Securitize, Jump Trading, and Jupiter launched fully onchain regulated trading for tokenised equities, and Republic launched tokenised Animoca Brands equity on Solana, custodied by BitGo and facilitated through INX Securities.

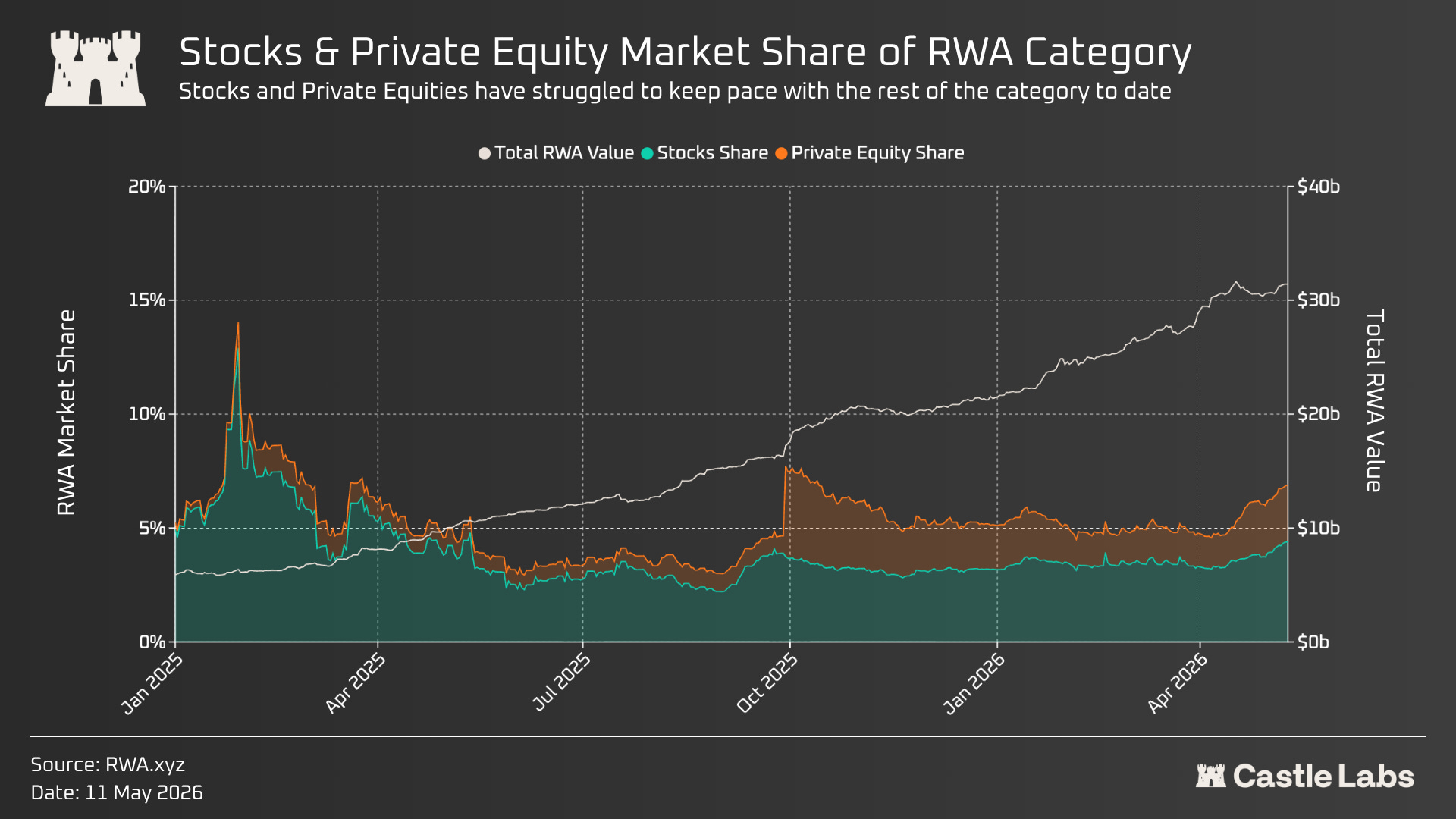

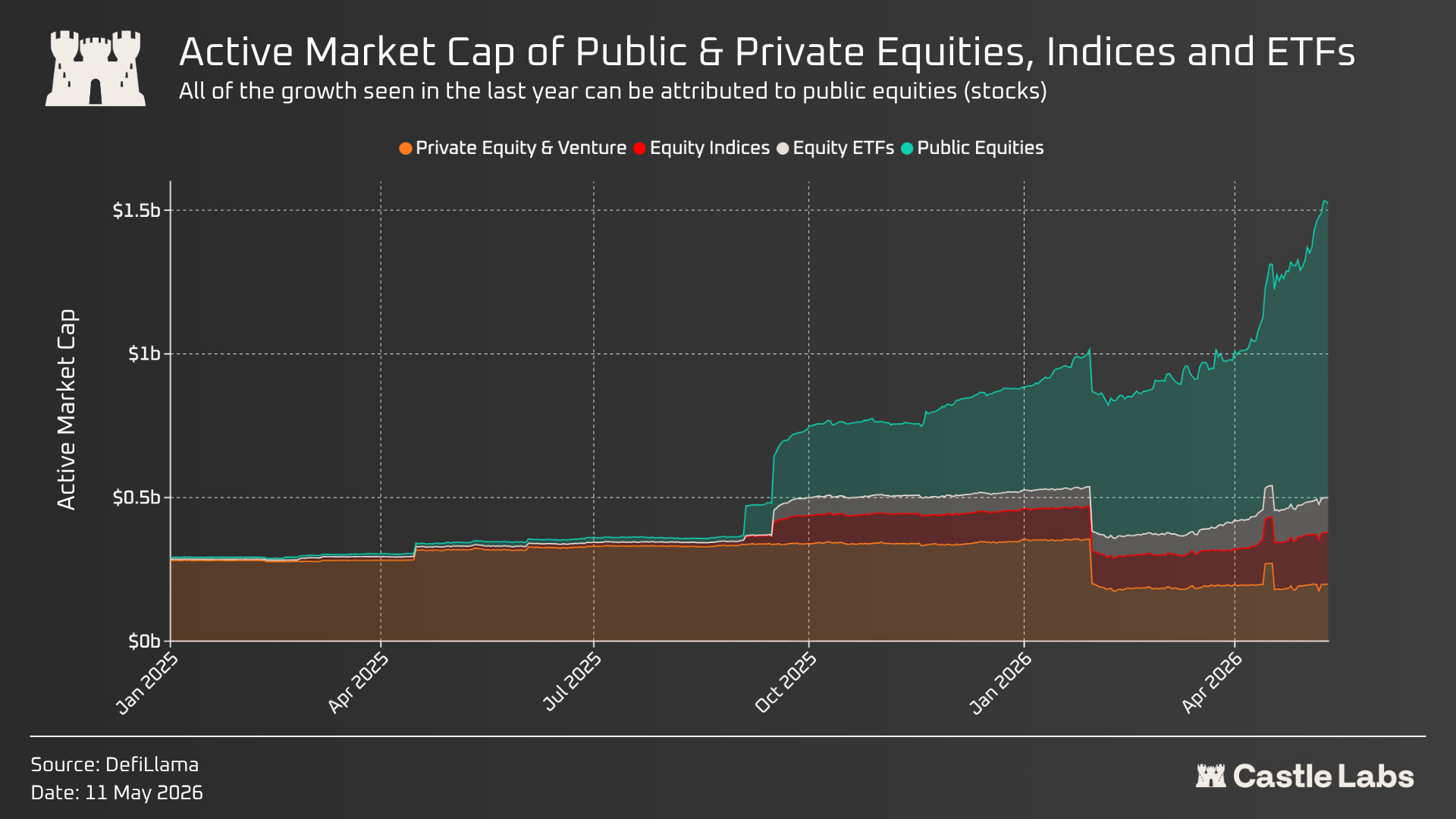

Each of these creates a new route to access tokenised equity onchain that was previously unavailable. We all know tokenisation is coming, and that RWA charts have been up and to the right, but tokenised equity has been lagging behind.

These three announcements show that the infrastructure required for mass growth is being put in place at several layers, particularly in the US, a critical region that current implementations have avoided. To date, xStocks, whilst crossing $25B in total transaction volume, has avoided US access.

Bullish’s acquisition of Equiniti is designed to create a transfer agent for tokenised securities and “position Bullish to lead the shift toward blockchain-native capital markets infrastructure.” Transfer agents maintain records of security owners, track stock ownership, and facilitate dividends, serving as intermediaries between companies and their shareholders.

The Securitize / Jump / Jupiter partnership brings together Securitize’s regulatory infrastructure, Jump’s liquidity through its prop AMM, and Jupiter’s distribution via its interfaces to offer an equity trading experience that rivals tradtional brokers. “The question is no longer whether assets can be issued onchain, but whether they can trade at scale in a way that meets the standards of public markets,” said Carlos Domingo, CEO and Co-Founder of Securitize. Securitize is itself the SEC-registered transfer agent, so the onchain token serves as the legal record of ownership where owners receive voting rights and dividends, unlike existing offerings.

The launch of Animoca Brands tokenised equity is through Republic’s secondary marketplace, using regulated securities-market infrastructure rather than a simple blockchain issuance layer. The move aims to broaden investor access and open secondary trading for existing Animoca Brands shareholders.

It should be noted that both of these offerings will likely require KYC and whitelisting, ensuring regulated execution and legally recognised ownership. However, these steps are necessary to ensure these offerings are fully regulated and compliant with the SEC.

But why does each matter?

Securitize / Jump / Jupiter: Until this week, every credible onchain equity venue excluded US users by design, so this is the first US-accessible path where the onchain token is the legal share rather than a wrapper or derivative claim

Bullish / Equiniti: Bullish controlling Equiniti means tokenised representations of companies can be wired directly into the official register without friction, paving the way for representations that are the legal share, rather than wrappers or derivative claims.

Republic / Animoca: The majority of the focus on bringing equity onchain to date has been on public stocks, but this targets shares that never had a public market in the first place, closing a different access gap and targeting a different audience.

These three join two embedded players in the tokenised equity arena:

Ondo Global Markets is the dominant offshore platform crossing $1B TVL yesterday, with 260+ tokenised US stocks and ETFs across Solana, Ethereum, and BNB Chain, with bridges to HyperEVM (where Felix Protocol is the primary distribution route). Each token is a senior secured structured note issued by Ondo Global Markets (BVI) Limited, with underlying shares custodied at Alpaca.

xStocks (Backed Finance, now Kraken-owned) has been live since June 2025 and is now multi-chain across six networks, including Ethereum, BNB Chain, Solana, Ink, TON, and Mantle. $424M in AUM and 120,743 onchain holders, and accounts for 8 of the top 11 tokenised equities by unique holders. Each xStock is a bearer debt instrument issued by Backed Assets (JE) Limited, a Jersey SPV, under a prospectus approved by the Liechtenstein FMA. Holders are creditors with a bankruptcy-remote claim to the fair market value of the underlying shares, which are custodied at Alpaca and InCore Bank.

Each of these has been driving equity tokenisation on the chain over the last year, with an acceleration in recent months.

We wrote about these and the wider tokenisation landscape in a recent report. Check out our coverage here:

69 Trillion: The Tokenisation Opportunity

$69 trillion: This is the estimated market cap of the US stock market, bringing the grand, global total to $130 trillion.

The main thing to watch will be whether US access proves to be a catalyst for growth, which the offshore issuers were missing.

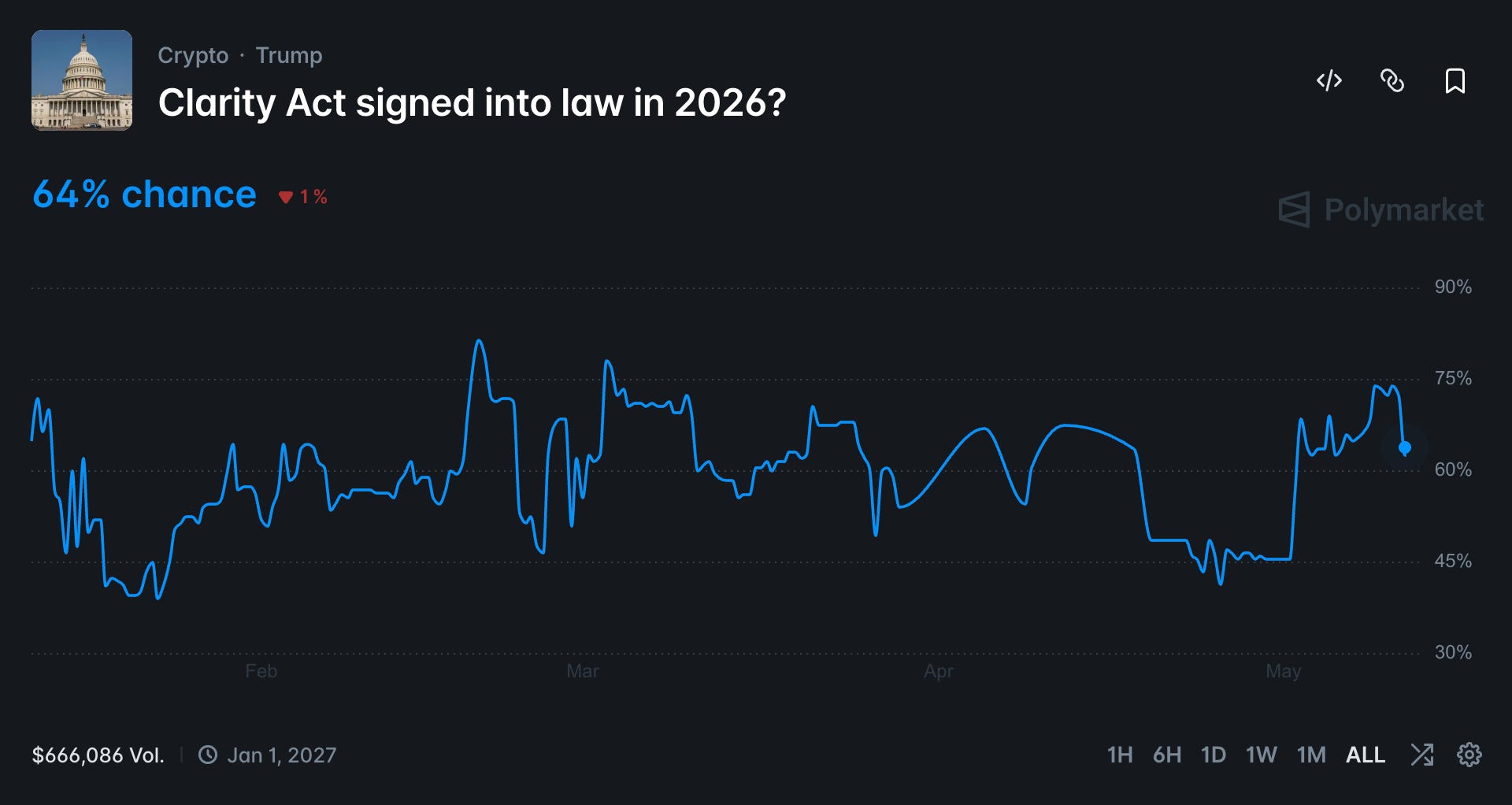

Stablecoin rewards decision heads to a Senate vote

Months since the original stablecoin yield question of the CLARITY Act was derailed in January, Senators released a compromise text. As a reminder, the GENIUS Act restricted issuers from paying yields or interest to holders. The CLARITY Act is being implemented for intermediaries.

The text bans yield “economically or functionally equivalent to” interest on bank deposits, but allows rewards tied to “bona fide activities or bona fide transactions.” Several activity-based rewards were explicitly carved out, including payments, transfers, trading, governance, and staking, with token balances and durations still allowed to factor into reward calculations.

Despite the Act potentially moving forward, there remains significant ambiguity in the text. For crypto companies, there should be plenty of room to create workarounds to pass on yield to users as rewards, especially through incentives for activities that may be positive for the industry and drive onchain activity. However, it will certainly impact the simple way that interest is currently passed on from asset issuers to alternative platforms, such as Coinbase passing on Circle’s USDC yield to users. Stablecoin revenue was Coinbase’s second-largest revenue line in 2025 at $1.35B vs $910M in 2024.

“Crypto’s unhappy, banks are unhappy, but they’re both about equally unhappy, and so we know that we got the right compromise,” said White House crypto adviser Patrick Witt.

The Senate Banking Committee has scheduled a CLARITY Act markup hearing for Thursday, May 14.

Odds that the Clarity Act would be signed into law in 2026 spiked from 45% to 74% in May after the compromise text was released, and now sit at 64%.

Coinbase outage and Q1 loss in the same week

Coinbase went offline for trading for around 7 hours last week after a thermal event at an AWS data centre, disrupting spot trading, Prime, International, and the derivatives exchange. This came as Coinbase reported a $394M net loss in Q1, along with layoffs that cut 14% of the workforce.

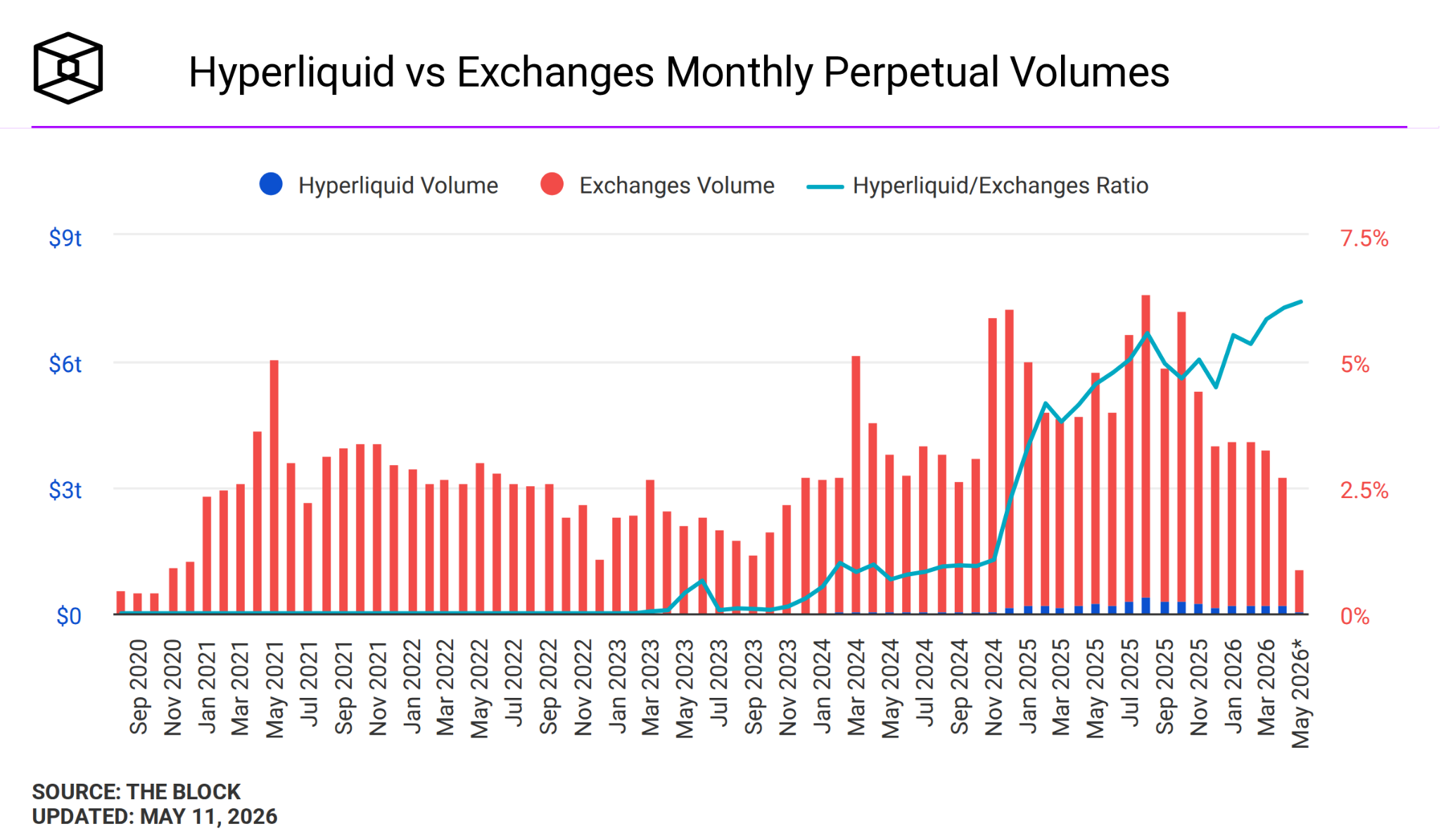

Events like this emphasise the importance of distributing a network’s core operations across multiple locations and mitigating single points of failure. Whilst decentralised trading venues are often not perfect and so too rely on cloud infrastructure, in this instance, they stayed online.

This chart from The Block plots Hyperliquid’s perpetual trading volumes against those of major centralised exchanges, showing consistent market share capture since launch.

Last week, we wrote about four new product offerings across onchain derivatives venues. Check out our coverage of them here:

Drift’s recovery plan could take eight years

Last week, Drift proposed a recovery plan following its $295 million exploit. If successful, they would issue a ‘recovery token’, each representing $1 of verified loss, to those affected, giving them a proportional claim on a ‘recovery pool’.

The recovery pool will be seeded with the protocol’s remaining assets ($3.8M). From there, the pool would grow through three distinct capital streams:

Revenue generated directly from Drift

Tether’s matched deployment, which has committed up to $127.5M as a revenue-linked credit facility, based on Drift’s future earnings

Additional strategic partner capital representing up to $20M

The pool would continue accruing until the total inflows match the exploit losses.

Despite the capital commitments, based on Drift’s 2025 earnings of $19M, the recovery pool could take over eight years to fully replenish, and longer if Drift can’t reclaim its pre-exploit market share (assuming all committed assets are used directly in the recovery pool).

Aave tightens listing rules after the Kelp hack

At Consensus last week, Aave announced that it will fundamentally reshape how it assesses new collateral. Instead of simply relying on historical price volatility, evaluations will now look at cybersecurity, interoperability, and the underlying technical architectures of new assets and protocols. Furthermore, they have committed to publishing a formal asset-issuer playbook with minimum standards that is sure to be adopted and iterated on across the industry, leading to further due diligence by other lenders.

If this industry is to grow and absorb off-chain liquidity, security practises need to be tightened, standardised, and above all demanded. So far, Aave has shown a masterclass in both action and communication across this crisis, compounding this week off the back of the successful motion to vacate, with the judge ruling that the Arbitrum DAO can now transfer the rescued $71M to Defi United. Whilst the amount will still be held in restraint with Aave due to the court order, Arbitrum DAO will be absolved of all liability, and Aave has pledged to cover the $71M with borrowed funds whilst the case is ongoing.

Cerebras lists Thursday, 14 May: CBRS is the only market on TradeXYZ’s IPOP, so this is the first hard test of how tokenised pre-IPO derivatives price against the real underwriting at the venue. The price range has been bumped from $115-$125 to $150-$160 in the last week.

CLARITY Act markup, Thursday 14 May: The Senate Banking Committee markup is the next step for the stablecoin compromise we covered above. This likely needs a positive outcome to ensure it is signed into law this year.

Powell out, Warsh in, Friday 15 May: Powell’s term ends, and Kevin Warsh is expected to succeed him. He’ll arrive with the most crypto exposure of any Fed chair in history.

Anthropic transfer restrictions: Sunday’s bylaw update declares unauthorised transfers void rather than voidable. Monitor communications from secondary platforms affected by this update, as well as any volume shifts in synthetic versions.

See you next week.

Don’t forget to join our Telegram channel for the latest updates from Castle and all our research: Link here

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn’t guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.