Onchain Finance is now Competing on Execution: The Castle Chronicle

PLUS: SpaceX price discovery happens onchain, Morpho doubles down on token over equity, and native yield becomes possible for BTC with Stacks

The rate of progress in onchain markets has never been higher.

The largest stocks in the world are accessible onchain with deep liquidity, regulators are designing future policy with blockchains in mind, banks of all forms are accessing onchain yield and capital, and AMM designs are evolving to handle these new flows.

This week:

SpaceX ($SPCX) was traded pre-Nasdaq listing across a range of venues onchain not only opening access but accurately pricing the stock itself

The SEC revisited a two-decade-old debate about how trading venues compete, opening the door to AMMs

Aerodrome is preparing to flip the liquidity incentives that define the product to a forward-looking predictive mechanism

Morpho raised one of the biggest rounds DeFi has ever seen, with no equity involved

PropAMMs are rapidly improving in performance on Ethereum, but who actually provides users with the best executable price?

Stacks is giving native yield to BTC without it leaving the network

SpaceX goes live with onchain leading price discovery

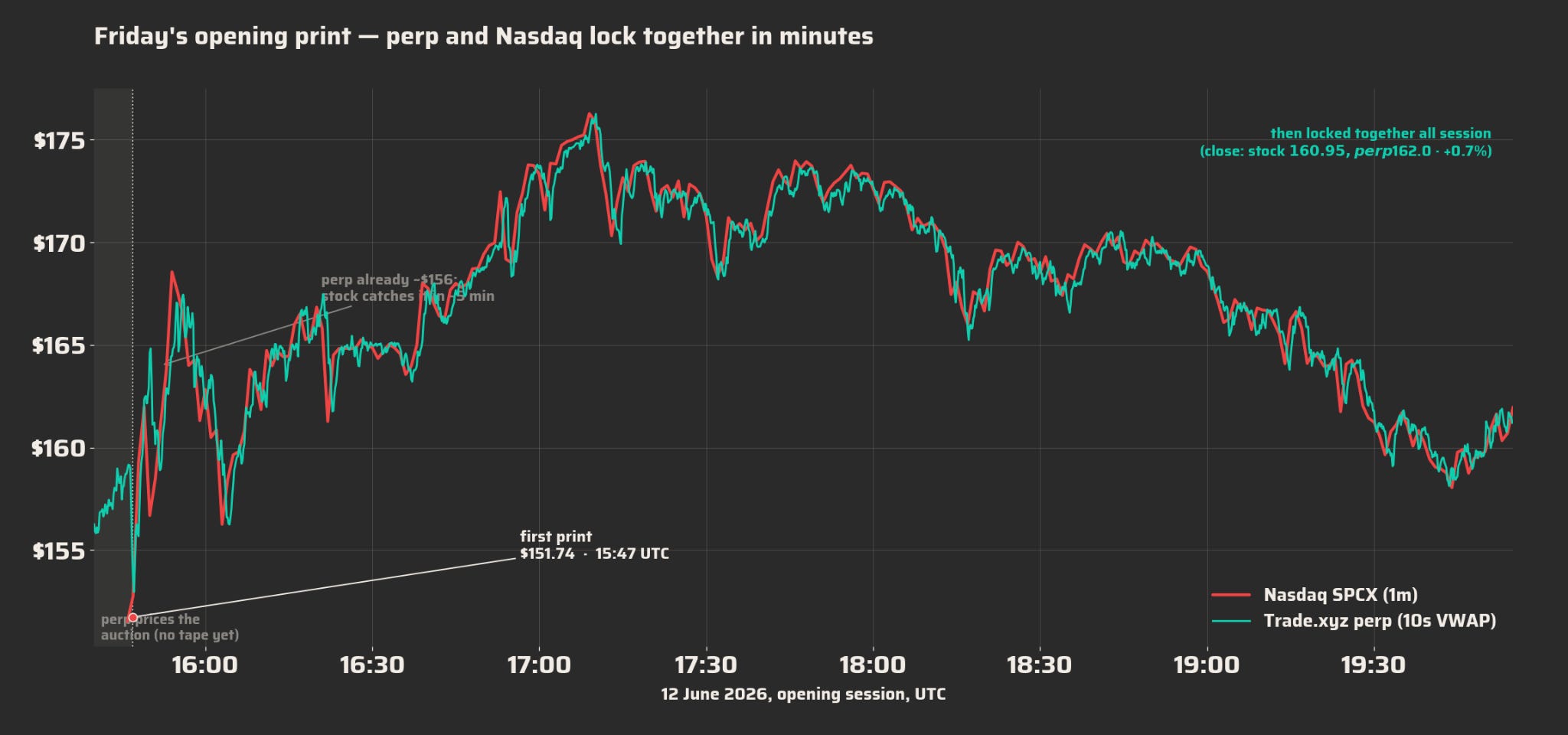

Last Friday, SPCX went live on Nasdaq, opening at $150 after an initial indication of $175. TradeXYZ and other perp venues called the lower price despite the higher indication, converging with Nasdaq after the print within minutes.

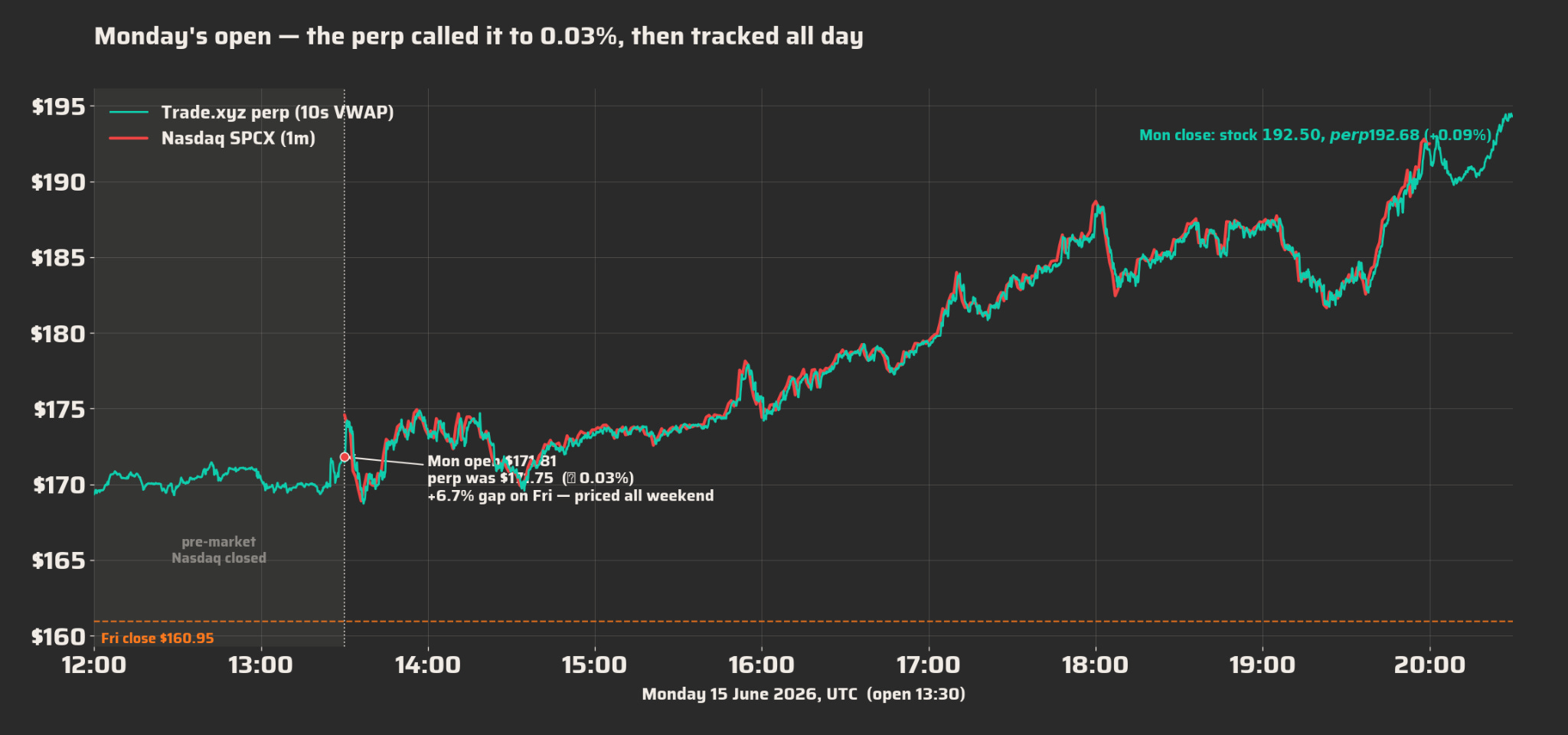

With the Nasdaq closed on weekends, onchain venues like TradeXYZ on Hyperliquid have an advantage: they are open 24/7, allowing access to directional traders and hedgers alike and attracting both the onchain and TradFi crowds. They are also getting better and better at predicting the Monday opens. xyz:SPCX sat at $171.75 on Monday morning when the Nasdaq opened at $171.81, a 0.03% deviation, all priced onchain.

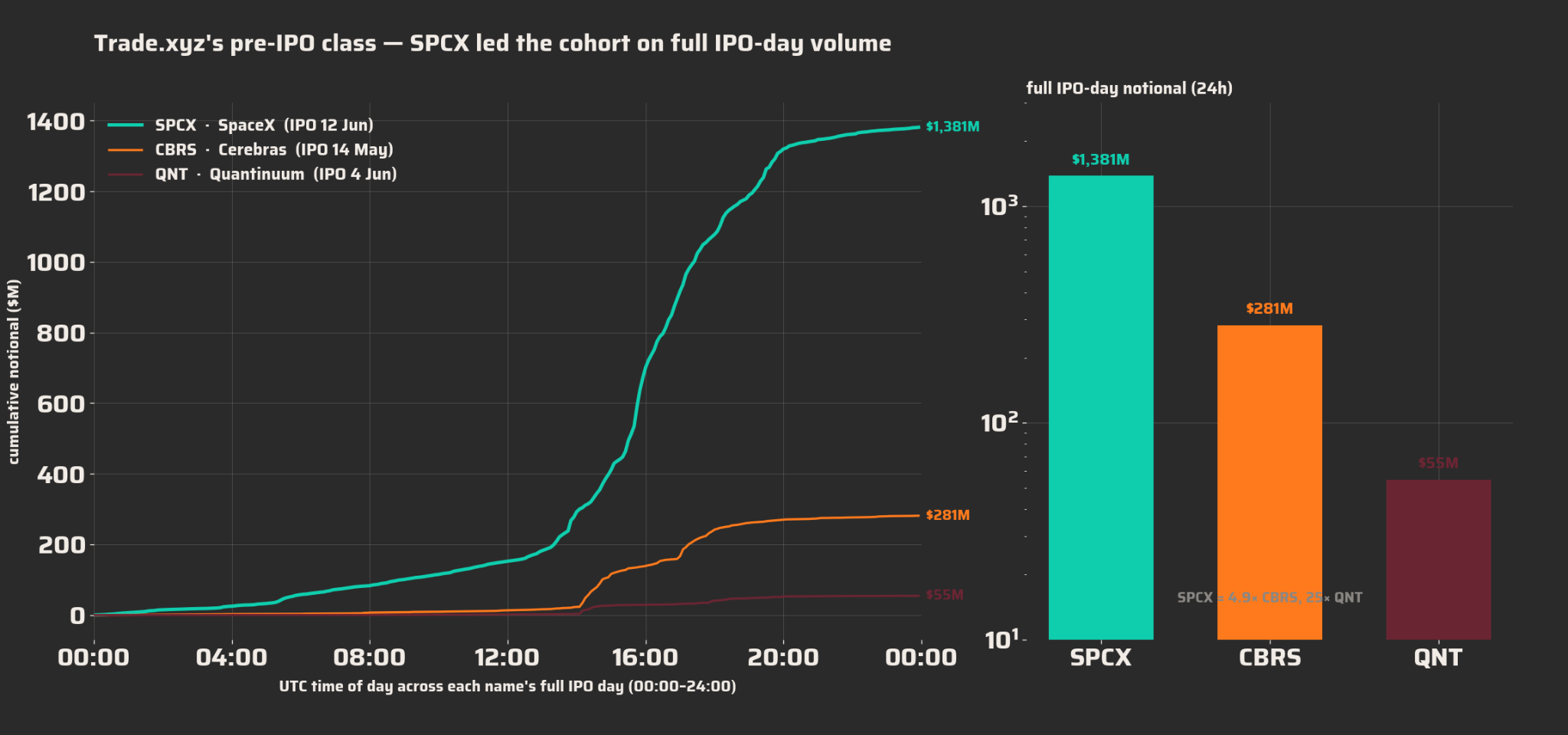

Across two prior Pre-IPO Perpetual (IPOP) markets, TradeXYZ tested its product methodology ahead of the largest IPO in history. xyz:SPCX set a new record for IPOPs, with $1.38B in volume on IPO day.

xyz:SPCX now ranks as the 3rd-highest-volume market on Hyperliquid (~$1.1B/24h), behind only BTC & ETH.

We pulled live order book data ahead of the opening print last Friday, which showed TradeXYZ had the largest open interest on SPCX with $315m, ahead of Binance’s $300m. Binance still led on 24h volume, but TradeXYZ’s depth, spread, and confidence in asset conversion make it the current leader in Pre-IPO trading - something almost no other venue can say when going head-to-head with a CEX heavyweight like Binance.

The SEC reopens equity trading rules after 20 years

The agency recently proposed rescinding Reg NMS Rules 611 and 610(e), which govern order protection and locked or crossed quotes in US equities. They essentially ensure users get the best price across exchanges.

That system assumes a certain kind of market: visible quotes, protected venues, and brokers routing between them. This way of doing things is at odds with onchain finance, which has evolved without these guardrails. For example, AMMs do not publish quotes in the same way exchanges do, so their automated, hard-coded pricing formulas cannot comply with such rules in the first place.

Now, the SEC is not rewriting equity rules specifically for onchain finance, but it is reopening a debate that will likely define how tokenised equities get to trade across exchanges, wrappers, perps, AMMs, solvers, and app-specific venues into the far future.

Aerodrome wants to make liquidity incentives predictive

Aerodrome has dominated as the leading DEX on Base over the years, pioneering the MetaDEX model, a ve(3,3) system where veAERO voters direct emissions toward liquidity pools, earning the fees and incentives attached to the pools they vote for. But now, according to WuBlockchain, Aerodrome will migrate to a predictive allocation mechanism that tries to anticipate where future demand will be.

Instead of directing incentives to high-volume and fee pools of the past, users will be rewarded for predicting the pools’ future performance.

Liquidity incentives are one of DeFi’s core products and have been key for bootstrapping and growing protocols across the industry. They ultimately decide where capital ends up, which pools gain depth, and which assets can be traded with size, especially on a protocol like Aerodrome.

The limitation is that liquidity incentives are mostly reactive, meaning capital often chases yesterday’s activity rather than tomorrow’s demand. If Aerodrome can make its incentives more forward-looking, it could improve the efficiency of liquidity allocation.

Morpho’s record-breaking raise with no equity in sight

Morpho’s $175m raise was not just one of the largest DeFi financings to date, it was a different kind of financing than we are used to, sparking wide discussion on token alignment, VCs, DAOs and more across socials.

The headline left much to the imagination, with few details about the valuation and no mention of tokens or equity. Morpho had previously committed to having only one asset, the MORPHO token, so people went digging for answers.

For those in tune with governance forums, Morpho DAO had approved a 150m MORPHO grant to the Morpho Association through MIP 131, giving the Association a token mandate to fund growth, partnerships, and institutional expansion. Whilst governance activity in Morpho DAO is extremely low, Morpho has shown a strong, tokenholder-aligned route to increase its distribution, growth, and runway.

This is a strong signal to the industry in support of token-first companies, at a time when investors are tired of equity taking the upper hand over tokenholders, who often feel ignored, overlooked, and exploited. If Morpho, one of the leading protocols in onchain finance can do it, why can’t others?

May this catalyse a renaissance in token-first principles and the structure of ownership in tokens over equity.

PropAMMs and the performance enhancement of Ethereum

For years, crypto market participants have had to choose between using a centralised exchange (CEX) to benefit from higher performance and operating onchain for accessibility, but at the expense of execution.

But propAMMs are changing the record.

“Permissionless blockchains have reached the point where the market structures built atop them can not only provide comparable execution to centralised exchanges (CEXs) but outcompete them entirely,” said Jump, one of the largest crypto market makers, in a recent article.

Instead of relying on passive AMM curves, propAMMs allow market makers to actively update prices, while swaps still settle onchain, giving onchain venues something they have historically lacked: tighter, more responsive pricing without sending the whole trade back to a centralised exchange, as some intent-based solutions attempted.

While the passive AMM model has its place, especially for longer-tail and less established assets, for core and in-demand pairs, execution matters, and liquidity and volume will flow and reside wherever this performance is highest.

For professional firms, institutional investors, and onchain strategies, a few % points of loss execution can make the difference between success and a strategy which cannot be leveraged in production.

So far, this has been a strong limitation of executing onchain, with those concerned about execution often resorting to operating on CEXs.

propAMMs have been live on Solana for some time because of the chain’s logic. Now the same is being done on Ethereum using offchain transactions.

This technology is only just getting started on Ethereum, but we can already see early success, with a spread 20 bps lower than its CEX counterparts for $1,000 orders on both ETH/USDT and ETH/USDC. While Binance still wins out for $10,000 trades and above, the issue is more with liquidity than anything technical. Most of this liquidity is currently allocated elsewhere, but as onchain execution improves, the incentives are to move it to where demand will be highest.

We believe this to be one of the most exciting onchain developments, especially for Ethereum.

Expect us to dive deeper into propAMMs and interview the most prominent builders in this vertical for you soon.

Stacks is trying to make BTC productive without leaving the chain

Over the last couple of years, since the launch of Bitcoin ETFs, BTC has become an increasingly institutionalised and legitimised asset.

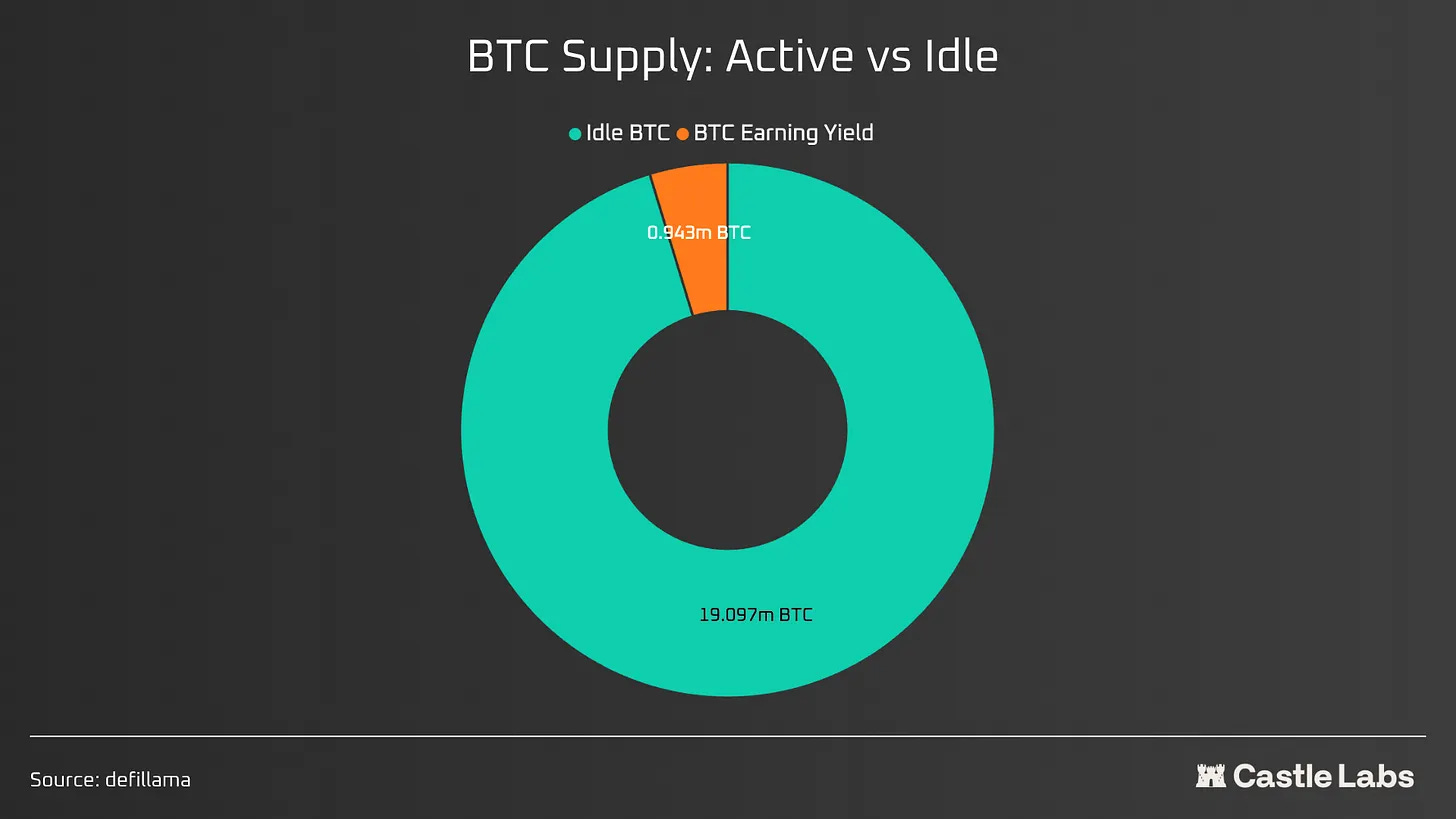

But far less development has occurred to put this capital to work effectively. In fact, over $1.4 trillion in BTC is currently sitting idle.

This idle BTC earns no yield, and the available options force trade-offs in custody, require wrapping, or require bridging BTC off the mainnet. Something conservative BTC holders would rather steer clear of.

Stacks’ Bitcoin Staking upgrade attempts to address this directly.

Rick Bartelink, Stacks CMO, states that: “BTC does not leave the L1, with the 5% in STX being the only L2 part you have to bond your BTC with.” They have ensured that BTC holders can earn native BTC yield while their coins remain on Bitcoin L1, without giving up custody or bridging assets.

Rick said Stacks’ research shows Bitcoin holders and institutions are far more accepting of having a “side option on different assets, as long as their BTC stays on the L1,” pointing to UTXO, the asset-management arm of Nakamoto, as an example.

“STX is the asset that secures the network.” By bonding BTC and STX, Stacks is trying to bootstrap Bitcoin liquidity into its ecosystem while positioning STX as “BTC’s beta asset” and “the rails of a Bitcoin economy.”

To ensure yield far out into the future, it’s clear that BTC Staking needs “a meaningful level of activity” for fees to become the main driver of the reward pool. That translates to liquid staking, STX surplus redeployment, Bitcoin holders becoming Stacks users, and more activity flowing into native apps.

The first liquid version will use a trust-minimised bridge, because “unilateral exit is a holy grail problem on Bitcoin no one has yet to solve.” Rick also noted that only Ethereum comes close to fee sustainability over time, while even Solana still relies predominantly on emissions.

Stacks has already demonstrated the power of its PoX model by distributing over 4200+ BTC to ecosystem participants since its launch in 2021. The latest update reinforces this with a stronger alignment with Bitcoin, a yield distributed in native BTC, and treasury companies like UTXO Management, the asset management arm of Nakamoto Inc., becoming inaugural participants in Bitcoin Staking on Stacks.

Read more about our coverage of Stacks here.

Hyperliquid HIP-4: Outcome markets have been live for several weeks now, with additional markets and trading volume increasing. With the World Cup now live and sportsbetting available on the platform, we’ll be watching how much market share the new venue can absorb from Polymarket and Kalshi

OpenAI and Anthropic Pre-IPOs: The success of SPCX is unlikely to be a one-off, with two more IPO giants still to come within the next year.

AI, robotics, and machine payments: With Tether’s latest investment in NEURA Robotics, we will be watching for early signs of demand for wallets, stablecoins, and programmable payment rails from autonomous machines and agents.

Don’t forget to join our Telegram channel for the latest updates from Castle and all our research: Link here

In our newsletter, we may discuss projects or tokens in which we hold positions. While we aim to provide informative content, our views are not financial advice. Please conduct your research and consult professionals before making investment decisions. Crypto markets are volatile, and past performance doesn’t guarantee future results. Invest responsibly, and be aware of the risks. Your capital is at risk, and we do not accept liability for any losses.